|

市場調查報告書

商品編碼

1698252

汽車熱交換器市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Automotive Heat Exchanger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

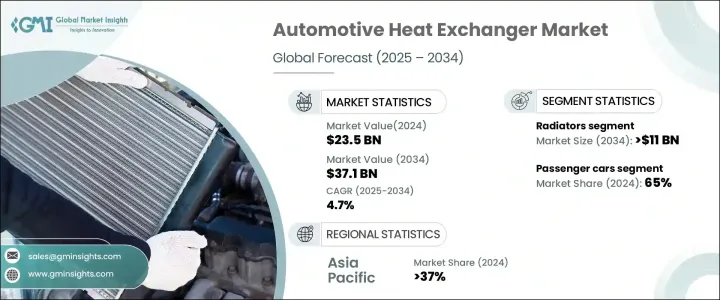

2024 年全球汽車熱交換器市場價值為 235 億美元,預計 2025 年至 2034 年的複合年成長率為 4.7%。全球範圍內電動車 (EV) 的日益普及和嚴格的排放法規正在推動對高效熱管理解決方案的需求。隨著充電基礎設施的改善和零件成本的下降,電動車的普及率正在上升,對熱管理系統的需求也隨之增加。廣泛應用於電動車的鋰離子電池需要在 15°C 至 35°C 範圍內穩定控制溫度,以確保電池的使用壽命和性能。熱交換器有助於維持最佳電池狀態,防止過熱並延長電池壽命。混合動力汽車也依靠這些系統來調節內燃機和電動馬達的溫度,確保高效運作。

美國、英國和中國等各國政府都在實施更嚴格的排放政策,促使汽車製造商開發先進的熱管理解決方案。正在採用廢氣再循環 (EGR) 系統等技術來減少氮氧化物排放並提高燃油效率。對永續性的日益重視進一步加速了熱管理的創新,使熱交換器成為現代車輛的關鍵部件。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 235億美元 |

| 預測值 | 371億美元 |

| 複合年成長率 | 4.7% |

汽車熱交換器市場按產品分類,其中散熱器佔據領先地位,2024 年市場佔有率超過 30%,預計到 2034 年將超過 110 億美元。散熱器對於引擎冷卻、防止過熱和最佳化燃油效率至關重要,尤其是在內燃機 (ICE) 汽車中。儘管替代燃料不斷湧現,但由於成本和易獲得性,汽油和柴油車輛仍然佔據主導地位,這加強了對高效冷卻系統的需求。

按車型分類,乘用車由於其廣泛使用,到 2024 年將佔據 65% 的市場佔有率。熱交換器對於確保這些車輛的安全性、舒適性和運作效率至關重要。汽車需求的不斷成長推動了中等輻射熱管理系統的採用,該系統包括散熱器、油冷卻器和冷凝器,以保持引擎的性能和壽命。

政府遏制排放的措施正在推動熱管理解決方案的進步。美國約 31% 的二氧化碳排放來自車輛,凸顯了更嚴格的監管和技術改進的必要性。增強型熱交換器系統擴大整合到車輛中以滿足不斷發展的標準,從而進一步推動市場成長。

從材料角度來看,鋁憑藉其成本效益、重量輕和高導熱性,將在 2024 年佔據市場主導地位。汽車行業正在轉向更輕的材料,以提高燃油效率和車輛性能,而鋁因其耐用性和耐腐蝕性而成為首選。這延長了組件的使用壽命,降低了製造商和消費者的長期成本。

在銷售通路方面,原始設備製造商 (OEM) 在 2024 年佔據了相當大的佔有率。汽車製造商與熱交換器製造商密切合作,開發適合車輛規格的標準和客製化組件。電動車和混合動力汽車市場的不斷成長促進了原始設備製造商和熱交換器供應商之間的合作,從而簡化了生產和整合流程。

2024 年,亞太地區佔據汽車熱交換器市場的 37% 佔有率,佔據主導地位。中國仍占主導地位,預計到 2034 年將達到 30 億美元。該地區強大的汽車製造基礎,加上較低的生產和勞動力成本,吸引了全球汽車製造商,推動了對熱交換器零件的高需求。此外,由於該地區汽車保有量高,這些零件的售後市場蓬勃發展,導致更換需求持續成長。

