|

市場調查報告書

商品編碼

1833687

醫療旅遊市場機會、成長動力、產業趨勢分析及2025-2034年預測Medical Tourism Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

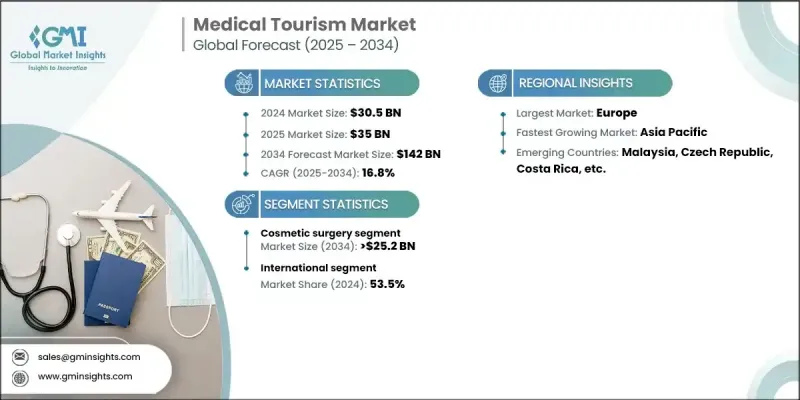

2024 年全球醫療旅遊市場價值為 305 億美元,預計到 2034 年將以 16.8% 的複合年成長率成長至 1,420 億美元。

推動市場成長的因素包括政府簡化跨境醫療旅遊的措施、發展中地區可負擔治療方案的可用性以及慢性病患者數量的增加。採用國際公認的手術標準也增強了人們對海外醫療程序的信心。亞太地區各國已成為重要的醫療中心,以較低的成本提供先進的護理,同時為國際患者提供專門的資源。來自西方國家的遊客經常選擇這些目的地來獲得優質的醫療服務,其中相當一部分人還將治療與短期健康或康復之旅結合起來。醫療旅遊的吸引力不僅在於價格實惠,還在於更短的等待時間、現代化的基礎設施和專業的照護。人們的健康意識不斷提高,加上對選擇性手術和生活方式相關治療的需求不斷成長,繼續推動醫療旅遊的發展。這些因素共同作用,使醫療旅遊成為全球患者的首選,市場也迅速調整以滿足全球需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 305億美元 |

| 預測值 | 1420億美元 |

| 複合年成長率 | 16.8% |

2024年,美容整形手術市場佔17%,這得益於旨在改善外觀的手術日益普及,而創新技術也使治療更加安全、精準和微創。更快的恢復期和更低的成本鼓勵了更多患者追求美容。數位平台的影響力日益增強,也提高了人們的認知度,尤其是在年輕人群中,這進一步刺激了美容治療的需求,並擴大了其在醫療旅遊中的作用。

2024年,國際醫療佔有率佔比53.5%,反映出尋求海外治療的患者數量穩定成長。出國就醫的吸引力在於能夠獲得先進的診療方案、降低費用,以及避開在本國冗長的候診名單。這種轉變增強了發展中國家在提供高品質醫療服務的同時保持成本競爭力的地位。來自不同地區的患者繼續選擇此類目的地作為滿足多樣化醫療需求的首選,這進一步強化了該行業的全球化特徵。

2024年,歐洲醫療旅遊市場佔36.5%的市場佔有率,預計未來幾年將大幅擴張。許多來自北美、中東及周邊國家的患者更青睞歐洲目的地,因為歐洲擁有先進的醫療基礎設施和相對較低的治療成本。歐洲一些國家仍然是吸引多學科患者的主要中心,確保在全球市場擴張中發揮重要作用。

醫療旅遊市場的主要參與者包括萊佛士醫療集團、納拉亞納健康集團、約翰霍普金斯醫院、馬克斯醫療保健、馬卡蒂醫療中心、富通醫療有限公司、梅奧診所、聖路加醫療中心、安納多盧醫療中心、康民國際醫院、KPJ 醫療保健有限公司、質子治療中心、伊麗莎白醫院、阿波羅醫院集團、康民國際醫院、KPJ 醫療保健有限公司、質子治療中心、伊麗莎白醫院、阿波羅醫院集團、克利夫蘭愛犬市閣、Skle KlinS Kliner

