|

市場調查報告書

商品編碼

1773464

永續寵物產品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Sustainable Pet Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

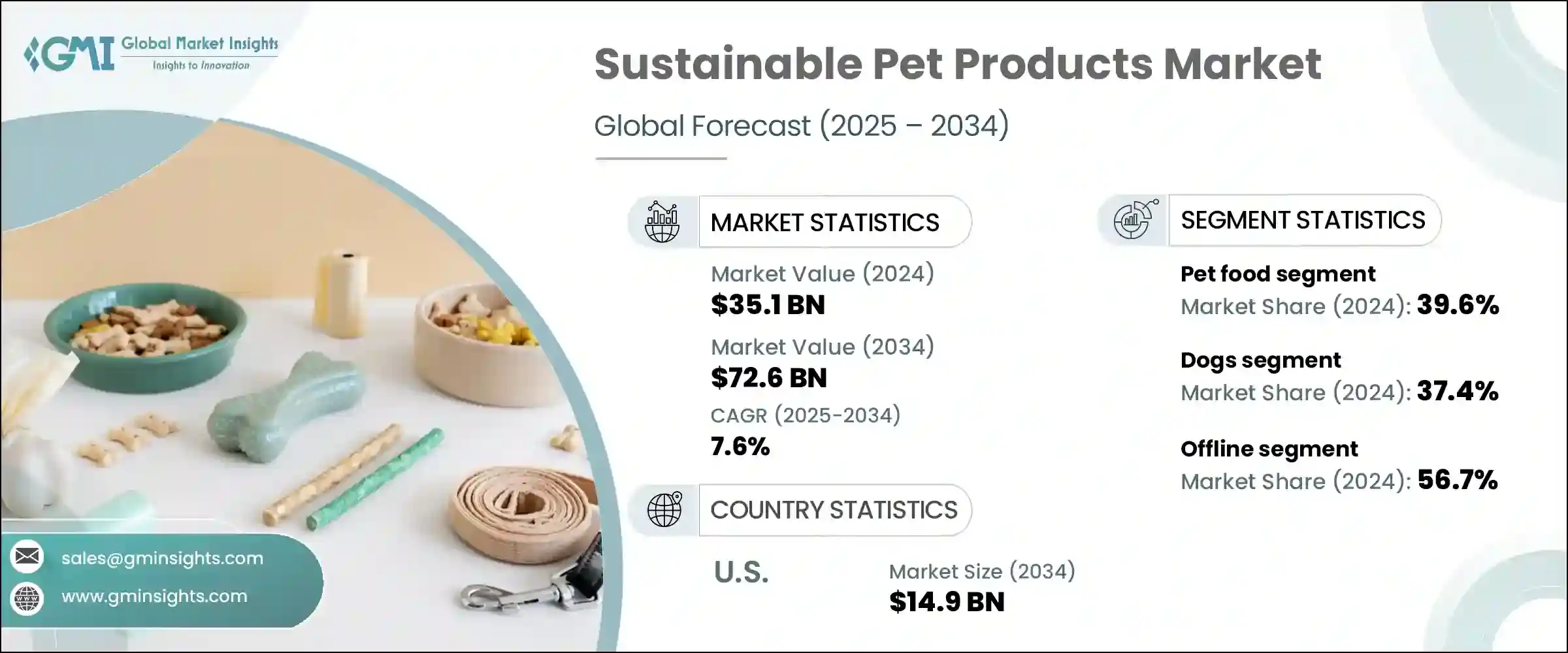

2024年,全球永續寵物產品市場規模達351億美元,預計到2034年將以7.6%的複合年成長率成長,達到726億美元。推動這一成長的因素包括日益增強的環保意識,寵物主人將寵物視為家庭成員,並增加對優質、符合道德規範產品的投資。對可生物分解垃圾袋、非塑膠美容用品、負責任採購的寵物食品和可回收包裝的需求,反映了人們普遍轉向環保寵物護理的趨勢。不斷成長的可支配收入推動了以健康為重點的寵物產品的支出,新興和成熟品牌都在材料、配方和包裝方面進行創新,以滿足這些不斷變化的需求。