目錄

第1章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原物料供應商

- 熱交換器製造商

- 經銷商

- 最終用途

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞和舉措

- 價格趨勢

- 監管格局

- 衝擊力

- 成長動力

- 電動和混合動力汽車的成長

- 嚴格的排放和燃油效率法規

- 熱交換器材料的進步

- 汽車產量和需求不斷增加

- 產業陷阱與挑戰

- 材料和製造成本高

- 熱管理系統的複雜性

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 散熱器

- 中冷器

- 油冷卻器

- 廢氣再循環(EGR)

- 其他

第6章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 轎車

- 越野車

- 掀背車

- 商用車

- 輕型商用車

- 丙型肝炎病毒

- 越野車

第7章:市場估計與預測:依資料,2021 - 2034 年

- 主要趨勢

- 鋁

- 銅

- 其他

第8章:市場估計與預測:依設計,2021 - 2034 年

- 主要趨勢

- 板棒

- 管翅片

- 其他

第9章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第 11 章:公司簡介

- Ahaus Tool & Engineering

- AKG Group

- American Industrial Heat Transfer

- Banco Products

- Denso

- G&M Radiator

- Hanon Systems

- HAUGG Group

- Koyorad

- Mahle

- Modine Manufacturing

- Nippon Light Metals

- Nissens

- SM Auto Engineering

- Sanden

- Senior

- Spectra Premium

- T.RAD Co.

- Tokyo Radiator

- Valeo

The Global Automotive Heat Exchanger Market was valued at USD 23.5 billion in 2024 and is projected to grow at a CAGR of 4.7% from 2025 to 2034. The increasing adoption of electric vehicles (EVs) and stringent emission regulations worldwide are driving demand for efficient heat management solutions. With improvements in charging infrastructure and declining component costs, EV adoption is rising, leading to a greater need for thermal management systems. Lithium-ion batteries, widely used in EVs, require stable temperature control within 15°C to 35°C to ensure longevity and performance. Heat exchangers help maintain optimal battery conditions, preventing overheating and extending battery life. Hybrid vehicles also rely on these systems to regulate temperatures for both internal combustion engines and electric motors, ensuring efficient operation.

Governments in various countries, including the US, UK, and China, are enforcing stricter emissions policies, prompting automakers to develop advanced heat management solutions. Technologies like exhaust gas recirculation (EGR) systems are being incorporated to reduce nitrogen oxide emissions and enhance fuel efficiency. The growing emphasis on sustainability has further accelerated innovations in thermal management, making heat exchangers a crucial component in modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.5 Billion |

| Forecast Value | $37.1 Billion |

| CAGR | 4.7% |

The automotive heat exchanger market is categorized by product, with radiators leading at over 30% market share in 2024 and expected to surpass USD 11 billion by 2034. Radiators are essential for engine cooling, preventing overheating, and optimizing fuel efficiency, particularly in internal combustion engine (ICE) vehicles. Despite the rise of alternative fuels, gasoline and diesel vehicles remain prevalent due to cost and accessibility, reinforcing the demand for efficient cooling systems.

By vehicle type, passenger cars accounted for 65% of the market share in 2024, driven by their widespread usage. Heat exchangers are critical in these vehicles for ensuring safety, comfort, and operational efficiency. The increasing demand for automobiles is fueling the adoption of moderate radiation heat management systems that include radiators, oil coolers, and condensers to maintain engine performance and longevity.

Government initiatives to curb emissions are leading to advancements in thermal management solutions. Approximately 31% of CO2 emissions in the US originate from vehicles, emphasizing the need for stricter regulations and technological enhancements. Enhanced heat exchanger systems are increasingly integrated into vehicles to meet these evolving standards, further propelling market growth.

Material-wise, aluminum dominated the market in 2024, attributed to its cost-effectiveness, lightweight nature, and high thermal conductivity. The automotive industry is shifting towards more lightweight materials to improve fuel efficiency and vehicle performance, with aluminum emerging as the preferred choice due to its durability and resistance to corrosion. This extends component lifespan, reducing long-term costs for manufacturers and consumers.

