|

市場調查報告書

商品編碼

1773237

瀝青乳化劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Bitumen Emulsifiers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

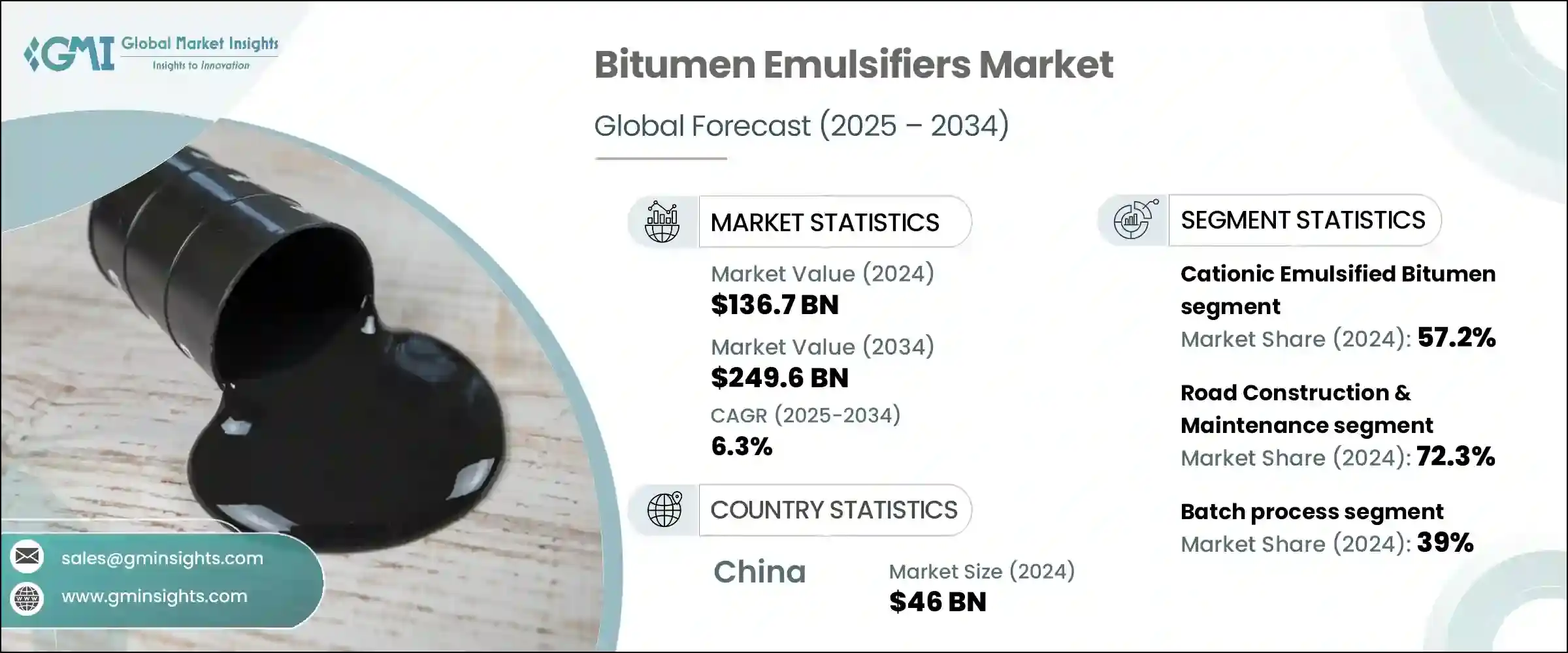

2024年,全球瀝青乳化劑市場規模達1,367億美元,預計到2034年將以6.3%的複合年成長率成長,達到2,496億美元。這一成長主要源自於基礎設施投資的增加,尤其是在具有挑戰性地形的大規模政府計畫。瀝青乳化劑因其耐寒施工和強大的耐惡劣天氣性能而成為這些項目的首選,是長期道路建設和維護的理想選擇。其水性配方顯著減少了碳氫化合物排放,無需加熱,符合全球各地日益嚴格的環境和安全法規。

