|

市場調查報告書

商品編碼

1913387

資料中心建置市場機會、成長要素、產業趨勢分析及2026年至2035年預測Data Center Construction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

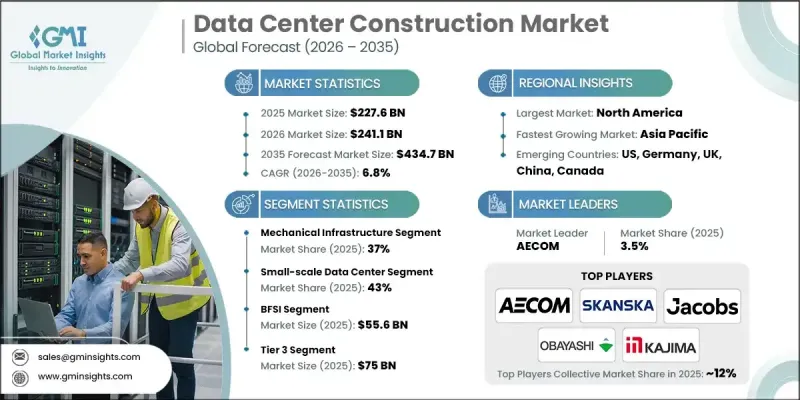

全球資料中心建設市場預計到 2025 年將達到 2,276 億美元,到 2035 年將達到 4,347 億美元,年複合成長率為 6.8%。

全球企業加速採用雲端服務交付模式是推動市場成長的主要動力。各組織機構正穩步將工作負載從本地基礎設施遷移到雲端,促使雲端服務供應商透過建造龐大的園區和區域設施來大幅提升容量。這種持續的需求推動了擴充性、標準化建設模式的不斷發展,這些模式支援快速部署和長期彈性。同時,高階運算工作負載日益成長的影響正在重塑設施需求,推動了對更高功率密度、先進冷卻解決方案和加固型電氣系統的需求。由數位化平台和企業轉型驅動的全球數據產生量不斷成長,進一步推動了對可靠處理和儲存容量的需求。此外,企業對共用基礎設施模式的日益依賴也推動了建設活動,因為企業越來越傾向於靈活的租賃安排,以降低資本密集度和營運負擔。這些趨勢共同推動了全球市場對現代化、高效且面向未來的資料中心設施的持續投資。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 2276億美元 |

| 預測金額 | 4347億美元 |

| 複合年成長率 | 6.8% |

預計到2025年,小規模資料中心市佔率將達到43%,並在2026年至2035年間以5%的複合年成長率成長。這些設施通常運作在低功耗範圍內,旨在支援區域營運、分散式運算需求和本地處理。隨著企業越來越重視反應速度和資料接近性,它們在分散式數位基礎設施中的作用也在不斷擴大。

2025年,銀行、金融服務和保險(BFSI)產業的市場規模預計將達到556億美元。金融機構需要高度安全、合規且具彈性的基礎設施,這推動了符合嚴格營運標準的設施的永續建設。監管要求和數據主權方面的考量正在推動該行業採用地域分散式發展策略。

美國資料中心建設市場預計到2025年將達到595億美元。大規模技術供應商的集中、先進的研究生態系統以及持續的基礎設施現代化,都為強勁的投資活動提供了支撐。美國在全球資料中心營運能力中佔據重要佔有率,預計到2030年將持續成長。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 系統平台提供者

- 硬體供應商

- 支付合作夥伴

- 利基專家

- 最終用途

- 成本結構

- 利潤率

- 每個階段的附加價值

- 影響供應鏈的因素

- 顛覆者

- 供應商情況

- 影響因素

- 促進要素

- 雲端運算的快速發展

- 人工智慧、機器學習和高效能運算的興起

- 數據生成和數位服務的激增

- 轉向託管和外包資料中心

- 產業潛在風險與挑戰

- 電力供應狀況和電網限制

- 建築和設備成本不斷上漲

- 關鍵設備的採購前置作業時間過長

- 市場機遇

- 擴展人工智慧賦能的高密度資料中心基礎設施

- 採用模組化和預製構件施工模式

- 整合現場發電和儲能解決方案

- 在電力資源豐富的次市場和新興市場開發資料中心

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- CCPA/CPRA(加州消費者隱私法案/加州隱私權法案)

- NERC CIP(北美電力可靠性委員會 - 關鍵基礎設施保護)

- 歐洲

- GDPR(一般資料保護規則)

- 2018年資料保護法(英國)

- 歐盟能源效率指令

- 氣候中和資料中心協議

- 國家網路安全局指令

- 亞太地區

- 2023年數位個人資料保護法(印度)

