|

市場調查報告書

商品編碼

1822555

自動餵魚器市場機會、成長動力、產業趨勢分析及2025-2034年預測Automatic Fish Feeders Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

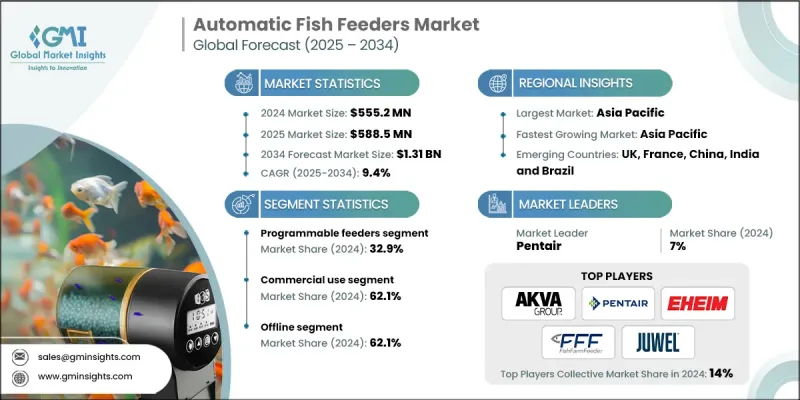

根據 Global Market Insights, Inc. 發布的最新報告,2024 年全球自動餵魚器市場價值為 5.552 億美元,預計將從 2025 年的 5.885 億美元成長到 2034 年的 13.2 億美元,複合年成長率為 9.4%。

市場持續成長,商業水產養殖場和觀賞魚養殖者對自動投餵系統解決方案的需求也日益成長。自動投餵系統可以提高投餵精度,減少對人工的依賴,並改善魚類的健康和生長,從而提高運作效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 5.552億美元 |

| 預測值 | 13.2億美元 |

| 複合年成長率 | 9.4% |

關鍵促進因素:

- 水產養殖自動化需求不斷成長:養魚場正在使用自動餵食系統來減少飼料浪費,提高飼料轉換率 (FCR),並更永續

- 業餘養魚的成長:城市消費者正在推動對家庭水族館和魚缸的需求,從而增加了小型可編程餵食器的銷售。

- 商業水產養殖勞動力短缺:自動化減少了勞動力效率低下,並為大規模養殖提供了標準化的餵食計畫。

- 可程式設備的進步:計時器、感測器和物聯網功能的使用,幫助使用者遠端操作送料器(例如線上)並即時追蹤送料。

關鍵參與者:

- 前五大廠商分別是 AKVA Group、Pentair、EHEIM、Fish Farm Feeder 和 Juwel,共佔 14% 的市場佔有率,反映市場集中度較高。

- 憑藉其尖端、可靠的餵食解決方案以及在水產養殖技術領域的強大全球影響力,濱特爾佔據了 7% 的市場佔有率,成為市場領導者。

主要挑戰:

- 農村電力依賴:專案饋線需要穩定的電力,這可能會成為一些發展中市場的限制因素。

- 大型餵料機初始投資高:商業餵料機雖然效率高,但往往需要大量的資本支出。

- 小型業者的產品意識程度低:缺乏自動化設備的訓練和經驗,減緩了傳統水產養殖經營的轉型。

瀏覽分佈在 210 頁的關鍵行業見解,其中包含 80 個市場資料表和圖表,來自報告“自動餵魚器市場規模 - 按類型、按安裝類型、按機制、按功能、按容量、按飼料類型、按材料、按最終用途、按配銷通路、成長預測,2025 - 2034”,詳情以及目錄:

1. 按類型 - 可程式供料器擴大市場

可程式自動餵食器憑藉其精準的餵食量、便利性以及在商業和觀賞用途上的廣泛應用,在2024年佔據了最大的市場佔有率。可程式自動餵食器是一種深度整合的解決方案,用於控制餵食頻率、時間和餵食量,因此在市場上取得了爆炸性成長,尤其受到所有消費群體的青睞。

2. 依最終用途分類-商業佔大多數

2024 年,商業領域(例如養殖場和水產養殖廠)佔據了最大的市場佔有率。可重複的魚庫使水產養殖系統能夠提高餵食性能、減少飼料浪費並節省勞動力,這再次推動了大型公司大規模採用自動餵食器。

3. 按配銷通路-線下通路占主導地位

2024年,線下通路佔據市場主導地位。寵物店、水產養殖設備零售商和農場用品商店仍然是購買點的首選,尤其是在對新消費者來說最重視實際演示和售後服務的地區。

4. 按地區分類-亞太地區發揮領導作用

2024年,亞太地區憑藉其龐大的水產養殖網路、良好的環境以及政府支持魚類養殖自動化的舉措,佔據了市場主導地位。中國和東南亞地區經歷了強勁的成長。

2024年,亞太地區憑藉其高水產養殖產量佔據了最大的市場佔有率,尤其是在中國、印度和印尼。魚類蛋白質需求的不斷成長、政府對水產養殖項目的支持以及養魚場自動化程度的提高,推動了可編程自動餵食器在該地區的應用。

