|

市場調查報告書

商品編碼

1741041

CNG 和 LPG 汽車市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測CNG and LPG Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

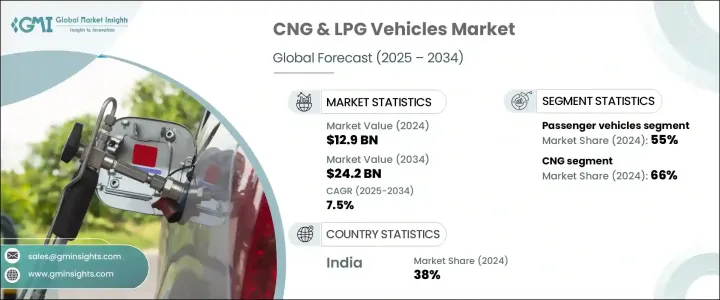

2024年,全球壓縮天然氣(CNG)和液化石油氣(LPG)汽車市場價值129億美元,預計到2034年將以7.5%的複合年成長率成長,達到242億美元,這得益於對環保節能汽車需求的激增。民眾對氣候變遷和空氣品質惡化的認知日益增強,促使政府和消費者尋求更環保的出行解決方案。隨著能源安全在全球日益受到重視,CNG和LPG汽車正逐漸成為傳統汽油和柴油汽車的實用替代品,可大幅節省成本並降低碳排放。世界各國正在推行嚴格的排放標準,收緊燃油經濟性標準,並鼓勵使用替代燃料,這使得CNG和LPG汽車成為越來越有吸引力的選擇。 CNG引擎的技術進步進一步提升了車輛性能,同時顯著減少了有害污染物的排放,為市場未來強勁成長奠定了基礎。對清潔能源基礎設施、改造解決方案和加油網路擴展的投資正在創建一個支持長期應用的生態系統。此外,燃料價格波動加劇,促使車隊營運商和個人消費者探索更經濟、更永續的選擇,使 CNG 和 LPG 汽車成為未來出行趨勢的前沿。

隨著各國大力推行兼顧環境責任與經濟可行性的交通替代方案,CNG 與 LPG 汽車正成為全球永續發展計劃的重要參與者。各國政府正採取大膽舉措,實施更嚴格的排放標準,並提供包括退稅和補助在內的誘人激勵措施,以推動清潔燃料的普及。在多個關鍵市場,越來越多的車隊營運商正從柴油轉向 CNG,以實現長期營運成本效益。價格實惠的改裝套件日益普及,加上公共運輸系統日益青睞經濟高效的解決方案,這些因素正在強化成本敏感型消費者對 CNG 和 LPG 汽車的青睞。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 129億美元 |

| 預測值 | 242億美元 |

| 複合年成長率 | 7.5% |

乘用車市場在2024年佔據55%的市場佔有率,預計到2034年將以7%的複合年成長率成長,因為買家更重視經濟性和環保性能。在商用車方面,以壓縮天然氣(CNG)為動力的卡車和送貨車的興起正在重塑城市物流,為傳統車隊提供清潔、節能的替代方案。商用車,尤其是在城市環境中,正受益於營運效率的提高和支持性政策框架。在人口密集的大都市地區,以壓縮天然氣(CNG)和液化石油氣(LPG)為動力的三輪車正在迅速普及,為短途運輸提供了實用且經濟實惠的解決方案。

2024年,壓縮天然氣(CNG)在全球CNG和LPG汽車市場佔據了66%的主導地位。其領先地位源於其在經濟實惠、減少排放以及符合日益嚴格的環境法規方面提供的顯著優勢。由於其減少碳足跡和節省成本,CNG將繼續成為商用車隊和個人消費者的首選。

2024年,印度的CNG和LPG汽車市場規模達24億美元,佔全球市場佔有率的38%。快速的都市化、傳統燃料價格的通膨壓力以及大力扶持替代燃料的公共政策,共同推動了這一成長。各大城市正穩步轉向更清潔的公共交通方式,其中CNG公車和計程車引領了這一趨勢。內燃機汽車的CNG套件改裝,進一步加速了城市景觀的轉型。

豐田、現代汽車公司、馬恆達、塔塔汽車、福特汽車公司、通用汽車、大眾集團、依維柯、曼恩集團和本田等領先汽車製造商正在大力投資產品創新,擴大其 CNG 和 LPG 汽車產品組合,並加強其分銷網路。許多公司正在與燃料供應商合作,以改善加油基礎設施,尤其是在新興市場。混合動力 CNG 技術、智慧車輛整合和車隊合作模式等策略正在幫助企業在不斷發展的 CNG 和 LPG 汽車市場中站穩腳跟。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 燃料供應商

- 零件製造商

- 汽車製造商(OEM)

