|

市場調查報告書

商品編碼

1716681

靜電集塵器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Electrostatic Precipitator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

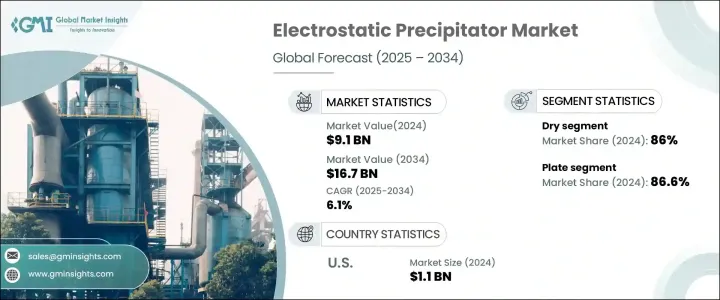

2024 年全球靜電集塵器市場規模達 91 億美元,預估 2025 年至 2034 年期間的複合年成長率為 6.1%。這一成長主要得益於新興經濟體的快速工業化,其中鋼鐵製造、化學品生產和燃煤發電等產業持續擴張。隨著這些產業的發展,對高效率排放控制系統的需求變得越來越重要。世界各國政府都在執行嚴格的環境法規,要求各產業採用先進技術有效管理空氣污染。靜電除塵器以其有效去除工業排放中的顆粒物的能力而聞名,隨著各行各業努力遵守這些嚴格的標準,靜電除塵器正受到越來越多的關注。此外,人們對環境永續性和減少有害排放的重要性的認知不斷提高,正在推動各行各業投資可靠的空氣污染控制技術。

人們對永續工業實踐的日益關注,以及公眾對空氣品質問題的認知不斷提高,進一步擴大了對靜電除塵器的需求。各行各業的公司都認知到需要對其污染控制系統進行現代化改造,以滿足不斷變化的環境標準並最大限度地減少碳足跡。隨著工業運作的擴大和政府實施更嚴格的空氣品質法規,新興經濟體(尤其是亞太地區的新興經濟體)對靜電除塵器的需求激增。此外,ESP技術的進步,包括能源效率和顆粒去除能力的提高,正在增強這些系統對於旨在平衡營運效率和環境合規性的行業的吸引力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 91億美元 |

| 預測值 | 167億美元 |

| 複合年成長率 | 6.1% |

2024 年,乾式靜電集塵器佔據了 86% 的市場佔有率,這反映了其在需要有效去除煙氣中顆粒物的行業中的受歡迎程度。這些系統在水泥和鋼鐵生產等行業尤其受到青睞,因為在這些行業中遵守嚴格的環境法規至關重要。乾式靜電集塵器能夠高效捕獲細顆粒物,同時保持較低的營運成本,使其成為尋求可靠排放控制解決方案的行業的首選。

根據設計,市場分為板式和管式部分,其中板式靜電集塵器在 2024 年將佔據 86.6% 的佔有率。板式 ESP 廣泛應用於工業應用,因為它們能夠以最小的能耗捕獲乾濕顆粒。它們的低營運成本和高效率使其成為需要可靠污染控制技術的行業的理想解決方案。

受污染控制技術持續投資和更嚴格的空氣品質法規實施的推動,美國靜電除塵器市場在 2024 年創造 11 億美元。隨著大眾對空氣品質的關注度不斷加深,靜電除塵器的採用預計將進一步增加,從而促進未來幾年市場的持續成長。對清潔空氣的需求不斷成長以及行業滿足環境合規標準的需求是支持美國靜電除塵器市場擴張的關鍵因素。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 戰略儀表板

- 創新與技術格局

第5章:市場規模及預測:依系統,2021 年至 2034 年

- 主要趨勢

- 乾燥

- 濕的

第6章:市場規模及預測:依設計,2021 年至 2034 年

- 主要趨勢

- 盤子

- 管狀

第7章:市場規模及預測:依排放業,2021 年至 2034 年

- 主要趨勢

- 發電

- 化學品和石化產品

- 水泥

- 金屬加工和採礦

- 製造業

- 海洋

- 其他

第8章:市場規模及預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 奈及利亞

- 安哥拉

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

- 秘魯

第9章:公司簡介

- Babcock and Wilcox Enterprises

- DURR Group

- DUCON

- FLSmidth

- Fuel Tech

- GEA Group

- GEECO Enercon

- KC Cottrell India

- Monroe Environmental

- Mitsubishi Heavy Industries.