- 韓國個人資訊保護法

- 1979 年通訊(攔截與訪問)法(澳洲)

- 國內資料在地化與網路安全相關法規

- 拉丁美洲

- LGPD(Lei Geral de Protecao de Dados - 巴西)

- 阿根廷國家個人資料保護監管機構條例

- 墨西哥《關於保護私人企業所持有個人資料的聯邦法律》

- 中東和非洲

- PDPL(個人資料保護法 - 阿拉伯聯合大公國、沙烏地阿拉伯)

- 網路犯罪對策法

- 電子交易法(南非共和國)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 定價分析

- 依產品

- 按地區

- 成本細分分析

- 供應商成本結構

- 成本構成實施

- 持續營運成本

- 間接客戶成本

- 專利分析

- 經營模式分析

- 比較資本投資銷售模式與管理服務模式

- 收入來源

- 混合商業結構

- 案例研究

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 未來前景與機遇

- 電力供應狀況、電網限制及其對能源戰略的影響

- 人工智慧賦能的高密度基礎設施設計要求

- 模組化、預製化和可擴展的部署模式

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 資料中心市場估算與預測,2022-2035年

- 小規模資料中心

- 中型資料中心

- 大型資料中心

6. 2022-2035年基礎設施市場估算與預測

- 電力基礎設施

- 不斷電系統(UPS)

- 電源分配單元(PDU)

- 緊急發電機

- 其他

- 機械和設備

- 冷卻系統

- HVAC

- 電腦房空調機組(CRAC機組)

- 風扇陣列

- 空氣流量測量阻尼器

- DOAS

- 精密空調(PAC)機組

- 採用EC馬達的表面安裝式靜壓箱風扇

- 月有效用戶(MAU)

- ERV

- 冷凍水系統

- 阻尼器

- 冷凝器風扇

- 通風系統

- 直接通膨(DX)系統

- 其他

- 電腦房空調機組(CRAC機組)

- 架子

- 管道工程

- 架空地板

- 其他

- 網路基礎設施

- 其他

7. 依最終用途分類的市場估計與預測,2022-2035 年

- BFSI

- 能源

- 政府

- 衛生保健

- 製造業

- 資訊科技/通訊

- 媒體與娛樂

- 零售

- 其他

第8章 2022-2035年各層級市場估算與預測

- 一級

- 二級

- 三級

- 第四級

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 泰國

- 印尼

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Global leaders

- AECOM

- Jacobs

- Fluor

- Bechtel

- Skanska

- Samsung C&T

- Larsen &Toubro(L&T)

- Kajima

- Obayashi

- Balfour Beatty

- Turner Construction Company

- Mace

- NTT Facilities

- DSCO

- 本地公司

- Holder Construction

- Mortenson

- JE Dunn Construction

- Whiting-Turner Contracting Company

- HITT Contracting

- Clayco

- Hensel Phelps

- DPR Construction

- ISG plc

- 新興企業

- AirTrunk

- Vantage Data Centers

- ODATA(Ascenty/ODATA)

- GreenSquareDC

- STO Building

The Global Data Center Construction Market was valued at USD 227.6 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 434.7 billion by 2035.

Market growth is driven by the accelerating adoption of cloud-based delivery models across enterprises worldwide. Organizations are steadily shifting workloads away from in-house infrastructure, prompting cloud service providers to invest heavily in new capacity through large campuses and regional facilities. This sustained demand is encouraging the continuous development of scalable, standardized construction models that support rapid deployment and long-term resilience. At the same time, the rising influence of advanced computing workloads is reshaping facility requirements, increasing the need for higher power density, sophisticated cooling solutions, and reinforced electrical systems. Growth in global data creation from digital platforms and enterprise transformation is further elevating the requirement for reliable processing and storage capacity. Construction activity is also supported by increasing reliance on shared infrastructure models, as businesses favor flexible leasing arrangements to reduce capital intensity and operational burden. Together, these trends are driving steady investment in modern, efficient, and future-ready data center facilities across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $227.6 Billion |

| Forecast Value | $434.7 Billion |

| CAGR | 6.8% |

The small-scale data center segment accounted for 43% share in 2025 and is expected to grow at a CAGR of 5% between 2026 and 2035. These facilities typically operate within lower power capacity ranges and are designed to support regional operations, distributed computing needs, and localized processing. Their role within decentralized digital infrastructure continues to grow as organizations prioritize responsiveness and data proximity.

The BFSI segment generated USD 55.6 billion in 2025. Financial institutions require highly secure, compliant, and resilient infrastructure, driving sustained construction of facilities that meet stringent operational standards. Regulatory requirements and data sovereignty considerations support the adoption of geographically distributed development strategies within this segment.

