|

市場調查報告書

商品編碼

1876566

壓縮天然氣(CNG)汽車系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Compressed Natural Gas (CNG) Vehicle System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

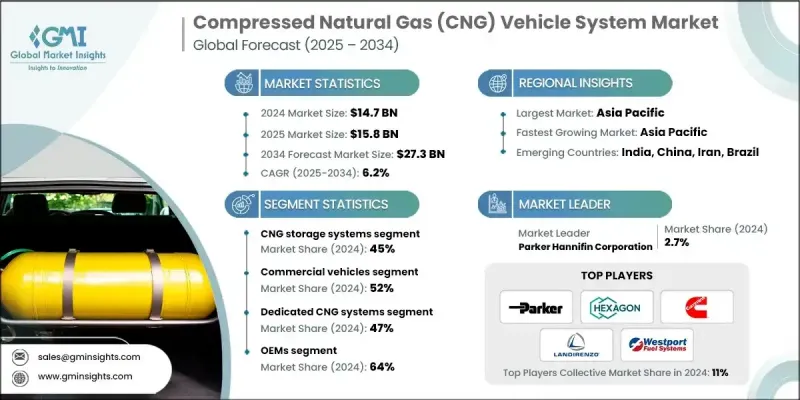

2024 年全球壓縮天然氣 (CNG) 汽車系統市值為 147 億美元,預計到 2034 年將以 6.2% 的複合年成長率成長至 273 億美元。

市場擴張主要得益於各大汽車產區日益嚴格的排放和碳減排法規,這些法規鼓勵整車製造商和車隊營運商採用更清潔的燃料替代品,例如壓縮天然氣 (CNG)。與柴油和汽油汽車相比,CNG 動力汽車的二氧化碳 (CO2)、氮氧化物 (NOx) 和顆粒物排放量顯著降低,有助於製造商滿足乘用車和商用車的歐 6 和印度第六階段排放標準等環保法規的要求。 CNG 的成本優勢進一步推動了市場成長,其每公里成本比汽油或柴油低約 30-40%,為車隊營運商和注重成本的消費者節省了大量資金。全球原油價格波動促使各國政府,特別是新興地區的政府,將推廣 CNG 作為降低燃料進口依賴的策略。對 CNG 加氣和分銷基礎設施的投資正在提高其可及性,公私合作和政府資助的項目正在擴大高速公路和城市走廊沿線的加氣站網路。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 147億美元 |

| 預測值 | 273億美元 |

| 複合年成長率 | 6.2% |

2024年,CNG儲氣系統市場規模為66.6億美元,預計2034年將達到122.1億美元。該市場受益於輕質複合材料的進步,研究表明,複合材料儲罐的製造成本預計將降低30-50%。

2024年,專用CNG系統市佔率達到47%,預計2025年至2034年將以7.8%的複合年成長率成長。由於其燃油效率高、排放量低,這些車輛在車隊和城市交通系統中廣受歡迎。儘管現有的CNG基礎設施仍然有限,但製造商正致力於最佳化引擎設計和儲氣系統以提高可靠性,使專用系統成為永續交通發展計畫的核心。

2024年,美國壓縮天然氣(CNG)汽車系統市場佔全球市場佔有率的91%,創造了1.064億美元的收入。雖然美國在全球市場中所佔佔有率較小,但由於該國石油資源豐富,與那些高度重視替代燃料的地區相比,美國仍然是一個成熟的市場,成長有限。

壓縮天然氣(CNG)汽車系統市場的主要參與者包括Westport Fuel Systems、Parker Hannifin、Hexagon Composites、Clean Energy Fuels、Cummins、BRC Gas、Galileo Technologies、Luxfer、Landi Renzo和Worthington Industries。這些企業正採取多種策略來鞏固自身地位並擴大市場佔有率。他們加大研發投入,以提高引擎效率、儲氣能力和燃料系統的耐久性。與汽車原始設備製造商(OEM)的策略合作,使得CNG系統能夠無縫整合到新車型中。此外,各公司也正在拓展全球經銷網路,與加氣基礎設施供應商建立合作關係,並積極支持政府所推行的清潔交通計劃。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預測模型

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 嚴格的排放法規

- 燃油成本差異不斷擴大

- 擴建加油基礎設施

- OEM整合與技術進步

- 產業陷阱與挑戰

- 新興地區加油基礎設施有限

- 初始轉換和儲存成本高

- 市場機遇

- 政府補貼和激勵措施

- 車隊電氣化-混合動力一體化

- 城市公共運輸需求日益成長

- 輕型複合材料汽缸的開發

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 技術準備度和成熟度評估

- 價格趨勢

- 按地區

- 依產品

- 生產統計

- 生產中心

- 消費中心

- 進出口

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 商業模式分析

- 設備銷售模式與租賃模式

- 服務和維護收入來源

- 基礎設施即服務模式

- 燃料供應合約結構

- 最終用戶調查洞察與要求

- 風險評估與緩解策略

- 技術風險分析

- 市場風險因素

- 監理風險評估

- 供應鏈風險評估

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

- 產品和服務基準測試

- 研發投資分析

- 供應商選擇標準

第5章:市場估算與預測:依產品分類,2021-2034年

- 主要趨勢

- CNG儲氣系統

- I 型(鋼)

