|

市場調查報告書

商品編碼

1844320

寵物配件市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Pet Accessories Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

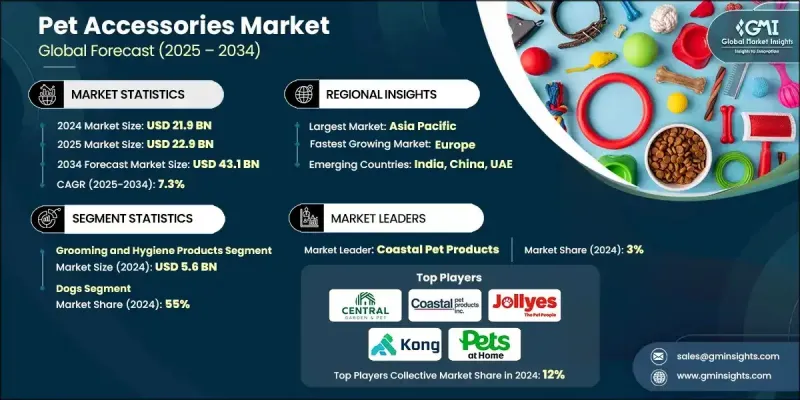

2024 年全球寵物配件市場價值為 219 億美元,預計將以 7.3% 的複合年成長率成長,到 2034 年達到 431 億美元。

城市、鄉村和郊區寵物擁有率的不斷上升,持續塑造市場的未來。隨著越來越多的家庭收養寵物,對必需品和小眾配件的需求都在激增。這為品牌創新和滿足寵物主人不斷變化的需求打開了大門。消費者對寵物健康、舒適度和參與度的意識日益增強,促使製造商探索新的產品類別,並改進設計,以反映當前的生活方式和價值觀,例如環保意識和個人化。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 219億美元 |

| 預測值 | 431億美元 |

| 複合年成長率 | 7.3% |

一些國家推出了鼓勵寵物收養的政策,加上可支配收入的提高,進一步推動了寵物擁有量的增加。這一趨勢也激發了人們對高階多功能產品的興趣,例如智慧項圈、人體工學玩具和人工智慧餵食器。分銷網路的增強,尤其是透過線上平台,正在擴大產品的可及性。從健身監測器到自動餵食系統,科技與配件的整合正成為主流,而新興經濟體則在推動產品價格的降低與創新。隨著各行各業擁抱數位商務和數據驅動的客製化,全球市場正在不斷湧現新的成長途徑。

2024年,寵物美容和衛生相關配件的市場規模達到56億美元,預計到2034年將以8%的複合年成長率成長。越來越多的寵物主人選擇互動玩具和衛生用品,以促進精神刺激和身體活動。這些玩具現在採用可生物分解和可回收的材料製成,以符合環保價值。永續發展的趨勢也影響寵物護理領域的設計決策和購買模式,使綠色替代品成為產品開發的驅動力。

寵物狗市場佔了55%的佔有率,預計2025年至2034年的複合年成長率將達到7.5%。寵物主人現在正在投資增強健康的配件,例如矯形床上用品、數位健康追蹤器和營養補充包。個人化配件,包括訂製服裝和刻字標籤,在狗主人中越來越常見,他們現在不僅重視寵物的舒適度和個性,也同樣重視自己的舒適度和個性。隨著寵物與人類關係的加深,專用配件的支出持續成長。

美國寵物配件市場佔76%的市場佔有率,2024年市場規模達59億美元。將寵物視為家庭成員的文化轉變持續影響消費者的消費行為。美國消費者擴大選擇智慧寵物配件,包括攝影機、GPS追蹤器和自動化系統。環保包裝和永續生產方式也越來越受到美國消費者的重視,這進一步增強了消費者對負責任的寵物產品的需求。

