|

市場調查報告書

商品編碼

1871285

食品酵素市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Food Enzymes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球食品酵素市場價值為 34 億美元,預計到 2034 年將以 5.2% 的複合年成長率成長至 58 億美元。

在食品加工產業對酵素製劑解決方案需求不斷成長的推動下,市場正穩步發展。酵素製劑能夠提高生產效率、降低營運成本,並改善多種食品類別的產品品質。全球工業化食品製造規模的不斷擴大進一步促進了這一成長,隨著食品產量的增加,對加工助劑的需求自然也隨之成長。此外,新興地區對加工食品和簡便食品日益成長的需求也為酵素製劑的應用開闢了新的途徑。目前,酵素製劑技術的研發投入已達到歷史新高,領先企業正投入大量資源進行創新。持續的研發投入確保了先進解決方案的不斷湧現,從而維持了市場的長期成長,並展現出即使在經濟波動中也能保持韌性的能力,這凸顯了酶製劑在現代食品生產系統中的關鍵作用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 34億美元 |

| 預測值 | 58億美元 |

| 複合年成長率 | 5.2% |

2024年,蛋白酶市場佔有率達到40%,預計2034年將以4.9%的複合年成長率成長。其市場主導地位源自於其在肉類、乳製品、烘焙和釀造等加工過程中改善產品質地、消化率和整體品質的廣泛應用。隨著消費者對富含蛋白質和功能性食品的需求不斷成長,蛋白酶的重要性也日益凸顯。

2024年,乳製品加工產業佔據28%的市場佔有率,預計2025年至2034年將以4.9%的複合年成長率成長。酵素在乳製品生產中發揮著至關重要的作用,包括乳酪製作和乳糖改性乳製品,以滿足消費者對多樣化營養選擇日益成長的需求。先進的酵素系統能夠改善風味、質地和延長保存期限,其中蛋白酶和脂肪酶是生產高品質功能性乳製品的核心。

預計到2024年,北美食品酵素市場佔有率將達到25%。該地區的成長得益於先進的食品加工基礎設施、嚴格的監管框架以及消費者對酵素益處的認知不斷提高。主要酵素生產商的存在,以及持續的創新和研發驅動的產品開發,進一步鞏固了北美的領先地位。

全球食品酵素市場的主要參與者包括Novozenis(原Novozymes A/S)、帝斯曼-菲美意(DSM-Firmenich)、巴斯夫(BASF SE)、凱瑞集團(Kerry Group plc)、國際香料香精公司(IFF)、科漢森控股(Chr. Hansen Holzy/S)、先進酵素技術公司(IFF)、科漢森控股(Chr. Hansen Holzy/S)、先進酵素技術有限公司(ApzyS) Inc)、生物催化劑有限公司(Biocatalysts Ltd)、凱敏工業有限公司(Kemin Industries Inc)、聯合英國食品公司(Associated British Foods plc)、酵素開發公司(Enzyme Development Corporation)、Maps Enzymes Ltd、Creative Enzymes、Prozomix Ltd、長瀨化學株接合公司(NBioel)公司(NBiox Corporation)公司(Enconx)、Enconzy)。食品酵素市場的企業採取多種策略來鞏固市場地位並擴大業務範圍。他們大力投資研發,以開發具有更強功能、更高穩定性和更廣泛應用的新型酵素。策略性併購和合作有助於拓展產品組合和區域市場滲透。此外,各公司也專注於製程最佳化、成本效益和技術整合,為工業食品加工商提供客製化解決方案。行銷活動、與食品生產商的合作以及知識共享計劃有助於建立品牌知名度和信任度。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 對清潔標籤產品的需求不斷成長

