|

市場調查報告書

商品編碼

1876798

抗體藥物偶聯物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Antibody Drug Conjugates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

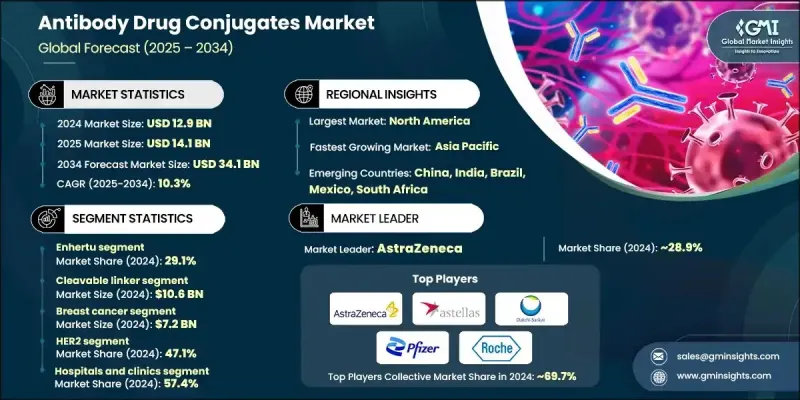

2024 年全球抗體藥物偶聯物市場價值為 129 億美元,預計到 2034 年將以 10.3% 的複合年成長率成長至 341 億美元。

在全球範圍內,包括血液癌、乳癌、尿路上皮癌和膀胱癌在內的多種癌症發生率不斷上升,推動了市場擴張。日益加重的癌症負擔使得人們迫切需要更精準、更有效的治療方法,抗體藥物偶聯物(ADC)已成為現代腫瘤治療的關鍵組成部分。抗體藥物偶聯物將標靶治療與化療結合,能夠將強效細胞毒性藥物直接遞送至癌細胞,同時保護健康組織。這些療法利用化學連接子將單株抗體與高效藥物連接起來,確保細胞毒性藥物能夠特異性地與腫瘤細胞上的抗原結合,從而提高治療效果並減少對周圍組織的損傷。隨著癌症發生率的上升,尤其是在老齡化人口和新興市場,預計抗體藥物偶聯物的應用將會加速。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 129億美元 |

| 預測值 | 341億美元 |

| 複合年成長率 | 10.3% |

Enhertu業務部門佔29.1%的市場佔有率,2024年估值達38億美元。其廣泛的治療應用涵蓋多種癌症類型,包括HER2陽性和HER2低表達腫瘤,擴大了患者群體,使其在與其他抗體偶聯藥物(ADC)的競爭中脫穎而出。臨床試驗結果顯示,該藥物具有較高的緩解率和顯著改善患者總存活期的療效,因此受到腫瘤科醫師的廣泛認可。

2024年,可裂解連接子片段的市場規模達到106億美元,預計將以10.2%的複合年成長率成長。可裂解連接子能夠特異性地在腫瘤微環境中釋放細胞毒性藥物,而這種釋放過程由酵素、pH值變化或氧化還原條件觸發。這種標靶釋放方式能夠最大限度地殺傷腫瘤細胞,同時最大限度地減少對健康組織的損傷,從而使可裂解連接子抗體藥物偶聯物(ADC)相比不可裂解型ADC具有明顯的臨床優勢。

預計到2024年,北美抗體藥物偶聯物(ADC)市佔率將達到42.1%。該地區受益於完善的醫療基礎設施、龐大的癌症患者群體以及眾多提供先進腫瘤治療方案的領先企業。強勁的研發投入、有利的監管環境以及對創新療法的早期應用,都為新型ADC產品的快速上市和市場推廣提供了有力支撐。

全球抗體藥物偶聯物(ADC)市場的主要參與者包括艾伯維(AbbVie)、安斯泰來(Astellas Pharma)、ADC Therapeutics、阿斯特捷利康(AstraZeneca)、第一三共(Daiichi Sankyo)、吉利德(Gilead)、葛蘭素史克(GSKizer)、ImmunoGen、PRochefizer(PRochefizer)。這些公司正透過大力投資研發,不斷發現針對多種癌症類型的新型ADC候選藥物,並提高臨床療效,鞏固其市場地位。與生物技術公司和學術機構的策略合作有助於加速創新並簡化法規核准流程。此外,各公司也正在擴大產能,以確保全球及時供應,並進軍新興市場以拓展新的病患群體。利用精準的行銷活動、臨床試驗資料以及腫瘤科醫師的教育項目,可以有效促進產品的推廣應用。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 癌症發生率上升