自動餵魚器產業的主要參與者有 AKVA Group、EHEIM、Fish Farm Feeder、Fish Mate、Hygger、Juwel、Kamber Tech、Lifegard Aquatics、Pentair、Pioneer Group、Resun、Sweeney Enterprise、Torlam、Yiyuan Technology 和 Zacro。

為了鞏固市場地位,主要參與者正著力於產品開發、新興市場滲透以及分銷網路建設。 AKVA Group 和 Fish Farm Feeder 正在透過在投餵駁船上安裝工業級投餵器來吸引商業水產養殖業者。 EHEIM、Zacro 和 Torlam 透過為水族愛好者和寵物主人提供可編程投餵器,在零售領域蓬勃發展。 Hygger 和 Lifegard Aquatics 正在為其產品設計添加智慧功能和備用電池,以追求便利性和可靠性。線下分銷和店內演示仍然至關重要,尤其是在亞太地區的高成長地區。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 水產養殖日益普及

- 智慧餵料器的技術進步

- 商業養魚場勞動成本的降低

- 產業陷阱與挑戰

- 商業規模系統的初始投資較高

- 技術問題和維護需求

- 機會

- 與物聯網和基於感測器的供料系統整合

- 針對特定物種的飲食和餵食模式進行客製化

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 監理框架

- 標準和合規要求

- 區域監理框架

- 認證標準

- 貿易統計(HS編碼:84798999)

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL分析

- 消費者行為分析

- 購買模式

- 偏好分析

- 消費者行為的區域差異

- 電子商務對購買決策的影響

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依類型,2021-2034

- 主要趨勢

- 可程式餵料器

- 旋轉給料機

- 滾筒給料機

- 氣動送料器

- 重力餵料機

- 其他(螺旋餵食器、振動餵食器、定量餵食器)

第6章:市場估計與預測:按安裝類型,2021-2034

- 主要趨勢

- 夾式送料器

- 浮動餵食器

- 內置儲罐供料器

第7章:市場估計與預測:按機制,2021-2034

- 主要趨勢

- 電動餵食器

- 太陽能餵食器

- 電池供電餵食器

第8章:市場估計與預測:依特徵,2021-2034

- 主要趨勢

- Wi-Fi 連接

- 智慧型手機控制

第9章:市場估計與預測:依產能,2021-2034

- 主要趨勢

- 1公升以下

- 1至10公升

- 超過10公升

第 10 章:市場估計與預測:按飼料類型,2021-2034 年

- 主要趨勢

- 顆粒

- 薄片

- 顆粒

- 冷凍乾燥食品

- 直播

第 11 章:市場估計與預測:按材料,2021-2034 年

- 主要趨勢

- 塑膠餵食器

- 金屬進料器

- 複合材料進料器

第 12 章:市場估計與預測:按最終用途,2021-2034 年

- 主要趨勢

- 住宅用途

- 商業用途

第 13 章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 線上

- 公司網站

- 線上零售商

- 離線

- 專賣店

- 寵物店

- 其他

第 14 章:市場估計與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 15 章:公司簡介

- AKVA Group

- EHEIM

- Fish Farm Feeder

- Fish Mate

- Hygger

- Juwel

- Kamber Tech

- Lifegard Aquatics

- Pentair

- Pioneer Group

- Resun

- Sweeney Enterprise

- Torlam

- Yiyuan Technology

- Zacro

The global automatic fish feeders market was valued at USD 555.2 million in 2024 and is projected to grow from USD 588.5 million in 2025 to USD 1.32 billion by 2034, at a CAGR of 9.4%, according to the latest report published by Global Market Insights, Inc.

The market is witnessing consistent growth and is seeing an increase in demand for automated feeding system solutions for commercial aquaculture farms and ornamental fishkeepers. Automatic fish feed systems improve feed accuracy, enable less reliance on manual labour, and also improve fish health and growth to improve operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $555.2 Million |

| Forecast Value | $1.32 Billion |

| CAGR | 9.4% |

Key Drivers:

- Increasing demand for aquaculture automation: fish farms are using automated feeding systems to reduce feed waste, improve FCR (feed conversion ratio) and be more sustainable

- Growth in hobby fishkeeping: urban consumers are driving the demand for home aquariums and fish tanks, which increases sales of smaller programmable feeders.

