|

市場調查報告書

商品編碼

1773447

葡萄酒及葡萄汁市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Wine and Grape Must Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

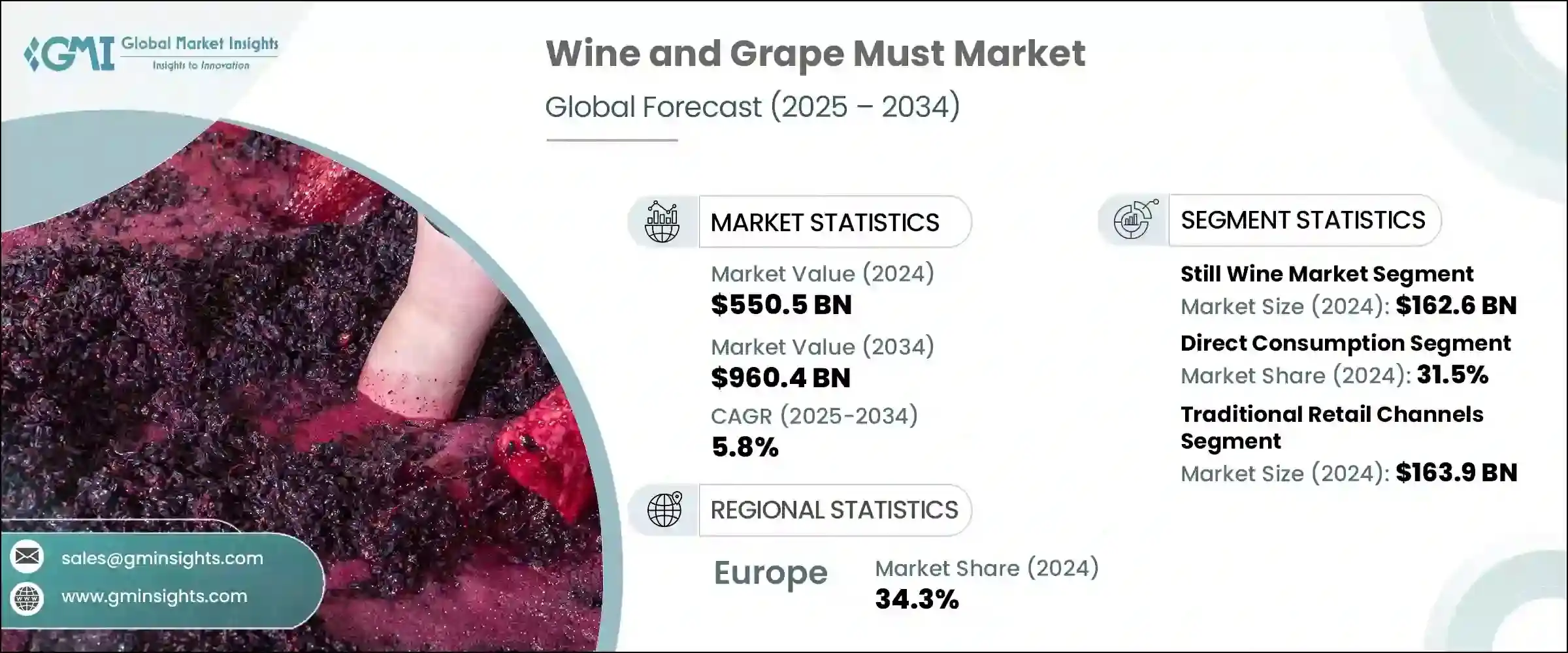

2024年,全球葡萄酒和葡萄汁市場規模達5,505億美元,預計到2034年將以5.8%的複合年成長率成長,達到9,604億美元。全球對高品質手工葡萄酒的強勁需求持續推動市場擴張,越來越多的消費者青睞優質、永續生產的飲品。不斷發展的葡萄栽培技術和更強的氣候適應能力提高了葡萄的產量和品質,支撐了該領域的持續成長。隨著消費者越來越注重健康和環保的生活方式,他們對有機、生物動力和本地釀造的葡萄酒表現出更強的偏好。

