|

市場調查報告書

商品編碼

1885891

發酵衍生蛋白市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Fermentation-Derived Proteins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

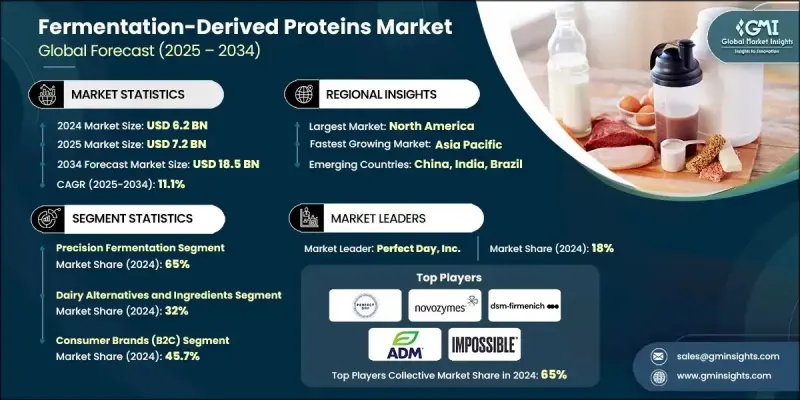

2024 年全球發酵衍生蛋白質市場價值為 62 億美元,預計到 2034 年將以 11.1% 的複合年成長率成長至 185 億美元。

隨著氣候壓力加劇,食品業加速擺脫傳統畜牧業,整個蛋白質格局正日益向發酵系統轉型。隨著企業擴大生產規模,生產出能夠複製乳製品、肉類和蛋類蛋白特性的替代品,發酵技術的商業應用迅速擴展。投資流入鞏固了Quorn、Impossible Foods和Perfect Day等領先創新者的市場地位,而包括ADM和DSM-Firmenich在內的全球主要食品集團也深化了合作,以提高產業整合度。包括減少溫室氣體排放和提高土地利用效率在內的永續性議題推動了這項轉型,2021年後發表的研究不斷證明,與傳統畜牧系統相比,發酵蛋白具有環境優勢。公眾對抗生素使用和人畜共患病風險的討論,進一步激發了人們對發酵技術的興趣,將其視為氣候和糧食安全政策規劃中的一項戰略組成部分。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 62億美元 |

| 預測值 | 185億美元 |

| 複合年成長率 | 11.1% |

到了2024年,精準發酵領域佔據65%的市場佔有率,預計到2034年將以10.9%的複合年成長率成長。企業依靠精準發酵、生質能發酵和傳統發酵平台來開發高功能性蛋白質,這些蛋白質能夠提供必要的起泡、凝膠和熔化特性。這些成分被尋求清潔標籤配方、改善質地、感官性能和營養價值的消費品公司所採用。

2024年,乳製品替代品和配料應用領域佔據32%的市場佔有率,預計到2034年將以8.6%的複合年成長率成長。發酵衍生的配料在飲料、烘焙食品、肉類替代品和乳製品替代品等品類中,其性能可與動物性蛋白質媲美甚至超越動物性蛋白質。品牌將這些蛋白質融入產品中,以改善口感、增強乳化效果、簡化成分錶並滿足監管標準,尤其是在醬料、冷凍甜點和即飲配方等產品中。

2024年北美發酵蛋白市場規模為23億美元,預計2034年將達69億美元。該地區受益於強大的研發基礎設施、早期商業化途徑、強勁的風險投資活動以及開放的分銷網路,這些都加速了替代乳製品、雞蛋和肉類產品的普及。