- Shortage of Commercial aquaculture labor: Automation reduces labor inefficiencies and provides standardization of feeding schedules in large-scale operations.

- Advancements in programmable devices: the use of timers, sensors, and IoT capability, are helping empower users to operate feeders remotely (e.g., online) and track-feed in real-time.

Key Players:

- Top 5 players are AKVA Group, Pentair, EHEIM, Fish Farm Feeder, and Juwel, together controlling 14% of the market, reflecting fragmented market concentration.

- Pentair is the market leader with 7% market share on account of its cutting-edge, reliable feeding solutions and robust worldwide presence in aquaculture technology.

Key Challenges:

- Rural power dependency: Stable electricity is required for program feeders, which could be a constraint in some developing markets.

- High initial investment for large feeders: Though efficient, commercial feeders tend to demand a lot of capital outlay.

- Low level of product awareness with small operators: Lack of training and experience with automation devices slows the transition in traditional aquaculture operations.

Browse key industry insights spread across 210 pages with 80 market data tables and figures from the report, "Automatic Fish Feeders Market Size - By Type, By Mounting Type, By Mechanism, By Features, By Capacity, By Feed Type, By Material, By End Use, By Distribution Channel, Growth Forecast, 2025 - 2034" in detail, along with the table of contents:

1. By Type - Programmable Feeders Expand Market

Programmable automatic feeders held the largest market share in 2024 due to precise feeding amounts, convenience, and availability for commercial and ornamental applications. Programmable automatic feeders are a deeply integrated solution for controlling frequency, times, and amounts of feeding, and therefore have exploded onto the market, particularly for all segments of the consumer.

2. By End Use - Commercial Makes Up the Majority

The commercial segment, such as fish farms and aquaculture plants, held the most significant market share in 2024. Repeatable depots of fish allows aquaculture systems to increase of feeding performance, less wasted feed, and save in labour, which again drives mass adoption of the automatic feeders among the largest firms.

3. By Distribution Channel - Offline Segment Dominates

Offline channels dominated the market in 2024. Pet stores, aquaculture equipment retailers, and farm supply stores are still the first choice for points of purchase, particularly in areas where hands-on demonstrations and post-sales services are most important for new consumers.

4. By Region - Asia Pacific Leverages Leadership

Asia Pacific dominated the market in 2024 thanks to its large aquaculture network, favorable environment, and government initiatives supporting fish farming automation. China and Southeast Asia experience robust growth.

The Asia Pacific region captured the largest market share in 2024 due to its high aquaculture production, especially in China, India, and Indonesia. Increasing fish protein demand, government support for aquaculture initiatives, and rising automation in fish farms drive programmable automatic feeders' adoption in this region.

Major players in the automatic fish feeders industry are AKVA Group, EHEIM, Fish Farm Feeder, Fish Mate, Hygger, Juwel, Kamber Tech, Lifegard Aquatics, Pentair, Pioneer Group, Resun, Sweeney Enterprise, Torlam, Yiyuan Technology, and Zacro.

To reinforce their market standing, major players are emphasizing product development, penetration into emerging markets, and distribution networks. AKVA Group and Fish Farm Feeder are pursuing commercial aquaculture operators with industrial-strength feeders built into feeding barges. EHEIM, Zacro, and Torlam are growing in retail by providing programmable feeders for the aquarist and pet owner. Hygger and Lifegard Aquatics are adding smart features and battery backup to their designs to pursue convenience and reliability. Offline distribution and in-store demonstrations remain critical, especially in Asia Pacific's high-growth regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Mounting type

- 2.2.4 Mechanism

- 2.2.5 Features

- 2.2.6 Capacity

- 2.2.7 Feed type

- 2.2.8 Material

- 2.2.9 End use

- 2.2.10 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing popularity of aquaculture

- 3.2.1.2 Technological advancements in smart feeders

- 3.2.1.3 Labor cost reduction in commercial fish farms

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment for commercial-scale systems

- 3.2.2.2 Technical issues and maintenance needs

- 3.2.3 Opportunities

- 3.2.3.1 Integration with IoT and sensor-based feeding systems

- 3.2.3.2 Customization for species-specific diets and feeding patterns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory framework

- 3.7.1 standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code: 84798999)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behaviour analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behaviour

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Programmable feeders

- 5.3 Rotary feeders

- 5.4 Drum feeders

- 5.5 Pneumatic feeders

- 5.6 Gravity feeders

- 5.7 Others (auger, vibrating, portion control fish feeders)

Chapter 6 Market Estimates & Forecast, By Mounting Type, 2021-2034 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Clamp-on feeders

- 6.3 Floating feeders

- 6.4 Built-in tank feeders

Chapter 7 Market Estimates & Forecast, By Mechanism, 2021-2034 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Electric feeders