- Sumitomo Heavy Industries

- Trion

- Valmet

- Wood

The Global Electrostatic Precipitator Market generated USD 9.1 billion in 2024 and is projected to grow at a CAGR of 6.1% between 2025 and 2034. This growth is primarily driven by the rapid industrialization of emerging economies, where industries such as steel manufacturing, chemical production, and coal-based power generation continue to expand. As these industries grow, the demand for efficient emissions control systems becomes increasingly critical. Governments worldwide are enforcing strict environmental regulations that require industries to implement advanced technologies to manage air pollution effectively. Electrostatic precipitators, known for their ability to efficiently remove particulate matter from industrial emissions, are gaining traction as industries strive to comply with these stringent standards. Additionally, growing awareness about environmental sustainability and the importance of reducing harmful emissions is pushing industries to invest in reliable air pollution control technologies.

The increasing focus on sustainable industrial practices, along with heightened public awareness of air quality concerns, is further amplifying the demand for electrostatic precipitators. Companies across various industries are recognizing the need to modernize their pollution control systems to meet evolving environmental standards and minimize their carbon footprint. Emerging economies, particularly in Asia-Pacific, are witnessing a surge in demand for electrostatic precipitators as industrial operations expand and governments enforce more rigorous air quality regulations. Moreover, advancements in ESP technology, including improvements in energy efficiency and particle removal capacity, are enhancing the appeal of these systems for industries aiming to balance operational efficiency with environmental compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.1 Billion |

| Forecast Value | $16.7 Billion |

| CAGR | 6.1% |

The dry electrostatic precipitator segment accounted for 86% of the market share in 2024, reflecting its popularity in industries that require efficient removal of particulate matter from flue gases. These systems are particularly favored in sectors such as cement and steel production, where maintaining compliance with strict environmental regulations is essential. Dry electrostatic precipitators offer high efficiency in capturing fine particles while keeping operational costs low, making them a preferred choice for industries seeking reliable emissions control solutions.

By design, the market is divided into plate and tubular segments, with plate electrostatic precipitators capturing an 86.6% share in 2024. Plate ESPs are widely used in industrial applications due to their ability to capture both dry and wet particles with minimal energy consumption. Their low operating costs and high efficiency make them an ideal solution for industries that need dependable pollution control technologies.

The US electrostatic precipitator market generated USD 1.1 billion in 2024, driven by continued investments in pollution control technologies and the implementation of stricter air quality regulations. As public concern about air quality intensifies, the adoption of electrostatic precipitators is expected to increase further, contributing to sustained market growth in the coming years. The rising demand for cleaner air and the need for industries to meet environmental compliance standards are key factors supporting the expansion of the US electrostatic precipitator market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By System, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Dry

- 5.3 Wet

Chapter 6 Market Size and Forecast, By Design, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Plate

- 6.3 Tubular

Chapter 7 Market Size and Forecast, By Emitting Industry, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Power generation

- 7.3 Chemicals and petrochemicals

- 7.4 Cement

- 7.5 Metal processing & mining

- 7.6 Manufacturing

- 7.7 Marine

- 7.8 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Indonesia

- 8.4.6 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.5.4 Nigeria

- 8.5.5 Angola

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Peru

Chapter 9 Company Profiles

- 9.1 Babcock and Wilcox Enterprises

- 9.2 DURR Group

- 9.3 DUCON

- 9.4 FLSmidth

- 9.5 Fuel Tech

- 9.6 GEA Group

- 9.7 GEECO Enercon

- 9.8 KC Cottrell India

- 9.9 Monroe Environmental

- 9.10 Mitsubishi Heavy Industries.

- 9.11 Sumitomo Heavy Industries

- 9.12 Trion

- 9.13 Valmet

- 9.14 Wood

靜電集塵器系統市場:2026-2032年全球市場預測(按終端用戶產業、技術類型、氣體類型、電極材料、額定功率、相數和管路配置分類)

靜電集塵器系統市場:2026-2032年全球市場預測(按終端用戶產業、技術類型、氣體類型、電極材料、額定功率、相數和管路配置分類) 全球化工與石化產業過程自動化市場(2025-2030 年)

全球化工與石化產業過程自動化市場(2025-2030 年) 靜電集塵器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、安裝類型、設備及解決方案分類全球靜電集塵器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

靜電集塵器市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、安裝類型、設備及解決方案分類全球靜電集塵器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球靜電集塵器市場報告

2026年全球靜電集塵器市場報告 靜電集塵器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按技術、設計、最終用戶、產品、地區和競爭格局分類),2021-2031年

靜電集塵器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按技術、設計、最終用戶、產品、地區和競爭格局分類),2021-2031年 靜電集塵器市場規模、佔有率及成長分析(按系統、設計、最終用途產業及地區分類)-2026-2033年產業預測

靜電集塵器市場規模、佔有率及成長分析(按系統、設計、最終用途產業及地區分類)-2026-2033年產業預測 全球靜電空氣濾清器市場

全球靜電空氣濾清器市場 2025-2033年靜電集塵器市場技術、設計、應用及地區報告

2025-2033年靜電集塵器市場技術、設計、應用及地區報告 化學品及石化產品靜電集塵器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

化學品及石化產品靜電集塵器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測