永續寵物照護的興起正在重塑整個產業,其核心是健康趨勢、環境問題和生活方式的改變。如今,消費者的價值觀與寵物選擇的產品一致,優先考慮寵物的健康、符合道德的採購以及對環境的最小影響。隨著寵物主人環保意識的增強,他們正在積極地用可生物分解、零殘忍或可回收材料製成的替代品來取代傳統產品。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 351億美元 |

| 預測值 | 726億美元 |

| 複合年成長率 | 7.6% |

此外,植物性飲食、清潔標籤配方和無毒美容解決方案的日益普及,反映了更廣泛的文化向更全面、更理性的生活方式的轉變。這種轉變並非曇花一現,而是一場長期的變革,永續性將成為寵物護理產品購買決策的標準期望,影響整個產業的產品開發、包裝設計和行銷策略。

2024年,永續寵物食品市場佔39.6%的市場佔有率,預計複合年成長率為8%。越來越多的寵物主人選擇有機、來源可靠且營養豐富的食品,以支持寵物的整體健康和福祉。人們對傳統肉類飲食對環境影響的擔憂,正激發人們對替代蛋白質的興趣,例如昆蟲蛋白、植物性蛋白質或實驗室培育蛋白。消費者重視那些採購透明、標籤清潔且包裝環保的品牌。

2024年,狗狗佔據寵物類別的主導地位,佔據37.4%的佔有率,預計到2034年將以8.2%的複合年成長率成長。主人與狗狗之間深厚的情感紐帶推動了永續產品支出的成長,包括可生物分解的垃圾袋、植物性食品以及由再生材料或環保紡織品製成的配件。這種需求與寵物人性化趨勢的興起直接相關。

美國永續寵物產品市場佔60.2%的市場佔有率,預計到2034年將達到149億美元。高寵物擁有率以及消費者對環保產品的興趣(在強勁的零售和電商管道的支持下)正在推動這一成長。美國公司提供植物性寵物食品、可生物分解垃圾袋和永續包裝產品,以滿足寵物主人不斷變化的需求。

該領域的領導企業包括 West Paw、Pawz、Beco Pets、Kurgo、Ruffwear、Spectrum Brands、高露潔棕欖、Jiminy's、Petcurean、Freshpet、Petco、Green Pet Shop、RC Pet Products、Purina 和 Hurtta。永續寵物產品領域的頂級品牌正在大力投資環保創新和供應鏈透明度,以贏得消費者的忠誠度。他們正在擴展產品組合,包括植物組成、可生物分解材料和可回收包裝。與永續材料供應商和環境認證機構的合作確保了產品的可信度。許多公司正在利用全通路分銷策略——將零售業務與強大的電商業務相結合——來覆蓋更廣泛的受眾。透過社群媒體、影響力合作和社群參與講述品牌故事有助於凸顯品牌價值。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 寵物人性化趨勢日益明顯

- 消費者在寵物照護方面的支出增加

- 消費者對道德實踐的需求

- 循環經濟中的經濟機遇

- 產業陷阱與挑戰

- 寵物產品需求的季節性

- 發展中和低度開發地區缺乏意識且支出低

- 寵物照護費用高

- 機會

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監理框架

- 標準和認證

- 環境法規

- 進出口法規

- 貿易統計(HS編碼:33051090)

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL分析

- 消費者行為分析

- 購買模式

- 偏好分析

- 消費者行為的區域差異

- 電子商務對購買決策的影響

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021-2034

- 主要趨勢

- 寵物食品

- 寵物配件

- 寵物護理產品

- 寵物服飾和寢具

第6章:市場估計與預測:依寵物類型,2021-2034

- 主要趨勢

- 狗

- 貓

- 鳥類

- 小動物(如兔子、倉鼠)

- 魚類和爬蟲類

- 其他(例如外來寵物)