U.S. Data Center Construction Market reached USD 59.5 billion in 2025. Strong investment activity is supported by the concentration of large technology providers, advanced research ecosystems, and ongoing infrastructure modernization. The country represents a significant share of global operational capacity, with continued expansion expected through 2030.

Key companies active in the Global Data Center Construction Market include Skanska, Turner & Townsend, AECOM, Jacobs Engineering, DPR Construction, NTT Facilities, Obayashi, Kaijima, Mace, and DSCO. Companies operating in the Global Data Center Construction Market are reinforcing their market position through strategic specialization, technological integration, and global expansion. Many firms are investing in expertise related to high-density and energy-efficient facility design to meet evolving workload requirements. Strategic partnerships with cloud providers and colocation operators help secure long-term project pipelines. Companies are also focusing on modular construction techniques to reduce build timelines and improve scalability. Geographic diversification allows firms to capture demand across emerging and established markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022-2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Data center

- 2.2.3 Infrastructure

- 2.2.4 End use

- 2.2.5 Tier

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 System & platform providers

- 3.1.1.2 Hardware suppliers

- 3.1.1.3 Payment partners

- 3.1.1.4 Niche specialists

- 3.1.1.5 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid growth in cloud computing

- 3.2.1.2 Proliferation of AI, machine learning, and high-performance computing

- 3.2.1.3 Explosion in data generation and digital services

- 3.2.1.4 Shift toward colocation and outsourced data centers

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Power availability and grid constraints

- 3.2.2.2 Rising construction and equipment costs

- 3.2.2.3 Long lead times for critical equipment

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of ai-ready and high-density data center infrastructure

- 3.2.3.2 Adoption of modular and prefabricated construction models

- 3.2.3.3 Integration of on-site power generation and energy storage solutions

- 3.2.3.4 Development of data centers in power-rich secondary and emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory Landscape

- 3.4.1 North America

- 3.4.1.1 CCPA / CPRA (California Consumer Privacy Act / California Privacy Rights Act)

- 3.4.1.2 NERC CIP (North American Electric Reliability Corporation - Critical Infrastructure Protection)

- 3.4.2 Europe

- 3.4.2.1 GDPR (General Data Protection Regulation)

- 3.4.2.2 Data Protection Act 2018 (UK)

- 3.4.2.3 EU Energy Efficiency Directive

- 3.4.2.4 Climate Neutral Data Centre Pact

- 3.4.2.5 National Cybersecurity Agency Directives

- 3.4.3 Asia Pacific

- 3.4.3.1 Digital Personal Data Protection Act 2023 (India)

- 3.4.3.2 PIPA (Personal Information Protection Act, South Korea)

- 3.4.3.3 Telecommunications (Interception and Access) Act 1979 (Australia)

- 3.4.3.4 National Data Localization and Cybersecurity Laws

- 3.4.4 Latin America

- 3.4.4.1 LGPD (Lei Geral de Protecao de Dados - Brazil)

- 3.4.4.2 National Directorate for Personal Data Protection Regulations (Argentina)

- 3.4.4.3 Federal Law on the Protection of Personal Data Held by Private Parties (Mexico)

- 3.4.5 Middle East & Africa

- 3.4.5.1 PDPL (Personal Data Protection Law - UAE, Saudi Arabia)

- 3.4.5.2 Anti-Cyber Crime Laws

- 3.4.5.3 Electronic Communications and Transactions Act (South Africa)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 By product

- 3.8.2 By region

- 3.9 Cost breakdown analysis

- 3.9.1 Vendor cost structure

- 3.9.2 Implementation of cost components

- 3.9.3 Ongoing operational costs

- 3.9.4 Indirect customer costs

- 3.10 Patent analysis

- 3.11 Business model analysis

- 3.11.1 Capex sale vs managed services models

- 3.11.2 Revenue streams

- 3.11.3 Hybrid commercial structures

- 3.12 Case studies

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Future outlook and opportunities

- 3.15 Power Availability, Grid Constraints & Energy Strategy Impact

- 3.16 AI-Ready & High-Density Infrastructure Design Requirements

- 3.17 Modular, Prefabricated & Scalable Deployment Models

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Data Center, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Small-scale data center

- 5.3 Medium data center

- 5.4 Large data center

Chapter 6 Market Estimates & Forecast, By Infrastructure, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Electrical infrastructure

- 6.2.1 UPS

- 6.2.2 Power distribution units (PDUs)