- 改裝商和售後市場供應商

- 分銷和零售基礎設施

- 利潤率分析

- 川普政府關稅

- 對產業的影響

- 供給側影響(原料)

- 主要材料價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 供給側影響(原料)

- 受影響的主要公司

- 對產業的影響

- 技術與創新格局

- 專利分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- CNG技術的快速進步

- 日益重視永續旅遊

- 對經濟高效的交通運輸的需求日益成長

- 比汽油動力汽車的維修成本更低

- 產業陷阱與挑戰

- 前期成本較高

- 與汽油動力汽車相比性能下降

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- 越野車

5.3 三輪車

- 商用車

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第6章:市場估計與預測:按燃料,2021 - 2034 年

- 主要趨勢

- 液化石油氣

- 天然氣

第7章:市場估計與預測:按引擎系統,2021 - 2034 年

- 主要趨勢

- 專用系統

- 雙燃料

- 雙燃料

第8章:市場估計和預測:按擬合,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第10章:公司簡介

- Ashok Leyland

- Bajaj Auto

- Ford Motor Company

- General Motors

- Honda

- Hyundai Motor Company

- Isuzu Motors

- IVECO

- Kia Motors

- Landi Renzo

- Mahindra & Mahindra

- MAN SE

- Maruti Suzuki

- Renault

- SEAT

- Skoda Auto

- Tata Motors

- Toyota

- Volkswagen Group

- Westport Fuel Systems

The Global CNG and LPG Vehicles Market was valued at USD 12.9 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 24.2 billion by 2034, driven by the surging demand for environmentally friendly and fuel-efficient vehicles. Growing public awareness about climate change and deteriorating air quality has pushed both governments and consumers toward greener mobility solutions. As energy security gains prominence worldwide, CNG and LPG vehicles are emerging as practical alternatives to traditional gasoline and diesel vehicles, offering substantial cost savings and lower carbon emissions. Countries around the world are rolling out aggressive emission norms, tightening fuel economy standards, and incentivizing alternative fuel adoption, making CNG and LPG vehicles an increasingly attractive choice. Technological advancements in CNG engines are further elevating vehicle performance while significantly cutting down harmful pollutants, positioning the market for strong future growth. Investment in clean energy infrastructure, retrofitting solutions, and the expansion of refueling networks is creating an ecosystem that supports long-term adoption. Moreover, rising fuel price volatility is pushing fleet operators and individual consumers to explore more economical and sustainable options, putting CNG and LPG vehicles at the forefront of future mobility trends.

CNG and LPG vehicles are becoming vital players in global sustainability initiatives as nations push for transportation alternatives that balance environmental responsibility with economic feasibility. Governments are taking bold steps by implementing stricter emission norms and offering attractive incentives, including tax rebates and grants, to drive the adoption of cleaner fuels. In several key markets, fleet operators are increasingly transitioning from diesel to CNG to realize long-term operational cost benefits. The availability of affordable retrofitting kits, combined with the growing presence of public transportation systems that favor cost-effective solutions, is reinforcing the trend toward CNG and LPG vehicle adoption among cost-sensitive consumers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.9 Billion |

| Forecast Value | $24.2 Billion |

| CAGR | 7.5% |

The passenger vehicles segment dominated the market with a 55% share in 2024 and is projected to grow at a CAGR of 7% through 2034, as buyers prioritize affordability and environmental performance. On the commercial side, the rise of CNG-powered trucks and delivery vans is reshaping urban logistics by offering clean, fuel-efficient alternatives to traditional fleets. Commercial vehicles, particularly in urban environments, are benefiting from operational efficiencies and supportive policy frameworks. In dense metropolitan areas, three-wheelers running on CNG and LPG are gaining rapid traction, offering a practical and affordable solution for short-distance transportation.

The compressed natural gas (CNG) segment held a commanding 66% share of the global CNG and LPG vehicles market in 2024. Its leadership stems from the clear benefits it offers in terms of affordability, reduced emissions, and compliance with increasingly stringent environmental regulations. CNG continues to emerge as a preferred choice for both commercial fleets and individual consumers, thanks to its reduced carbon footprint and cost savings.

India's CNG and LPG Vehicles Market generated USD 2.4 billion in 2024, capturing a 38% share of the global market. Rapid urbanization, inflationary pressures on conventional fuel prices, and robust public policies favoring alternative fuels are driving this growth. Major cities are witnessing a steady shift toward cleaner public transportation options, with CNG buses and taxis leading the way. Retrofitting of internal combustion engine vehicles with CNG kits is further accelerating this transition across urban landscapes.