這些環保優勢顯著加速了瀝青乳化劑在永續建築實踐中的應用,尤其是在優先考慮碳中和和職業安全的地區。由於乳化劑無需在施工過程中進行高溫加熱,因此可大幅降低燃料消耗和相關的溫室氣體排放。這種能源消耗的減少與全球向綠色基礎設施和淨零排放目標的轉變相契合。此外,其冷施工特性可最大限度地降低火災隱患和工人接觸有害煙霧的風險,從而提高施工現場的安全性。北美、歐洲和亞太地區的政府和監管機構擴大要求在公共基礎設施項目中使用低揮發性有機化合物 (VOC) 和環保材料,這進一步增強了對瀝青乳化劑的需求,使其成為比傳統瀝青更安全、更清潔、更高效的替代品。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1367億美元 |

| 預測值 | 2496億美元 |

| 複合年成長率 | 6.3% |

陽離子瀝青乳化劑領域在2024年佔據主導地位,市佔率達57.2%,這主要歸功於其與帶負電荷的骨材表面的出色黏結能力。這種卓越的附著力確保了路面在交通繁忙和天氣變化條件下具有更好的耐久性和彈性。陽離子配方還具有多功能性,使其非常適合從山區地形到沿海氣候的各種施工環境。它們在不同溫度和濕度條件下的穩定性能持續推動其需求,尤其是在大規模城市發展和主要道路基礎設施項目。

2024年,道路建設和維護領域佔了72.3%的市場。瀝青乳化劑在現代鋪路施工中至關重要,因為它們廣泛用於黏結層、修補料、碎石封層和路面敷料。其冷施工特性降低了操作風險,即使在低溫條件下也能施工,從而減少了能源消耗和專案延誤。這些優勢使其成為新建和日常維護的理想選擇,尤其適用於交通繁忙的道路和快速修復工程。其速凝特性還能最大限度地減少交通中斷,這在城市地區至關重要。

2024年,中國瀝青乳化劑市場規模達460億美元。中國持續投資交通基礎設施,包括國道、鄉村公路和智慧城市走廊,推動了高性能瀝青乳化劑的廣泛應用。政府致力於永續、低排放施工實務的措施與冷敷乳化瀝青的環境效益相契合,冷敷乳化瀝青的揮發性有機化合物(VOC)排放量更低,能耗更低。隨著長期戰略性基礎設施項目的實施,對環保耐用道路材料的需求將持續成長,這將鞏固中國在市場成長領域的領先地位。

影響瀝青乳化劑產業的關鍵參與者包括英傑維蒂公司、阿科瑪集團、贏創工業股份公司、諾力昂和巴斯夫歐洲公司。這些公司透過持續的產品開發和市場擴張來塑造競爭環境。為了鞏固自身地位,瀝青乳化劑領域的公司正在優先研發能夠滿足不同氣候和環境需求的先進配方。他們正在擴大區域分銷網路,並與道路建設公司和公共基礎設施機構建立策略合作夥伴關係。永續性是核心關注點——各公司正在加大對環保、低VOC乳化劑的投資,並推廣符合綠色建築要求的解決方案。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 基礎建設不斷推進

- 環境效益與法規

- 成本效益

- 技術進步

- 產業陷阱與挑戰

- 應用溫度範圍有限

- 儲存穩定性問題

- 與熱拌瀝青相比強度較低

- 原油價格波動

- 市場機會

- 新興經濟體的需求不斷成長

- 更重視永續建築

- 生物基乳化劑的開發

- 冷回收技術的應用日益廣泛

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 陽離子瀝青乳化劑

- 快速凝固(CRS)

- 中等設定(CMS)

- 慢速設定(CSS)

- 陰離子瀝青乳化劑

- 快速設定(RS)