第7章:市場估計與預測:依價格,2021-2034 年

- 主要趨勢

- 低的

- 中等的

- 高的

第8章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 網路零售

- 電子商務平台(亞馬遜、Chewy 等)

- 品牌自有網站

- 線下零售

- 寵物專賣店

- 超市和大賣場

- 獸醫診所

- 生態/有機商店

第9章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Beco Pets

- Colgate-Palmolive

- Freshpet

- Green Pet Shop

- Hurtta

- Jiminy's

- Kurgo

- Pawz

- Petco

- Petcurean

- Purina

- RC Pet Products

- Ruffwear

- Spectrum Brands

- West Paw

The Global Sustainable Pet Products Market was valued at USD 35.1 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 72.6 billion by 2034. This expansion is driven by increasingly eco-conscious pet owners who treat their pets as family members and are investing more in premium, ethically produced goods. Demand for biodegradable waste bags, non-plastic grooming items, responsibly sourced pet food, and recyclable packaging reflects a broader shift toward environmentally friendly pet care. Rising disposable incomes are fueling spending on health-focused pet products, and both emerging and established brands are innovating in materials, formulations, and packaging to meet these evolving expectations.

This surge in sustainable pet care is reshaping the industry, with health trends, environmental concerns, and lifestyle changes at its core. Consumers are now aligning their values with the products they choose for their pets, prioritizing wellness, ethical sourcing, and minimal environmental impact. As pet owners become more eco-aware, they are actively replacing conventional products with alternatives made from biodegradable, cruelty-free, or recycled materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $35.1 Billion |

| Forecast Value | $72.6 Billion |

| CAGR | 7.6% |

Additionally, the rising popularity of plant-based diets, clean-label formulations, and toxin-free grooming solutions reflects a broader cultural shift toward holistic, conscious living. This transformation is not just a passing trend-it signals a long-term movement where sustainability becomes a standard expectation in pet care purchasing decisions, influencing product development, packaging design, and marketing strategies across the sector.

In 2024, the sustainable pet food segment held a 39.6% share and is expected to grow at an 8% CAGR. Pet owners are increasingly choosing organic, responsibly sourced, and nutritionally dense food options to support their pets' overall health and well-being. Concerns over the environmental footprint of traditional meat-based diets are boosting interest in alternative proteins like insect-based, plant-based, or lab-grown options. Consumers value brands that practice transparent sourcing, clean labeling, and eco-friendly packaging.

The dog segment dominated pet categories in 2024, capturing 37.4% share, and is forecasted to grow at 8.2% CAGR through 2034. The strong emotional bond between owners and dogs is driving increased spending on sustainable products, including biodegradable waste bags, plant-based foods, and accessories made from recycled materials or eco-friendly textiles. This demand is directly tied to the rising trend of pet humanization.

U.S. Sustainable Pet Products Market held a 60.2% share and is projected to reach USD 14.9 billion by 2034. High pet ownership rates and consumer interest in eco-conscious products-supported by robust retail and e-commerce channels-are propelling this growth. U.S. companies offer plant-based pet foods, biodegradable waste bags, and sustainably packaged goods to meet pet parents' evolving needs.

Leading players in this space include West Paw, Pawz, Beco Pets, Kurgo, Ruffwear, Spectrum Brands, Colgate Palmolive, Jiminy's, Petcurean, Freshpet, Petco, Green Pet Shop, RC Pet Products, Purina, and Hurtta. Top brands in the sustainable pet products arena are investing heavily in eco-friendly innovation and supply chain transparency to capture consumer loyalty. They are expanding their portfolios to include plant-based ingredients, biodegradable materials, and recyclable packaging. Partnerships with sustainable material suppliers and environmental certification bodies ensure product credibility. Many companies are leveraging omnichannel distribution strategies-combining retail presence with strong e-commerce-to reach a wider audience. Storytelling through social media, influencer collaborations, and community engagement helps highlight brand values.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Pet type

- 2.2.3 Price

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing trend of pet humanization