線上零售和直銷通路的影響力日益增強,使得優質葡萄酒和葡萄汁比以往任何時候都更容易獲得,進一步加速了全球市場的成長。此外,罐裝和可回收瓶裝等創新包裝形式也吸引了注重永續發展的買家,它們在提升便利性的同時,也減少了對環境的影響。由於買家追求每一口都能獲得真實的體驗,真實性、清潔標籤趨勢和地理特色如今已成為主要賣點。這種直接消費趨勢正在重塑品牌與終端用戶的溝通方式,提供更個人化和透明的互動體驗。消費者對優質、可追溯性和所有接觸點永續性的期望正引領市場的轉型。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 5505億美元 |

| 預測值 | 9604億美元 |

| 複合年成長率 | 5.8% |

2024年,靜態葡萄酒市場產值達1,626億美元,佔29.5%。隨著人們對具有地理特色、有機、永續且擁有引人入勝背景故事的葡萄酒的需求不斷成長,該市場將繼續蓬勃發展。氣泡酒也越來越受歡迎,尤其是在發展中地區,在那裡它被視為奢華和慶典的象徵,與消費者追求的消費趨勢相契合。加強型葡萄酒仍然是愛好者的熱門選擇,這得益於人們對傳統葡萄酒以及與精釀雞尾酒文化和高級餐飲相關的高階選擇重新燃起的興趣。

直接消費領域在2024年佔31.5%,預計到2034年將以5.2%的複合年成長率成長。隨著越來越多的消費者青睞新鮮、天然生產且加工程度最低的葡萄酒和葡萄汁,這種消費模式正日益受到青睞。葡萄酒和葡萄汁在更廣泛的食品和飲料應用領域的需求顯著成長,其獨特的口味和天然的健康益處在烹飪和功能性產品中得到充分發揮。隨著消費者對食品和飲料成分的關注度不斷提高,自然發酵和清潔標章產品在各個品類中都越來越具有吸引力。

2024年,歐洲葡萄酒及葡萄汁市場佔34.3%的市佔率。該地區憑藉其長期以來的優質聲譽以及致力於生產具有地理標誌和有機認證的葡萄酒的承諾,仍然保持著全球領先地位。氣候驅動的葡萄栽培實踐和地理特色進一步提升了歐洲葡萄酒的吸引力。在北美,永續性和小批量創新是關鍵驅動力,對葡萄的需求也在成長,尤其是在以健康為導向的產品系列中。在其他地區,東南亞、南美和中國的市場正在迅速擴張,將古老的傳統與創新技術結合,以促進產量和消費量的雙重成長。區域多樣性正成為該行業全球成長的標誌。

影響全球葡萄酒和葡萄汁產業競爭態勢的關鍵參與者包括富邑葡萄酒集團 (Treasury Wine Estates)、葡萄酒集團 (The Wine Group)、嘉露酒莊 (E. & J. Gallo Winery)、星座集團 (Constellation Brands, Inc.) 和保樂力加 (Pernod Ricard)。葡萄酒和葡萄產業的公司正加大對永續生產實踐、高階產品開發和直接消費者關係的投資。他們強調可追溯性和真實性,以迎合那些重視原產地、有機認證和自然方法的挑剔受眾。各大品牌正在利用數位平台和電子商務打造個人化體驗,讓消費者更容易獲得獨家產品。向新興市場的策略性擴張使公司能夠挖掘新的客戶群,而包裝的持續創新則有助於實現環保目標。許多公司也正在加強圍繞地域遺產和釀酒傳統的故事敘述,以與受眾建立更牢固的情感聯繫。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 靜止葡萄酒市場