- 中等設定(MS)

- 慢凝(SS)

- 非離子瀝青乳化劑

- 改質瀝青乳化劑

- 聚合物改性

- SBS改性

- SBR改性

- 其他

- 乳膠改性

- 其他

- 聚合物改性

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 道路建設與維護

- 表面修整

- 黏層

- 底漆

- 稀漿封層

- 微表處

- 冷拌瀝青

- 霧封

- 碎石封層

- 防水

- 建築施工

- 基礎設施

- 路面回收

- 全深度填海(FDR)

- 就地冷再生(CIR)

- 冷中央工廠回收(CCPR)

- 其他

- 土壤穩定

- 黏合劑

- 工業應用

第7章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 道路和高速公路建設

- 機場建設

- 建築施工

- 住宅

- 商業的

- 工業的

- 其他

- 鐵路

- 海洋

- 農業

第8章:市場估計與預測:按製造程序,2021 - 2034 年

- 主要趨勢

- 批次處理

- 連續製程

- 半連續工藝

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- Alternative Environmental Technologies (AET)

- Arkema Group

- BASF SE

- Bharat Petroleum Corporation Limited (BPCL)

- BTBA

- Dow Chemical Company

- Evonik Industries AG

- GlobeCore

- Hindustan Colas Limited (HINCOL)

- Hindustan Petroleum Corporation Limited (HPCL)

- Ingevity Corporation

- Jey Oil Refining Company

- Kao Corporation

- Marathon Petroleum Asphalt & Emulsions

- Nouryon

- Nynas AB

- Petro Naft

- Pro-Road Global

- Royal Dutch Shell plc

- Tiki Tar Industries

- Total Energies SE

- Winstrol Petrochemicals Pvt. Ltd.

The Global Bitumen Emulsifiers Market was valued at USD 136.7 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 249.6 billion by 2034. This growth is primarily driven by increased investment in infrastructure, particularly large-scale government initiatives across challenging terrains. Bitumen emulsifiers are preferred for these projects due to their cold application and strong resistance to adverse weather, making them ideal for long-lasting road construction and maintenance. Their water-based formulation significantly reduces hydrocarbon emissions and eliminates the need for heating, aligning well with stricter environmental and safety regulations across global regions.

These eco-friendly benefits have significantly accelerated the adoption of bitumen emulsifiers in sustainable construction practices, particularly in regions prioritizing carbon neutrality and occupational safety. Since emulsifiers eliminate the need for high-temperature heating during application, they drastically lower fuel consumption and associated greenhouse gas emissions. This reduction in energy usage aligns with the global shift toward green infrastructure and net-zero targets. Additionally, their cold-application nature minimizes risks of fire hazards and worker exposure to harmful fumes, enhancing safety on construction sites. Governments and regulatory bodies across North America, Europe, and Asia-Pacific are increasingly mandating the use of low-VOC and environmentally responsible materials in public infrastructure projects, which has further reinforced the demand for bitumen emulsifiers as a safer, cleaner, and more efficient alternative to conventional asphalt.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $136.7 Billion |

| Forecast Value | $249.6 Billion |

| CAGR | 6.3% |

The cationic bitumen emulsifiers segment held the dominant position with a 57.2% market share in 2024, largely attributed to its excellent bonding ability with negatively charged aggregate surfaces. This superior adhesion ensures better durability and resilience of road surfaces under heavy traffic and shifting weather conditions. Cationic formulations also offer versatility, making them highly suitable for a range of construction environments-from mountainous terrains to coastal climates. Their consistent performance under various temperature and moisture levels continues to drive their demand, particularly in large-scale urban development and major roadway infrastructure projects.

The road construction and maintenance segment held a 72.3% share in 2024. Bitumen emulsifiers are critical in modern paving operations as they are widely used in tack coats, patching compounds, chip seals, and surface dressings. Their cold-application properties reduce operational hazards and allow construction even in low-temperature conditions, cutting down on energy usage and project delays. These advantages make them ideal for both new construction and routine maintenance, especially for high-traffic roads and rapid rehabilitation efforts. Their quick-setting nature also minimizes traffic disruptions, which is essential in urban areas.

