|

市場調查報告書

商品編碼

1892689

再生原料化學品市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Renewable Feedstock Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

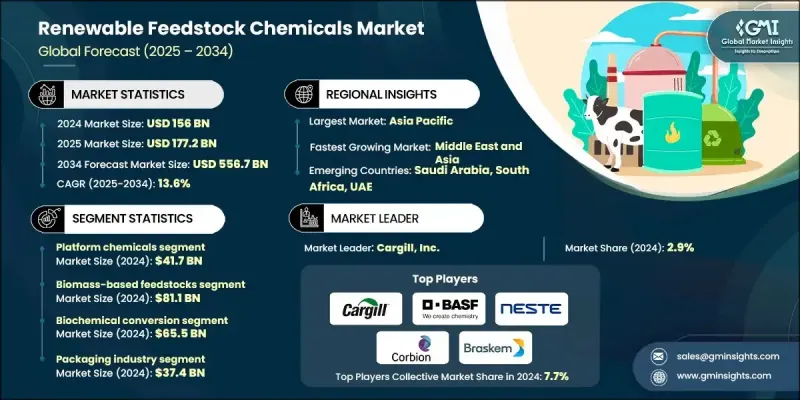

2024年全球再生原料化學品市場價值為1,560億美元,預計2034年將以13.6%的複合年成長率成長至5,567億美元。

再生原料化學品源自永續的非化石資源,包括生質能、農業殘餘物、有機廢棄物和生物基中間體。與傳統的石油化學產品不同,這些化學品旨在降低碳足跡、促進資源高效生產並滿足全球永續發展要求。生物技術、生物化學和熱化學轉化方法的創新顯著推動了市場發展,其中酶轉化、精準發酵、氣化和廢物製化學品技術提高了產量和原料多樣性。包裝、汽車、建築、紡織和消費品等行業的需求不斷成長,正在加速其應用。企業正擴大將可直接替代的生物基材料整合到現有生產線中,以在不中斷營運的情況下減少排放。強力的監管支持、企業對環境、社會和治理(ESG)的承諾以及消費者對綠色產品的偏好轉變,正在進一步推動市場成長,並塑造向循環工業價值鏈的轉型。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1560億美元 |

| 預測值 | 5567億美元 |

| 複合年成長率 | 13.6% |

平台化學品市場規模預計在2024年達到417億美元,是許多下游生物基化學產品的關鍵組成部分。有利於永續材料的法規正在加速生物聚合物和樹脂在包裝領域的應用。再生塑膠生產效率的提高和成熟途徑的建立,提升了生物基芳烴、烯烴、二醇和二羧酸在生物聚酯和高附加價值材料生產中的重要性。

2024年,生化轉化領域創造了655億美元的產值,凸顯了其在利用發酵和酶促途徑從生質能生產高價值化學品方面的重要作用。熱化學轉化因其能夠利用多種原料生產合成氣、生物油和先進燃料而日益受到關注。化學轉化技術能夠實現精確的分子轉化,進而提高產品產率和性能。

2024年,美國再生原料化學品市場規模達566億美元,引領北美市場成長。該地區受益於雄心勃勃的永續發展目標、向生物基材料的產業轉型、有利的法規以及企業脫碳措施。聯邦政府的激勵措施、私營部門對生物聚合物、再生中間體和負碳製程日益成長的需求,正使美國成為北美市場擴張的關鍵驅動力。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 生物基聚合物和替代化學品的應用日益廣泛

- 生物化學和熱化學技術的進步

- 擴大廢棄物和殘渣原料的供應

- 產業陷阱與挑戰

- 高昂的生產成本限制了競爭力

- 產品品質不穩定

- 市場機遇

- 與循環經濟解決方案的整合

- 特種生物基化學品的開發

- 利用數位化可追溯性打造高階產品

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 平台化學品

- 醇類

- 乙醇(生物乙醇、纖維素乙醇)

- 甲醇(生物甲醇)

- 丁醇(生物丁醇)

- 有機酸

- 乳酸

- 琥珀酸

- 檸檬酸

- 衣康酸

- 甘油和多元醇

- 甘油(丙三醇)

- 山梨醇

- 木糖醇

- 醇類

- 生物聚合物和樹脂

- 可生物分解聚合物

- 聚乳酸(PLA)

