|

市場調查報告書

商品編碼

1951145

全球國防衛星通訊罩市場:2026-2036年Global Defense SATCOM Domes Market 2026-2036 |

||||||

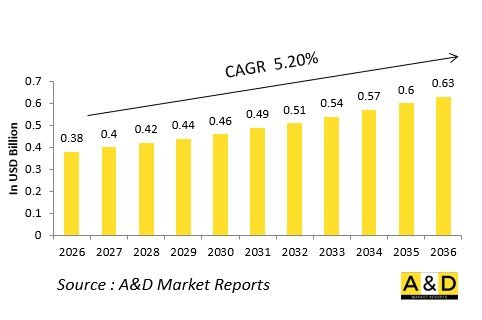

全球國防衛星通訊罩市場預計將從2026年的3.8億美元成長到2036年的6.3億美元,2026年至2036年的年複合成長率(CAGR)為 5.20%。

簡介:

全球國防衛星通訊罩市場處於安全軍事通訊的前沿,為指揮、控制和情報行動提供強大的衛星連結。這些專用外殼可保護天線免受惡劣環境的影響,同時確保即使在作戰環境中也能保持不間斷的連接。地緣政治緊張局勢加劇和多域戰爭的演變,正推動著對整合相控陣技術和低可觀測性設計的先進雷達罩的需求激增。自適應波束成形和抗干擾能力等關鍵創新對於船艦、地面站和空中平台非常重要。領先企業正大力投資研發耐環境材料,例如具有增強射頻透明度和隱身性能的雷達罩,以應對電子戰威脅。不斷成長的全球國防預算,尤其是優先發展以網路為中心的作戰,推動市場發展。新興應用擴展到高超音速平台和無人系統,在這些領域,緊湊型、高吞吐量的雷達罩仍然具有優勢。總體而言,在日益複雜的作戰環境中,對無縫和安全衛星通訊的需求不斷成長,預計該行業將持續發展。

科技對國防衛星通訊雷達罩的影響

技術創新革新國防衛星通訊雷達罩,提升其在高頻寬任務的效能。整合在穹頂內的相控陣天線可實現電子波束控制,無需機械萬向節,提高追蹤速度並降低被干擾的風險。多頻段運轉支援在X、Ku和Ka波段同時運作,最佳化擁擠頻譜中的頻譜效率。材料科學的進步催生了具有優異介電性能的輕量複合材料的開發,最大限度地減少了訊號損耗並提高了增益。穹頂設計整合了抗干擾和低截獲機率功能,並採用氮化鎵放大器以實現高功率耐久性。人工智慧賦能的自主系統能夠預測干擾並動態調整波形。與軟體定義無線電的整合實現了無縫升級並延長了使用壽命。這些創新降低尺寸、重量和功耗,這對軍艦和無人機等行動平台非常重要。衛星通訊穹頂正從被動屏蔽裝置發展成為在受干擾環境中保持資訊優勢的主動核心設備。

國防衛星通訊罩市場的主要驅動因素

推動國防衛星通訊罩市場發展的因素是多方面的。日益激烈的強國競爭需要強大且抗干擾的通訊能力,以支援空中、陸地、海洋和太空領域的聯合行動。現代化專案用配備高頻寬即時資料共享能力的新一代通訊罩取代傳統系統。海軍艦隊的電氣化和無人機艦隊的擴張需要緊湊、可適應惡劣環境的設計。對頻譜效率和網路安全標準的監管壓力推動先進雷達通訊罩技術的應用。隨著各國為降低地緣政治風險而實現採購來源多元化,供應鏈韌性也成為一個驅動因素。北約等聯盟內部的互通性要求加速標準化通訊罩的部署。耐氣候材料能夠滿足極地和沙漠地區日益成長的作戰需求。對反太空能力的投資間接推動了衛星通訊罩的銷售,因為敵方會以衛星為目標,帶動了對低地球軌道(LEO)終端的廣泛需求。這些因素共同作用,使衛星通訊罩成為面向未來的防禦架構的重要組成部分。

國防衛星通訊罩的區域趨勢

區域趨勢揭示了國防衛星通訊罩市場的清晰發展方向。北美在為航母打擊群和遠徵部隊積極採購方面處於領先地位,重點是推廣隱身和高頻能力的通訊罩。歐洲正致力於透過聯合計畫來提高北約的互通性,並在東線局勢緊張的情況下優先發展多軌道能力。亞太地區正經歷快速擴張,主要得益於海上衝突以及主要大國國內生產能力的提升。印太地區的盟國投資用於島嶼間通訊場景的行動通訊罩,並整合增強型5G連結。中東市場則優先考慮適用於沙漠環境的通訊罩,以建構持續監視網路。新興趨勢包括推動在南美和非洲進行在地化生產,以服務維和與邊境安全。區域合作加速技術轉讓,將美國的創新與歐洲的製造能力結合。總體而言,低成本衛星星座的日益普及推動了對經濟實惠、可擴展的衛星通訊罩的需求,以應對獨特的區域威脅。 本報告深入分析了全球國防衛星通訊罩市場,全面剖析了關鍵趨勢、市場影響因素、關鍵技術及其影響、主要地區和國家的市場趨勢以及市場機會。

