|

市場調查報告書

商品編碼

1797834

液氫市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Liquid Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

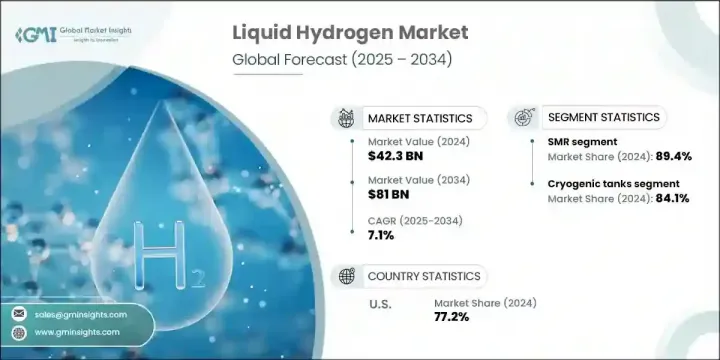

2024年,全球液氫市場規模達423億美元,預計2034年將以7.1%的複合年成長率成長,達到810億美元。氫能樞紐的建設預計將推動需求成長,因為這些樞紐是氫氣生產、儲存和分配的關鍵中心。技術供應商與能源服務公司之間的合作正在推動產業發展,促進創新,從而提高生產效率。

各國和各企業也在建立國際合作夥伴關係,以加速氫能技術進步並建立強大的全球供應鏈。這些合作旨在協調監管標準、匯集研發投資並支持跨境基礎設施建設。政府和私人企業之間的合資企業正在推動氫能樞紐、跨國管道、儲存網路和加氫站的建設,以確保可擴展性和效率。此外,各國正在建立戰略聯盟,以確保關鍵材料的獲取,促進電解槽製造領域的知識共享,並實現燃料電池、綠色氨和工業脫碳等氫能應用的商業化。此類跨國合作對於降低成本、克服技術障礙以及培育支持氣候目標和能源安全目標的全球互聯氫能經濟至關重要。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 423億美元 |

| 預測值 | 810億美元 |

| 複合年成長率 | 7.1% |

液氫市場依生產方法細分,主要包括煤氣化、電解和SMR(小型模組化反應器)。 SMR在2024年佔據了89.4%的市場佔有率,這得益於其在大規模製氫中的經濟可行性和效率。 SMR的成本優勢使其在天然氣資源豐富的地區成為首選。催化劑、製程效率和熱回收系統的不斷進步,正在增強SMR的運作效率,最大限度地減少排放,並提高整體永續性。

根據配銷通路,液氫市場分為管道和低溫儲罐。 2024年,低溫儲槽市場佔84.1%的佔有率。增強的隔熱技術顯著提高了低溫儲罐的效率,最大限度地減少了氫氣損失,並保持了穩定的儲存條件。先進材料的開發也降低了蒸發率,確保了液氫的安全可靠運輸。氫能樞紐和產業群聚正在蓬勃發展,透過廣泛的管道網路連接多個設施。

2024年,美國液氫市場規模達162億美元。政府支持力度加大、產業投資不斷增加以及環保意識日益增強是推動市場擴張的關鍵因素。強而有力的政策框架和財政激勵措施正在鼓勵各行各業採用氫能技術。各行各業正朝著永續發展目標邁進,鞏固了該地區在氫能創新和基礎設施建設領域的領先地位。

推動液氫市場創新和成長的知名公司包括殼牌、查特工業、岩穀株式會社、GENH2、液化空氣集團、普拉格能源、林德、薩爾茨堡鋁業集團、空氣化工產品公司、Engie、普萊克斯技術公司、無錫元通燃氣、川崎重工、梅塞爾、INOXCVA 和通用電氣家電。為了鞏固其在全球液氫市場的地位和領導地位,這些公司正在實施各種策略性措施。他們正在大力投資低溫儲存技術、先進液化系統和大型氫氣生產工廠的開發。他們與政府和研究機構的合作項目也很常見,旨在加速基礎設施建設和政策協調。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 2021-2034年價格趨勢分析

