|

市場調查報告書

商品編碼

1936044

全球戰鬥機登機梯市場(2026-2036)Global Defense Fighter Aircraft Boarding Ladders Market 2026-2036 |

||||||

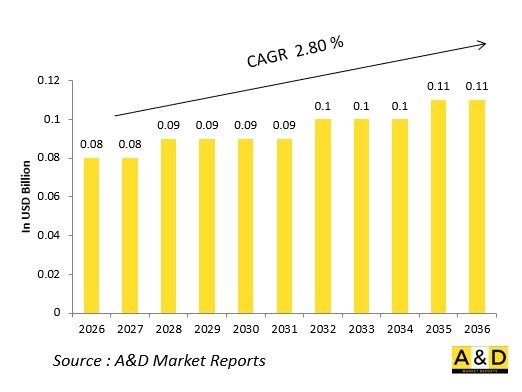

據估計,全球戰鬥機登機梯市場在2026年價值8,000萬美元,預計到2036年將達到1.1億美元,2026年至2036年的複合年增長率為2.80%。

引言

全球戰鬥機登機梯市場在提升世界各國空軍的作戰準備方面發揮著至關重要的作用。這些專用梯子為作戰人員提供了至關重要的登機解決方案,確保飛行員在執行任務、維護或快速部署期間能夠快速登機和下機。隨著國防部隊在熱點地區優先考慮機動性,對耐用、便攜且易於使用的梯子的需求正在飆升。

市場發展反映了航空航太保障領域的更廣泛趨勢,登機梯已從基本的機械輔助設備發展成為與飛機平台整合的智慧系統。製造商正在創新地採用耐腐蝕合金、複合材料和模組化設計,以適應從傳統平台到下一代隱形飛機的各種戰鬥機型號。輕量化結構最大限度地減少了後勤負擔,而折疊和伸縮機構則加快了在條件惡劣的機場上的安裝速度。

地緣政治緊張局勢和現代化計劃正在推動採購,空軍正在尋求與先進航空電子設備和感測器套件相容的梯子。抵禦極端天氣和電磁幹擾的能力是供應鏈中的關鍵優先事項。競爭格局的特點是成熟的航太公司與專業供應商並存,從而促進了客製化解決方案的合作。該市場凸顯了地面支援設備與空中優勢之間的關鍵聯繫,在國防預算不斷增長和技術融合的背景下,預計將實現持續成長。

國防戰鬥機登機梯市場的主要驅動因素

推動國防戰鬥機登機梯市場發展的因素很多。機隊現代化是重中之重,空軍正在用先進平台取代老舊戰鬥機,而這些先進平台需要精確且相容的登機解決方案。這種轉變推動了高度可調梯子和隱身兼容材料的研發,對隱身設計、低可觀測性塗層以及與高架機身無縫整合的方向舵設計提出了更高的要求。

另一個驅動因素是作戰節奏的加快,這是由強調在勢均力敵的對手作戰場景中快速部署和高出動率的戰術理論所驅動的。為了支援在前線作戰基地快速登機,設計必須注重便攜性、單手展開以及耐沙、耐鹽和耐極寒。物流優化也在推動需求,減輕重量可以降低運輸成本並融入空運供應鏈。

地緣政治格局的重組正在推動採購需求,尤其是在加強空中威懾的地區。出口導向生產受益於盟友間的互通性標準,並促進了舵面介面的標準化。永續性要求推動了可再生複合材料和低維護塗層的應用,以符合環保採購政策。確保供應鏈的韌性推動了在中斷後採取本地生產和雙重採購策略。

飛行員安全和降低受傷風險等人為因素強調符合人體工學的設計,例如減少疲勞的底座和整合照明。抗衝擊性和防火性的法規要求進一步影響產品規格。這些因素使得登機梯成為空中優勢的關鍵要素,並與更廣泛的航空航太保障生態系統緊密相連。

國防戰鬥機登機梯區域趨勢

區域動態凸顯了國防戰鬥機登機梯市場的明顯趨勢。亞太地區空軍的快速擴張使其高度重視國內生產,以支援不斷增長的多用途戰鬥機機隊。各國優先考慮適用於熱帶氣候和島嶼間作戰的堅固耐用型登機梯,從而促進了本地供應商的發展,並將其納入抵消貿易合約。