目錄

國防衛星通訊罩市場:目錄

國防衛星通訊罩市場:報告定義

國防衛星通訊罩市場:細分

依地區

依平台

依尺寸

依材料

未來十年國防衛星通訊罩市場分析

國防衛星通訊罩市場成長、趨勢變化、技術應用概要及市場吸引力詳情

國防衛星通訊罩市場:技術

預計將影響市場的十大技術及其對整體市場的潛在影響

全球國防衛星通訊罩市場:預測

以上各細分市場均詳細涵蓋了未來十年的市場預測。

國防衛星通訊穹頂市場趨勢及預測:依地區劃分

本報告涵蓋市場趨勢、驅動因素、限制因素、挑戰以及政治、經濟、社會和技術因素。報告還提供了詳細的區域市場預測和情境分析。區域分析最後對主要公司、供應商格局和公司基準進行了概述。目前市場規模是基於正常情境估算的。

北美

驅動因素、限制因素與挑戰

PEST 分析

市場預測與情境分析

主要公司

供應商層級

公司標竿分析

歐洲

中東

亞太地區

南美洲

國防衛星通訊穹頂市場:國家分析

美國

國防計畫

最新資訊

專利

當前市場技術成熟度

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防衛星通訊穹頂市場:機會矩陣

專家對國防衛星通訊穹頂市場報告的見解

概述討論

關於航空和國防市場報告

The Global Defense SATCOM domes market is estimated at USD 0.38 billion in 2026, projected to grow to USD 0.63 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 5.20% over the forecast period 2026-2036.

Introduction:

The Global defense SATCOM domes market stands at the forefront of secure military communications, enabling resilient satellite links for command, control, and intelligence operations. These specialized enclosures protect antennas from harsh environments while ensuring uninterrupted connectivity in contested battlespaces. As geopolitical tensions escalate and multi-domain warfare evolves, demand surges for advanced domes integrating phased-array technologies and low-observable designs. Key innovations include adaptive beamforming and anti-jam capabilities, vital for naval vessels, ground stations, and airborne platforms. Major players invest heavily in ruggedized materials like radomes with enhanced RF transparency and stealth features to counter electronic warfare threats. The market benefits from rising defense budgets worldwide, prioritizing network-centric operations. Emerging applications extend to hypersonic platforms and unmanned systems, where compact, high-throughput domes maintain superiority. Overall, this sector promises sustained growth, driven by the need for seamless, secure SATCOM in increasingly complex operational theaters.

Technology Impact in Defense SATCOM Domes

Technological advancements profoundly shape defense SATCOM domes, elevating performance in bandwidth-intensive missions. Phased-array antennas embedded within domes enable electronic beam steering, eliminating mechanical gimbals for faster tracking and reduced vulnerability. Multi-band operations support simultaneous X, Ku, and Ka frequencies, optimizing spectrum use amid spectrum congestion. Materials science breakthroughs yield lightweight composites with superior dielectric properties, minimizing signal loss and boosting gain. Anti-jam and low-probability-of-intercept features integrate into dome designs, incorporating gallium nitride amplifiers for high-power resilience. Artificial intelligence enhances dome autonomy, predicting interference and dynamically adjusting waveforms. Integration with software-defined radios allows seamless upgrades, extending lifecycle utility. These innovations reduce size, weight, and power demands, critical for mobile platforms like warships and UAVs. Consequently, SATCOM domes evolve from passive shields to active enablers of tactical superiority, transforming how forces maintain information dominance in denied environments.

Key Drivers in Defense SATCOM Domes

Several forces propel the defense SATCOM domes market forward. Heightened great-power competition demands robust, jam-resistant communications to sustain joint operations across air, land, sea, and space domains. Modernization programs replace legacy systems with next-generation domes featuring wideband capabilities for real-time data sharing. Electrification of naval fleets and expansion of drone swarms necessitate compact, conformal designs enduring extreme conditions. Regulatory pushes for spectrum efficiency and cybersecurity standards spur adoption of advanced radome technologies. Supply chain resilience emerges as a driver, with nations diversifying sourcing to mitigate geopolitical risks. Interoperability requirements under allied frameworks like NATO accelerate standardized dome deployments. Climate-resilient materials address rising operational demands in polar and desert theaters. Investment in counter-space capabilities indirectly boosts dome sales, as adversaries target satellites, heightening needs for proliferated low-Earth orbit terminals. Collectively, these drivers position SATCOM domes as indispensable for future-proofed defense architectures.