- 按生產方式

- 按地區

- 成本結構分析

- 主要生產基地列表

- 按國家

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 按地區分析公司市場佔有率

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

- 戰略儀表板

- 策略舉措

- 公司標竿分析

- 創新與技術格局

第5章:市場規模及預測:依生產方式,2021 - 2034 年

- 主要趨勢

- 瓦斯化

- 小型磁共振

- 電解

第6章:市場規模及預測:以分銷方式,2021 - 2034 年

- 主要趨勢

- 管道

- 低溫儲罐

第7章:市場規模及預測:依最終用途,2021 - 2034

- 主要趨勢

- 運輸

- 輕型車輛

- 丁型肝炎病毒

- 氫動力船

- 軌

- 港口機械

- 工程機械

- 化學

- 其他

第8章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 世界其他地區

第9章:公司簡介

- Air Liquide

- Air Products and Chemicals, Inc.

- Chart Industries

- Engie

- GE Appliances

- GENH2

- INOXCVA

- Iwatani Corporation

- Kawasaki Heavy Industries

- Linde

- Messer

- Plug Power

- Praxair Technology, Inc.

- Salzburger Aluminium Group

- Shell

- Wuxi Yuantong Gas

The Global Liquid Hydrogen Market generated USD 42.3 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 81 billion by 2034. The development of hydrogen hubs is expected to drive demand, as these locations serve as key centers for hydrogen production, storage, and distribution. Collaboration between technology providers and energy service companies is advancing the industry, fostering innovations that enhance production efficiency.

Countries and corporations are also forming international partnerships to accelerate hydrogen technology advancements and establish a robust global supply chain. These collaborations aim to harmonize regulatory standards, pool R&D investments, and support infrastructure development across borders. Joint ventures between governments and private players are driving the construction of hydrogen hubs, transnational pipelines, storage networks, and refueling stations to ensure scalability and efficiency. In addition, strategic alliances are being formed to secure access to critical materials, foster knowledge-sharing in electrolyzer manufacturing, and enable the commercialization of hydrogen-based applications such as fuel cells, green ammonia, and industrial decarbonization. Such cross-border efforts are essential to reducing costs, overcoming technical barriers, and fostering a globally interconnected hydrogen economy that supports climate goals and energy security objectives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $42.3 Billion |

| Forecast Value | $81 Billion |

| CAGR | 7.1% |

The liquid hydrogen market is segmented based on production methods, with key categories including coal gasification, electrolysis, and SMR. The SMR segment held 89.4% share in 2024, driven by its economic feasibility and efficiency in large-scale hydrogen production. Its cost advantage over alternative methods makes it a preferred choice in regions with abundant natural gas resources. Continuous advancements in catalysts, process efficiency, and heat recovery systems are enhancing SMR operations, minimizing emissions, and increasing overall sustainability.

Based on distribution channel the liquid hydrogen market is divided into pipelines and cryogenic tanks. Cryogenic tanks segment held 84.1% share in 2024. Enhanced insulation technologies have significantly improved cryogenic tank efficiency, minimizing hydrogen loss and maintaining stable storage conditions. The development of advanced materials has also reduced boil-off rates, ensuring the safe and reliable transportation of liquid hydrogen. Hydrogen hubs and industrial clusters are gaining momentum, connecting multiple facilities through an extensive pipeline network.

U.S. Liquid Hydrogen Market was valued at USD 16.2 billion in 2024. Rising government support, increasing industrial investments, and growing environmental consciousness are key factors fueling market expansion. Strong policy frameworks and financial incentives are encouraging the adoption of hydrogen technologies across various sectors. Industries are aligning with sustainability goals, reinforcing the region's position as a leader in hydrogen innovation and infrastructure development.

