|

市場調查報告書

商品編碼

1797706

光纖元件市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Fiber Optic Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

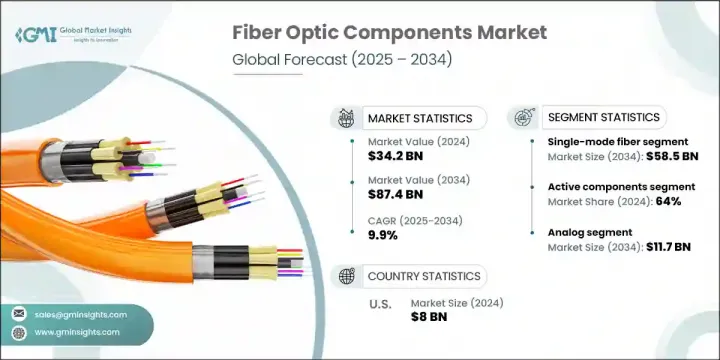

2024 年全球光纖元件市場價值為 342 億美元,預計到 2034 年將以 9.9% 的複合年成長率成長至 874 億美元。這一強勁成長主要得益於雲端運算、邊緣基礎設施和超大規模資料中心擴張所帶來的高速資料傳輸需求。物聯網技術與工業和城市應用中互聯生態系統的日益整合進一步增強了需求。隨著各行各業實現現代化和數位轉型,對快速、可靠通訊基礎設施的需求正在推動多個行業採用光纖技術。各國政府(尤其是在發展中經濟體)對寬頻部署、智慧電網和數位服務的投資正在加速全球光纖元件市場的滲透。光纖基礎設施在實現資料密集和延遲敏感型環境中的高效能連接方面發揮著至關重要的作用。

5G 的推出顯著增加了對光纖組件的需求,尤其是在網路前傳和回傳領域。電信業者正在快速擴展其基礎設施,以滿足低延遲、高頻寬的需求。光纖連接對於智慧城市框架、物聯網、監控和數位服務平台也至關重要。這些變化推動了市場對能夠提供無縫通訊和高彈性性能的組件的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 342億美元 |

| 預測值 | 874億美元 |

| 複合年成長率 | 9.9% |

2024年,有源元件領域佔據光纖元件市場64%的領先佔有率。 5G網路、資料中心和城域光纖基礎設施中收發器、放大器和調製器的大規模部署將繼續推動該領域的發展。隨著系統朝向更高的連接埠密度和更低的光學層功耗發展,對緊湊、節能設計的需求也日益成長。

預計到2034年,單模光纖市場規模將達585億美元。其在長距離傳輸、低衰減以及城域網路和核心網路應用日益普及方面的優勢,鞏固了其重要性。海底通訊系統和5G回程基礎設施的擴張顯著促進了該領域的發展勢頭,尤其是在資料消費模式轉向高吞吐量、雲端原生應用的背景下。

2024年,美國光纖元件市場規模達80億美元。人工智慧驅動的工作負載成長、業務快速遷移至雲端以及下一代資料中心的擴張,正在推動對先進光纖解決方案的需求。美國國內供應商正致力於開發低延遲、高容量、熱效率更高、跨平台互通性更強的光學元件,以滿足不斷變化的效能需求。

光纖元件市場的公司包括藤倉、Broadex Technologies、Ciena、思科系統、古河電工、光迅科技、康寧、3M、博通、安費諾和康普。為了鞏固其在光纖元件市場的地位,主要參與者正在採取多管齊下的策略。領先的公司優先考慮研發投資,以提供針對人工智慧、雲端運算和5G基礎設施量身定做的緊湊、節能、高速的光學技術。與電信業者和超大規模企業的合作有助於將產品創新與部署需求結合。擴大製造能力並加強區域供應鏈可以縮短交付週期,並支持地方政府的數位化專案。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 物聯網和連網設備的普及率不斷提高

- 全球5G基礎設施擴張

- 資料中心和雲端運算服務的成長

- 智慧城市和智慧電網的普及

- 軍事和航太應用的需求不斷成長

- 產業陷阱與挑戰

- 初始部署和安裝成本高

- 網路基礎設施管理的複雜性

- 市場機會

- 發展中經濟體的新興需求

- 光纖在5G及更高技術中的整合

- 高頻寬應用(AR/VR、串流媒體、AI)的需求不斷成長

- 光纖在國防和航太領域的應用

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各區域市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按組件類型,2021 - 2034 年

- 主要趨勢

- 主動元件

- 發射器

- 接收器

- 光放大器

- 被動元件

- 光纖電纜

- 連接器和適配器

- 耦合器和分離器

- 光開關

- 其他

第6章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 單模光纖

- 多模光纖

第7章:市場估計與預測:按資料傳輸速率,2021 - 2034 年

- 主要趨勢

- 低於 10 GBPS

- 10 至 40 GBPS

- 40 至 100 GBPS

- 超過 100 GBPS

第8章:市場估計與預測:按技術,2021 - 2034 年

- 主要趨勢

- 類比光纖元件

- 數位光纖裝置

第9章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 電信和資料通訊

- 長途傳輸網路

- 城域網路/核心網

- 接網路

- 移動回傳/前傳

- 企業網路(LAN/WAN)