全球發酵蛋白市場的主要活躍企業包括:The Better Meat Co.、ADM(Archer Daniels Midland)、奇華頓(Givaudan)、杜邦(IFF)、Solar Foods Oy、Perfect Day, Inc.、TurtleTree Labs、Quorn Foods、Kerry Group、Standing Ovation、諾維信A/S)、帝斯曼-菲美意(DSM-Firmenich)、嘉吉(Cargill)、Calysta、Onego Bio、Impossible Foods Inc.、Nature's Fynd、Formo、EVERY Company 和 Corbion。這些企業正透過積極擴張產能、產品多元化以及與大型食品飲料生產商建立長期合作關係來鞏固其競爭地位。許多企業正在開發專有發酵菌株,以提高產量、降低成本並創造差異化的功能性蛋白質。與原料供應商和消費品品牌進行策略合作,有助於加速配方推廣,同時增強供應鏈的穩定性。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 對永續、不含動物成分的蛋白質解決方案的需求日益成長

- 精準發酵和菌株工程技術的進展

- 與全球食品飲料企業建立策略夥伴關係

- 產業陷阱與挑戰

- 高生產力和資本支出要求

- 監管不確定性和核准流程緩慢

- 市場機遇

- 企業環境與ESG承諾的改善

- 新興市場和應用中的未開發潛力

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按來源

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依發酵製程分類,2021-2034年

- 主要趨勢

- 精準發酵

- 乳蛋白

- 雞蛋蛋白

- 功能性和特殊性蛋白質

- 風味和香氣蛋白/化合物

- 生質能發酵

- 真菌蛋白

- 酵母或細菌基生質能

- 利用氣體或非常規原料製備單細胞蛋白

- 傳統/混合發酵

- 發酵植物蛋白基質

- 利用動物或植物原料進行混合發酵

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 乳製品替代品和配料

- 雞蛋替代品和功能性雞蛋成分

- 肉類和海鮮替代品

- 麵包店、糖果店和甜點店

- 飲料和營養產品

- 食品服務及工業原料

第7章:市場估計與預測:依配銷通路分類,2021-2034年

- 主要趨勢

- 消費品牌(B2C)

- 原料配方供應商(B2B)

- 合約研發生產組織(CDMO)

- 飼料和寵物食品製造商

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Perfect Day, Inc.

- The EVERY Company

- Impossible Foods Inc.

- Nature's Fynd

- The Better Meat Co.

- Solar Foods Oy

- TurtleTree Labs

- Formo

- Onego Bio

- Standing Ovation

- Quorn Foods

- Givaudan (including Naturals & Ingredients)

- Novozymes A/S

- ADM (Archer Daniels Midland)

- DSM-Firmenich

- Kerry Group

- Cargill

- Corbion

- DuPont (IFF)

- Calysta

The Global Fermentation-Derived Proteins Market was valued at USD 6.2 billion in 2024 and is estimated to grow at a CAGR of 11.1% to reach USD 18.5 billion by 2034.

The broader protein landscape is increasingly shifting toward fermentation-based systems as climate pressures intensify and the food sector accelerates its move away from conventional animal agriculture. Commercial adoption of fermentation technologies has expanded rapidly as companies scale production of alternatives that replicate the characteristics of dairy, meat, and egg proteins. Investment inflows have strengthened the market presence of leading innovators such as Quorn, Impossible Foods, and Perfect Day, while major global food groups-including ADM and DSM-Firmenich have deepened collaboration to improve industrial integration. Sustainability concerns, including greenhouse gas reduction and land-use efficiency, have supported the transition, as research published after 2021 consistently demonstrates the environmental advantages of fermentation-derived proteins compared to traditional livestock systems. Public conversations about antibiotic use and zoonotic risks have driven further interest in fermentation technologies as a strategic component in climate and food-security policy planning.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.2 Billion |

| Forecast Value | $18.5 Billion |

| CAGR | 11.1% |

The precision fermentation segment held a 65% share in 2024 and is estimated to grow at a CAGR of 10.9% through 2034. Companies rely on precision, biomass, and traditional fermentation platforms to develop highly functional proteins that provide essential foaming, gelling, and melting characteristics. These ingredients are adopted by consumer product firms seeking clean-label reformulations with improved texture, sensory performance, and nutritional value.