- 聚羥基脂肪酸酯(PHA)

- 澱粉基聚合物

- 即插即用的生物聚合物

- 生物基聚乙烯(Bio-PE、Bio-HDPE、Bio-LDPE)

- 生物基聚對苯二甲酸乙二酯(Bio-PET)

- 生物基乙烯-醋酸乙烯酯共聚物(Bio-EVA)

- 生物基芳烴和烯烴

- 芳烴(BTX)

- 生物苯

- 生物甲苯

- 生物二甲苯(Bio-PX)

- 木質素中的芳香物質

- 烯烴

- 生物乙烯

- 生物丙烯

- 可生物分解聚合物

- 二醇和二元酸

- 二醇

- 單乙二醇(生物-MEG)

- 丙二醇(1,2-丙二醇)

- 1,3-丙二醇

- 1,4-丁二醇(Bio-BDO)

- 異山梨醇

- 二元酸

- 呋喃二甲酸(FDCA)

- 己二酸

- 癸二酸

- 壬二酸

- 二醇

- 脂肪酸及其衍生物

- 脂肪酸

- 脂肪酸衍生物

- 二聚體脂肪酸

- 脂肪醇

- 脂肪酸酯(FAME、FAEE)

- 特種化學品

- 生物溶劑

- 界面活性劑

- 用於聚氨酯的多元醇

- 潤滑劑

- 生物中間體

- 液態生物中間體(生物原油、生物油)

- 氣態生物中間體(合成氣、沼氣)

- 固體/半固體生物中間體(醣類、遊離脂肪酸、乳酸)

第6章:市場估算與預測:依原料類型分類,2021-2034年

- 生質原料

- 農業原料

- 澱粉作物(玉米、高粱、大麥)

- 糖料作物(甘蔗、甜菜、甜高粱)

- 油料作物(大豆、油菜籽、亞麻薺、棕櫚)

- 農業殘餘物

- 玉米秸稈

- 小麥秸稈

- 甘蔗渣和糖蜜

- 森林來源原料

- 伐木殘餘物

- 磨坊殘渣(鋸屑、樹皮、黑液)

- 專用能源作物

- 柳枝稷和芒草

- 短輪伐期木本作物

- 藻類和海洋生質能

- 農業原料

- 廢棄物衍生原料

- 城市生活垃圾和有機垃圾(生活垃圾、食物垃圾)

- 工業廢棄物(廢食用油、牛油、蒸餾油)

- 農業及動物廢棄物(糞便、墊料)

- 沼氣(垃圾掩埋場、沼氣池)

- 再生碳原料

- 機械回收

- 化學回收(熱解、氣化)

- 捕獲的碳原料

- 大氣/直接空氣捕獲(DAC)

- 工業點源(煙氣、廢氣)

- 生物源二氧化碳(發酵、厭氧消化)

第7章:市場估計與預測:依轉換技術分類,2021-2034年

- 生化轉化

- 發酵(酒精發酵、乳酸發酵、高級發酵)

- 酵素水解

- 厭氧消化

- 熱化學轉化

- 氣化

- 熱解(快速、慢速)

- 熱催化轉化(BioTCat)

- 化學轉化

- 酯交換反應

- 加氫處理/加氫處理

- 費托合成

- 脫水

- 甲醇制烯烴/芳烴(MTO/MTA)

- 電化學及碳捕集與利用工藝

- 電解(可再生氫氣生產)

- 二氧化碳電化學還原

- 二氧化碳與氫氣的合成

- 機械和物理過程

- 機械回收

- 化學回收

第8章:市場估算與預測:依最終用途產業分類,2021-2034年

- 包裝產業

- 汽車產業

- 紡織服裝業

- 建築業

- 食品飲料業

- 製藥和醫療保健產業

- 個人護理和化妝品行業

- 油漆和塗料行業

- 農業產業

- 化工

- 電子業

- 石油和天然氣產業

第9章:市場估計與預測:依地區分類,2021-2034年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- Amyris, Inc.

- Axens

- Avantium NV

- BASF SE

- Braskem SA

- Cargill, Incorporated

- Corbion NV

- Covation Bio

- dsm-firmenich

- Genomatica, Inc.

