|

市場調查報告書

商品編碼

1892911

現場服務管理市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Field Service Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

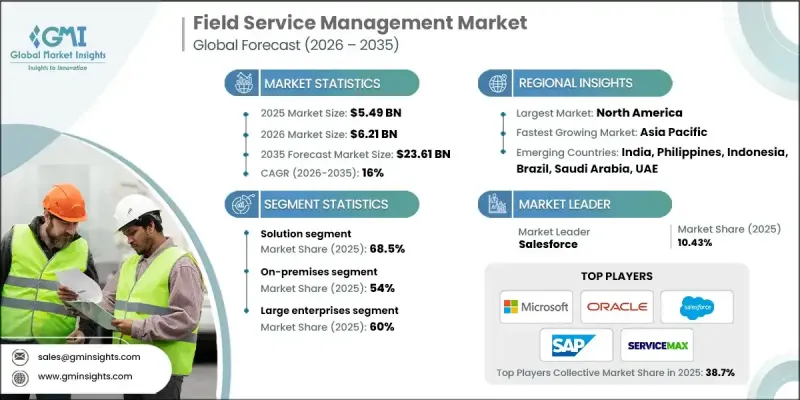

2025 年全球現場服務管理市場價值為 54.9 億美元,預計到 2035 年將以 16% 的複合年成長率成長至 236.1 億美元。

數位化優先營運、智慧勞動力自動化和互聯資產網路的快速普及正在重塑市場格局。現代現場服務管理 (FSM) 平台融合了行動勞動力管理應用、人工智慧驅動的調度引擎、物聯網賦能的資產診斷以及雲端原生服務編排。這些功能使企業能夠最大限度地減少停機時間、提高技術人員效率、提高首次修復率並增強客戶滿意度。公用事業、電信、醫療保健、製造業、暖通空調以及石油天然氣等行業正在積極採用 FSM,以滿足日益嚴格的服務期望、遵守安全法規並實現分散式現場營運的現代化。從人工紙本工作轉向預測性維護、數位化工作流程和自動化調度,正在推動 FSM 的廣泛應用。 FSM 供應商、物聯網供應商、ERP 公司和雲端超大規模雲端服務商之間的合作關係,建構了無縫現場營運、擴增實境支援、即時監控和低程式碼客製化的整合生態系統,從而提高了企業服務管理的效率和可擴展性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 54.9億美元 |

| 預測值 | 236.1億美元 |

| 複合年成長率 | 16% |

到了2025年,解決方案細分市場佔據68.5%的市場佔有率,預計到2035年將以15.5%的複合年成長率成長。企業越來越依賴綜合性的現場服務管理(FSM)平台來進行排班、工單管理、資產追蹤和技術人員績效監控。人工智慧、物聯網、GPS和自動化工具的整合使企業能夠消除低效環節、最佳化一次性修復率並高效擴展營運規模。公用事業、電信、醫療保健、能源和製造業等各行各業的組織都優先考慮統一的數位化解決方案,而不是分散或手動流程,這推動了FSM解決方案的持續成長。

到2025年,本地部署市場佔有率將達到54%,預計到2035年將以15.1%的複合年成長率成長。國防、醫療保健、公用事業、石油天然氣和製造業等管理敏感營運資料、關鍵資產和關鍵現場資訊的產業更傾向於部署本地現場服務管理(FSM)系統。這些系統能夠提供對伺服器的完全控制、可自訂的安全協定以及符合合規要求的治理。本地部署解決方案還能確保在低連線環境下不間斷地存取現場資料,同時最大限度地降低與第三方雲端漏洞相關的風險。

美國現場服務管理市場佔據85%的市場佔有率,預計2025年將達到18.1億美元。美國市場的成長主要得益於企業採用數位化平台來簡化營運、縮短服務回應時間並提升客戶體驗。 IT、電信、醫療保健和製造等行業的公司都在利用現場服務管理(FSM)工具來最佳化勞動力、即時追蹤技術人員並實現服務流程自動化。物聯網設備和預測性維護解決方案的普及進一步加速了對先進現場服務管理系統的需求。