Leading automakers like Toyota, Hyundai Motor Company, Mahindra and Mahindra, Tata Motors, Ford Motor Company, General Motors, Volkswagen Group, IVECO, MAN SE, and Honda are heavily investing in product innovations, expanding their CNG and LPG vehicle portfolios, and strengthening their distribution networks. Many are collaborating with fuel providers to improve refueling infrastructure, especially in emerging markets. Strategies such as hybridized CNG technologies, smart vehicle integrations, and fleet partnership models are helping companies solidify their foothold in the evolving CNG and LPG vehicles market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Fuel providers

- 3.2.2 Component manufacturers

- 3.2.3 Vehicle manufacturers (OEMs)

- 3.2.4 Retrofitters and aftermarket suppliers

- 3.2.5 Distribution and retail infrastructure

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on the industry

- 3.4.1.1 Supply-side impact (raw materials)

- 3.4.1.1.1 Price volatility in key materials

- 3.4.1.1.2 Supply chain restructuring

- 3.4.1.1.3 Production cost implications

- 3.4.1.2 Demand-side impact (selling price)

- 3.4.1.2.1 Price transmission to end markets

- 3.4.1.2.2 Market share dynamics

- 3.4.1.1 Supply-side impact (raw materials)

- 3.4.2 Key companies impacted

- 3.4.1 Impact on the industry

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rapid advancements in CNG technology

- 3.9.1.2 Increasing emphasis on sustainable mobility

- 3.9.1.3 Rising need for cost-effective transportation

- 3.9.1.4 Lower maintenance cost than petrol-powered vehicles

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Higher upfront costs

- 3.9.2.2 Reduced performance compared to petrol-powered vehicles

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUV

5.3 Three-wheelers

- 5.4 Commercial vehicles

- 5.4.1 Light Commercial Vehicles (LCV)

- 5.4.2 Medium Commercial Vehicles (MCV)

- 5.4.3 Heavy Commercial Vehicles (HCV)

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 LPG

- 6.3 CNG

Chapter 7 Market Estimates & Forecast, By Engine System, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Dedicated system

- 7.3 Bi-fuel

- 7.4 Dual fuel

Chapter 8 Market Estimates & Forecast, By Fitting, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Ashok Leyland

- 10.2 Bajaj Auto

- 10.3 Ford Motor Company

- 10.4 General Motors

- 10.5 Honda

- 10.6 Hyundai Motor Company

- 10.7 Isuzu Motors

- 10.8 IVECO

- 10.9 Kia Motors

- 10.10 Landi Renzo

- 10.11 Mahindra & Mahindra

- 10.12 MAN SE

- 10.13 Maruti Suzuki

- 10.14 Renault

- 10.15 SEAT

- 10.16 Skoda Auto

- 10.17 Tata Motors

- 10.18 Toyota

- 10.19 Volkswagen Group

- 10.20 Westport Fuel Systems

CNG 和 LPG 汽車市場:按燃料類型、引擎系統、汽缸類型、車輛類型、應用和銷售管道分類 - 全球市場預測(2026-2032 年)

CNG 和 LPG 汽車市場:按燃料類型、引擎系統、汽缸類型、車輛類型、應用和銷售管道分類 - 全球市場預測(2026-2032 年) CNG 和 LPG 汽車市場分析及預測(至 2035 年):按服務、技術、組件、應用、最終用戶、安裝類型、設備和燃料類型分類

CNG 和 LPG 汽車市場分析及預測(至 2035 年):按服務、技術、組件、應用、最終用戶、安裝類型、設備和燃料類型分類 CNG 和 LPG 汽車市場 - 全球產業規模、佔有率、趨勢、機會和預測:按燃料類型、車輛類型、需求類別、地區和競爭格局分類,2021-2031 年

CNG 和 LPG 汽車市場 - 全球產業規模、佔有率、趨勢、機會和預測:按燃料類型、車輛類型、需求類別、地區和競爭格局分類,2021-2031 年 全球 CNG 和 LPG 汽車市場規模、佔有率、趨勢和成長分析報告(2026-2034 年)

全球 CNG 和 LPG 汽車市場規模、佔有率、趨勢和成長分析報告(2026-2034 年) 2026年全球CNG和LPG汽車市場報告

2026年全球CNG和LPG汽車市場報告 壓縮天然氣(CNG)汽車系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

壓縮天然氣(CNG)汽車系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球 CNG 和 LPG 汽車市場

全球 CNG 和 LPG 汽車市場 印度 CNG 汽車市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)非洲的 CNG 和 LPG 車輛:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)CNG 摩托車市場按產品類型、引擎類型、控制系統、引擎容量、燃料箱容量和最終用戶分類 - 2025-2030 年全球預測

印度 CNG 汽車市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)非洲的 CNG 和 LPG 車輛:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)CNG 摩托車市場按產品類型、引擎類型、控制系統、引擎容量、燃料箱容量和最終用戶分類 - 2025-2030 年全球預測