- India Glycols Limited

- NatureWorks LLC

- Neste Corporation

- Novamont SpA

- Qore - Cargill/HELM Joint Venture

- Roquette

- Toray Industries

- UPM Biochemicals

The Global Renewable Feedstock Chemicals Market was valued at USD 156 billion in 2024 and is estimated to grow at a CAGR of 13.6% to reach USD 556.7 billion by 2034.

Renewable feedstock chemicals are derived from sustainable, non-fossil sources, including biomass, agricultural residues, organic waste, and bio-based intermediates. Unlike conventional petrochemical products, these chemicals are designed to lower carbon footprints, promote resource-efficient production, and meet global sustainability mandates. Innovations in biotechnological, biochemical, and thermochemical conversion methods have significantly boosted the market, with enzymatic conversion, precision fermentation, gasification, and waste-to-chemicals technologies enhancing yield and feedstock diversity. Rising demand from industries such as packaging, automotive, construction, textiles, and consumer goods is accelerating adoption. Companies are increasingly integrating drop-in bio-based materials into existing production lines to reduce emissions without operational disruption. Strong regulatory support, corporate ESG commitments, and shifting consumer preferences toward green products are further driving market growth and shaping the transition toward circular industrial value chains.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $156 Billion |

| Forecast Value | $556.7 Billion |

| CAGR | 13.6% |

The platform chemicals segment accounted for USD 41.7 billion in 2024, acting as essential building blocks for a wide range of downstream bio-based chemical products. Regulations favoring sustainable materials are accelerating the adoption of biopolymers and resins for packaging applications. Improved production efficiency and established pathways for renewable plastics have elevated the importance of bio-based aromatics, olefins, diols, and dicarboxylic acids in bio-polyester and value-added material production.

The biochemical conversion segment generated USD 65.5 billion in 2024, highlighting its role in producing high-value chemicals from biomass using fermentation and enzymatic pathways. Thermochemical conversion is gaining traction for its versatility in producing syngas, bio-oils, and advanced fuels from diverse feedstocks. Chemical conversion techniques enable precise molecular transformations, boosting product yield and performance.

U.S. Renewable Feedstock Chemicals Market accounted for USD 56.6 billion in 2024, leading North America's growth. The region benefits from ambitious sustainability targets, industrial transitions to bio-based materials, supportive regulations, and corporate decarbonization initiatives. Federal incentives, rising private-sector demand for biopolymers, renewable intermediates, and carbon-negative processes are positioning the U.S. as a key driver of market expansion in North America.

Major players operating in the Global Renewable Feedstock Chemicals Market include Amyris, Inc., Axens, Avantium N.V., BASF SE, Braskem S.A., Cargill, Incorporated, Corbion N.V., Covation Bio, DSM-Firmenich, Genomatica, Inc., India Glycols Limited, NatureWorks LLC, Neste Corporation, Novamont S.p.A., Qore (Cargill/HELM Joint Venture), Roquette, Toray Industries, and UPM Biochemicals. Companies in the Global Renewable Feedstock Chemicals Market are adopting strategies such as expanding production capacity, investing in R&D for novel feedstocks and conversion technologies, and forming strategic alliances to broaden distribution networks. They focus on developing drop-in bio-based alternatives compatible with existing infrastructure, enhancing product portfolio diversification, and emphasizing regulatory compliance and sustainability certifications. Firms are leveraging circular economy principles, optimizing process efficiencies, and utilizing digital solutions for supply chain traceability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Feedstock Type

- 2.2.3 Conversion Technology

- 2.2.4 End use Industry

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of bio-based polymers & drop-in chemicals

- 3.2.1.2 Advancements in biochemical & thermochemical technologies

- 3.2.1.3 Expanding availability of waste & residue feedstocks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs limit competitiveness

- 3.2.2.2 Inconsistent product quality

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with circular economy solutions

- 3.2.3.2 Development of specialty bio-based chemicals

- 3.2.3.3 Leveraging digital traceability for premium products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Platform chemicals

- 5.2.1 Alcohols

- 5.2.1.1 Ethanol (bioethanol, cellulosic ethanol)

- 5.2.1.2 Methanol (bio-methanol)

- 5.2.1.3 Butanol (bio-butanol)