目錄

第1章:方法論

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 設備複雜性增加,需要先進的現場服務解決方案。

- 預測性維護在各工業領域的應用日益普及。

- 對更快的服務解決速度和 SLA 合規性的需求激增。

- 公用事業、電信和製造業的數位轉型措施不斷增加。交通運輸解決方案

- 售後服務模式和長期維護合約的興起。

- 產業陷阱與挑戰

- 現有CRM或ERP系統的複雜性

- 熟練技術人員不足

- 市場機遇

- 人工智慧副駕駛和生成式人工智慧在現場自動化領域的應用激增。

- 物聯網連接資產安裝量的增加推動了預測性服務的發展機會。

- 遠端和自主維護工具的興起,包括無人機和擴增實境支援。

- 新興市場對經濟高效的雲端FSM解決方案的需求日益成長

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國:HIPAA(健康保險流通與責任法案)影響聯邦密克羅尼西亞聯邦對醫療保健服務就診中受保護健康資訊的處理。

- 加拿大:PIPEDA(個人資訊保護和電子文件法)規範了聯邦供應機構供應商對國家個人資料的處理。

- 歐洲

- 德國:BSI IT 安全法案 / BSI 指南,針對關鍵基礎設施和軟體供應商的國家網路安全規則。

- 英國:英國《一般資料保護規範》(GDPR) 和 2018 年《資料保護法》規範了英國脫歐後在英國營運的 FSM 供應商的資料使用和傳輸。

- 法國:GDPR(歐盟)/CNIL 指南(資料保護和地理定位)。

- 義大利:Testo Unico sulla Sicurezza sul Lavoro(職業安全法)

- 亞太地區

- 中國:網路安全法(網路產品/關鍵資訊基礎設施)

- 印度:《數位個人資料保護法》(2023 年)(及《資訊科技法》條款)

- 日本:《個人資訊保護法》(APPI)

- 澳洲:澳洲安全工作規範(工作場所和技術人員安全)

- 拉丁美洲

- 巴西:LGPD(Lei Geral de Protecao de Dados/通用資料保護法)

- 墨西哥:LFPDPPP(私人持有個人資料保護聯邦法)

- 阿根廷:省級電動計程車法規(布宜諾斯艾利斯)

- MEA

- 阿拉伯聯合大公國:聯邦法令第45號/個人資料保護法(PDPL)(以及杜拜國際金融中心/阿布達比全球市場資料規則)

- 沙烏地阿拉伯:國家網路安全局/SASO 標準和工作場所安全規則

- 南非:《個人資訊保護法》(POPIA)

- 北美洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利分析

- 永續性和環境影響分析

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 未來展望與機遇

- 技術路線圖和演進時間表

- 新興應用機會

- 投資需求及資金來源

- 風險評估與緩解策略

- 針對市場參與者的策略建議

- 用例

- 最佳情況

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估算與預測:依組件分類,2022-2035年

- 解決方案

- 移動現場執行

- 服務合約管理

- 保固管理

- 勞動力管理

- 客戶管理

- 庫存管理

- 其他

- 服務

- 執行

- 培訓與支援

- 諮詢顧問

第6章:市場估算與預測:依部署模式分類,2022-2035年

- 現場

- 雲

第7章:市場估計與預測:依產業垂直領域分類,2022-2035年

- 能源與公用事業

- 資訊科技和電信

- 製造業

- 衛生保健

- 金融服務業

- 運輸與物流

- 零售與電子商務

- 其他

第8章:市場估算與預測:依企業規模分類,2022-2035年

- 中小企業

- 大型企業

第9章:市場估算與預測:依應用領域分類,2022-2035年

- 工單管理

- 合約管理

- 移動勞動力管理

- 資產管理

- 車隊監控

- 其他

第10章:市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 菲律賓

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 全球參與者

- Salesforce

- Microsoft

- SAP

- Oracle

- IFS

- ServiceMax (PCT)

- Trimble

- Accruent

- 區域玩家

- Zinier

- KloudGin

- Zuper

- FieldAware

- Praxedo

- simPRO

- OverIT

- ProntoForms

- 新興參與者

- FieldEZ Technologies

- Jobber

- Housecall

- ServicePower

The Global Field Service Management Market was valued at USD 5.49 billion in 2025 and is estimated to grow at a CAGR of 16% to reach USD 23.61 billion by 2035.