- 其他

- 資料中心和雲端基礎設施

- 資料中心內部連接

- 跨資料中心

- 高速收發器

- 儲存區域網路 (SAN)

- 其他

- 軍事與國防

- 安全的戰術通訊網路

- 雷達和感測器系統

- 指揮和控制系統

- 航空電子和海軍通訊系統

- 其他

- 醫療保健

- 醫學影像系統

- 雷射傳輸系統

- 生物醫學感測器和儀器

- 醫院網路基礎設施

- 其他

- 工業自動化

- 工廠自動化和製程控制網路

- 機器人和機器視覺系統

- 遙感和監測

- 工業乙太網路

- 其他

- 廣播和視訊傳輸

- 現場活動廣播基礎設施

- 演播室到發射機鏈路 (STL)

- 有線電視和 IPTV 發行網路

- 室外轉播車和移動製作

- 其他

- 石油和天然氣

- 井下光纖感

- 海底通訊鏈路

- 管道監測和洩漏檢測系統

- 遠端站點連線

- 其他

- 航太

- 航空電子資料網路

- 衛星地面站連接

- 機上娛樂 (IFE) 系統

- 太空船光通訊系統

- 其他

- 其他

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Global Key Players

- Regional Key Players

- 利基市場參與者/顛覆者

- 3M

- 光迅科技

- 博德科技

- 立訊精密

- 奧普特森科技

- 先光

The Global Fiber Optic Components Market was valued at USD 34.2 billion in 2024 and is estimated to grow at a CAGR of 9.9% to reach USD 87.4 billion by 2034. This robust growth is primarily driven by the increasing need for high-speed data transmission, fueled by the expansion of cloud computing, edge infrastructure, and hyperscale data centers. The rising integration of IoT technologies and connected ecosystems across industrial and urban applications is further strengthening demand. As industries modernize and shift towards digitalization, the need for fast, reliable communication infrastructure is driving the adoption of fiber optics across several sectors. Government investments in broadband rollout, smart grids, and digital services-especially in developing economies-are accelerating market penetration of fiber optic components globally. The role of fiber infrastructure has become essential in enabling high-performance connectivity across data-intensive and latency-sensitive environments.

The rollout of 5G is significantly increasing the need for fiber optic components, particularly in network fronthaul and backhaul segments. Telecom providers are rapidly scaling their infrastructure to meet low-latency, high-bandwidth requirements. Fiber-based connectivity is also critical for smart city frameworks, powering IoT, surveillance, and digital service platforms. These changes are pushing the market for components capable of delivering seamless communication and resilient performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.2 Billion |

| Forecast Value | $87.4 Billion |

| CAGR | 9.9% |

In 2024, the active components segment held the leading share of 64% in the fiber optic components market. High-volume deployment of transceivers, amplifiers, and modulators in 5G networks, data centers, and metro optical infrastructure continues to propel this segment. The demand for compact, energy-efficient designs is increasing as systems move toward higher port densities and reduced power consumption across optical layers.

The single-mode fiber optics segment is anticipated to generate USD 58.5 billion by 2034. Their advantage in long-range transmission, lower attenuation, and increasing use in metro and core network applications solidifies their relevance. The expansion of submarine communication systems and 5G backhaul infrastructure has significantly contributed to this segment's momentum, particularly as data consumption patterns shift toward high-throughput, cloud-native applications.

U.S. Fiber Optic Components Market was valued at USD 8 billion in 2024. Growth in AI-driven workloads, rapid migration to the cloud, and expansion of next-gen data centers are fueling demand for advanced fiber solutions. Domestic suppliers are focusing on developing low-latency, high-capacity optical components with better thermal efficiency and cross-platform interoperability to meet evolving performance requirements.

Companies operating in the Fiber Optic Components Market include Fujikura, Broadex Technologies, Ciena, Cisco Systems, Furukawa Electric, Accelink Technologies, Corning, 3M, Broadcom, Amphenol, and CommScope. To strengthen their presence in the Fiber Optic Components Market, key players are embracing a multi-pronged strategy. Leading companies are prioritizing R&D investments to deliver compact, energy-efficient, and high-speed optical technologies tailored for AI, cloud, and 5G infrastructure. Partnerships with telecom operators and hyperscalers help align product innovation with deployment needs. Expanding manufacturing capabilities and strengthening regional supply chains enable faster delivery cycles and support local government digitalization programs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Component type trends

- 2.2.2 Type trends

- 2.2.3 Data transfer rate trends

- 2.2.4 Technology trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing penetration of IoT and connected devices

- 3.2.1.2 Expansion of 5G infrastructure globally

- 3.2.1.3 Growth in data centers and cloud computing services

- 3.2.1.4 Proliferation of smart cities and smart grids

- 3.2.1.5 Growing demand from military and aerospace applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial deployment and installation costs

- 3.2.2.2 Complexity in network infrastructure management

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging demand in developing economies