China Bitumen Emulsifiers Market generated USD 46 billion in 2024. The country's ongoing investments in transportation infrastructure-including national highways, rural roads, and smart city corridors-have fueled the widespread adoption of high-performance bitumen emulsifiers. Government initiatives focused on sustainable, low-emission construction practices further align with the environmental benefits of cold-applied emulsified bitumen, which releases fewer VOCs and requires less energy. With long-term strategic infrastructure projects in place, the demand for eco-friendly, durable road materials is set to increase, reinforcing China's position at the forefront of market growth.

Key players influencing the Bitumen Emulsifiers Industry include Ingevity Corporation, Arkema Group, Evonik Industries AG, Nouryon, and BASF SE. These companies shape the competitive environment through ongoing product development and market expansion. To strengthen their position, companies in the bitumen emulsifiers space are prioritizing R&D for advanced formulations that address varying climatic and environmental demands. They are expanding their regional distribution networks and engaging in strategic partnerships with road construction firms and public infrastructure agencies. Sustainability is a core focus-firms are increasing investment in eco-friendly, low-VOC emulsifiers and promoting solutions that meet green construction mandates.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Manufacturing process

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising infrastructure development

- 3.2.1.2 Environmental benefits & regulations

- 3.2.1.3 Cost-effectiveness

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited temperature range for application

- 3.2.2.2 Storage stability concerns

- 3.2.2.3 Lower strength compared to hot mix asphalt

- 3.2.2.4 Fluctuating crude oil prices

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in emerging economies

- 3.2.3.2 Increasing focus on sustainable construction

- 3.2.3.3 Development of bio-based emulsifiers

- 3.2.3.4 Rising adoption in cold recycling technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cationic bitumen emulsifiers

- 5.2.1 Rapid setting (CRS)

- 5.2.2 Medium setting (CMS)

- 5.2.3 Slow setting (CSS)

- 5.3 Anionic bitumen emulsifiers

- 5.3.1 Rapid setting (RS)

- 5.3.2 Medium setting (MS)

- 5.3.3 Slow setting (SS)

- 5.4 Non-ionic bitumen emulsifiers

- 5.5 Modified bitumen emulsifiers

- 5.5.1 Polymer modified

- 5.5.1.1 SBS modified

- 5.5.1.2 SBR modified

- 5.5.1.3 Others

- 5.5.2 Latex modified

- 5.5.3 Others

- 5.5.1 Polymer modified

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Road construction & maintenance

- 6.2.1 Surface dressing

- 6.2.2 Tack coat

- 6.2.3 Prime coat

- 6.2.4 Slurry seal

- 6.2.5 Micro surfacing

- 6.2.6 Cold mix asphalt

- 6.2.7 Fog seal

- 6.2.8 Chip seal

- 6.3 Waterproofing

- 6.3.1 Building construction

- 6.3.2 Infrastructure

- 6.4 Pavement recycling

- 6.4.1 Full depth reclamation (FDR)

- 6.4.2 Cold in-place recycling (CIR)

- 6.4.3 Cold central plant recycling (CCPR)

- 6.5 Others

- 6.5.1 Soil stabilization

- 6.5.2 Adhesives

- 6.5.3 Industrial applications

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Road & highway construction

- 7.3 Airport construction

- 7.4 Building construction

- 7.4.1 Residential

- 7.4.2 Commercial

- 7.4.3 Industrial

- 7.5 Others

- 7.5.1 Railways

- 7.5.2 Marine

- 7.5.3 Agriculture

Chapter 8 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Batch process

- 8.3 Continuous process

- 8.4 Semi-continuous process

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alternative Environmental Technologies (AET)