The market is reshaped by the rapid adoption of digital-first operations, intelligent workforce automation, and connected asset networks. Modern FSM platforms now combine mobile workforce management apps, AI-driven scheduling engines, IoT-enabled asset diagnostics, and cloud-native service orchestration. These capabilities enable companies to minimize downtime, boost technician efficiency, improve first-time fix rates, and elevate customer satisfaction. Sectors such as utilities, telecom, healthcare, manufacturing, HVAC, and oil & gas are embracing FSM to meet stricter service expectations, comply with safety regulations, and modernize decentralized field operations. The shift away from manual paperwork toward predictive maintenance, digital workflows, and automated dispatching is driving strong adoption. Collaborative partnerships between FSM providers, IoT vendors, ERP firms, and cloud hyperscalers create integrated ecosystems for seamless field operations, augmented reality support, real-time monitoring, and low-code customization, making enterprise service management more efficient and scalable.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.49 Billion |

| Forecast Value | $23.61 Billion |

| CAGR | 16% |

The solution segment held 68.5% share in 2025 and is expected to grow at a CAGR of 15.5% through 2035. Businesses increasingly rely on comprehensive FSM platforms for scheduling, work order management, asset tracking, and technician performance monitoring. Integration of AI, IoT, GPS, and automation tools enables companies to eliminate inefficiencies, optimize first-time fixes, and scale operations efficiently. Organizations across utilities, telecom, healthcare, energy, and manufacturing prioritize unified digital solutions over fragmented or manual processes, fueling sustained growth in FSM solutions adoption.

The on-premises segment held a 54% share in 2025 and is projected to grow at a CAGR of 15.1% through 2035. Industries that manage sensitive operational data, critical assets, and mission-critical field information, such as defense, healthcare, utilities, oil & gas, and manufacturing, prefer on-premises FSM deployments. These systems offer complete control over servers, customizable security protocols, and compliance-aligned governance. On-premises solutions also ensure uninterrupted access to field data in low-connectivity environments while minimizing risks associated with third-party cloud vulnerabilities.

US Field Service Management Market held an 85% share, generating USD 1.81 billion in 2025. Growth in the US market is fueled by enterprises adopting digital platforms to streamline operations, reduce service response times, and enhance customer experiences. Companies across IT, telecom, healthcare, and manufacturing leverage FSM tools for workforce optimization, real-time technician tracking, and automated service processes. The expansion of IoT devices and predictive maintenance solutions further accelerates the need for advanced field service management systems.

Major companies operating in the Global Field Service Management Market include Salesforce, SAP, Microsoft, Oracle, IFS, Jobber, Zinier, ServiceMax, Trimble, and Housecall. To strengthen their foothold in the Field Service Management Market, companies are investing in advanced digital solutions that integrate AI, IoT, and cloud capabilities to optimize field operations. They are expanding platform functionalities to include predictive maintenance, augmented reality support, and real-time analytics to improve technician productivity and first-time fix rates. Strategic partnerships with IoT manufacturers, ERP providers, and cloud service vendors enable the creation of interoperable ecosystems for seamless workflow automation. Firms are also focusing on on-premises deployments for data-sensitive clients and offering flexible subscription-based models to attract SMEs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Enterprise Size

- 2.2.4 Deployment Mode

- 2.2.5 Industry Vertical

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in equipment complexity requiring advanced field service solutions.

- 3.2.1.2 Rise in predictive maintenance adoption across industrial sectors.

- 3.2.1.3 Surge in demand for faster service resolution and SLA compliance.

- 3.2.1.4 Increase in digital transformation initiatives in utilities, telecom, and manufacturing. transportation solutions

- 3.2.1.5 Rise in after-sales service models and long-term maintenance contracts.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexities in the existing CRM or ERP systems

- 3.2.2.2 Insufficient skilled technicians

- 3.2.3 Market opportunities

- 3.2.3.1 Surge in adoption of AI copilots and generative AI for field automation.

- 3.2.3.2 Increase in IoT-connected asset installations driving predictive service opportunities.

- 3.2.3.3 Rise in remote and autonomous maintenance tools, including drones and AR support.

- 3.2.3.4 Growing demand for cost-effective cloud FSM solutions in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US: HIPAA (Health Insurance Portability & Accountability Act) impacts FSM handling of protected health information for healthcare service visits.

- 3.4.1.2 Canada: PIPEDA (Personal Information Protection and Electronic Documents Act) governs national personal data processing by FSM vendors.

- 3.4.2 Europe

- 3.4.2.1 Germany: BSI IT Security Act / BSI-Guidelines national cybersecurity rules for critical infrastructure and software vendors.

- 3.4.2.2 UK: UK GDPR & Data Protection Act 2018 governs data use and transfer post-Brexit for FSM providers operating in the UK

- 3.4.2.3 France: GDPR (EU) / CNIL guidance (data protection & geolocation).