- 3.2.3.2 Integration of fiber optics in 5g and beyond technologies

- 3.2.3.3 Growing need for high-bandwidth applications (AR/VR, streaming, AI)

- 3.2.3.4 Adoption of fiber optics in defense and aerospace sectors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Active components

- 5.2.1 Transmitters

- 5.2.2 Receivers

- 5.2.3 Optical amplifiers

- 5.3 Passive components

- 5.3.1 Fiber optic cables

- 5.3.2 Connectors & adapters

- 5.3.3 Couplers & splitters

- 5.3.4 Optical switches

- 5.3.5 Others

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Single-mode fiber

- 6.3 Multi-mode fiber

Chapter 7 Market Estimates and Forecast, By Data Transfer Rate, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Less than 10 GBPS

- 7.3 10 to 40 GBPS

- 7.4 40 to 100 GBPS

- 7.5 More than 100 GBPS

Chapter 8 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 Analog fiber optic components

- 8.3 Digital fiber optic components

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion)

- 9.1 Key trends

- 9.2 Telecommunications & data communication

- 9.2.1 Long-haul transmission networks

- 9.2.2 Metro/core networks

- 9.2.3 Access networks

- 9.2.4 Mobile backhaul / fronthaul

- 9.2.5 Enterprise networks (LAN/WAN)

- 9.2.6 Others

- 9.3 Data centers & cloud infrastructure

- 9.3.1 Intra-data center connectivity

- 9.3.2 Inter-data center

- 9.3.3 High-speed transceivers

- 9.3.4 Storage area networks (SAN)

- 9.3.5 Others

- 9.4 Military & defense

- 9.4.1 Secure tactical communication networks

- 9.4.2 Radar & sensor systems

- 9.4.3 Command and control systems

- 9.4.4 Avionics and naval communication systems

- 9.4.5 Others

- 9.5 Medical & healthcare

- 9.5.1 Medical imaging systems

- 9.5.2 Laser delivery systems

- 9.5.3 Biomedical sensors & instrumentation

- 9.5.4 Hospital network infrastructure

- 9.5.5 Others

- 9.6 Industrial automation

- 9.6.1 Factory automation and process control networks

- 9.6.2 Robotics & machine vision systems

- 9.6.3 Remote sensing and monitoring

- 9.6.4 Industrial Ethernet

- 9.6.5 Others

- 9.7 Broadcasting & video transmission

- 9.7.1 Live event broadcasting infrastructure

- 9.7.2 Studio-to-transmitter links (STL)

- 9.7.3 Cable TV & IPTV distribution networks

- 9.7.4 Outside broadcast (OB) vans & mobile production

- 9.7.5 Others

- 9.8 Oil & gas

- 9.8.1 Downhole fiber optic sensing

- 9.8.2 Subsea communication links

- 9.8.3 Pipeline monitoring & leak detection systems

- 9.8.4 Remote site connectivity

- 9.8.5 Others

- 9.9 Aerospace

- 9.9.1 Avionics data networks

- 9.9.2 Satellite ground station connectivity

- 9.9.3 In-flight entertainment (IFE) systems

- 9.9.4 Spacecraft optical communication systems

- 9.9.5 Others

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Broadcom

- 11.1.2 Cisco Systems

- 11.1.3 Corning

- 11.1.4 Fujikura

- 11.1.5 Huawei Technologies

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Ciena

- 11.2.1.2 CommScope

- 11.2.1.3 Lumentum Holdings

- 11.2.1.4 Viavi Solutions

- 11.2.1.5 TE Connectivity

- 11.2.2 Europe

- 11.2.2.1 Amphenol

- 11.2.2.2 Molex

- 11.2.2.3 Prysmian Group

- 11.2.3 APAC

- 11.2.3.1 Furukawa Electric

- 11.2.3.2 Sumitomo Electric

- 11.2.3.3 ZTE

- 11.2.1 North America

- 11.3 Niche Players / Disruptors

- 11.3.1 3Ms

- 11.3.2 Accelink Technologies

- 11.3.3 Broadex Technologies

- 11.3.4 Luxshare-ICT

- 11.3.5 Optosun Technology

- 11.3.6 Senko

光纖組件市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2024-2032 年)

光纖組件市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2024-2032 年) 光隔離器:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

光隔離器:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 光纖元件市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、資料速率、應用、地區和競爭細分,2020-2030 年預測)

光纖元件市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、資料速率、應用、地區和競爭細分,2020-2030 年預測) 2025年全球光纖元件市場報告

2025年全球光纖元件市場報告 光纖組件市場按組件類型、傳輸模式、資料速率、應用、最終用戶和銷售管道分類 - 2025-2030 年全球預測

光纖組件市場按組件類型、傳輸模式、資料速率、應用、最終用戶和銷售管道分類 - 2025-2030 年全球預測 全球光隔離器市場全球被動光元件市場全球光擴大機市場光纖放大器市場:未來預測(2025-2030)

全球光隔離器市場全球被動光元件市場全球光擴大機市場光纖放大器市場:未來預測(2025-2030) 被動光學組件市場:按元件、按材料類型、按應用、按地區

被動光學組件市場:按元件、按材料類型、按應用、按地區