為了鞏固市場地位,醫療旅遊公司正推行多元化策略。領先的醫院和醫療保健集團正在擴大與旅行社、保險公司和健康中心的合作,提供涵蓋治療、住宿和後續護理的綜合套餐。他們正在大力投資先進的醫療技術和基礎設施,以確保醫療服務達到國際認可的標準。許多機構也透過客製化的行銷活動、多語言服務和專門的國際患者部門來瞄準海外患者。透過衛星設施和與地區醫院的合作拓展新興市場,有助於提高醫療服務的可近性並建立對病患的信任。包括遠距醫療諮詢和線上預約平台在內的數位轉型進一步擴大了服務範圍,同時提升了整體患者體驗。

目錄

第1章:方法論與範圍

第 2 章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 開發中國家醫療費用低廉

- 日益符合外科手術的國際標準

- 政府推出多項政策,便利醫療旅遊

- 慢性病盛行率不斷上升

- 產業陷阱與挑戰

- 某些醫療程序的等待時間較長

- 患者追蹤及術後併發症問題

- 機會

- 健康經濟特區發展

- 數位醫療和遠距醫療

- 成長動力

- 成長潛力分析

- 監管格局

- 技術和創新格局

- 當前的技術趨勢

- 人工智慧翻譯工具

- 數位健康平台

- 電子病歷(EMR)整合

- 新興技術

- 基於區塊鏈的健康資料安全

- AR/VR 醫療旅遊

- 當前的技術趨勢

- 醫療保險場景

- 消費者洞察

- 各地區醫院數量

- 各國的發展與舉措

- 患者/遊客的人口統計數據

- 投資前景

- 波特的分析

- PESTEL分析

- 差距分析

- 未來市場趨勢

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 心血管外科

- 整容手術

- 隆乳

- 植髮

- 其他整容手術

- 骨科手術

- 腫瘤治療

- 生育治療

- 減重手術

- 其他應用

第6章:市場估計與預測:依旅遊類型,2021 - 2034 年

- 主要趨勢

- 國內的

- 國際的

第7章:市場估計與預測:按國家/地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 土耳其

- 捷克共和國

- 亞太地區

- 日本

- 印度

- 泰國

- 韓國

- 新加坡

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 哥倫比亞

- 哥斯大黎加

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 8 章:醫療保健提供者

- 關鍵球員

- 康民國際醫院

- COMO 飯店及度假村

- 四季酒店

- 希爾頓全球控股公司

- IHH醫療保健

- 洲際集團

- KPJ醫療保健有限公司

- 仁愛醫療中心

- 馬卡蒂醫療中心

- 萬豪國際集團

- 國家心臟研究所(Institut Jantung Negara)

- 檳城安息日醫院

- 麗笙酒店集團

- 萊佛士醫療集團

- 瑰麗酒店集團

- 新加坡保健集團

- 聖路加醫療中心

- 雙威集團

- 新興企業

- AEK烏隆國際醫院

- Gojek

- Grab控股有限公司

- 卡瑪拉雅

- 基馬拉

- RAKxa

- 然禧國際醫院

The Global Medical Tourism Market was valued at USD 30.5 billion in 2024 and is estimated to grow at a CAGR of 16.8% to reach USD 142 billion by 2034.

