|

市場調查報告書

商品編碼

1996995

全球國防衛星通訊終端市場:2026-2036年Global Defense SATCOM Terminals Market 2026-2036 |

||||||

全球國防衛星通訊終端市場

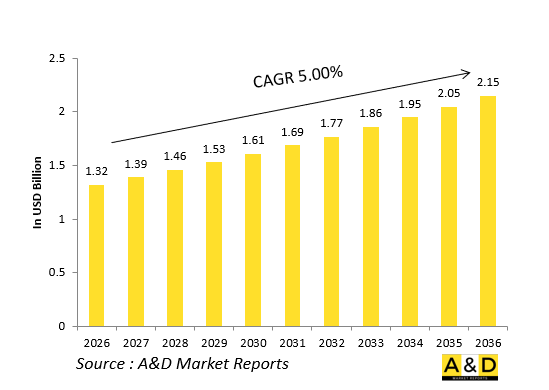

2026年全球國防衛星通訊終端市場規模估計為 13.2億美元,預計在2026年至2036年的預測期內將以 5.00%的年複合成長率成長,到2036年達到 21.5億美元。

1.引言:

國防衛星通訊(SATCOM)終端是任務關鍵型衛星星系。這些終端部署在飛機、艦艇、地面車輛、固定設施和步兵部隊上,提供超視距(BLOS)語音、資料和視訊鏈路,這些鏈路對於指揮控制、資訊傳播和聯合行動非常重要。隨著各國軍隊向網路化、多域作戰轉型,國防衛星通訊終端市場不斷擴大,這需要在2026年至2036年間保持持續的全球連結。

現代終端正從笨重的固定頻寬系統演變為緊湊型、多頻段、軟體定義單元,能夠處理多種波形、加密標準和軌道配置。這些終端與機載任務電腦、資料鏈路和基於IP的網路日益整合,實現了平台與指揮中心之間的無縫資料流。隨著衛星星系競爭的加劇,對具備抗干擾能力、低截獲機率和網路安全韌性的衛星通訊終端的需求日益成長,這些終端即使在電子對抗環境下也能保持連線。這些特性使衛星通訊終端成為數位戰生態系統中的核心基礎設施節點。

2.科技對國防衛星通訊終端市場的影響

技術進步正將國防衛星通訊終端從靜態的、基於硬體的無線電設備轉變為動態的、軟體定義的、網路感知節點。現代終端利用多頻段和多軌道能力,不僅能夠衛星群到傳統的地球靜止軌道,還能連接到新興的低地球軌道和中地球軌道星座。先進的數位訊號處理、自適應調變和波形捷變技術提高了頻譜效率和吞吐量,同時降低了受干擾和干擾的風險。

與戰術資料鏈路和基於IP的架構整合,衛星通訊終端不僅能夠傳輸語音,還能傳輸大量資料、影像和影片串流,支援即時情境察覺和任務計畫更新。諸如擴頻訊號、頻率捷變和自適應功率控制等頻譜和低截獲機率(LPI)功能,增強了在競爭激烈的射頻環境中的可靠性。安全金鑰管理、更快的加密處理和防篡改韌體等網路安全增強功能,可保護傳輸中的資料並防止未授權存取。小型化和低功耗使其能夠部署在小型無人機、攜帶式背包系統和空間有限的平台上。這些創新技術協同工作,提高了連接的可靠性、頻寬效率和生存能力,使衛星通訊終端成為現代空中、陸地和海上作戰中不可或缺的工具。

3.國防衛星通訊終端市場的主要促進因素

國防衛星通訊終端市場的需求源自於在分散式、一體化部隊結構中維持安全、永續且全球可用的連接。隨著作戰行動跨越多個戰區和領域,軍事負責人需要衛星通訊鏈路來支援即時指揮控制、資訊共用和後勤協調,而無需考慮平台位置。艦隊現代化和延壽計畫用支援先進波形和加密標準的多頻段軟體定義終端取代傳統的衛星通訊硬體。