- 對基於抗體的癌症療法的需求日益成長

- 抗體技術的不斷進步

- 擴大抗體偶聯藥物(ADC)的核准範圍

- 產業陷阱與挑戰

- 高昂的研發和製造成本

- 與抗體藥物偶聯物 (ADC) 相關的安全性和毒性問題

- 市場機遇

- 擴散至實體腫瘤

- 採用下一代ADC技術

- 成長促進因素

- 成長潛力分析

- 監管環境

- 技術格局

- 當前技術趨勢

- 新興技術

- 管道分析

- 全球癌症統計數據

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 恩赫爾圖

- 卡德西拉

- 阿德塞特里斯

- 帕德切夫

- 特羅德爾維

- 波利維

- 其他產品類型

第6章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 可裂解連接子

- 不可切割的連接子

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 乳癌

- 血癌

- 淋巴瘤

- 白血病

- 多發骨髓瘤

- 尿路上皮癌和膀胱癌

- 其他應用

第8章:市場估算與預測:依目標類型分類,2021-2034年

- 主要趨勢

- HER2

- CD30

- CD22

- 其他目標類型

第9章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院和診所

- 腫瘤中心

- 其他最終用途

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- AbbVie

- ADC Therapeutics

- Astellas Pharma

- AstraZeneca

- Daiichi Sankyo

- Gilead

- GSK

- ImmunoGen

- Pfizer

- Roche

The Global Antibody Drug Conjugates Market was valued at USD 12.9 billion in 2024 and is estimated to grow at a CAGR of 10.3% to reach USD 34.1 billion by 2034.

Market expansion is driven by the rising prevalence of various cancers, including blood, breast, urothelial, and bladder cancers worldwide. The increasing cancer burden is creating urgent demand for more precise and effective therapies, making ADCs a critical component of modern oncology treatment. Antibody drug conjugates combine targeted therapy with chemotherapy, delivering potent cytotoxic agents directly to cancer cells while sparing healthy tissues. These therapies use monoclonal antibodies linked to highly potent drugs through chemical linkers, ensuring that the cytotoxic agent binds specifically to antigens on tumor cells, which enhances treatment efficacy and reduces collateral damage. As cancer rates rise, particularly in aging populations and emerging markets, the adoption of ADCs is expected to accelerate.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.9 Billion |

| Forecast Value | $34.1 Billion |

| CAGR | 10.3% |

The Enhertu segment held a 29.1% share, valued at USD 3.8 billion in 2024. Its broad therapeutic application across multiple cancer types, including HER2-positive and HER2-low tumors, has expanded the patient pool, providing a competitive advantage over other ADCs. Clinical trial results demonstrate high response rates and improved overall survival, contributing to its strong adoption among oncologists.

The cleavable linker segment generated USD 10.6 billion in 2024 and is projected to grow at a CAGR of 10.2%. Cleavable linkers release the cytotoxic drug specifically within the tumor microenvironment, triggered by enzymes, pH changes, or redox conditions. This targeted release maximizes tumor cell destruction while minimizing damage to healthy tissues, giving cleavable linker ADCs a clear clinical advantage over non-cleavable variants.

North America Antibody Drug Conjugates Market held a 42.1% share in 2024. The region benefits from a well-established healthcare infrastructure, a large cancer patient population, and the presence of leading players offering advanced oncology treatments. Strong R&D investments, favorable regulatory frameworks, and early adoption of innovative therapies support the rapid introduction and uptake of new ADC products.

Key players operating in the Global Antibody Drug Conjugates Market include AbbVie, Astellas Pharma, ADC Therapeutics, AstraZeneca, Daiichi Sankyo, Gilead, GSK, ImmunoGen, Pfizer, and Roche. Companies in the Antibody Drug Conjugates Market are strengthening their foothold by investing heavily in research and development to discover new ADC candidates targeting multiple cancer types and improving clinical efficacy. Strategic collaborations with biotech firms and academic institutions help accelerate innovation and streamline regulatory approvals. Firms are also expanding manufacturing capacity to ensure timely global supply and entering emerging markets to capture new patient populations. Leveraging targeted marketing campaigns, clinical trial data, and educational programs for oncologists enhances product adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 Target type trends

