|

市場調查報告書

商品編碼

1721415

電動商用車 MRO(維修、維修、大修)市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Electric Commercial Vehicle MRO (Maintenance, Repair, Overhaul) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

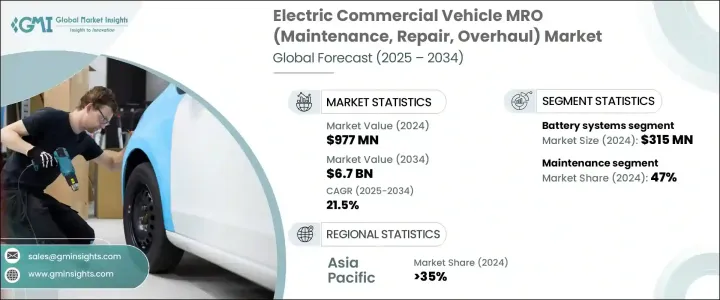

2024 年全球電動商用車 MRO 市場價值為 9.77 億美元,預計到 2034 年將以 21.5% 的複合年成長率成長,達到 67 億美元。隨著電動商用車 (ECV) 在各個行業中得到越來越廣泛的接受,該市場正在獲得強勁發展勢頭。由於日益成長的環境問題、嚴格的排放法規以及政府支持的電動車激勵措施,從內燃機 (ICE) 汽車到電動車的轉變正在加速。車隊正日益走向電氣化,以實現永續發展目標並降低整體擁有成本。隨著電動商用車不斷滲透公共和私人交通系統,特別是在最後一英里配送、物流和公共交通等領域,對可靠、快速和專業化的 MRO 服務的需求正在迅速擴大。除了車輛維護之外,支援電動車的生態系統(包括充電基礎設施和診斷工具)也在不斷發展。對客製化維護程序、零件更換和基於軟體的診斷的需求不斷成長,增加了新的複雜性,促使 MRO 供應商採用下一代工具和技術,以在動態環境中保持競爭力。

推動這一市場擴張的一個重要因素是電動車充電基礎設施的廣泛發展,這直接支持了電動商用車的更廣泛應用。隨著越來越多的充電站出現,特別是在偏遠或服務不足的地區,車隊營運商發現從傳統燃料驅動系統轉向電動車越來越可行。維護這些基礎設施(例如充電器、連接器、內部電纜和軟體)進一步促進了對 MRO 服務日益成長的需求。隨著電動車輛成為物流、配送和公共交通營運不可或缺的一部分,它們需要量身定做的維修和服務支持,從而推動北美、亞太、拉丁美洲、歐洲以及中東和非洲等地區的發展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 9.77億美元 |

| 預測值 | 67億美元 |

| 複合年成長率 | 21.5% |

按組件分類,市場包括電動傳動系統、熱管理系統、充電系統、電池系統等。 2024 年,電池系統佔 30% 的市場佔有率,價值 3.15 億美元。這些部件對於車輛的行駛里程和效率至關重要,其性能直接影響正常運行時間。重複充電、暴露在極端溫度下以及使用磨損通常會導致電池效能下降,需要定期評估並及時更換。車隊營運商優先考慮電池健康狀況,以避免代價高昂的停機,確保對提供專注電池管理服務的專業 MRO 供應商的需求穩定。

按服務類型細分,市場包括維護、維修和大修,其中維護在 2024 年將佔據 47% 的佔有率。儘管電動車輛的機械部件比傳統車輛少,但它們需要精確的維護,例如軟體診斷、煞車檢查和零件校準。定期維護對於延長車輛壽命、提高安全性和最佳化性能仍然至關重要。車隊營運商嚴重依賴預防性維護計劃,該計劃提供可預測的成本和最小的中斷,為服務提供者提供穩定的收入來源。

2024 年,中國電動商用車 MRO 市場規模達 9,210 萬美元。強勁的國內生產、政策支援和快速的車隊部署使中國成為全球領先者。蓬勃發展的城市配送、公共運輸和物流行業繼續提升對強大、技術支援的 MRO 服務的需求——從診斷到複雜的維修。