電子戰威脅日益加劇和頻寬擁塞是推動衛星通訊發展的另一個主要動力,促使人們採用能夠在惡劣環境下運作的、具有強大抗干擾能力的衛星通訊終端。無人系統和分散式感測器的普及進一步增加了對緊湊型、低尺寸、輕重量、低功耗(SWaP)終端的需求,這些終端能夠將遠端平台的資料中繼到指揮中心。盟軍間的互通性需求推動了標準化衛星通訊通訊協定和介面定義的開發,實現共用和波形相容性。安全相關和任務關鍵型應用,例如空中預警和海上巡邏任務,也推動了對高可靠性、多通道衛星通訊架構的需求。所有這些因素共同促進了柔軟性、安全且互通性的衛星通訊終端解決方案的蓬勃發展。

4.國防衛星通訊終端市場的區域趨勢

從區域層面來看,北美仍然是先進衛星通訊終端研發的領先中心,這得益於其為戰鬥機、多用途飛機、海軍航空兵和地面部隊制定的大規模現代化計劃,這些計劃優先考慮安全的超視距通訊。美國及其合作夥伴經營廣泛的軍用和商用衛星基礎設施,並推動採購與現有和下一代衛星星系相容的多頻段、軟體定義和環境適應性強的衛星通訊終端。

在歐洲,聯合作戰航空和聯合部隊計劃推動通用衛星通訊終端標準和波形的採用,支援盟國之間的互通性和後勤共用。在亞太地區,多國空軍和海軍正利用衛星通訊快速擴展其遠程打擊和海上巡邏能力。在許多情況下,與區域衛星架構相銜接的國產或共同開發的終端解決方案更受青睞。中東和海灣國家投資建造現代化艦隊,其衛星通訊終端必須支援加密、容錯通訊鏈路,並能與西方和區域部隊互通性。在全部區域,對可在固定翼、旋翼、艦載和地面平台上重複使用和升級的模組化、開放式架構衛星通訊終端的需求日益成長。能夠最大限度減少電磁干擾並降低頻率管理複雜性的設計同樣非常重要。

5.主要國防衛星通訊終端市場計畫

2026年至2036年間,多項重大國防計畫將塑造衛星通訊終端市場。下一代戰鬥機和多用途作戰飛機舉措需要與數位任務電腦和資料鏈路緊密整合的先進衛星通訊終端,以便在複雜的聯合作戰行動中實現安全的遠端語音和資料通訊。海軍航空兵和航空母艦打擊群計畫則依賴強大的衛星通訊終端,用於衝突地區環境下的艦空通訊、艦隊範圍內的協調以及全球指揮控制。

在無人作戰飛行器(UAV)和長途飛行無人機專案中,緊湊型衛星通訊終端正用於支援超視距中繼和資料下行鏈路能力,同時保持頻寬效率和平台機動性。陸軍和特種作戰計畫投資行動和攜帶式衛星通訊終端,以在惡劣環境和都市區實現安全、高頻寬的連接。多域和聯盟層級的專案推進衛星通訊終端波形和介面的標準化,實現夥伴國家之間程序、培訓和後勤支援的共用。透過這些計畫,衛星通訊終端正從簡單的衛星連接無線電發展成為整合化的、網路化的組件,支援在所有作戰領域(空中、陸地和海上)實現安全、永續且全球可用的戰場通訊。

目錄

國防衛星通訊終端市場 - 目錄

國防衛星通訊終端市場報告定義

國防衛星通訊終端市場細分

依地區

依平台

依頻段

依設備尺寸

依資料速率

未來十年國防衛星通訊終端市場分析

本章基於對國防衛星通訊終端市場 10年的分析,詳細概述了國防衛星通訊終端市場的成長、發展趨勢、技術採用和市場吸引力。

國防衛星通訊終端市場的技術趨勢

本節將說明預計將對該市場產生影響的十大技術及其對整個市場的潛在影響。

全球國防衛星通訊終端市場預測

本市場對國防衛星通訊終端市場未來 10年的發展趨勢進行了全面預測,涵蓋了上述各個細分市場。

區域國防衛星通訊終端市場趨勢及預測。

本節說明了無人機市場的區域趨勢、促進因素、限制、挑戰以及政治、經濟、社會和技術方面。此外,還提供了詳細的區域市場預測和情境分析。區域分析的最後一部分涵蓋了主要企業概況、供應商格局和公司基準。目前的市場規模估算是基於典型情境。