In terms of sales channels, original equipment manufacturers (OEMs) held a significant share in 2024. Automakers collaborate closely with heat exchanger manufacturers to develop standard and custom components tailored to vehicle specifications. The growing EV and hybrid vehicle market has led to increased partnerships between OEMs and heat exchanger suppliers, streamlining production and integration processes.

Asia Pacific led the automotive heat exchanger market with a 37% share in 2024. China remains the dominant player, projected to reach USD 3 billion by 2034. The region's strong automobile manufacturing base, combined with lower production and labor costs, has attracted global automakers, driving high demand for heat exchanger components. Additionally, the aftermarket for these components is thriving due to the region's high vehicle population, leading to consistent replacement demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Heat exchanger manufacturers

- 3.2.3 Distributors

- 3.2.4 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Price trend

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Growth of electric and hybrid vehicles

- 3.9.1.2 Stringent emissions and fuel efficiency regulations

- 3.9.1.3 Advancements in heat exchanger material

- 3.9.1.4 Increasing vehicle production and demand

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High material and manufacturing costs

- 3.9.2.2 Complexity of thermal management systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Radiators

- 5.3 Intercoolers

- 5.4 Oil coolers

- 5.5 Exhaust gas recirculation (EGR)

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedan

- 6.2.2 SUV

- 6.2.3 Hatchback

- 6.3 Commercial vehicle

- 6.3.1 LCV

- 6.3.2 HCV

- 6.4 Off highway vehicle

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Aluminum

- 7.3 Copper

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Design, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Plate bar

- 8.3 Tube fin

- 8.4 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Ahaus Tool & Engineering

- 11.2 AKG Group

- 11.3 American Industrial Heat Transfer

- 11.4 Banco Products

- 11.5 Denso

- 11.6 G&M Radiator

- 11.7 Hanon Systems

- 11.8 HAUGG Group

- 11.9 Koyorad

- 11.10 Mahle

- 11.11 Modine Manufacturing

- 11.12 Nippon Light Metals

- 11.13 Nissens

- 11.14 S.M. Auto Engineering

- 11.15 Sanden

- 11.16 Senior

- 11.17 Spectra Premium

- 11.18 T.RAD Co.

- 11.19 Tokyo Radiator

- 11.20 Valeo

動力傳動系統熱交換器市場規模、佔有率和成長分析:按熱交換器類型、應用、材質、設計類型和地區分類-產業預測(2026-2033 年)

動力傳動系統熱交換器市場規模、佔有率和成長分析:按熱交換器類型、應用、材質、設計類型和地區分類-產業預測(2026-2033 年) 汽車熱交換器全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

汽車熱交換器全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 汽車熱交換器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按應用、設計類型、車輛類型、動力系統、地區和競爭格局分類,2021-2031年)

汽車熱交換器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按應用、設計類型、車輛類型、動力系統、地區和競爭格局分類,2021-2031年) 2025年全球汽車顯示器溫度控管市場報告

2025年全球汽車顯示器溫度控管市場報告 油氣熱交換器市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

油氣熱交換器市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球汽車熱交換器市場按類型、材料、翅片類型、車輛類型、應用、最終用戶、用途和銷售管道- 全球預測 2025-20322025年全球汽車熱交換器市場報告

全球汽車熱交換器市場按類型、材料、翅片類型、車輛類型、應用、最終用戶、用途和銷售管道- 全球預測 2025-20322025年全球汽車熱交換器市場報告 汽車熱交換器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

汽車熱交換器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 全球汽車熱交換器市場(按推進系統和零件、設計、車輛類型、電動車類型、非公路用車輛類型、地區分類)- 預測至 2032 年

全球汽車熱交換器市場(按推進系統和零件、設計、車輛類型、電動車類型、非公路用車輛類型、地區分類)- 預測至 2032 年 汽車熱交換器市場分析及預測(至2034年):類型、產品、技術、組件、應用、材料類型、最終用戶、功能、安裝類型、設備

汽車熱交換器市場分析及預測(至2034年):類型、產品、技術、組件、應用、材料類型、最終用戶、功能、安裝類型、設備