- 7.3 Solar-powered feeders

- 7.4 Battery-operated feeders

Chapter 8 Market Estimates & Forecast, By Features, 2021-2034 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Wi-Fi connectivity

- 8.3 Smartphone control

Chapter 9 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Under 1 liter

- 9.3 1 to 10 liters

- 9.4 More than 10 liters

Chapter 10 Market Estimates & Forecast, By Feed Type, 2021-2034 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Pellets

- 10.3 Flakes

- 10.4 Granules

- 10.5 Freeze-dried food

- 10.6 Live feed

Chapter 11 Market Estimates & Forecast, By Material, 2021-2034 (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 Plastic feeders

- 11.3 Metal feeders

- 11.4 Composite material feeders

Chapter 12 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Thousand Units)

- 12.1 Key trends

- 12.2 Residential use

- 12.3 Commercial use

Chapter 13 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Thousand Units)

- 13.1 Key trends

- 13.2 Online

- 13.2.1 Company websites

- 13.2.2 Online retailers

- 13.3 Offline

- 13.3.1 Specialty stores

- 13.3.2 Pet stores

- 13.3.3 Others

Chapter 14 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Thousand Units)

- 14.1 Key trends

- 14.2 North America

- 14.2.1 U.S.

- 14.2.2 Canada

- 14.3 Europe

- 14.3.1 Germany

- 14.3.2 UK

- 14.3.3 France

- 14.3.4 Italy

- 14.3.5 Spain

- 14.4 Asia Pacific

- 14.4.1 China

- 14.4.2 India

- 14.4.3 Japan

- 14.4.4 South Korea

- 14.4.5 Australia

- 14.5 Latin America

- 14.5.1 Brazil

- 14.5.2 Mexico

- 14.5.3 Argentina

- 14.6 MEA

- 14.6.1 South Africa

- 14.6.2 Saudi Arabia

- 14.6.3 UAE

Chapter 15 Company Profiles

- 15.1 AKVA Group

- 15.2 EHEIM

- 15.3 Fish Farm Feeder

- 15.4 Fish Mate

- 15.5 Hygger

- 15.6 Juwel

- 15.7 Kamber Tech

- 15.8 Lifegard Aquatics

- 15.9 Pentair

- 15.10 Pioneer Group

- 15.11 Resun

- 15.12 Sweeney Enterprise

- 15.13 Torlam

- 15.14 Yiyuan Technology

- 15.15 Zacro

寵物咖啡木磨牙棒市場:按動物類型、產品類型、口味、生命階段、原料品質和通路分類,全球預測,2026-2032年

寵物咖啡木磨牙棒市場:按動物類型、產品類型、口味、生命階段、原料品質和通路分類,全球預測,2026-2032年 全球電動寵物按摩器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球電動寵物按摩器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 寵物床市場 - 全球產業規模、佔有率、趨勢、機會及預測(按床型、材料類型、分銷管道、地區和競爭格局分類,2021-2031年)寵物濕紙巾市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、產品類型、分銷管道、地區和競爭格局分類,2021-2031年)寵物糞便袋市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、寵物類型、尺寸、分銷管道、地區和競爭格局分類,2021-2031年)狗安全牽引繩市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、分銷管道、地區和競爭格局分類,2021-2031年寵物慢食碗市場:依寵物類型、材質、容量、形狀、價格範圍和通路分類-2026-2032年全球預測寵物濕紙巾市場:依動物種類、產品類型、包裝、材料種類、價格範圍、通路和最終用戶分類-2026-2032年全球預測寵物碗市場按產品類型、寵物類型、材質和通路分類-2026年至2032年全球預測寵物美容擦拭巾市場按產品類型、動物種類、配方、擦拭巾材質、通路和最終用戶分類-2026-2032年全球預測

寵物床市場 - 全球產業規模、佔有率、趨勢、機會及預測(按床型、材料類型、分銷管道、地區和競爭格局分類,2021-2031年)寵物濕紙巾市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、產品類型、分銷管道、地區和競爭格局分類,2021-2031年)寵物糞便袋市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、寵物類型、尺寸、分銷管道、地區和競爭格局分類,2021-2031年)狗安全牽引繩市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、分銷管道、地區和競爭格局分類,2021-2031年寵物慢食碗市場:依寵物類型、材質、容量、形狀、價格範圍和通路分類-2026-2032年全球預測寵物濕紙巾市場:依動物種類、產品類型、包裝、材料種類、價格範圍、通路和最終用戶分類-2026-2032年全球預測寵物碗市場按產品類型、寵物類型、材質和通路分類-2026年至2032年全球預測寵物美容擦拭巾市場按產品類型、動物種類、配方、擦拭巾材質、通路和最終用戶分類-2026-2032年全球預測