戴姆勒、Element Fleet Management、ATS Euromaster、BP Pulse、Ferdotti Motor Services、斯堪尼亞、Lion Electric、MAN Global、Merchants Fleet 和沃爾沃等主要產業參與者正在擴大其 MRO 產品組合。這些公司正在建立專門的電動車服務中心,加強技術人員培訓計劃,並利用遠端資訊處理進行預測性維護。與汽車製造商和車隊營運商的策略合作夥伴關係有助於他們確保高效的服務交付。人工智慧診斷和遠端監控正在成為加速維修週期和最大限度地減少車輛停機時間的標準工具。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原始設備製造商

- 獨立服務提供者

- 零件供應商

- 技術提供者

- 最終用途

- 利潤率分析

- 技術與創新格局

- 專利分析

- 案例研究

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 電動商用車隊的採用率不斷提高

- 擴大充電基礎設施

- 電動車和電池成本下降

- 對清潔和永續交通的需求增加

- 產業陷阱與挑戰

- 電動商用車初始成本高

- 熟練勞動力有限

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 輕型商用車

- 平均血紅素 (MCV)

- 丙型肝炎病毒

第6章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 電池系統

- 熱管理系統

- 充電系統

- 電動傳動系統

- 其他

第7章:市場估計與預測:按服務,2021 - 2034 年

- 主要趨勢

- 維護

- 維修

- 大修

第8章:市場估計與預測:按服務供應商,2021 - 2034 年

- 主要趨勢

- OEM服務中心

- 獨立服務提供者

- 艦隊維護作業

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- ATS Euromaster

- BP Pulse

- Daimler

- Element Fleet Management

- Ferdotti Motor Services

- Kerlin Bus Sales & Leasing

- Lightning eMotors

- Lion Electric

- MAN Global

- Merchants Fleet

- Northeastern Bus Rebuilders

- Orange EV

- Scania

- Sonny Merryman

- Transdev

- VDL Company

- VEV Services Limited

- Volvo

- WattEV

- YES EU

The Global Electric Commercial Vehicle MRO Market was valued at USD 977 million in 2024 and is estimated to grow at a CAGR of 21.5% to reach USD 6.7 billion by 2034. The market is gaining robust momentum as electric commercial vehicles (ECVs) become more widely accepted across various industries. The shift from internal combustion engine (ICE) vehicles to electric alternatives is accelerating due to rising environmental concerns, stringent emissions regulations, and government-backed EV incentives. Fleets are increasingly moving toward electrification to meet sustainability goals and reduce the total cost of ownership. As electric commercial vehicles continue to penetrate public and private transport systems, especially in sectors such as last-mile delivery, logistics, and public transit, the demand for reliable, fast, and specialized MRO services is expanding rapidly. Alongside vehicle maintenance, the ecosystem supporting ECVs-including charging infrastructure and diagnostic tools-is also evolving. The rising need for customized maintenance programs, parts replacement, and software-based diagnostics has added new layers of complexity, driving MRO providers to adopt next-gen tools and technologies to remain competitive in a dynamic landscape.

A significant contributor to this market expansion is the widespread development of EV charging infrastructure, which directly supports greater adoption of electric commercial vehicles. As more charging stations emerge, particularly in remote or underserved regions, fleet operators find it increasingly feasible to switch from traditional fuel-powered systems to electric mobility. Maintaining this infrastructure-such as chargers, connectors, internal cabling, and software-further contributes to the growing demand for MRO services. As ECVs become integral to logistics, delivery, and public transport operations, they require tailored repair and service support, pushing growth across regions including North America, Asia Pacific, Latin America, Europe, and the Middle East & Africa.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $977 Million |

| Forecast Value | $6.7 Billion |

| CAGR | 21.5% |

By component, the market includes electric drivetrain, thermal management systems, charging systems, battery systems, and others. In 2024, battery systems held a dominant 30% market share, valued at USD 315 million. These components are critical to a vehicle's range and efficiency, and their performance directly impacts operational uptime. Repeated charging cycles, exposure to extreme temperatures, and usage wear often degrade batteries, prompting routine assessments and timely replacements. Fleet operators prioritize battery health to avoid costly downtimes, ensuring steady demand for expert MRO providers that offer focused battery management services.