- II 型(鋼+複合材料)

- 第三類(鋁+複合材料)

- 四型(全複合型)

- 燃油輸送系統

- 壓力調節器

- 燃油噴射器

- 電子控制單元

- 燃油管路及接頭

- 改裝套件

- 完整的改造系統

- 雙燃料轉換套件

- 專用 CNG 系統

- 其他部件

- 安全系統

- 儀表和指示器

- 安裝配件

第6章:市場估算與預測:依系統分類,2021-2034年

- 主要趨勢

- 專用 CNG 系統

- 雙燃料(CNG/汽油)系統

- 雙燃料(CNG/柴油)系統

第7章:市場估價與預測:依車輛類型分類,2021-2034年

- 主要趨勢

- 搭乘用車

- 轎車

- SUV

- 掀背車

- 商用車輛

- 輕型商用車(LCV)

- 重型商用車(HCV)

- 中型商用車(MCV)

- 非公路車輛

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- OEM(原始設備製造商)

- 售後市場

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐

- 俄羅斯

- 波蘭

- 羅馬尼亞

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 伊朗

第10章:公司簡介

- Global companies

- BRC Gas

- Chart Industries

- Clean Energy Fuel

- Cummins

- Hexagon Composites

- Landi Renzo

- Luxfer

- Parker Hannifin

- Westport Fuel Systems

- Worthington Industries

- Regional companies

- Allison Transmission

- Angi Energy Systems

- Faber Industrie

- Quantum Fuel Systems Technologies

- Swagelok Company

- Trillium CNG

- WEH

- Emerging companies

- Ashok Leyland

- Beijing Tianhai Industry

- Censtar Science & Technology

- Galileo Technologies

- IMPCO Technologies

The Global Compressed Natural Gas (CNG) Vehicle System Market was valued at USD 14.7 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 27.3 billion by 2034.

The market expansion is driven by stringent emission and carbon reduction regulations across major automotive regions, encouraging OEMs and fleet operators to adopt cleaner fuel alternatives such as CNG. Compared to diesel and gasoline vehicles, CNG-powered vehicles emit substantially lower levels of CO2, NOx, and particulate matter, helping manufacturers comply with environmental regulations like Euro 6 and Bharat Stage VI standards for both passenger and commercial vehicles. The cost advantage of CNG further supports market growth, as it costs approximately 30-40% less per kilometer than gasoline or diesel, offering significant savings for fleet operators and cost-conscious consumers. Global crude oil price volatility has prompted governments, particularly in emerging regions, to incentivize CNG adoption as a strategy to reduce fuel import dependence. Investment in CNG refueling and distribution infrastructure is improving accessibility, with public-private partnerships and government-funded initiatives expanding station networks along highways and urban corridors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.7 Billion |

| Forecast Value | $27.3 Billion |

| CAGR | 6.2% |

The CNG storage systems segment generated USD 6.66 billion in 2024 and is expected to reach USD 12.21 billion by 2034. This segment benefits from advances in lightweight composite materials, with research showing potential cost reductions of 30-50% in manufacturing composite tanks.

The dedicated CNG systems segment held a 47% share in 2024 and is projected to grow at a CAGR of 7.8% from 2025 to 2034. These vehicles are popular among fleets and urban transit systems due to their fuel efficiency and low emissions. Although existing CNG infrastructure remains limited, manufacturers are focusing on optimizing engine designs and storage systems to improve reliability, making dedicated systems central to sustainable transportation initiatives.

US Compressed Natural Gas (CNG) Vehicle System Market accounted for a 91% share and generated USD 106.4 million in 2024. While the US represents a smaller portion of the global opportunity, it remains a mature market with limited growth compared to regions focusing heavily on alternative fuels, largely due to the country's abundant petroleum resources.

Key players operating in the Compressed Natural Gas (CNG) Vehicle System Market include Westport Fuel Systems, Parker Hannifin, Hexagon Composites, Clean Energy Fuels, Cummins, BRC Gas, Galileo Technologies, Luxfer, Landi Renzo, and Worthington Industries. Companies in the Compressed Natural Gas (CNG) Vehicle System Market are employing multiple strategies to strengthen their position and expand market share. They are investing in research and development to enhance engine efficiency, storage capacity, and fuel system durability. Strategic collaborations with automotive OEMs allow seamless integration of CNG systems into new vehicle models. Firms are expanding their global distribution networks, establishing partnerships with fueling infrastructure providers, and supporting government initiatives for cleaner transportation.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 System

- 2.2.4 Vehicle

- 2.2.5 End Use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent emission regulations

- 3.2.1.2 Rising fuel cost differentials

- 3.2.1.3 Expanding refueling infrastructure

- 3.2.1.4 OEMs integration and technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited refueling infrastructure in emerging regions