Eminent companies driving innovation and growth in the Liquid Hydrogen Market include Shell, Chart Industries, Iwatani Corporation, GENH2, Air Liquide, Plug Power, Linde, Salzburger Aluminium Group, Air Products and Chemicals, Inc., Engie, Praxair Technology, Inc., Wuxi Yuantong Gas, Kawasaki Heavy Industries, Messer, INOXCVA, and GE Appliances. To strengthen their presence and leadership in the global liquid hydrogen market, these companies are implementing a variety of strategic initiatives. They are heavily investing in the development of cryogenic storage technologies, advanced liquefaction systems, and large-scale hydrogen production plants. Collaborative ventures with governments and research institutions are common, aimed at accelerating infrastructure development and policy alignment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Production trends

- 2.4 Distribution trends

- 2.5 End use trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Price trend analysis, 2021-2034

- 3.2.1 By production method

- 3.2.2 By region

- 3.3 Cost structure analysis

- 3.4 List of key manufacturing sites

- 3.4.1 By country

- 3.5 Regulatory landscape

- 3.6 Industry impact forces

- 3.6.1 Growth drivers

- 3.6.2 Industry pitfalls & challenges

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.8.1 Bargaining power of suppliers

- 3.8.2 Bargaining power of buyers

- 3.8.3 Threat of new entrants

- 3.8.4 Threat of substitutes

- 3.9 PESTEL analysis

- 3.9.1 Political factors

- 3.9.2 Economic factors

- 3.9.3 Social factors

- 3.9.4 Technological factors

- 3.9.5 Legal factors

- 3.9.6 Environmental factors

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Rest of World

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Production Method, 2021 - 2034 (USD Billion & MT)

- 5.1 Key trends

- 5.2 Coal Gasification

- 5.3 SMR

- 5.4 Electrolysis

Chapter 6 Market Size and Forecast, By Distribution Method, 2021 - 2034 (USD Billion & MT)

- 6.1 Key trends

- 6.2 Pipelines

- 6.3 Cryogenic Tanks

Chapter 7 Market Size and Forecast, By End Use, 2021 - 2034 (USD Billion & MT)

- 7.1 Key trends

- 7.2 Transportation

- 7.2.1 LDV

- 7.2.2 HDV

- 7.2.3 Hydrogen Ship

- 7.2.4 Rail

- 7.2.5 Port Machinery

- 7.2.6 Construction Machinery

- 7.3 Chemical

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion & MT)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Rest of World

Chapter 9 Company Profiles

- 9.1 Air Liquide

- 9.2 Air Products and Chemicals, Inc.

- 9.3 Chart Industries

- 9.4 Engie

- 9.5 GE Appliances

- 9.6 GENH2

- 9.7 INOXCVA

- 9.8 Iwatani Corporation

- 9.9 Kawasaki Heavy Industries

- 9.10 Linde

- 9.11 Messer

- 9.12 Plug Power

- 9.13 Praxair Technology, Inc.

- 9.14 Salzburger Aluminium Group

- 9.15 Shell

- 9.16 Wuxi Yuantong Gas

化學液氫市場規模、佔有率和成長分析:按純度、製造方法、儲存類型、應用、最終用戶和地區分類-2026-2033年產業預測

化學液氫市場規模、佔有率和成長分析:按純度、製造方法、儲存類型、應用、最終用戶和地區分類-2026-2033年產業預測 液氫市場規模、佔有率及成長分析(依生產方式、分銷方式、終端用戶產業及地區分類)-2026-2033年產業預測

液氫市場規模、佔有率及成長分析(依生產方式、分銷方式、終端用戶產業及地區分類)-2026-2033年產業預測 全球煤炭氣化液氫市場全球電解液氫市場化學液氫全球市場全球液氫市場

全球煤炭氣化液氫市場全球電解液氫市場化學液氫全球市場全球液氫市場 化學液氫市場機會、成長動力、產業趨勢分析及2025-2034年預測

化學液氫市場機會、成長動力、產業趨勢分析及2025-2034年預測 液氫-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太液氫 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美液氫 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

液氫-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太液氫 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美液氫 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)