- 3.2.1.2 Higher consumer spending on pet care

- 3.2.1.3 Consumer demand for ethical practices

- 3.2.1.4 Economic opportunities in the circular economy

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Seasonality in pet products demand

- 3.2.2.2 Lack of awareness & low spending in developing and under-developed regions

- 3.2.2.3 High pet care cost

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics (HS code: 33051090)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behaviour analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behaviour

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Pet food

- 5.3 Pet accessories

- 5.4 Pet care products

- 5.5 Pet apparel and bedding

Chapter 6 Market Estimates & Forecast, By Pet Type, 2021-2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Birds

- 6.5 Small animals (e.g., rabbits, hamsters)

- 6.6 Fish & reptiles

- 6.7 Others (e.g., exotic pets)

Chapter 7 Market Estimates & Forecast, By Price, 2021-2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Online retail

- 8.2.1 E-commerce platforms (Amazon, Chewy, etc.)

- 8.2.2 Brand-owned websites

- 8.3 Offline retail

- 8.3.1 Pet specialty stores

- 8.3.2 Supermarkets and hypermarkets

- 8.3.3 Veterinary clinics

- 8.3.4 Eco/organic stores

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Beco Pets

- 10.2 Colgate-Palmolive

- 10.3 Freshpet

- 10.4 Green Pet Shop

- 10.5 Hurtta

- 10.6 Jiminy's

- 10.7 Kurgo

- 10.8 Pawz

- 10.9 Petco

- 10.10 Petcurean

- 10.11 Purina

- 10.12 RC Pet Products

- 10.13 Ruffwear

- 10.14 Spectrum Brands

- 10.15 West Paw

循環寵物用品市場預測至2034年-全球分析(按產品類型、材料類型、循環模式、寵物類型、價格範圍、分銷管道、最終用戶和地區分類)

循環寵物用品市場預測至2034年-全球分析(按產品類型、材料類型、循環模式、寵物類型、價格範圍、分銷管道、最終用戶和地區分類) 2026-2030年全球寵物用品市場

2026-2030年全球寵物用品市場 寵物用品市場規模、佔有率、趨勢和預測:按產品類型、寵物類型、分銷管道和地區分類,2026-2034 年

寵物用品市場規模、佔有率、趨勢和預測:按產品類型、寵物類型、分銷管道和地區分類,2026-2034 年 寵物零食分配器市場:2026-2032年全球市場預測(按產品類型、連接方式、最終用戶和分銷管道分類)個人化時尚寵物服飾及配件市場預測至2034年-按產品類型、個人化方式、材料、應用、最終用戶及地區分類的全球分析

寵物零食分配器市場:2026-2032年全球市場預測(按產品類型、連接方式、最終用戶和分銷管道分類)個人化時尚寵物服飾及配件市場預測至2034年-按產品類型、個人化方式、材料、應用、最終用戶及地區分類的全球分析 全球寵物床市場規模、佔有率、趨勢和成長分析報告(2026-2034年)寵物用品市場:依動物種類、產品類型、價格範圍、材質和通路分類-全球預測(2026-2032 年)寵物咖啡木磨牙棒市場:按動物類型、產品類型、口味、生命階段、原料品質和通路分類,全球預測,2026-2032年全球電動寵物按摩器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球寵物床市場規模、佔有率、趨勢和成長分析報告(2026-2034年)寵物用品市場:依動物種類、產品類型、價格範圍、材質和通路分類-全球預測(2026-2032 年)寵物咖啡木磨牙棒市場:按動物類型、產品類型、口味、生命階段、原料品質和通路分類,全球預測,2026-2032年全球電動寵物按摩器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 寵物床市場 - 全球產業規模、佔有率、趨勢、機會及預測(按床型、材料類型、分銷管道、地區和競爭格局分類,2021-2031年)

寵物床市場 - 全球產業規模、佔有率、趨勢、機會及預測(按床型、材料類型、分銷管道、地區和競爭格局分類,2021-2031年)