- 10.2 Arkema Group

- 10.3 BASF SE

- 10.4 Bharat Petroleum Corporation Limited (BPCL)

- 10.5 BTBA

- 10.6 Dow Chemical Company

- 10.7 Evonik Industries AG

- 10.8 GlobeCore

- 10.9 Hindustan Colas Limited (HINCOL)

- 10.10 Hindustan Petroleum Corporation Limited (HPCL)

- 10.11 Ingevity Corporation

- 10.12 Jey Oil Refining Company

- 10.13 Kao Corporation

- 10.14 Marathon Petroleum Asphalt & Emulsions

- 10.15 Nouryon

- 10.16 Nynas AB

- 10.17 Petro Naft

- 10.18 Pro-Road Global

- 10.19 Royal Dutch Shell plc

- 10.20 Tiki Tar Industries

- 10.21 Total Energies SE

- 10.22 Winstrol Petrochemicals Pvt. Ltd.

瀝青乳化劑市場分析及預測(至2035年):類型、產品、應用、技術、組成成分、最終用戶、劑型、材料類型、製程、解決方案瀝青市場分析及預測(至2035年):依類型、產品類型、應用、技術、最終用戶、形態、材質、製程及功能分類環保瀝青生產市場分析及預測(至2035年):類型、產品、服務、技術、應用、形式、材料類型、製程、最終用戶、設備

瀝青乳化劑市場分析及預測(至2035年):類型、產品、應用、技術、組成成分、最終用戶、劑型、材料類型、製程、解決方案瀝青市場分析及預測(至2035年):依類型、產品類型、應用、技術、最終用戶、形態、材質、製程及功能分類環保瀝青生產市場分析及預測(至2035年):類型、產品、服務、技術、應用、形式、材料類型、製程、最終用戶、設備 瀝青:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

瀝青:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球瀝青市場報告

2026年全球瀝青市場報告 瀝青市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、應用、地區和競爭格局分類,2021-2031年

瀝青市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、應用、地區和競爭格局分類,2021-2031年 瀝青市場規模、佔有率和成長分析(按產品類型、形態、原料、製造流程、等級、分銷管道、應用和地區分類)-2026-2033年產業預測

瀝青市場規模、佔有率和成長分析(按產品類型、形態、原料、製造流程、等級、分銷管道、應用和地區分類)-2026-2033年產業預測![中國瀝青市場評估:依類型[鋪路瀝青、氧化瀝青、聚合物改質瀝青、其他]、應用[道路建設、防水、黏合劑、其他]、地區、機會及預測(2018-2032)](/sample/img/cover/42/default_cover_mx.png) 中國瀝青市場評估:依類型[鋪路瀝青、氧化瀝青、聚合物改質瀝青、其他]、應用[道路建設、防水、黏合劑、其他]、地區、機會及預測(2018-2032)印度瀝青市場評估:依類型[鋪路瀝青、氧化瀝青、聚合物改質瀝青、其他]、應用[道路建設、防水、黏合劑、其他]、地區、機會及預測(2019-2033 年)日本瀝青市場評估:依類型[鋪路瀝青、氧化瀝青、聚合物改質瀝青、其他]、應用[道路建設、防水、黏合劑、其他]、地區、機會及預測(2019-2033年)

中國瀝青市場評估:依類型[鋪路瀝青、氧化瀝青、聚合物改質瀝青、其他]、應用[道路建設、防水、黏合劑、其他]、地區、機會及預測(2018-2032)印度瀝青市場評估:依類型[鋪路瀝青、氧化瀝青、聚合物改質瀝青、其他]、應用[道路建設、防水、黏合劑、其他]、地區、機會及預測(2019-2033 年)日本瀝青市場評估:依類型[鋪路瀝青、氧化瀝青、聚合物改質瀝青、其他]、應用[道路建設、防水、黏合劑、其他]、地區、機會及預測(2019-2033年)