北美洲

促進因素、阻礙因素和挑戰

PEST

市場預測與情境分析

主要企業

供應商層級狀態

企業標竿管理

歐洲

中東

亞太地區

南美洲

對國防衛星通訊終端市場進行國別分析。

本章將說明該市場的主要國防計畫,以及該市場的最新新聞和專利申請。此外,還將說明針對特定國家的十年市場預測和情境分析。

美國

國防計劃

最新消息

專利

該市場目前的技術成熟度水準

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防衛星通訊終端市場機會矩陣

機會矩陣幫助讀者了解該市場中具有高機會的細分市場。

專家對國防衛星通訊終端市場報告的意見

總結了專家們對該市場分析潛力的意見。

結論

關於航空航太和國防市場報告

Global Defense SATCOM Terminals Market

The Global Defense SATCOM Terminals Market is estimated at USD 1.32 billion in 2026, projected to grow to USD 2.15 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 5.00% over the forecast period 2026-2036.

1. Introduction:

Defense satellite communication (SATCOM) terminals are mission critical radio systems that enable secure, long range connectivity between military platforms and global command networks via geostationary and, increasingly, multi orbit satellite constellations. These terminals are deployed on aircraft, naval vessels, ground vehicles, fixed installations, and dismounted teams, providing beyond line of sight voice, data, and video links essential for command and control, intelligence dissemination, and joint operations. Over the 2026-2036 horizon, the defense SATCOM terminal market is expanding as armed forces shift toward networked, multi domain warfare that demands persistent, global connectivity.

Modern terminals are evolving from bulky, fixed band systems into compact, multi band, software defined units capable of supporting multiple waveforms, encryption standards, and orbital regimes. They are increasingly integrated with onboard mission computers, datalinks, and IP based networks, enabling seamless data flow between platforms and headquarters. As satellite constellations become more contested, demand is growing for anti jamming, low probability of intercept, and cyber hardened SATCOM terminals that can maintain connectivity in electronically hostile environments. These attributes position SATCOM terminals as core infrastructure nodes in the digital warfare ecosystem.

2. Technology Impact in Defense SATCOM Terminals Market

Technology is transforming defense SATCOM terminals from static, hardware based radios into dynamic, software defined, network aware nodes. Modern terminals leverage multi band and multi orbital capabilities, allowing links to both traditional geostationary and emerging low and medium Earth orbit constellations. Advanced digital signal processing, adaptive modulation, and waveform agility improve spectral efficiency and throughput while reducing susceptibility to jamming and interference.

Integration with tactical datalinks and IP based architectures enables SATCOM terminals to carry not only voice but also high volume data, imagery, and video streams, supporting real time situational awareness and mission planning updates. Anti jamming and low probability of intercept features such as spread spectrum signaling, frequency agility, and adaptive power control enhance resilience in contested RF environments. Cybersecurity enhancements, including secure key management, cryptographic acceleration, and tamper resistant firmware, protect data in transit and prevent unauthorized access. Miniaturization and reduced power consumption are enabling deployment on small UAVs, handheld backpack systems, and tightly sized platforms. These innovations collectively raise connectivity reliability, bandwidth efficiency, and survivability, making SATCOM terminals indispensable in modern air, land, and sea operations.

3. Key Drivers in Defense SATCOM Terminals Market

The defense SATCOM terminal market is driven by the need to maintain secure, persistent, and globally available connectivity across dispersed joint force structures. As operations span multiple theaters and domains, military planners require SATCOM links that support real time command and control, intelligence sharing, and logistics coordination regardless of platform location. Fleet modernization and life extension programs are replacing legacy SATCOM hardware with multi band, software defined terminals that support advanced waveforms and encryption standards.

Another key driver is the growing threat of electronic warfare and spectrum congestion, which is pushing adoption of hardened, anti jamming SATCOM terminals that can operate in contested environments. The proliferation of unmanned systems and distributed sensors further increases demand for compact, low SWaP terminals that can relay data from remote platforms back to command centers. Interoperability requirements across allied forces are encouraging standardized SATCOM protocols and interface definitions, enabling shared satellite access and waveform compatibility. Safety related and mission critical applications, such as airborne early warning and maritime patrol missions, also reinforce demand for high reliability, multi channel SATCOM architectures. Together, these factors sustain strong growth in flexible, secure, and interoperable SATCOM terminal solutions.

4. Regional Trends in Defense SATCOM Terminals Market

Regionally, North America remains a leading hub for advanced SATCOM terminal development, supported by large scale fighter, multi role, naval aviation, and ground forces modernization programs that emphasize secure, beyond line of sight communications. The United States and its partners operate extensive military and commercial satellite infrastructures, driving procurement of multi band, software defined, and hardened SATCOM terminals compatible with both legacy and next generation constellations.