影響全球寵物配件市場的關鍵公司包括 KONG Company、Red Dingo、Outward Hound、Pets at Home Group、Jollyes Pet Superstores、ZippyPaws、Coastal Pet Products、Central Garden & Pet、Ferplast、Merrick Pet Care、Rogz Pet Gear、Hartz Mountain、Nestle Purina PetCare、MidWest for ProductsCare、MidWest for Productss 和 Pettz。寵物配件市場的領導者正在優先考慮產品創新、高階化和永續性,以保持競爭力。許多品牌正在推出由 GPS、健康監測和自動化等互聯技術支援的智慧寵物產品,以滿足現代生活方式。客製化產品(例如訂製項圈或量身定做的服裝)正在推出,以吸引尋求個人化的寵物主人。公司也正在投資永續材料和可回收包裝,以順應日益成長的環保意識。與零售連鎖店的策略合作以及透過電子商務平台擴大其數位影響力使公司能夠接觸到更廣泛的受眾。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 寵物主人數量不斷增加

- 寵物人性化趨勢日益明顯

- 消費者在寵物照護方面的支出增加

- 產業陷阱與挑戰

- 寵物服裝和配件的季節性

- 供應鏈中斷

- 市場競爭激烈

- 機會

- 環保且永續

- 智慧/科技配件

- 多功能且節省空間的設計

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監管格局

- 標準和合規性要求

- 區域監理框架

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特的分析

- PESTEL分析

- 消費者行為分析

- 購買模式

- 偏好分析

- 消費者行為的區域差異

- 電子商務對購買決策的影響

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034

- 主要趨勢

- 餵料和飲水系統

- 自動餵食器和智慧分配器

- 傳統碗和噴泉

- 旅行和攜帶式餵食解決方案

- 專門的飲食支援配件

- 美容和衛生用品

- 刷子、梳子和美容工具

- 洗髮精和清潔產品

- 指甲護理和牙齒衛生

- 專業美容設備

- 住房和運輸工具

- 室內飼養解決方案(籠子、狗舍)

- 運輸箱和旅行箱

- 寢具和舒適配件

- 戶外庇護所和天氣保護

- 玩具和益智產品

- 互動與益智玩具

- 咀嚼玩具和牙齒保健產品

- 運動和活動器材

- 物種特異性富集解決方案

- 項圈、皮帶和挽具

- 傳統項圈和身分標籤

- 智慧項圈和 GPS 追蹤設備

- 牽引繩和伸縮系統

- 安全帶和安全設備

- 其他(健康與安全產品等)

第6章:市場估計與預測:依寵物類型,2021 - 2034

- 主要趨勢

- 狗

- 貓

- 鳥類

- 魚類和水生寵物

- 爬蟲類

- 其他(哺乳動物、兔子、倉鼠等)

第7章:市場估計與預測:依價格區間,2021 - 2034

- 主要趨勢

- 低的

- 中等的

- 高的

第 8 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 線上

- 電子商務

- 公司網站

- 離線

- 超市和大賣場

- 寵物專賣店

- 其他零售店(寵物醫院等)

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Central Garden & Pet Company

- Coastal Pet Products

- Ferplast

- Furhaven Pet Products

- Hartz Mountain

- Jollyes Pet Superstores

- KONG Company

- Merrick Pet Care

- MidWest Homes for Pets

- Nestle Purina PetCare

- Outward Hound

- Pets at Home Group

- Red Dingo

- Rogz Pet Gear

- ZippyPaws

The Global Pet Accessories Market was valued at USD 21.9 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 43.1 billion by 2034.