- 6.2.3 Backup generators

- 6.2.4 Others

- 6.3 Mechanical infrastructure

- 6.3.1 Cooling systems

- 6.3.2 Hvac

- 6.3.2.1 Computer room air conditioning (CRAC) units

- 6.3.2.1.1 Fan arrays

- 6.3.2.1.2 Air flow measurement damper

- 6.3.2.1.3 DOAS

- 6.3.2.2 Precision air conditioning (PAC) units

- 6.3.2.2.1 Face mounted plenum fan with EC motor

- 6.3.2.2.2 MAU

- 6.3.2.2.3 ERV

- 6.3.2.3 Chilled water systems

- 6.3.2.3.1 Dampers

- 6.3.2.3.2 Condenser fans

- 6.3.2.4 Ventilation systems

- 6.3.2.5 Direct expansion (DX) systems

- 6.3.2.6 Others

- 6.3.2.1 Computer room air conditioning (CRAC) units

- 6.3.3 Racks

- 6.3.4 Ductwork

- 6.3.5 Raised flooring

- 6.3.6 Others

- 6.4 Networking infrastructure

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 BFSI

- 7.3 Energy

- 7.4 Government

- 7.5 Healthcare

- 7.6 Manufacturing

- 7.7 IT & telecom

- 7.8 Media & entertainment

- 7.9 Retail

- 7.10 Others

Chapter 8 Market Estimates & Forecast, By Tier, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Tier 1

- 8.3 Tier 2

- 8.4 Tier 3

- 8.5 Tier 4

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Benelux

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Thailand

- 9.4.7 Indonesia

- 9.4.8 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Chile

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global leaders

- 10.1.1 AECOM

- 10.1.2 Jacobs

- 10.1.3 Fluor

- 10.1.4 Bechtel

- 10.1.5 Skanska

- 10.1.6 Samsung C&T

- 10.1.7 Larsen & Toubro (L&T)

- 10.1.8 Kajima

- 10.1.9 Obayashi

- 10.1.10 Balfour Beatty

- 10.1.11 Turner Construction Company

- 10.1.12 Mace

- 10.1.13 NTT Facilities

- 10.1.14 DSCO

- 10.2 Regional players

- 10.2.1 Holder Construction

- 10.2.2 Mortenson

- 10.2.3 JE Dunn Construction

- 10.2.4 Whiting-Turner Contracting Company

- 10.2.5 HITT Contracting

- 10.2.6 Clayco

- 10.2.7 Hensel Phelps

- 10.2.8 DPR Construction

- 10.2.9 ISG plc

- 10.3 Emerging players

- 10.3.1 AirTrunk

- 10.3.2 Vantage Data Centers

- 10.3.3 ODATA (Ascenty / ODATA)

- 10.3.4 GreenSquareDC

- 10.3.5 STO Building

資料中心建置市場:依資料中心類型、建設形式、等級、組件、建設服務類型及最終用戶產業分類-2026-2032年全球市場預測

資料中心建置市場:依資料中心類型、建設形式、等級、組件、建設服務類型及最終用戶產業分類-2026-2032年全球市場預測 2026年全球資料中心建置市場報告

2026年全球資料中心建置市場報告 資料中心建置市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材料類型、部署模式、最終用戶、設備

資料中心建置市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材料類型、部署模式、最終用戶、設備 資料中心建置市場規模、佔有率和趨勢分析報告:按基礎設施、層級、最終用途、地區和細分市場預測(2026-2033 年)

資料中心建置市場規模、佔有率和趨勢分析報告:按基礎設施、層級、最終用途、地區和細分市場預測(2026-2033 年) 2026-2030年全球資料中心建置市場

2026-2030年全球資料中心建置市場 新加坡資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

新加坡資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 資料中心建置市場報告:按建設類型、資料中心類型、等級標準、產業垂直領域和地區分類(2026-2034 年)

資料中心建置市場報告:按建設類型、資料中心類型、等級標準、產業垂直領域和地區分類(2026-2034 年) 資料中心建置市場-全球產業規模、佔有率、趨勢、機會及預測(依基礎設施類型、層級、資料中心規模、最終用戶產業、地區及競爭格局分類,2021-2031)資料中心機械設備建置市場(依組件類型、液冷系統、建置類型、等級及計劃類型分類)-2026-2032年全球預測拉丁美洲資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

資料中心建置市場-全球產業規模、佔有率、趨勢、機會及預測(依基礎設施類型、層級、資料中心規模、最終用戶產業、地區及競爭格局分類,2021-2031)資料中心機械設備建置市場(依組件類型、液冷系統、建置類型、等級及計劃類型分類)-2026-2032年全球預測拉丁美洲資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)