- 2.2.6 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer

- 3.2.1.2 Growing demand for antibody-based cancer therapies

- 3.2.1.3 Increasing advancements in antibody technology

- 3.2.1.4 Expanding approval of ADCs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and manufacturing costs

- 3.2.2.2 Safety and toxicity concerns associated with ADCs

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into solid tumors

- 3.2.3.2 Adoption of next-generation ADC technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Global cancer statistics

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Enhertu

- 5.3 Kadcyla

- 5.4 Adcetris

- 5.5 Padcev

- 5.6 Trodelvy

- 5.7 Polivy

- 5.8 Other product types

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cleavable linker

- 6.3 Non-cleavable linker

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Breast cancer

- 7.3 Blood cancer

- 7.3.1 Lymphoma

- 7.3.2 Leukemia

- 7.3.3 Multiple myeloma

- 7.4 Urothelial cancer and bladder cancer

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By Target Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 HER2

- 8.3 CD30

- 8.4 CD22

- 8.5 Other target types

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Oncology centers

- 9.4 Other End Use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 ADC Therapeutics

- 11.3 Astellas Pharma

- 11.4 AstraZeneca

- 11.5 Daiichi Sankyo

- 11.6 Gilead

- 11.7 GSK

- 11.8 ImmunoGen

- 11.9 Pfizer

- 11.10 Roche

聯合抗體療法市場:按適應症、產品類型、治療方法、治療方法、最終用戶和分銷管道分類-2026-2032年全球預測

聯合抗體療法市場:按適應症、產品類型、治療方法、治療方法、最終用戶和分銷管道分類-2026-2032年全球預測 抗體藥物複合體(ADC)市場規模、佔有率和成長分析:按產品、標靶、技術、應用和地區分類-2026-2033年產業預測

抗體藥物複合體(ADC)市場規模、佔有率和成長分析:按產品、標靶、技術、應用和地區分類-2026-2033年產業預測 ADC技術市場分析及預測至2035年:依類型、產品類型、服務、技術、組件、應用、製程、最終用戶、裝置、階段分類抗體藥物複合體(ADC) 市場分析及預測至 2035 年:按類型、產品類型、服務、技術、應用、最終用戶、製程、階段、解決方案、模式抗體藥物複合體(ADC) 市場分析及預測(至 2035 年):按類型、產品、技術、應用、最終用戶、組件、製程、安裝類型、模式和階段分類

ADC技術市場分析及預測至2035年:依類型、產品類型、服務、技術、組件、應用、製程、最終用戶、裝置、階段分類抗體藥物複合體(ADC) 市場分析及預測至 2035 年:按類型、產品類型、服務、技術、應用、最終用戶、製程、階段、解決方案、模式抗體藥物複合體(ADC) 市場分析及預測(至 2035 年):按類型、產品、技術、應用、最終用戶、組件、製程、安裝類型、模式和階段分類 ADC細胞毒性有效載荷和彈頭市場(第二版):市場趨勢及至2035年預測 - 按產品類型、有效載荷類型、有效載荷/彈頭子類別和地區劃分ADC 連接器市場按產品類型、技術、應用、最終用途和分銷管道分類,全球預測,2026-2032 年ADC藥物CDMO服務市場按服務類型、服務規模、偶聯化學、治療用途和最終用戶分類-2026-2032年全球預測PMO偶聯物市場按產品類型、應用、最終用戶、遞送方式和分子類型分類,全球預測,2026-2032年抗體寡核苷酸偶聯物CDMO市場按服務模式、營運規模、治療用途、寡核苷酸類型、抗體形式和最終用戶分類,全球預測,2026-2032年

ADC細胞毒性有效載荷和彈頭市場(第二版):市場趨勢及至2035年預測 - 按產品類型、有效載荷類型、有效載荷/彈頭子類別和地區劃分ADC 連接器市場按產品類型、技術、應用、最終用途和分銷管道分類,全球預測,2026-2032 年ADC藥物CDMO服務市場按服務類型、服務規模、偶聯化學、治療用途和最終用戶分類-2026-2032年全球預測PMO偶聯物市場按產品類型、應用、最終用戶、遞送方式和分子類型分類,全球預測,2026-2032年抗體寡核苷酸偶聯物CDMO市場按服務模式、營運規模、治療用途、寡核苷酸類型、抗體形式和最終用戶分類,全球預測,2026-2032年