The rising rate of pet ownership across urban, rural, and suburban regions continues to shape the future of the market. With more households adopting pets, demand for both essential and niche accessories is surging. This has opened doors for brands to innovate and meet the evolving needs of pet owners. Growing consumer awareness around pet wellness, comfort, and engagement is encouraging manufacturers to explore fresh product categories and improve designs that reflect current lifestyles and values, such as eco-consciousness and personalization.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.9 Billion |

| Forecast Value | $43.1 Billion |

| CAGR | 7.3% |

Policy support in several countries encouraging pet adoption, alongside rising disposable income, is further increasing pet ownership. This rising trend has amplified interest in high-end, multifunctional products like smart collars, ergonomic toys, and AI-powered feeders. Enhanced distribution networks, especially through online platforms, are expanding product accessibility. The integration of technology in accessories, from fitness monitors to automated feeding systems, is becoming mainstream, while emerging economies are driving both affordability and innovation. As industry embraces digital commerce and data-driven customization, new growth avenues are constantly unfolding across global markets.

In 2024, the grooming and hygiene-related accessories generated USD 5.6 billion and are projected to grow at a CAGR of 8% through 2034. Pet owners are increasingly opting for interactive toys and hygiene essentials that cater to mental stimulation and physical activity. These toys are now made from biodegradable and recyclable materials to align with environmentally responsible values. The shift toward sustainability is also influencing design decisions and purchase patterns across the pet care space, making green alternatives a driving force in product development.

The dogs segment held a 55% share and is expected to grow at a CAGR of 7.5% from 2025 to 2034. Pet owners are now investing in health-enhancing accessories such as orthopedic bedding, digital health trackers, and supplement packs. Personalized accessories, including custom outfits and engraved tags, are becoming common among dog parents who now prioritize their pet's comfort and individuality as much as their own. As the pet-human bond deepens, spending on specialized accessories continues to rise.

U.S. Pet Accessories Market held a 76% share and generated USD 5.9 billion in 2024. The cultural shift toward treating pets as part of the family continues to influence spending behavior. Consumers in the U.S. are increasingly opting for smart pet accessories, including cameras, GPS trackers, and automated systems. Eco-friendly packaging and sustainable production practices are also gaining importance among American shoppers, reinforcing the demand for responsibly crafted pet products.

Key companies shaping the Global Pet Accessories Market include KONG Company, Red Dingo, Outward Hound, Pets at Home Group, Jollyes Pet Superstores, ZippyPaws, Coastal Pet Products, Central Garden & Pet, Ferplast, Merrick Pet Care, Rogz Pet Gear, Hartz Mountain, Nestle Purina PetCare, MidWest Homes for Pets, and Furhaven Pet Products. Leading players in the Pet Accessories Market are prioritizing product innovation, premiumization, and sustainability to stay competitive. Many brands are introducing smart pet products powered by connected technologies like GPS, health monitoring, and automation to cater to modern lifestyles. Customized offerings such as bespoke collars or tailored apparel are being introduced to appeal to pet owners seeking personalization. Companies are also investing in sustainable materials and recyclable packaging to align with growing environmental awareness. Strategic collaborations with retail chains and expanding their digital presence through e-commerce platforms allow firms to reach wider audiences.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of pet owners

- 3.2.1.2 Growing trend of pet humanization

- 3.2.1.3 Higher consumer spending on pet care

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Seasonality in pet clothing & accessories

- 3.2.2.2 Supply chain disruptions

- 3.2.2.3 Intense market competition

- 3.2.3 Opportunities

- 3.2.3.1 Eco-conscious & sustainable

- 3.2.3.2 Smart/tech-enabled accessories

- 3.2.3.3 Multi-functional and space-saving designs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade Statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Feeding & watering systems

- 5.2.1 Automated feeders & smart dispensers

- 5.2.2 Traditional bowls & water fountains

- 5.2.3 Travel & portable feeding solutions

- 5.2.4 Specialized dietary support accessories

- 5.3 Grooming & hygiene products

- 5.3.1 Brushes, combs & grooming tools

- 5.3.2 Shampoos & cleaning products

- 5.3.3 Nail care & dental hygiene

- 5.3.4 Professional grooming equipment

- 5.4 Housing & carriers

- 5.4.1 Indoor housing solutions (cages, kennels)