Regional Trends in Defense SATCOM Domes

Regional dynamics reveal distinct trends in the defense SATCOM domes landscape. North America leads with aggressive procurement for carrier strike groups and expeditionary forces, emphasizing stealthy, high-frequency domes. Europe focuses on collaborative programs enhancing NATO interoperability, prioritizing multi-orbit compatibility amid Eastern flank tensions. Asia-Pacific sees rapid expansion, fueled by maritime disputes and indigenous production ramps in key powers. Indo-Pacific allies invest in mobile domes for island-hopping scenarios, integrating 5G-augmented links. Middle East markets prioritize desert-hardened variants for persistent surveillance networks. Emerging trends include localization efforts in South America and Africa, driven by peacekeeping mandates and border security. Cross-regional partnerships accelerate technology transfers, blending U.S. innovation with European manufacturing prowess. Overall, proliferation of low-cost proliferated constellations spurs demand for affordable, scalable domes tailored to regional threats.

Key Defense SATCOM Domes Programs

Prominent defense SATCOM domes programs underscore strategic priorities worldwide. Naval initiatives feature enterprise-wide upgrades for destroyer and submarine fleets, deploying flat-panel domes with automated tracking for blue-water dominance. Airborne programs equip strategic bombers and tankers with low-drag enclosures supporting beyond-line-of-sight relays. Ground-based efforts include tactical vehicle kits with rapid-deploy radomes for special operations. Collaborative allied ventures develop common apertures interoperable across constellations, reducing logistical burdens. Hypersonic testbeds integrate experimental domes resilient to aero-thermal stresses. Unmanned systems programs embed miniaturized variants in loyal wingman drones and undersea vehicles. Key milestones involve live-fire survivability demos and multi-domain exercises validating performance. These programs not only field cutting-edge hardware but also pioneer sustainment models like modular upgrades, ensuring long-term relevance amid evolving threats.

Table of Contents

Defense SATCOM Domes Market - Table of Contents

Defense SATCOM Domes Market Report Definition

Defense SATCOM Domes Market Segmentation

By Region

By Platform

By Size

By Material

Defense SATCOM Domes Market Analysis for next 10 Years

The 10-year Defense SATCOM Domes Market analysis would give a detailed overview of Defense SATCOM Domes Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense SATCOM Domes Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense SATCOM Domes Market Forecast

The 10-year Defense SATCOM Domes Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense SATCOM Domes Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense SATCOM Domes Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense SATCOM Domes Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense SATCOM Domes Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Size, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Size, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Region, 2026-2036

List of Figures

- Figure 1: Global Defense Satcom Domes Market Forecast, 2026-2036

- Figure 2: Global Defense Satcom Domes Market Forecast, By Size, 2026-2036

- Figure 3: Global Defense Satcom Domes Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Satcom Domes Market Forecast, By Region, 2026-2036

- Figure 5: North America, Defense Satcom Domes Market, Forecast, 2026-2036

- Figure 6: Europe, Defense Satcom Domes Market, Forecast, 2026-2036

- Figure 7: Middle East, Defense Satcom Domes Market, Forecast, 2026-2036

- Figure 8: APAC, Defense Satcom Domes Market, Forecast, 2026-2036

- Figure 9: South America, Defense Satcom Domes Market, Forecast, 2026-2036

- Figure 10: United States, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 11: United States, Defense Satcom Domes Market, Forecast, 2026-2036

- Figure 12: Canada, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Defense Satcom Domes Market, Forecast, 2026-2036

- Figure 14: Italy, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 17: France, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense Satcom Domes Market, Forecast, 2026-2036

- Figure 28: Brazil, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 33: India, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 35: China, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Satcom Domes Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Satcom Domes Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Satcom Domes Market, By Size(Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Satcom Domes Market, By Size(CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Satcom Domes Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Satcom Domes Market, By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Satcom Domes Market, By Region (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Satcom Domes Market, By Region (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Satcom Domes Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Satcom Domes Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Satcom Domes Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Satcom Domes Market, By Size, 2026-2036

- Figure 58: Scenario 1, Defense Satcom Domes Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Satcom Domes Market, By Region, 2026-2036

- Figure 60: Scenario 2, Defense Satcom Domes Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Satcom Domes Market, By Size, 2026-2036

- Figure 62: Scenario 2, Defense Satcom Domes Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Satcom Domes Market, By Region, 2026-2036

- Figure 64: Company Benchmark, Defense Satcom Domes Market, 2026-2036