- 不斷提高的食品加工效率需求

- 健康意識日益增強

- 產業陷阱與挑戰

- 監理合規的複雜性

- 高額研發投入需求

- 市場機遇

- 植物性食品的新興應用

- 生物技術創新管道

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 蛋白酶

- 凝乳酵素和凝乳酶

- 胃蛋白酶和胰蛋白酶

- 木瓜蛋白酶和鳳梨蛋白酶

- 微生物蛋白酶

- 碳水化合物酶

- α-澱粉酶

- 葡糖澱粉酶和普魯蘭酶

- 纖維素酶和半纖維素酶

- 果膠酶和木聚醣酶

- 脂肪酶

- 動物脂肪酶

- 微生物脂肪酶

- 植物源性脂肪酶

- 植酸酶

- 微生物植酸酶

- 基因改造植酸酶

- 過氧化氫酶

- 牛肝過氧化氫酶

- 微生物過氧化氫酶

- 聚合酶和核酸酶

- DNA聚合酶

- RNA加工酶

- 其他

- 轉谷氨醯胺酶

- 葡萄糖氧化酶

- 轉化酶和乳糖酶

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 乳製品加工

- 乳酪生產與凝固

- 牛奶加工與改良

- 乳清加工和蛋白質回收

- 無乳糖產品開發

- 烘焙食品和糖果

- 麵團的改良和強化

- 抗老化及延長保存期限

- 質地和體積改善

- 丙烯醯胺還原

- 動物飼料

- 植酸酶的應用

- 碳水化合物酶的應用

- 蛋白酶應用

- 多酵素複合物

- 飲料

- 果汁澄清與加工

- 釀造與發酵

- 葡萄酒生產與品質提升

- 運動飲料和功能飲料

- 加工食品

- 蛋白質改質與質構化

- 脂肪替代和減少

- 風味增強

- 營養強化

- 澱粉和甜味劑生產

- 葡萄糖漿生產

- 高果糖玉米糖漿(HFCS)

- 麥芽糊精和改性澱粉

- 特種甜味劑

第7章:市場估計與預測:依來源分類,2021-2034年

- 主要趨勢

- 微生物酵素

- 細菌來源

- 真菌來源

- 酵母來源

- 基因改造酶

- 重組凝乳酶

- 革蘭氏陰性菌微生物酶

- 工程酶變體

- 植物源酵素

- 木瓜蛋白酶

- 鳳梨蛋白酶

- 無花果中的無花果苷

- 動物源性酵素

- 胰臟

- 胃蛋白酶

- 動物凝乳酶

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Novozymes A/S (now Novonesis)

- DSM-firmenich

- International Flavors & Fragrances Inc. (IFF)

- Kerry Group plc

- BASF SE

- Chr. Hansen Holding A/S

- Associated British Foods plc

- Advanced Enzyme Technologies Ltd

- Kemin Industries Inc

- Amano Enzyme Inc

- Biocatalysts Ltd

- Enzyme Development Corporation

- Maps Enzymes Ltd

- Creative Enzymes

- Prozomix Ltd

- Nagase ChemteX Corporation

- Enzyme Solutions Inc

- Biocon Ltd

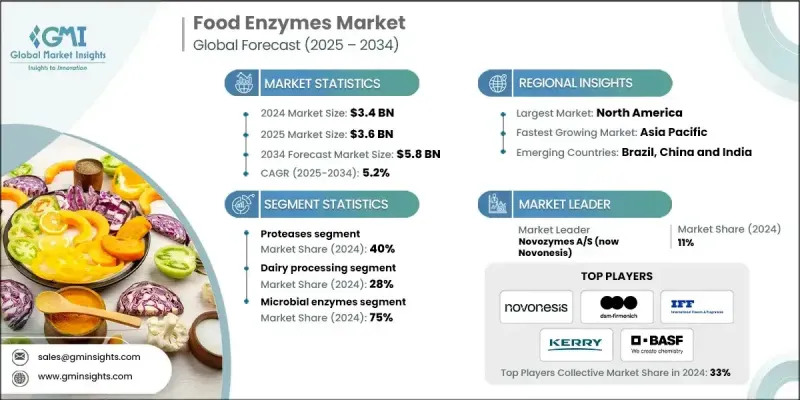

The Global Food Enzymes Market was valued at USD 3.4 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 5.8 billion by 2034.