In Europe, collaborative combat air and joint force initiatives are encouraging adoption of common SATCOM terminal standards and waveforms, supporting interoperability and shared logistics across allied nations. The Asia Pacific region is witnessing rapid growth as several air forces and navies expand their SATCOM enabled long range strike and maritime patrol capabilities, often favoring indigenous or co developed terminal solutions tied to regional satellite architectures. Middle Eastern and Gulf states are investing in modernized fleets whose SATCOM terminals must support both encrypted, resilient links and interoperability with a mix of Western and regional forces. Across these regions, there is a growing preference for modular, open architecture SATCOM terminals that can be reused or upgraded across fixed wing, rotary wing, naval, and ground platforms, alongside designs that minimize electromagnetic interference and spectrum management complexity.

5. Key Defense SATCOM Terminals Market Program

Several flagship defense programs are shaping the SATCOM terminal market over the 2026-2036 period. Next generation fighter and multi role combat air initiatives are specifying advanced SATCOM terminals that integrate tightly with digital mission computers and datalinks, enabling secure, long range voice and data exchanges during complex joint force operations. Naval aviation and carrier strike programs rely on robust SATCOM terminals for ship to air, fleet wide coordination, and global reach command and control in contested maritime environments.

Unmanned combat air and long endurance UAV programs are adopting compact SATCOM terminals that support beyond line of sight relay and data downlink functions while preserving spectrum efficiency and platform agility. Ground forces and special operations programs are investing in mobile and handheld SATCOM terminals that enable secure, high bandwidth connectivity in austere and urban environments. Multi domain and coalition level programs are standardizing SATCOM terminal waveforms and interfaces, enabling shared procedures, training, and logistics support across partner nations. Through these programs, SATCOM terminals are evolving from simple satellite linked radios into integrated, network capable elements that underpin secure, persistent, and globally available battlefield communications across the full spectrum of air, land, and sea operations.

Table of Contents

Defense SATCOM Terminals Market - Table of Contents

Defense SATCOM Terminals Market Report Definition

Defense SATCOM Terminals Market Segmentation

By Region

By Platform

By Band

By Terminal Size

By Data Rate

Defense SATCOM Terminals Market Analysis for next 10 Years

The 10-year Defense SATCOM Terminals Market analysis would give a detailed overview of Defense SATCOM Terminals Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense SATCOM Terminals Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense SATCOM Terminals Market Forecast

The 10-year Defense SATCOM Terminals Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense SATCOM Terminals Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense SATCOM Terminals Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense SATCOM Terminals Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense SATCOM Terminals Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Band, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Band, 2026-2036

List of Figures

- Figure 1: Global Defense SATCOM Terminals Market Forecast, 2026-2036

- Figure 2: Global Defense SATCOM Terminals Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense SATCOM Terminals Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense SATCOM Terminals Market Forecast, By Band, 2026-2036

- Figure 5: North America, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 6: Europe, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 8: APAC, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 10: United States, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 11: United States, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 12: Canada, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 13: Canada, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 14: Italy, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 15: Italy, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 16: France, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 17: France, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 19: Germany, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 23: Belgium, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 25: Spain, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 27: Sweden, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 29: Brazil, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 31: Australia, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 32: India, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 33: India, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 34: China, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 35: China, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 39: South Korea, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 41: Japan, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 45: Singapore, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense SATCOM Terminals Market, Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense SATCOM Terminals Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense SATCOM Terminals Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense SATCOM Terminals Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense SATCOM Terminals Market, By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense SATCOM Terminals Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense SATCOM Terminals Market, By Band(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense SATCOM Terminals Market, By Band(CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense SATCOM Terminals Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense SATCOM Terminals Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense SATCOM Terminals Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense SATCOM Terminals Market, By Region, 2026-2036

- Figure 58: Scenario 1, Defense SATCOM Terminals Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense SATCOM Terminals Market, By Band, 2026-2036

- Figure 60: Scenario 2, Defense SATCOM Terminals Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense SATCOM Terminals Market, By Region, 2026-2036

- Figure 62: Scenario 2, Defense SATCOM Terminals Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense SATCOM Terminals Market, By Band, 2026-2036

- Figure 64: Company Benchmark, Defense SATCOM Terminals Market, 2026-2036