本報告分析了全球國防戰鬥機登機梯市場,深入探討了影響該市場的技術、未來十年的預測以及區域趨勢。

目錄

戰鬥機登機梯市場報告定義

戰鬥機登機梯市場細分

依整合類型

依展開機制

依材料

依飛機類型

依儲存位置

未來十年戰鬥機登機梯市場分析

戰鬥機登機梯市場技術

全球戰鬥機登機梯市場預測

區域戰鬥機登機梯市場趨勢及預測

北美

驅動因素、限制因素及挑戰

PEST分析

市場預測與情境分析

主要公司

供應商等級

公司標竿分析

歐洲

中東

亞太地區

南美洲

國防戰鬥機登機梯市場國家分析

美國

國防項目

最新消息

專利

當前市場技術成熟度

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

戰鬥機登機梯市場機會矩陣

戰鬥機登機梯市場專家意見

結論

關於航空與國防市場報告

The Global Defense Fighter Aircraft Boarding Ladders Market is estimated at USD 0.08 billion in 2026, projected to grow to USD 0.11 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 2.80% over the forecast period 2026-2036.

Introduction

The global Defense Fighter Aircraft Boarding Ladders market plays a vital role in enhancing operational readiness for air forces worldwide. These specialized ladders provide essential access solutions for fighter jets, ensuring pilots can board and disembark swiftly during missions, maintenance, or rapid deployments. As defense forces prioritize agility in contested environments, demand surges for ladders that combine durability, portability, and ease of use.

Market evolution reflects broader trends in aerospace sustainment, where boarding ladders evolve from basic mechanical aids to smart systems integrated with aircraft platforms. Manufacturers innovate with corrosion-resistant alloys, composite materials, and modular designs that adapt to various fighter models, from legacy platforms to next-generation stealth aircraft. Emphasis on reduced weight minimizes logistical burdens, while foldable and telescopic mechanisms accelerate setup in austere airfields.

Geopolitical tensions and modernization programs drive procurement, with air forces seeking ladders compatible with advanced avionics and sensor suites. Supply chains emphasize ruggedization against extreme weather and electromagnetic interference. Competitive landscapes feature established aerospace firms alongside specialized suppliers, fostering collaborations for customized solutions. This market underscores the critical link between ground support equipment and aerial superiority, promising sustained growth amid rising defense budgets and technological convergence.

Technology Impact in Defense Fighter Aircraft Boarding Ladders

Technological advancements profoundly shape the Defense Fighter Aircraft Boarding Ladders sector, transforming simple access tools into high-performance assets. Integration of lightweight composites and carbon fiber reduces overall mass, enabling faster deployment without compromising structural integrity under high winds or rough terrain. Automation emerges as a game-changer, with hydraulic or electric actuators allowing one-person operation and automatic stabilization sensors that adjust to aircraft tilt.

Smart materials, such as shape-memory alloys, enable self-deploying ladders that respond to environmental cues, minimizing human error in high-stress scenarios. Embedded IoT sensors monitor wear, predict maintenance needs, and transmit data to base stations, aligning with predictive logistics trends in modern air forces. Compatibility with fighter jet canopies incorporates non-slip surfaces treated with advanced coatings to prevent icing or chemical exposure.

Additive manufacturing accelerates prototyping of custom ladder segments, tailored to specific aircraft variants like multirole fighters or lightweight interceptors. Electromagnetic shielding protects against directed-energy threats, while modular designs facilitate rapid reconfiguration for different mission profiles. These innovations enhance sortie generation rates, reduce turnaround times, and bolster safety protocols. Ultimately, technology elevates boarding ladders from ancillary gear to integral components of networked air operations, driving efficiency in contested airspace.

Key Drivers in Defense Fighter Aircraft Boarding Ladders

Several forces propel the Defense Fighter Aircraft Boarding Ladders market forward. Fleet modernization stands paramount, as air forces upgrade aging fighters to advanced platforms requiring precise, compatible access solutions. This shift demands ladders that interface seamlessly with stealth designs, low-observable coatings, and elevated fuselages, spurring innovation in adjustable heights and stealth-compatible materials.

Operational tempo escalates drivers, with doctrines emphasizing rapid deployment and high sortie rates in peer-adversary scenarios. Ladders must support quick boarding in forward operating bases, prompting designs focused on portability, one-hand deployment, and resistance to sand, salt, or arctic conditions. Logistics optimization fuels demand, as lighter ladders cut transport costs and integrate with air-mobile sustainment chains.