The dairy alternatives and ingredient applications segment accounted for a 32% share in 2024 and is expected to grow at an 8.6% CAGR toward 2034. Fermentation-derived ingredients can match or exceed the performance of animal-based proteins across categories such as beverages, baked goods, meat substitutes, and dairy alternatives. Brands integrate these proteins into products to enhance mouthfeel, strengthen emulsification, simplify ingredient lists, and meet regulatory standards, especially in items like sauces, frozen desserts, and ready-to-drink formulations.

North America Fermentation-Derived Proteins Market generated USD 2.3 billion in 2024 and is forecast to reach USD 6.9 billion by 2034. The region benefits from strong R&D infrastructure, early commercialization pathways, robust venture capital activity, and receptive distribution networks that accelerate adoption across alternative dairy, egg, and meat products.

Key companies active in the Global Fermentation-Derived Proteins Market include The Better Meat Co., ADM (Archer Daniels Midland), Givaudan, DuPont (IFF), Solar Foods Oy, Perfect Day, Inc., TurtleTree Labs, Quorn Foods, Kerry Group, Standing Ovation, Novozymes A/S, DSM-Firmenich, Cargill, Calysta, Onego Bio, Impossible Foods Inc., Nature's Fynd, Formo, EVERY Company, and Corbion. Companies in the Fermentation-Derived Proteins Market are strengthening their competitive position through aggressive capacity expansion, product diversification, and long-term partnerships with major food and beverage manufacturers. Many are developing proprietary fermentation strains to improve yield, reduce cost, and create differentiated functional proteins. Strategic collaborations with ingredient suppliers and CPG brands help accelerate formulation adoption while reinforcing supply chain stability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fermentation Process

- 2.2.3 Application

- 2.2.4 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for sustainable, animal-free protein solutions

- 3.2.1.2 Advances in precision fermentation and strain engineering

- 3.2.1.3 Strategic partnerships with global food and beverage players

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and capital expenditure requirements

- 3.2.2.2 Regulatory uncertainty and slow approval pathways

- 3.2.3 Market opportunities

- 3.2.3.1 Rising corporate climate and ESG commitments

- 3.2.3.2 Untapped potential in emerging markets and applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Source

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Fermentation Process, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Precision fermentation

- 5.2.1 Dairy proteins

- 5.2.2 Egg proteins

- 5.2.3 Functional and specialty proteins

- 5.2.4 Flavor and aroma proteins/compounds

- 5.3 Biomass fermentation

- 5.3.1 Mycoprotein

- 5.3.2 Yeast- or bacterial-based biomass

- 5.3.3 Single-cell protein from gases or unconventional feedstocks

- 5.3.4 Traditional / mixed fermentation

- 5.3.5 Fermented plant-based protein matrices

- 5.3.6 Hybrid fermentation with animal or plant inputs

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy alternatives and ingredients

- 6.3 Egg alternatives and functional egg ingredients

- 6.4 Meat and seafood alternatives

- 6.5 Bakery, confectionery, and desserts

- 6.6 Beverages and nutrition products

- 6.7 Food service and industrial ingredients

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Consumer brands (B2C)

- 7.3 Ingredient and formulation suppliers (B2B)

- 7.4 Contract development and manufacturing organizations (CDMOs)

- 7.5 Feed and pet food manufacturers

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Perfect Day, Inc.

- 9.2 The EVERY Company

- 9.3 Impossible Foods Inc.

- 9.4 Nature’s Fynd

- 9.5 The Better Meat Co.

- 9.6 Solar Foods Oy

- 9.7 TurtleTree Labs

- 9.8 Formo

- 9.9 Onego Bio

- 9.10 Standing Ovation

- 9.11 Quorn Foods

- 9.12 Givaudan (including Naturals & Ingredients)

- 9.13 Novozymes A/S

- 9.14 ADM (Archer Daniels Midland)

- 9.15 DSM-Firmenich

- 9.16 Kerry Group

- 9.17 Cargill

- 9.18 Corbion

- 9.19 DuPont (IFF)

- 9.20 Calysta