- 5.4.2 Transport carriers & travel crates

- 5.4.3 Bedding & comfort accessories

- 5.4.4 Outdoor shelters & weather protection

- 5.5 Toys & enrichment products

- 5.5.1 Interactive & puzzle toys

- 5.5.2 Chew toys & dental health products

- 5.5.3 Exercise & activity equipment

- 5.5.4 Species-specific enrichment solutions

- 5.6 Collars, leashes & harnesses

- 5.6.1 Traditional collars & identification tags

- 5.6.2 Smart collars & GPS tracking devices

- 5.6.3 Leashes & retractable systems

- 5.6.4 Harnesses & safety equipment

- 5.7 Others (health & safety products, etc.)

Chapter 6 Market Estimates & Forecast, By Pet Type, 2021 - 2034 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Birds

- 6.5 Fish & aquatic pets

- 6.6 Reptiles

- 6.7 Others (mammals, rabbits, hamsters, etc.)

Chapter 7 Market Estimates & Forecast, By Price range, 2021 - 2034 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce

- 8.2.2 Company website

- 8.3 Offline

- 8.3.1 Supermarkets and hypermarkets

- 8.3.2 Pet specialty stores

- 8.3.3 Other retail stores (pet hospitals, etc.)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Central Garden & Pet Company

- 10.2 Coastal Pet Products

- 10.3 Ferplast

- 10.4 Furhaven Pet Products

- 10.5 Hartz Mountain

- 10.6 Jollyes Pet Superstores

- 10.7 KONG Company

- 10.8 Merrick Pet Care

- 10.9 MidWest Homes for Pets

- 10.10 Nestle Purina PetCare

- 10.11 Outward Hound

- 10.12 Pets at Home Group

- 10.13 Red Dingo

- 10.14 Rogz Pet Gear

- 10.15 ZippyPaws

2026-2030年全球寵物用品市場

2026-2030年全球寵物用品市場 寵物零食分配器市場:2026-2032年全球市場預測(按產品類型、連接方式、最終用戶和分銷管道分類)

寵物零食分配器市場:2026-2032年全球市場預測(按產品類型、連接方式、最終用戶和分銷管道分類) 個人化時尚寵物服飾及配件市場預測至2034年-按產品類型、個人化方式、材料、應用、最終用戶及地區分類的全球分析

個人化時尚寵物服飾及配件市場預測至2034年-按產品類型、個人化方式、材料、應用、最終用戶及地區分類的全球分析 全球寵物床市場規模、佔有率、趨勢和成長分析報告(2026-2034年)寵物用品市場:依動物種類、產品類型、價格範圍、材質和通路分類-全球預測(2026-2032 年)寵物咖啡木磨牙棒市場:按動物類型、產品類型、口味、生命階段、原料品質和通路分類,全球預測,2026-2032年全球電動寵物按摩器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球寵物床市場規模、佔有率、趨勢和成長分析報告(2026-2034年)寵物用品市場:依動物種類、產品類型、價格範圍、材質和通路分類-全球預測(2026-2032 年)寵物咖啡木磨牙棒市場:按動物類型、產品類型、口味、生命階段、原料品質和通路分類,全球預測,2026-2032年全球電動寵物按摩器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 寵物床市場 - 全球產業規模、佔有率、趨勢、機會及預測(按床型、材料類型、分銷管道、地區和競爭格局分類,2021-2031年)寵物濕紙巾市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、產品類型、分銷管道、地區和競爭格局分類,2021-2031年)寵物糞便袋市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、寵物類型、尺寸、分銷管道、地區和競爭格局分類,2021-2031年)

寵物床市場 - 全球產業規模、佔有率、趨勢、機會及預測(按床型、材料類型、分銷管道、地區和競爭格局分類,2021-2031年)寵物濕紙巾市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、產品類型、分銷管道、地區和競爭格局分類,2021-2031年)寵物糞便袋市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、寵物類型、尺寸、分銷管道、地區和競爭格局分類,2021-2031年)