- 5.2.2 Organic acids

- 5.2.2.1 Lactic acid

- 5.2.2.2 Succinic acid

- 5.2.2.3 Citric acid

- 5.2.2.4 Itaconic acid

- 5.2.3 Glycerol & polyols

- 5.2.3.1 Glycerol (glycerin)

- 5.2.3.2 Sorbitol

- 5.2.3.3 Xylitol

- 5.2.1 Alcohols

- 5.3 Biopolymers & resins

- 5.3.1 Biodegradable polymers

- 5.3.1.1 Polylactic acid (PLA)

- 5.3.1.2 Polyhydroxyalkanoates (PHA)

- 5.3.1.3 Starch-based polymers

- 5.3.2 Drop-in biopolymers

- 5.3.2.1 Bio-polyethylene (Bio-PE, Bio-HDPE, Bio-LDPE)

- 5.3.2.2 Bio-polyethylene terephthalate (Bio-PET)

- 5.3.2.3 Bio-ethylene vinyl acetate (Bio-EVA)

- 5.3.2.4 Bio-based aromatics & olefins

- 5.3.3 Aromatics (BTX)

- 5.3.3.1 Bio-benzene

- 5.3.3.2 Bio-toluene

- 5.3.3.3 Bio-xylene (Bio-PX)

- 5.3.3.4 Aromatics from lignin

- 5.3.4 Olefins

- 5.3.4.1 Bio-ethylene

- 5.3.4.2 Bio-propylene

- 5.3.1 Biodegradable polymers

- 5.4 Diols & diacids

- 5.4.1 Diols

- 5.4.1.1 Monoethylene glycol (Bio-MEG)

- 5.4.1.2 propylene glycol (1,2-propanediol)

- 5.4.1.3 1,3-propanediol

- 5.4.1.4 1,4-butanediol (Bio-BDO)

- 5.4.1.5 Isosorbide

- 5.4.2 Diacids

- 5.4.2.1 Furandicarboxylic acid (FDCA)

- 5.4.2.2 Adipic acid

- 5.4.2.3 Sebacic acid

- 5.4.2.4 Azelaic acid

- 5.4.1 Diols

- 5.5 Fatty acids & derivatives

- 5.5.1 Fatty acids

- 5.5.2 Fatty acid derivatives

- 5.5.2.1 Dimer fatty acids

- 5.5.2.2 Fatty alcohols

- 5.5.2.3 Fatty acid esters (FAME, FAEE)

- 5.6 Specialty chemicals

- 5.6.1 Bio-solvents

- 5.6.2 Surfactants

- 5.6.3 Polyols for polyurethanes

- 5.6.4 Lubricants

- 5.7 Biointermediates

- 5.7.1 Liquid biointermediates (Biocrude, Bio-oil)

- 5.7.2 Gaseous biointermediates (Syngas, Biogas)

- 5.7.3 Solid/Semi-solid biointermediates (Sugars, FFA, Lactide)

Chapter 6 Market Estimates and Forecast, By Feedstock Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Biomass-based feedstocks

- 6.2.1 Agricultural feedstocks

- 6.2.1.1 Starch crops (Corn, Grain Sorghum, Barley)

- 6.2.1.2 Sugar crops (Sugarcane, Sugar Beets, Sweet Sorghum)

- 6.2.1.3 Oil crops (Soybean, Canola, Camelina, Palm)

- 6.2.2 Agricultural residues

- 6.2.2.1 Corn stover

- 6.2.2.2 Wheat straw

- 6.2.2.3 Bagasse & molasses

- 6.2.3 Forest-derived feedstocks

- 6.2.3.1 Logging residues

- 6.2.3.2 Mill residues (Sawdust, Bark, Black Liquor)

- 6.2.4 Dedicated energy crops

- 6.2.4.1 Switchgrass & miscanthus

- 6.2.4.2 Short-rotation woody crops

- 6.2.4.3 Algae & marine biomass

- 6.2.1 Agricultural feedstocks

- 6.3 Waste-derived feedstocks

- 6.3.1 Municipal & organic waste (MSW, Food Waste)

- 6.3.2 Industrial waste (UCO, Tallow, Distillers Oils)

- 6.3.3 Agricultural & animal waste (Manure, Litter)

- 6.3.4 Biogas (Landfill, Digesters)