Geopolitical realignments intensify procurement, particularly in regions bolstering airpower deterrence. Export-oriented production benefits from allied interoperability standards, encouraging standardized ladder interfaces. Sustainability mandates push for recyclable composites and low-maintenance finishes, aligning with green procurement policies. Supply chain resilience, post-disruptions, drives localized manufacturing and dual-sourcing strategies.

Human factors, including pilot safety and reduced injury risks, underscore ergonomic designs with anti-fatigue steps and integrated lighting. Regulatory compliance for crashworthiness and fire resistance further shapes offerings. Collectively, these drivers position boarding ladders as enablers of air dominance, intertwining with broader aerospace sustainment ecosystems.

Regional Trends in Defense Fighter Aircraft Boarding Ladders

Regional dynamics reveal distinct trends in the Defense Fighter Aircraft Boarding Ladders market. In Asia-Pacific, rapid air force expansion dominates, with emphasis on indigenous production to support growing fleets of multirole fighters. Nations prioritize rugged ladders for tropical climates and island-hopping operations, fostering local suppliers integrated into offset agreements.

North America leads in technological sophistication, where mature ecosystems drive smart, sensor-equipped ladders compatible with fifth-generation aircraft. Focus shifts to expeditionary capabilities, with designs optimized for carrier decks and austere strips amid great-power competition.

Europe emphasizes standardization through collaborative programs, yielding modular ladders interoperable across NATO fleets. Harsh weather adaptations, like de-icing mechanisms, gain traction, alongside sustainability-focused materials from regional composites hubs.

Middle East trends center on high-mobility solutions for desert environments, with demand for heat-resistant, dust-proof ladders tied to fighter acquisitions from global primes. Latin America sees steady sustainment-driven procurement, upgrading legacy platforms with cost-effective, lightweight designs.

Africa's market evolves around peacekeeping and counter-insurgency needs, favoring portable, low-maintenance ladders for bush airstrips. Cross-regional supply chains converge on advanced materials, while export controls shape technology transfers. These patterns highlight tailored innovations meeting diverse threat landscapes.

Key Defense Fighter Aircraft Boarding Ladders Programs

Prominent programs highlight the strategic importance of Defense Fighter Aircraft Boarding Ladders. Next-generation fighter sustainment initiatives integrate advanced ladders with stealth platforms, featuring automated deployment and biometric locks for secure access. Collaborative developments yield universal kits adaptable to multiple airframes, streamlining logistics for multinational exercises.

Navalized variants emerge in carrier strike group enhancements, with corrosion-proof, stowable ladders designed for deck operations amid rough seas. Expeditionary air wing programs prioritize air-transportable models that erect in seconds, supporting distributed lethality concepts.

Upgrade packages for legacy fleets retrofit smart ladders with vibration-dampening and load sensors, extending service life while boosting safety. Indigenous programs in emerging powers develop cost-optimized designs using local alloys, aligned with self-reliance goals.

Simulation-integrated testing validates ladders under extreme scenarios, from electromagnetic pulses to blast overpressures. Joint ventures between OEMs and specialists produce hybrid electro-mechanical systems, reducing manpower needs. Export-oriented programs bundle ladders with aircraft deals, ensuring compatibility and training packages.

These efforts underscore ladders' role in mission readiness, intertwining with digital twins for virtual prototyping and fleet management. Ongoing prototypes explore drone-compatible mini-ladders, foreshadowing unmanned trends.

Table of Contents

Defense Fighter Aircraft Boarding Ladders Market - Table of Contents

Defense Fighter Aircraft Boarding Ladders Market Report Definition

Defense Fighter Aircraft Boarding Ladders Market Segmentation

By Integration Type

By Deployment Mechanism

By Material

By Aircraft Type

By Stowage Location

Defense Fighter Aircraft Boarding Ladders Market Analysis for next 10 Years

The 10-year Defense Fighter Aircraft Boarding Ladders Market analysis would give a detailed overview of Defense Fighter Aircraft Boarding Ladders Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Fighter Aircraft Boarding Ladders Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Fighter Aircraft Boarding Ladders Market Forecast