- 紅葡萄酒部分

- 優質紅酒

- 中檔紅酒

- 超值紅酒

- 白葡萄酒部分

- 優質白葡萄酒

- 中檔白酒

- 超值白葡萄酒

- 桃紅葡萄酒部分

- 紅葡萄酒部分

- 氣泡酒市場

- 香檳與優質氣泡酒

- 普羅塞克和中檔氣泡酒

- 超值氣泡酒

- 加強葡萄酒市場

- 波特酒與雪莉酒

- 苦艾酒和開胃酒

- 其他加強葡萄酒

- 葡萄汁市場

- 新鮮葡萄汁

- 濃縮葡萄汁

- 精餾濃縮葡萄汁

- 有機葡萄汁

- 特色和替代葡萄酒產品

- 有機和生物動力葡萄酒

- 低醇和無醇葡萄酒

- 罐裝和替代包裝

- 自有品牌葡萄酒

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 直接消費

- 現場消費(餐廳、酒吧、飯店)

- 場外消費(零售、超商)

- 直接面對消費者的銷售

- 食品飲料產業應用

- 料酒和烹飪應用

- 飲料混合和調味

- 食品加工和製造

- 工業應用

- 醫藥和營養保健用途

- 化妝品和個人護理應用

- 化學和工業加工

- 葡萄汁的具體應用

- 釀酒和發酵

- 食品和糖果業

- 保健食品和補充劑製造

- 傳統和文化用途

第7章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- 傳統零售通路

- 超市和大賣場

- 葡萄酒專賣店

- 便利商店

- 百貨公司

- 本地通路

- 餐廳和高級餐廳

- 酒吧和酒館

- 飯店及餐飲業

- 酒吧和品酒室

- 直銷通路

- 酒廠直接面對消費者

- 葡萄酒俱樂部和訂閱

- 酒窖門銷售

- 葡萄酒旅遊和品酒體驗

- 電子商務與數位管道

- 線上葡萄酒零售商

- 市場平台

- 行動應用程式

- 社群商務

- 批發和分銷

- 傳統三層系統

- 專業葡萄酒經銷商

- 進出口通路

- 經紀人網路

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- E. & J. Gallo Winery

- Constellation Brands, Inc.

- Treasury Wine Estates

- Pernod Ricard

- The Wine Group

- Castel Group

- Accolade Wines

- Caviro Group

- Freixenet Group

- Changyu Pioneer Wine Company

- Great Wall Wine Company

- Dynasty Fine Wines Group

- Suntory Holdings

- Sapporo Holdings

The Global Wine and Grape Must Market was valued at USD 550.5 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 960.4 billion by 2034. Strong global demand for high-quality and artisanal wine continues to drive market expansion, as more consumers gravitate toward premium, sustainably produced beverages. Evolving viticulture techniques and improved climate adaptability have enhanced both yield and grape quality, supporting consistent growth in this space. Consumers are showing stronger preferences for organic, biodynamic, and locally crafted options, driven by an increasing shift toward health-aware and environmentally responsible lifestyles.

The rising influence of online retail and direct-to-consumer distribution channels has made premium wine and grape must more accessible than ever, further accelerating growth across global markets. In addition, innovative packaging formats such as cans and recyclable bottles are appealing to sustainability-minded buyers, enhancing convenience while reducing environmental impact. Authenticity, clean-label trends, and regional character are now major selling points, as buyers seek genuine experiences with every sip. This direct consumption trend is reshaping how brands connect with end-users, offering a more personalized and transparent engagement. The market's transformation is being led by consumer expectations for premium quality, traceability, and sustainability across all touchpoints.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $550.5 Billion |

| Forecast Value | $960.4 Billion |

| CAGR | 5.8% |

In 2024, the still wine segment generated USD 162.6 billion, claiming a 29.5% share. This segment continues to thrive as demand rises for regionally distinct, organic, and sustainable selections with compelling backstories. Sparkling wine is also gaining popularity, especially in developing regions, where it is seen as a symbol of luxury and celebration, aligning with aspirational consumer trends. Fortified wine remains a niche favorite among enthusiasts, supported by renewed interest in heritage varieties and high-end options connected to craft cocktail culture and fine dining.