Segmented by service type, the market includes maintenance, repair, and overhaul, with maintenance commanding a 47% share in 2024. Even though ECVs have fewer mechanical components than traditional vehicles, they require precise care such as software diagnostics, brake inspections, and component calibration. Scheduled maintenance remains essential to prolonging vehicle life, enhancing safety, and optimizing performance. Fleet operators rely heavily on preventive maintenance programs, which provide predictable costs and minimal disruptions, supporting a consistent revenue stream for service providers.

China's Electric Commercial Vehicle MRO Market generated USD 92.1 million in 2024. Strong domestic production, policy support, and rapid fleet deployment have made the country a global frontrunner. Its booming urban delivery, public transport, and logistics sectors continue to elevate the need for robust, tech-enabled MRO services-from diagnostics to complex repairs.

Key industry players such as Daimler, Element Fleet Management, ATS Euromaster, BP Pulse, Ferdotti Motor Services, Scania, Lion Electric, MAN Global, Merchants Fleet, and Volvo are expanding their MRO portfolios. These companies are establishing dedicated EV service centers, enhancing technician training programs, and leveraging telematics for predictive maintenance. Strategic partnerships with automakers and fleet operators help them ensure efficient service delivery. AI-powered diagnostics and remote monitoring are becoming standard tools to accelerate repair cycles and minimize vehicle downtime.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Original equipment manufacturers

- 3.2.2 Independent service providers

- 3.2.3 Component suppliers

- 3.2.4 Technology providers

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Case study

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increased adoption of electric commercial fleets

- 3.9.1.2 Expansion of charging infrastructure

- 3.9.1.3 Declining costs of electric vehicles and batteries

- 3.9.1.4 Rise in demand for clean and sustainable transportation

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High Initial cost of electric commercial vehicles

- 3.9.2.2 Limited availability of skilled workforce

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 LCV

- 5.3 MCV

- 5.4 HCV

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Battery systems

- 6.3 Thermal management systems

- 6.4 Charging system

- 6.5 Electric drivetrain

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Service, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Maintenance

- 7.3 Repair

- 7.4 Overhaul

Chapter 8 Market Estimates & Forecast, By Service Provider, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 OEM service centers

- 8.3 Independent service providers

- 8.4 Fleet maintenance operations

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ATS Euromaster

- 10.2 BP Pulse

- 10.3 Daimler

- 10.4 Element Fleet Management

- 10.5 Ferdotti Motor Services

- 10.6 Kerlin Bus Sales & Leasing

- 10.7 Lightning eMotors

- 10.8 Lion Electric

- 10.9 MAN Global

- 10.10 Merchants Fleet

- 10.11 Northeastern Bus Rebuilders

- 10.12 Orange EV

- 10.13 Scania

- 10.14 Sonny Merryman

- 10.15 Transdev

- 10.16 VDL Company

- 10.17 VEV Services Limited

- 10.18 Volvo

- 10.19 WattEV

- 10.20 YES EU

全球專用車輛市場全球商用卡車市場

全球專用車輛市場全球商用卡車市場 全球回收卡車市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測全球平闆卡車市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測全球特種商用車市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測全球平闆卡車市場

全球回收卡車市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測全球平闆卡車市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測全球特種商用車市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測全球平闆卡車市場 2025年全球工業車輛市場報告

2025年全球工業車輛市場報告 印度攪拌機、果汁機和研磨機市場:依產品類型、價格範圍、應用、通路、地區、機會及預測,2019-2033攪拌機榨汁機·研磨機的全球市場的評估,各產品類型,各種價格,各用途,各流通管道,各地區,機會,預測,2018年~2032年乘用車座艙監控系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

印度攪拌機、果汁機和研磨機市場:依產品類型、價格範圍、應用、通路、地區、機會及預測,2019-2033攪拌機榨汁機·研磨機的全球市場的評估,各產品類型,各種價格,各用途,各流通管道,各地區,機會,預測,2018年~2032年乘用車座艙監控系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測