- 6.4 Recycled carbon feedstocks

- 6.4.1 Mechanical recycling

- 6.4.2 Chemical recycling (pyrolysis, gasification)

- 6.5 Captured carbon feedstocks

- 6.5.1 Atmospheric/Direct air capture (DAC)

- 6.5.2 Industrial point sources (Flue Gases, Off-Gases)

- 6.5.3 Biogenic CO2 (Fermentation, Anaerobic Digestion)

Chapter 7 Market Estimates and Forecast, By Conversion Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Biochemical conversion

- 7.2.1 Fermentation (Alcoholic, Lactic Acid, Advanced)

- 7.2.2 Enzymatic hydrolysis

- 7.2.3 Anaerobic digestion

- 7.3 Thermochemical conversion

- 7.3.1 Gasification

- 7.3.2 Pyrolysis (Fast, Slow)

- 7.3.3 Thermocatalytic conversion (BioTCat)

- 7.4 Chemical conversion

- 7.4.1 Transesterification

- 7.4.2 Hydrotreatment/hydrotreating

- 7.4.3 Fischer-tropsch synthesis

- 7.4.4 Dehydration

- 7.4.5 Methanol-to-olefins/Aromatics (MTO/MTA)

- 7.5 Electrochemical & CCU Processes

- 7.5.1 Electrolysis (Renewable hydrogen production)

- 7.5.2 Co2 electrochemical reduction

- 7.5.3 Co2 + h2 synthesis

- 7.6 Mechanical & physical processes

- 7.6.1 Mechanical recycling

- 7.6.2 Chemical recycling

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Packaging industry

- 8.3 Automotive industry

- 8.4 Textile & apparel industry

- 8.5 Construction industry

- 8.6 Food & beverage industry

- 8.7 Pharmaceuticals & healthcare industry

- 8.8 Personal care & cosmetics industry

- 8.9 Paints & coatings industry

- 8.10 Agriculture industry

- 8.11 Chemical industry

- 8.12 Electronics industry

- 8.13 Oil & gas industry

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Amyris, Inc.

- 10.2 Axens

- 10.3 Avantium N.V.

- 10.4 BASF SE

- 10.5 Braskem S.A.

- 10.6 Cargill, Incorporated

- 10.7 Corbion N.V.

- 10.8 Covation Bio

- 10.9 dsm-firmenich

- 10.10 Genomatica, Inc.

- 10.11 India Glycols Limited

- 10.12 NatureWorks LLC

- 10.13 Neste Corporation

- 10.14 Novamont S.p.A.

- 10.15 Qore - Cargill/HELM Joint Venture

- 10.16 Roquette

- 10.17 Toray Industries

- 10.18 UPM Biochemicals

環保建設化學品市場預測至2034年:按產品類型、技術、應用和地區分類的全球分析全球可再生原料化學品市場預測(至2034年):依原料類型、化學品類型、最終用戶及地區分類全球永續特種化學品市場預測(至2032年):依產品種類、原料、應用及地區分類

環保建設化學品市場預測至2034年:按產品類型、技術、應用和地區分類的全球分析全球可再生原料化學品市場預測(至2034年):依原料類型、化學品類型、最終用戶及地區分類全球永續特種化學品市場預測(至2032年):依產品種類、原料、應用及地區分類 永續化學品市場-全球產業規模、佔有率、趨勢、機會和預測,依產品、應用、地區和競爭格局分類,2020-2030年預測

永續化學品市場-全球產業規模、佔有率、趨勢、機會和預測,依產品、應用、地區和競爭格局分類,2020-2030年預測 永續建築化學品市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)全球生物基和永續性原料市場:預測(至2032年)-按產品類型、原料類型、技術、應用和地區分類的分析永續造紙化學品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

永續建築化學品市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)全球生物基和永續性原料市場:預測(至2032年)-按產品類型、原料類型、技術、應用和地區分類的分析永續造紙化學品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 永續化學品用下一代原料市場:按產品、應用、地區和國家的分析和預測(2025-2034年)

永續化學品用下一代原料市場:按產品、應用、地區和國家的分析和預測(2025-2034年) 永續的化學原料的全球市場(2025年~2035年)

永續的化學原料的全球市場(2025年~2035年) 全球永續化學品市場(2025-2035)

全球永續化學品市場(2025-2035)