The direct consumption segment represented a 31.5% share in 2024 and projected to grow at a CAGR of 5.2% through 2034. This mode of consumption is experiencing increased traction as more consumers favor wines and grape must that are fresh, naturally produced, and minimally processed. There is a notable surge in demand for wine and grape must in broader food and beverage applications, where their unique taste profiles and natural health-enhancing qualities leveraged in culinary and functional products. As consumers become more aware of what goes into their food and drinks, naturally fermented and clean-label offerings are becoming more attractive across categories.

Europe Wine and Grape Must Market held a 34.3% share in 2024. The region remains a global leader due to its long-established reputation for quality and its commitment to producing wines with geographic identity and organic certification. Climate-driven viticultural practices and regional storytelling further enhance the appeal of European wines. In North America, sustainability and small-batch innovation are key drivers, while demand for grapes is growing, especially in wellness-oriented product lines. Elsewhere, markets in Southeast Asia, South America, and China are rapidly expanding, combining age-old traditions with innovative technology to grow both production and consumption. Regional diversity is becoming a hallmark of the industry's global growth.

Key players shaping the competitive dynamics of the Global Wine and Grape Must Industry include Treasury Wine Estates, The Wine Group, E. & J. Gallo Winery, Constellation Brands, Inc., and Pernod Ricard. Companies within the wine and grape sector are increasingly investing in sustainable production practices, premium product development, and direct consumer relationships. Emphasis is placed on traceability and authenticity to cater to a discerning audience that values origin, organic certification, and natural methods. Brands are leveraging digital platforms and e-commerce to create personalized experiences, making it easier for consumers to access exclusive products. Strategic expansion into emerging markets allows companies to tap into new customer bases, while continuous innovation in packaging supports environmental goals. Many are also enhancing storytelling around regional heritage and winemaking traditions to build stronger emotional connections with their audiences.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Still wine market

- 5.2.1 Red wine segment

- 5.2.1.1 Premium red wine

- 5.2.1.2 Mid-range red wine

- 5.2.1.3 Value red wine

- 5.2.2 White wine segment

- 5.2.2.1 Premium white wine

- 5.2.2.2 Mid-range white wine

- 5.2.2.3 Value white wine

- 5.2.3 Rose wine segment

- 5.2.1 Red wine segment

- 5.3 Sparkling wine market

- 5.3.1 Champagne and premium sparkling

- 5.3.2 Prosecco and mid-range sparkling

- 5.3.3 Value sparkling wine

- 5.4 Fortified wine market

- 5.4.1 Port and sherry

- 5.4.2 Vermouth and aperitifs

- 5.4.3 Other fortified wines

- 5.5 Grape must market

- 5.5.1 Fresh grape must

- 5.5.2 Concentrated grape must

- 5.5.3 Rectified concentrated grape must

- 5.5.4 Organic grape must

- 5.6 Specialty and alternative wine products

- 5.6.1 Organic and biodynamic wines

- 5.6.2 Low and No-alcohol wines

- 5.6.3 Canned and alternative packaging

- 5.6.4 Private label wines

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Direct consumption

- 6.2.1 On-premise consumption (restaurants, bars, hotels)

- 6.2.2 Off-premise consumption (retail, supermarkets)