The market is steadily advancing, driven by the rising demand for enzyme-based solutions in the food processing industry. Enzymes enhance production efficiency, reduce operational costs, and improve product quality across multiple food categories. The growth is further supported by the expanding scale of industrial food manufacturing worldwide, where demand for processing aids naturally rises with higher food output. Additionally, the growing preference for processed and convenience foods in emerging regions creates fresh avenues for enzyme applications. Research and development investments in enzyme technologies are at an all-time high, with leading companies allocating substantial resources to innovation. Continuous R&D ensures the introduction of advanced solutions, sustaining long-term market growth and demonstrating resilience even through economic fluctuations, highlighting the essential role of enzymes in modern food production systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $5.8 Billion |

| CAGR | 5.2% |

The proteases segment held a 40% share in 2024 and is expected to grow at a CAGR of 4.9% by 2034. Their dominance stems from their versatile applications in enhancing texture, digestibility, and overall product quality in meat, dairy, baking, and brewing processes. Proteases continue to be vital as demand for protein-rich and functional foods expands.

The dairy processing segment held a 28% share in 2024 and is projected to grow at a CAGR of 4.9% from 2025 to 2034. Enzymes play a critical role in dairy production, including cheese-making and lactose-modified milk products, catering to the increasing consumer demand for diverse nutritional options. Advanced enzyme systems now improve flavor, texture, and shelf life, with proteases and lipases being central to producing high-quality, functional dairy products.

North America Food Enzymes Market held a 25% share in 2024. The region's growth is fueled by advanced food processing infrastructure, stringent regulatory frameworks, and consumer awareness about enzyme benefits. The presence of key enzyme manufacturers, coupled with ongoing innovation and R&D-driven product development, further strengthens North America's leadership position.

Leading players in the Global Food Enzymes Market include Novonesis (formerly Novozymes A/S), DSM-Firmenich, BASF SE, Kerry Group plc, International Flavors & Fragrances Inc. (IFF), Chr. Hansen Holding A/S, Advanced Enzyme Technologies Ltd, Amano Enzyme Inc, Biocatalysts Ltd, Kemin Industries Inc, Associated British Foods plc, Enzyme Development Corporation, Maps Enzymes Ltd, Creative Enzymes, Prozomix Ltd, Nagase ChemteX Corporation, Enzyme Solutions Inc, and Biocon Ltd. Companies in the Food Enzymes Market adopt a variety of strategies to strengthen market presence and expand their footprint. They invest heavily in research and development to create novel enzymes with enhanced functionality, improved stability, and broader application across food categories. Strategic mergers, acquisitions, and partnerships enable expansion of product portfolios and regional penetration. Firms also focus on process optimization, cost efficiency, and technology integration to provide tailored solutions for industrial food processors. Marketing initiatives, collaboration with food manufacturers, and knowledge-sharing programs help build brand recognition and trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Source

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for clean label products

- 3.2.1.2 Increasing food processing efficiency requirements

- 3.2.1.3 Rising health & wellness consciousness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory compliance complexity

- 3.2.2.2 High R&D investment requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging applications in plant-based foods