The 10-year Defense Fighter Aircraft Boarding Ladders Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Fighter Aircraft Boarding Ladders Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Fighter Aircraft Boarding Ladders Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Fighter Aircraft Boarding Ladders Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Fighter Aircraft Boarding Ladders Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Integration , 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Integration , 2026-2036

List of Figures

- Figure 1: Global Fighter Aircraft Boarding Ladders Market Forecast, 2026-2036

- Figure 2: Global Fighter Aircraft Boarding Ladders Market Forecast, By Region, 2026-2036

- Figure 3: Global Fighter Aircraft Boarding Ladders Market Forecast, By Platform, 2026-2036

- Figure 4: Global Fighter Aircraft Boarding Ladders Market Forecast, By Integration , 2026-2036

- Figure 5: North America, Fighter Aircraft Boarding Ladders Market, Forecast, 2026-2036

- Figure 6: Europe, Fighter Aircraft Boarding Ladders Market, Forecast, 2026-2036

- Figure 7: Middle East, Fighter Aircraft Boarding Ladders Market, Forecast, 2026-2036

- Figure 8: APAC, Fighter Aircraft Boarding Ladders Market, Forecast, 2026-2036

- Figure 9: South America, Fighter Aircraft Boarding Ladders Market, Forecast, 2026-2036

- Figure 10: United States, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 11: United States, Fighter Aircraft Boarding Ladders Market, Forecast, 2026-2036

- Figure 12: Canada, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Fighter Aircraft Boarding Ladders Market, Forecast, 2026-2036

- Figure 14: Italy, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 16: France, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 17: France, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 18: Germany, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 24: Spain, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 30: Australia, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 32: India, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 33: India, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 34: China, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 35: China, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 40: Japan, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Fighter Aircraft Boarding Ladders Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Fighter Aircraft Boarding Ladders Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Fighter Aircraft Boarding Ladders Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Fighter Aircraft Boarding Ladders Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Fighter Aircraft Boarding Ladders Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Fighter Aircraft Boarding Ladders Market, By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Fighter Aircraft Boarding Ladders Market, By Integration (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Fighter Aircraft Boarding Ladders Market, By Integration (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Fighter Aircraft Boarding Ladders Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Fighter Aircraft Boarding Ladders Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Fighter Aircraft Boarding Ladders Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Fighter Aircraft Boarding Ladders Market, By Region, 2026-2036

- Figure 58: Scenario 1, Fighter Aircraft Boarding Ladders Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Fighter Aircraft Boarding Ladders Market, By Integration , 2026-2036

- Figure 60: Scenario 2, Fighter Aircraft Boarding Ladders Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Fighter Aircraft Boarding Ladders Market, By Region, 2026-2036

- Figure 62: Scenario 2, Fighter Aircraft Boarding Ladders Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Fighter Aircraft Boarding Ladders Market, By Integration , 2026-2036

- Figure 64: Company Benchmark, Fighter Aircraft Boarding Ladders Market, 2026-2036

全球戰鬥機市場(2026-2036)

全球戰鬥機市場(2026-2036) 戰鬥機市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、起降方式、飛機類型、地區和競爭格局分類,2020-2030年預測有無人機聯合(MUM-T)系統的全球市場(2025年~2035年)

戰鬥機市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、起降方式、飛機類型、地區和競爭格局分類,2020-2030年預測有無人機聯合(MUM-T)系統的全球市場(2025年~2035年) 戰鬥機市場按用途、代數、引擎數量、最終用戶和製造商分類——2025-2032年全球預測戰鬥機IRST的全球市場:2025年~2035年

戰鬥機市場按用途、代數、引擎數量、最終用戶和製造商分類——2025-2032年全球預測戰鬥機IRST的全球市場:2025年~2035年 戰鬥機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

戰鬥機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 戰鬥機市場分析及2034年預測:類型、產品、服務、技術、零件、應用、材料類型、最終用戶、能力

戰鬥機市場分析及2034年預測:類型、產品、服務、技術、零件、應用、材料類型、最終用戶、能力 2025年全球戰鬥機市場報告

2025年全球戰鬥機市場報告 2025-2029年全球戰鬥機市場

2025-2029年全球戰鬥機市場 戰鬥機的全球市場的評估,各類型,各用途,起飛和各降落類型,各地區,機會,預測(2018年~2032年)

戰鬥機的全球市場的評估,各類型,各用途,起飛和各降落類型,各地區,機會,預測(2018年~2032年)