Market growth is driven by government initiatives that simplify cross-border medical travel, the availability of affordable treatment options in developing regions, and the increasing number of patients suffering from chronic illnesses. The adoption of internationally recognized surgical standards has also encouraged confidence in medical procedures abroad. Countries across the Asia Pacific have emerged as prominent hubs, offering advanced care at lower costs while dedicating specialized resources to international patients. Travelers from Western nations often seek these destinations for quality medical services, and a considerable portion also combine their treatment with short wellness or recovery-focused trips. The appeal lies not only in affordability but also in shorter waiting periods, modern infrastructure, and specialized care. Rising health awareness, coupled with growing demand for elective procedures and lifestyle-related treatments, continues to fuel momentum. Together, these factors are establishing medical tourism as a preferred option for patients worldwide, with markets adapting rapidly to meet global demand.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $30.5 Billion |

| Forecast Value | $142 Billion |

| CAGR | 16.8% |

The cosmetic surgery segment held a 17% share in 2024, driven by the increasing popularity of procedures aimed at improving physical appearance, supported by innovations that have made treatments safer, more precise, and minimally invasive. Faster recovery periods and reduced costs have encouraged more patients to pursue cosmetic enhancements. The growing influence of digital platforms has also heightened awareness, especially among younger demographics, further boosting demand for cosmetic treatments and expanding their role within medical tourism.

The international segment held a 53.5% share in 2024, reflecting the steady rise in patients seeking treatment abroad. The appeal of traveling for healthcare includes access to advanced procedures, reduced expenses, and the opportunity to bypass lengthy waiting lists in home countries. This shift has strengthened the position of developing nations that provide high-quality services while remaining cost-competitive. Patients from various regions continue to select such destinations as preferred choices for diverse medical needs, reinforcing the global nature of this industry.

Europe Medical Tourism Market held a 36.5% share in 2024 and is projected to expand significantly in the years ahead. Many patients from North America, the Middle East, and neighboring countries prefer European destinations due to the combination of advanced healthcare infrastructure and relatively lower treatment costs. Several countries within Europe remain leading centers for attracting patients across multiple specialties, ensuring a strong role in global market expansion.

Key players in the Medical Tourism Market include Raffles Medical Group, Narayana Health, Johns Hopkins Hospital, Max Healthcare, Makati Medical Center, Fortis Healthcare Limited, Mayo Clinic, St. Luke's Medical Center, Anadolu Medical Center, Bumrungrad International Hospital, KPJ Healthcare Berhad, Proton Therapy Center, Mount Elizabeth Hospitals, Apollo Hospitals Group, Mahkota Medical Centre, Gleneagles Hospital, Asklepios Kliniken GmbH & Co. KGaA, and Cleveland Clinic.

To reinforce their market position, companies in medical tourism are pursuing diverse strategies. Leading hospitals and healthcare groups are expanding partnerships with travel agencies, insurance providers, and wellness centers to offer comprehensive packages that include treatment, accommodation, and aftercare. Significant investments are being made in advanced medical technologies and infrastructure to ensure internationally accredited standards of care. Many organizations are also targeting overseas patients with tailored marketing campaigns, multilingual services, and dedicated international patient departments. Expansion into emerging markets through satellite facilities and affiliations with regional hospitals helps increase accessibility and build trust among patients. Digital transformation, including telemedicine consultations and online booking platforms, has further strengthened outreach while enhancing the overall patient experience.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Application trends

- 2.2.3 Travel type trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Low cost of medical treatment in developing countries

- 3.2.1.2 Growing compliance towards international standards for surgical procedures

- 3.2.1.3 Various government policies to ease medical travel

- 3.2.1.4 Increasing prevalence of chronic diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Long wait time for certain medical procedures

- 3.2.2.2 Issue with patient follow-up and post-surgery complications

- 3.2.3 Opportunities

- 3.2.3.1 Development of health special economic zones

- 3.2.3.2 Digital healthcare and telemedicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.1.1 AI-powered translation tools

- 3.5.1.2 Digital wellness platforms

- 3.5.1.3 Electronic medical records (EMR) integration

- 3.5.2 Emerging technologies

- 3.5.2.1 Blockchain-based health data security

- 3.5.2.2 AR/VR for medical tourism

- 3.5.1 Current technological trends

- 3.6 Medical coverage scenario

- 3.7 Consumer insights

- 3.8 Number of hospitals by region

- 3.9 Developments and initiatives by country

- 3.10 Demographics of patients/tourists

- 3.11 Investment landscape

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

- 3.15 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers and acquisitions

- 4.5.2 Partnerships and collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiovascular surgery