- 3.4.2.4 Italy: Testo Unico sulla Sicurezza sul Lavoro (occupational safety law)

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Cybersecurity Law (network products / critical information infrastructure)

- 3.4.3.2 India: DPDP Act / Digital Personal Data Protection Act (2023) (and IT Act provisions)

- 3.4.3.3 Japan: APPI (Act on the Protection of Personal Information)

- 3.4.3.4 Australia: Safe Work Australia codes (workplace & technician safety)

- 3.4.4 Latin America

- 3.4.4.1 Brazil: LGPD (Lei Geral de Protecao de Dados / General Data Protection Law)

- 3.4.4.2 Mexico: LFPDPPP (Federal Law on Protection of Personal Data Held by Private Parties)

- 3.4.4.3 Argentina: Provincial EV Taxi Regulations (Buenos Aires)

- 3.4.5 MEA

- 3.4.5.1 UAE: Federal Decree-Law No. 45 / Personal Data Protection Law (PDPL) (and DIFC/ADGM data rules)

- 3.4.5.2 Saudi Arabia: National Cybersecurity Authority / SASO standards and workplace safety rules

- 3.4.5.3 South Africa: POPIA (Protection of Personal Information Act)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability and environmental impact analysis

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Future outlook & opportunities

- 3.10.1 Technology roadmap & evolution timeline

- 3.10.2 Emerging application opportunities

- 3.10.3 Investment requirements & funding sources

- 3.10.4 Risk assessment & mitigation strategies

- 3.10.5 Strategic recommendations for market participants

- 3.11 Use cases

- 3.12 Best-case scenario

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Mobile field execution

- 5.2.2 Service contract management

- 5.2.3 Warranty management

- 5.2.4 Workforce management

- 5.2.5 Customer management

- 5.2.6 Inventory management

- 5.2.7 Others

- 5.3 Services

- 5.3.1 Implementation

- 5.3.2 Training & support

- 5.3.3 Consulting & advisory

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Industry Vertical, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Energy & utilities

- 7.3 IT and Telecom

- 7.4 Manufacturing

- 7.5 Healthcare

- 7.6 BFSI

- 7.7 Transportation & logistics

- 7.8 Retail and E-commerce

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large Enterprises

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Work Order Management

- 9.3 Contract Management

- 9.4 Mobile Workforce Management

- 9.5 Asset Management

- 9.6 Fleet Monitoring

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Salesforce

- 11.1.2 Microsoft

- 11.1.3 SAP

- 11.1.4 Oracle

- 11.1.5 IFS

- 11.1.6 ServiceMax (PCT)

- 11.1.7 Trimble

- 11.1.8 Accruent

- 11.2 Regional Players

- 11.2.1 Zinier

- 11.2.2 KloudGin

- 11.2.3 Zuper

- 11.2.4 FieldAware

- 11.2.5 Praxedo

- 11.2.6 simPRO

- 11.2.7 OverIT

- 11.2.8 ProntoForms

- 11.3 Emerging Players

- 11.3.1 FieldEZ Technologies

- 11.3.2 Jobber

- 11.3.3 Housecall

- 11.3.4 ServicePower

現場服務管理市場:按組件、應用、最終用戶產業、部署類型和組織規模分類-2026-2032年全球市場預測

現場服務管理市場:按組件、應用、最終用戶產業、部署類型和組織規模分類-2026-2032年全球市場預測 2026年全球現場服務管理解決方案市場報告

2026年全球現場服務管理解決方案市場報告 2026-2030年全球現場服務管理(FSM)軟體市場2026年全球現場服務管理市場報告

2026-2030年全球現場服務管理(FSM)軟體市場2026年全球現場服務管理市場報告 現場服務管理市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類

現場服務管理市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類 全球現場服務管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球現場服務管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 現場服務管理市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、部署模式、公司規模、產業垂直領域、地區和競爭格局分類,2021-2031 年)

現場服務管理市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、部署模式、公司規模、產業垂直領域、地區和競爭格局分類,2021-2031 年) 現場服務管理 (FSM) 市場規模、佔有率和成長分析(按軟體和服務類型、部署類型和地區分類)—2026-2033 年行業預測

現場服務管理 (FSM) 市場規模、佔有率和成長分析(按軟體和服務類型、部署類型和地區分類)—2026-2033 年行業預測 現場服務管理市場依產品、部署模式、組織規模、產業及地區分類-預測至2030年

現場服務管理市場依產品、部署模式、組織規模、產業及地區分類-預測至2030年 全球 NOC 即服務市場(按服務類型、支援模式和行業垂直分類)- 預測至 2030 年

全球 NOC 即服務市場(按服務類型、支援模式和行業垂直分類)- 預測至 2030 年