- 3.2.3.2 Biotechnology innovation pipeline

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Proteases

- 5.2.1 Rennet & chymosin

- 5.2.2 Pepsin & trypsin

- 5.2.3 Papain & bromelain

- 5.2.4 Microbial proteases

- 5.3 Carbohydrases

- 5.3.1 Alpha-amylase

- 5.3.2 Glucoamylase & pullulanase

- 5.3.3 Cellulase & hemicellulase

- 5.3.4 Pectinase & xylanase

- 5.4 Lipases

- 5.4.1 Animal lipases

- 5.4.2 Microbial lipases

- 5.4.3 Plant-derived lipases

- 5.5 Phytases

- 5.5.1 Microbial Phytases

- 5.5.2 Genetically modified phytases

- 5.6 Catalases

- 5.6.1 Bovine liver catalase

- 5.6.2 Microbial catalases

- 5.7 Polymerases & Nucleases

- 5.7.1 DNA polymerases

- 5.7.2 RNA processing enzymes

- 5.8 Other

- 5.8.1 Transglutaminases

- 5.8.2 Glucose oxidase

- 5.8.3 Invertase & lactase

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy processing

- 6.2.1 Cheese production & coagulation

- 6.2.2 Milk processing & modification

- 6.2.3 Whey processing & protein recovery

- 6.2.4 Lactose-free product development

- 6.3 Bakery & confectionery

- 6.3.1 Dough conditioning & strengthening

- 6.3.2 Anti-staling & shelf-life extension

- 6.3.3 Texture & volume improvement

- 6.3.4 Acrylamide reduction

- 6.4 Animal feed

- 6.4.1 Phytase applications

- 6.4.2 Carbohydrase applications

- 6.4.3 Protease applications

- 6.4.4 Multi-enzyme complexes

- 6.5 Beverages

- 6.5.1 Juice clarification & processing

- 6.5.2 Brewing & fermentation

- 6.5.3 Wine production & quality enhancement

- 6.5.4 Sports & functional beverages

- 6.6 Processed foods

- 6.6.1 Protein modification & texturization

- 6.6.2 Fat replacement & reduction

- 6.6.3 Flavor enhancement

- 6.6.4 Nutritional fortification

- 6.7 Starch & sweetener production

- 6.7.1 Glucose syrup production

- 6.7.2 High fructose corn syrup (HFCS)

- 6.7.3 Maltodextrin & modified starches

- 6.7.4 Specialty sweeteners

Chapter 7 Market Estimates and Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Microbial enzymes

- 7.2.1 Bacterial sources

- 7.2.2 Fungal sources

- 7.2.3 Yeast sources

- 7.3 Genetically modified enzymes

- 7.3.1 Recombinant chymosin

- 7.3.2 Gm microbial enzymes

- 7.3.3 Engineered enzyme variants

- 7.4 Plant-derived enzymes

- 7.4.1 Papain from papaya

- 7.4.2 Bromelain from pineapple

- 7.4.3 Ficin from fig

- 7.5 Animal-derived enzymes

- 7.5.1 Pancreatin

- 7.5.2 Pepsin

- 7.5.3 Animal Rennet

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Novozymes A/S (now Novonesis)

- 9.2 DSM-firmenich

- 9.3 International Flavors & Fragrances Inc. (IFF)

- 9.4 Kerry Group plc

- 9.5 BASF SE

- 9.6 Chr. Hansen Holding A/S

- 9.7 Associated British Foods plc

- 9.8 Advanced Enzyme Technologies Ltd

- 9.9 Kemin Industries Inc

- 9.10 Amano Enzyme Inc

- 9.11 Biocatalysts Ltd

- 9.12 Enzyme Development Corporation

- 9.13 Maps Enzymes Ltd

- 9.14 Creative Enzymes

- 9.15 Prozomix Ltd

- 9.16 Nagase ChemteX Corporation

- 9.17 Enzyme Solutions Inc

- 9.18 Biocon Ltd

食品酵素市場報告:趨勢、預測與競爭分析(至2035年)

食品酵素市場報告:趨勢、預測與競爭分析(至2035年) 蔬果加工酶市場規模、佔有率及成長分析:依酵素類型、原料、應用、配方類型、終端用戶產業、地區及產業預測分類,2026-2033年

蔬果加工酶市場規模、佔有率及成長分析:依酵素類型、原料、應用、配方類型、終端用戶產業、地區及產業預測分類,2026-2033年 食品酵素市場:按類型、原料、應用、地區分類

食品酵素市場:按類型、原料、應用、地區分類 食品酵素市場規模、佔有率和成長分析(按類型、配方、成分、應用和地區分類)-2026-2033年產業預測

食品酵素市場規模、佔有率和成長分析(按類型、配方、成分、應用和地區分類)-2026-2033年產業預測 全球蔬果加工用酶市場-2025-2030年預測

全球蔬果加工用酶市場-2025-2030年預測 全球食品酵素市場(至2030年)按類型(碳水化合物分解酶、蛋白酶、脂肪酶、聚合酵素、核酸酶)、應用(食品和飲料)、來源(微生物、動物、植物)、配方、功能和地區分類

全球食品酵素市場(至2030年)按類型(碳水化合物分解酶、蛋白酶、脂肪酶、聚合酵素、核酸酶)、應用(食品和飲料)、來源(微生物、動物、植物)、配方、功能和地區分類 食品酵素市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、來源、地區和競爭細分,2020-2030 年

食品酵素市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、來源、地區和競爭細分,2020-2030 年