- 6.2.3 Direct-to-consumer sales

- 6.3 Food and beverage industry applications

- 6.3.1 Cooking wine and culinary applications

- 6.3.2 Beverage blending and flavoring

- 6.3.3 Food processing and manufacturing

- 6.4 Industrial applications

- 6.4.1 Pharmaceutical and nutraceutical uses

- 6.4.2 Cosmetic and personal care applications

- 6.4.3 Chemical and industrial processing

- 6.5 Grape must specific applications

- 6.5.1 Winemaking and fermentation

- 6.5.2 Food and confectionery industry

- 6.5.3 Health food and supplement manufacturing

- 6.5.4 Traditional and cultural uses

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Traditional retail channels

- 7.2.1 Supermarkets and hypermarkets

- 7.2.2 Specialty wine stores

- 7.2.3 Convenience stores

- 7.2.4 Department stores

- 7.3 On-premise channels

- 7.3.1 Restaurants and fine dining

- 7.3.2 Bars and pubs

- 7.3.3 Hotels and hospitality

- 7.3.4 Wine bars and tasting rooms

- 7.4 Direct sales channels

- 7.4.1 Winery direct-to-consumer

- 7.4.2 Wine clubs and subscriptions

- 7.4.3 Cellar door sales

- 7.4.4 Wine tourism and tasting experiences

- 7.5 E-commerce and digital channels

- 7.5.1 Online wine retailers

- 7.5.2 Marketplace platforms

- 7.5.3 Mobile applications

- 7.5.4 Social commerce

- 7.6 Wholesale and Distribution

- 7.6.1 Traditional three-tier system

- 7.6.2 Specialized wine distributors

- 7.6.3 Import/Export channels

- 7.6.4 Broker networks

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 E. & J. Gallo Winery

- 9.2 Constellation Brands, Inc.

- 9.3 Treasury Wine Estates

- 9.4 Pernod Ricard

- 9.5 The Wine Group

- 9.6 Castel Group

- 9.7 Accolade Wines

- 9.8 Caviro Group

- 9.9 Freixenet Group

- 9.10 Changyu Pioneer Wine Company

- 9.11 Great Wall Wine Company

- 9.12 Dynasty Fine Wines Group

- 9.13 Suntory Holdings

- 9.14 Sapporo Holdings

滋補酒市場規模、佔有率及成長分析(依成分類型、包裝、風味特徵、酒精濃度、通路、應用及地區分類)-2026-2033年產業預測

滋補酒市場規模、佔有率及成長分析(依成分類型、包裝、風味特徵、酒精濃度、通路、應用及地區分類)-2026-2033年產業預測 全球玫瑰紅葡萄酒市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球葡萄酒市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球葡萄酒澄清劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球玫瑰紅葡萄酒市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球葡萄酒市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球葡萄酒澄清劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 精釀葡萄酒市場規模、佔有率和成長分析(按產品類型、葡萄品種、分銷管道、包裝類型和地區分類)-2026-2033年產業預測

精釀葡萄酒市場規模、佔有率和成長分析(按產品類型、葡萄品種、分銷管道、包裝類型和地區分類)-2026-2033年產業預測 葡萄酒市場規模、佔有率和成長分析(按產品類型、價格範圍、分銷管道、包裝類型和地區分類)-2026-2033年產業預測

葡萄酒市場規模、佔有率和成長分析(按產品類型、價格範圍、分銷管道、包裝類型和地區分類)-2026-2033年產業預測 無氣泡葡萄酒市場規模、佔有率和成長分析(按產品類型、葡萄酒品質、包裝類型、分銷管道、最終用戶和地區分類)—產業預測(2026-2033 年)全球葡萄酒市場:未來預測(2025-2030)

無氣泡葡萄酒市場規模、佔有率和成長分析(按產品類型、葡萄酒品質、包裝類型、分銷管道、最終用戶和地區分類)—產業預測(2026-2033 年)全球葡萄酒市場:未來預測(2025-2030) 按產品類型、顏色和地區分類的葡萄酒市場

按產品類型、顏色和地區分類的葡萄酒市場 印度的葡萄酒市場評估,葡萄酒類別,各包裝,各零售流通管道,不同生產量,各地區,機會,預測,2018~2032年

印度的葡萄酒市場評估,葡萄酒類別,各包裝,各零售流通管道,不同生產量,各地區,機會,預測,2018~2032年