- 5.3 Cosmetic surgery

- 5.3.1 Breast augmentation

- 5.3.2 Hair transplant

- 5.3.3 Other cosmetic surgeries

- 5.4 Orthopedic surgery

- 5.5 Oncology treatment

- 5.6 Fertility treatment

- 5.7 Bariatric surgery

- 5.8 Other applications

Chapter 6 Market Estimates and Forecast, By Travel Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Domestic

- 6.3 International

Chapter 7 Market Estimates and Forecast, By Country, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Turkey

- 7.3.7 Czech Republic

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 India

- 7.4.3 Thailand

- 7.4.4 South Korea

- 7.4.5 Singapore

- 7.4.6 Malaysia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Colombia

- 7.5.4 Costa Rica

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Healthcare Providers

- 8.1 Key players

- 8.1.1 Bumrungrad International Hospital

- 8.1.2 COMO Hotels and Resorts

- 8.1.3 Four Seasons Hotels

- 8.1.4 Hilton Worldwide Holdings Inc.

- 8.1.5 IHH Healthcare

- 8.1.6 InterContinental Group

- 8.1.7 KPJ Healthcare Berhad

- 8.1.8 Mahkota Medical Centre

- 8.1.9 Makati Medical Center

- 8.1.10 Marriott International

- 8.1.11 National Heart Institute (Institut Jantung Negara)

- 8.1.12 Penang Adventist Hospital

- 8.1.13 Radisson Hotel Group

- 8.1.14 Raffles Medical Group

- 8.1.15 Rosewood Hotel Group

- 8.1.16 SingHealth Group

- 8.1.17 St. Luke's Medical Center

- 8.1.18 Sunway Group

- 8.2 Emerging players

- 8.2.1 AEK Udon International Hospital

- 8.2.2 Gojek

- 8.2.3 Grab Holdings Ltd.

- 8.2.4 Kamalaya

- 8.2.5 Keemala

- 8.2.6 RAKxa

- 8.2.7 Yanhee International Hospital

牙科旅遊市場-全球產業規模、佔有率、趨勢、機會和預測,按服務(植牙、矯正)、提供者(醫院、牙科診所)、地區和競爭格局分類,2020-2030 年預測

牙科旅遊市場-全球產業規模、佔有率、趨勢、機會和預測,按服務(植牙、矯正)、提供者(醫院、牙科診所)、地區和競爭格局分類,2020-2030 年預測 醫療旅遊市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2024-2032)

醫療旅遊市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2024-2032) 牙科旅遊市場分析及預測(至2034年):類型、產品、服務、技術、應用、最終用戶、安裝類型、設備、解決方案

牙科旅遊市場分析及預測(至2034年):類型、產品、服務、技術、應用、最終用戶、安裝類型、設備、解決方案 醫療旅遊市場:全球產業分析、規模、佔有率、成長、趨勢與預測(2025-2032)

醫療旅遊市場:全球產業分析、規模、佔有率、成長、趨勢與預測(2025-2032) 2032 年醫療旅遊市場預測:按治療類型、旅客類型、服務提供者、預訂管道和地區進行的全球分析

2032 年醫療旅遊市場預測:按治療類型、旅客類型、服務提供者、預訂管道和地區進行的全球分析 全球牙科旅遊市場

全球牙科旅遊市場 2025 年至 2033 年醫療旅遊市場規模、佔有率、趨勢及預測(按治療類型和地區)醫療旅遊市場-2025年至2030年的預測全球生育旅遊市場全球睡眠旅遊市場

2025 年至 2033 年醫療旅遊市場規模、佔有率、趨勢及預測(按治療類型和地區)醫療旅遊市場-2025年至2030年的預測全球生育旅遊市場全球睡眠旅遊市場