- 3.2.2.2 High initial conversion and storage costs

- 3.2.3 Market opportunities

- 3.2.3.1 Government subsidies and incentives

- 3.2.3.2 Fleet electrification-hybrid integration

- 3.2.3.3 Growing urban public transport demand

- 3.2.3.4 Lightweight composite cylinder development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology readiness & maturity assessment

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

- 3.14 Business model analysis

- 3.14.1 Equipment sales vs leasing models

- 3.14.2 Service and maintenance revenue streams

- 3.14.3 Infrastructure-as-a-service models

- 3.14.4 Fuel supply contract structures

- 3.15 End Use survey insights & requirements

- 3.16 Risk assessment & mitigation strategies

- 3.16.1 Technology risk analysis

- 3.16.2 Market risk factors

- 3.16.3 Regulatory risk assessment

- 3.16.4 Supply chain risk evaluation

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Product and service benchmarking

- 4.8 R&D investment analysis

- 4.9 Vendor selection criteria

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 CNG storage systems

- 5.2.1 Type I (Steel)

- 5.2.2 Type II (Steel+composite)

- 5.2.3 Type III (Aluminum+composite)

- 5.2.4 Type IV (Full composite)

- 5.3 Fuel delivery systems

- 5.3.1 Pressure regulators

- 5.3.2 Fuel injectors

- 5.3.3 Electronic control units

- 5.3.4 Fuel lines & fittings

- 5.4 Conversion kits

- 5.4.1 Complete retrofit systems

- 5.4.2 Bi-fuel conversion kits

- 5.4.3 Dedicated CNG systems

- 5.5 Other components

- 5.5.1 Safety systems

- 5.5.2 Gauges & indicators

- 5.5.3 Installation accessories

Chapter 6 Market Estimates & Forecast, By System, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Dedicated CNG systems

- 6.3 Bi-fuel (CNG/Gasoline) systems

- 6.4 Dual-fuel (CNG/Diesel) systems

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedan

- 7.2.2 SUV

- 7.2.3 Hatchback

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Heavy commercial vehicles (HCV)

- 7.3.3 Medium commercial vehicles (MCV)

- 7.4 Off-highway vehicles

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEMs (Original equipment manufacturer)

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Iran

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 BRC Gas

- 10.1.2 Chart Industries

- 10.1.3 Clean Energy Fuel

- 10.1.4 Cummins

- 10.1.5 Hexagon Composites

- 10.1.6 Landi Renzo

- 10.1.7 Luxfer

- 10.1.8 Parker Hannifin

- 10.1.9 Westport Fuel Systems

- 10.1.10 Worthington Industries

- 10.2 Regional companies

- 10.2.1 Allison Transmission

- 10.2.2 Angi Energy Systems

- 10.2.3 Faber Industrie

- 10.2.4 Quantum Fuel Systems Technologies

- 10.2.5 Swagelok Company

- 10.2.6 Trillium CNG

- 10.2.7 WEH

- 10.3 Emerging companies

- 10.3.1 Ashok Leyland

- 10.3.2 Beijing Tianhai Industry

- 10.3.3 Censtar Science & Technology

- 10.3.4 Galileo Technologies

- 10.3.5 IMPCO Technologies

CNG 和 LPG 汽車市場:按燃料類型、引擎系統、汽缸類型、車輛類型、應用和銷售管道分類 - 全球市場預測(2026-2032 年)

CNG 和 LPG 汽車市場:按燃料類型、引擎系統、汽缸類型、車輛類型、應用和銷售管道分類 - 全球市場預測(2026-2032 年) CNG 和 LPG 汽車市場分析及預測(至 2035 年):按服務、技術、組件、應用、最終用戶、安裝類型、設備和燃料類型分類

CNG 和 LPG 汽車市場分析及預測(至 2035 年):按服務、技術、組件、應用、最終用戶、安裝類型、設備和燃料類型分類 CNG 和 LPG 汽車市場 - 全球產業規模、佔有率、趨勢、機會和預測:按燃料類型、車輛類型、需求類別、地區和競爭格局分類,2021-2031 年

CNG 和 LPG 汽車市場 - 全球產業規模、佔有率、趨勢、機會和預測:按燃料類型、車輛類型、需求類別、地區和競爭格局分類,2021-2031 年 全球 CNG 和 LPG 汽車市場規模、佔有率、趨勢和成長分析報告(2026-2034 年)

全球 CNG 和 LPG 汽車市場規模、佔有率、趨勢和成長分析報告(2026-2034 年) 2026年全球CNG和LPG汽車市場報告

2026年全球CNG和LPG汽車市場報告 全球 CNG 和 LPG 汽車市場

全球 CNG 和 LPG 汽車市場 CNG 和 LPG 汽車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

CNG 和 LPG 汽車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 印度 CNG 汽車市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)非洲的 CNG 和 LPG 車輛:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)CNG 摩托車市場按產品類型、引擎類型、控制系統、引擎容量、燃料箱容量和最終用戶分類 - 2025-2030 年全球預測

印度 CNG 汽車市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)非洲的 CNG 和 LPG 車輛:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)CNG 摩托車市場按產品類型、引擎類型、控制系統、引擎容量、燃料箱容量和最終用戶分類 - 2025-2030 年全球預測