|

市場調查報告書

商品編碼

1927655

全球國防3D列印市場(2026-2036)Global Cruise Missiles Market 2026-2036 |

||||||

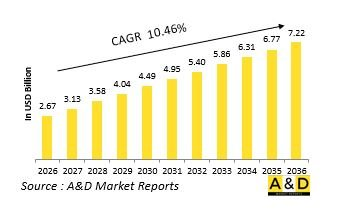

據估計,2026年全球國防3D列印市場規模為26.7億美元,預計到2036年將達到72.2億美元,2026年至2036年的複合年增長率(CAGR)為10.46%。

全球國防3D列印簡介

全球國防3D列印正在成為一種新興的製造方法,它正在改變軍事零件的設計、製造和維護方式。 與傳統生產方法不同,積層製造逐層建造零件,能夠實現使用傳統技術難以或不切實際的複雜幾何形狀。在國防領域,這項技術支援快速原型製作、客製化零件生產以及在作戰環境中按需製造。國防機構越來越重視將 3D 列印作為提高戰備水準和減少對冗長供應鏈依賴的戰略工具。該技術加速了設計迭代,實現了組件測試和改進,同時縮短了開發週期。它還支援輕量化結構的生產,從而在不犧牲強度的前提下提昇平台性能。在空中、陸地和海上領域,3D 列印技術透過實現備件和關鍵作戰組件的本地化生產,為資產維護做出了貢獻。其日益普及反映了向靈活、反應迅速的製造模式的轉變,這種轉變符合現代國防對速度、適應性和作戰韌性的要求。

科技對全球國防領域 3D 列印的影響

技術進步正在擴大 3D 列印在國防應用領域的範圍和可靠性。 金屬積層製造技術的進步使得高強度零件的生產成為可能,這些零件可用於結構和承重應用。列印精度的提高提升了尺寸精度和表面質量,滿足了嚴格的國防規範。材料科學的創新催生了專為嚴苛運作環境設計的特殊合金和複合材料。整合式數位設計工具實現了從建模到生產的無縫過渡,並支援快速修復。諸如製程監控等品質保證技術提高了一致性並降低了缺陷風險。安全的數位化工作流程保護了分散式製造中的敏感設計資料。這些發展使得3D列印從原型製作工具演變為支援作戰部署的生產技術。如今,它在提升性能、減少材料浪費以及快速響應國防平台不斷變化的作戰需求方面發揮著重要作用。

全球國防領域3D列印的關鍵驅動因素

國防領域採用3D列印技術的主要驅動因素是作戰彈性、供應鏈韌性和成本效益。軍事機構需要快速取得替換零件,以最大限度地減少設備停機時間。 現場或附近製造減少了對集中式供應商和長途物流路線的依賴。平台現代化專案促進了先進製造技術的應用,這些技術支援輕量化和最佳化設計。預算效率目標推動了減少模具需求和材料浪費的技術發展。小批量、複雜零件的生產能力與國防採購模式高度契合。勞動力技能發展和數位轉型措施進一步支持了積層製造技術融入國防生態系統。這些驅動因素體現了國防製造對敏捷性、永續性和應變能力的戰略關注。 本報告探索並分析了全球國防3D列印市場,提供了影響該市場的技術資訊、未來十年的預測以及區域趨勢。

目錄

國防3D列印市場報告定義

國防3D列印市場區隔

按應用

按地區

按元件

未來十年國防3D列印市場分析

國防3D列印市場技術

全球國防3D列印市場預測

區域國防3D列印市場趨勢及預測

北美

驅動因素、限制因素與挑戰

PEST分析

市場預測及情境分析

主要公司

供應商層級概覽

公司基準分析

歐洲

中東

亞太地區

南美洲

國防3D列印市場國家分析

美國

國防項目

最新資訊

專利

當前市場技術成熟度

市場預測及情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防3D列印市場機會矩陣

專家對國防3D列印市場的看法

結論

關於航空和國防市場報告

The global Cruise Missile market is estimated at USD 9.60 billion in 2026, projected to grow to USD 14.80 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.42% over the forecast period 2026-2036.

Introduction to the Global Cruise Missile Systems

The global cruise missile landscape represents a critical pillar of modern military capability, shaped by evolving doctrines of precision warfare and strategic deterrence. Cruise missiles are designed for sustained, guided flight at low altitudes, allowing them to evade detection while delivering highly accurate strikes against designated targets. Their role extends across strategic, tactical, and operational missions, including land attack, maritime strike, and suppression of enemy defenses. Unlike ballistic systems, cruise missiles offer flexibility in launch platforms, enabling deployment from air, sea, and ground assets. This adaptability has made them integral to both offensive and defensive postures of advanced armed forces. Global interest in cruise missiles is closely linked to shifting security environments, where nations seek credible stand-off capabilities without escalating to large-scale conflict. The market is influenced by indigenous development programs, collaborative defense initiatives, and export controls that shape accessibility and competition. As military planners increasingly emphasize precision, survivability, and controlled escalation, cruise missiles continue to gain prominence as tools that balance effectiveness with strategic restraint. Their growing relevance reflects broader transformations in warfare, where technological sophistication and mission versatility define combat readiness rather than sheer force concentration.

Technology Impact in Cruise Missile Systems

Technological advancement has fundamentally reshaped cruise missile capabilities, transforming them into highly intelligent and adaptive weapon systems. Progress in guidance and navigation has enabled missiles to follow complex flight paths while maintaining exceptional accuracy, even in contested environments. Advances in propulsion have improved endurance and range efficiency, supporting prolonged low-altitude flight with reduced signatures. Materials engineering has contributed to lighter structures and enhanced stealth characteristics, allowing missiles to penetrate sophisticated air defense networks. The integration of artificial intelligence and advanced software has enhanced target recognition, mission reprogramming, and resistance to electronic interference. Sensor fusion now allows real-time data processing from multiple inputs, improving situational awareness throughout the flight profile. Network-centric warfare concepts further amplify impact by enabling cruise missiles to operate as part of coordinated strike packages rather than isolated assets. These technological shifts reduce dependence on manned platforms and minimize operational risk. Overall, technology has elevated cruise missiles from simple delivery systems to complex, autonomous instruments of precision warfare, reinforcing their strategic value in contemporary and future military operations.

Key Drivers in the Cruise Missile Systems

The cruise missile domain is driven by a combination of strategic necessity, evolving threat perceptions, and doctrinal shifts in modern warfare. Nations increasingly prioritize stand-off strike capabilities to neutralize high-value targets while safeguarding personnel and platforms. The need for precision engagement in densely populated or politically sensitive environments has further reinforced demand for accurate, low-collateral weapon systems. Deterrence considerations also play a significant role, as cruise missiles provide credible response options without immediate escalation to broader conflict. The modernization of armed forces, particularly air and naval units, supports integration of advanced missile systems as force multipliers. Additionally, the rise of integrated air defense networks compels investment in weapons capable of penetration and survivability. Industrial policy and defense self-reliance initiatives encourage domestic development to reduce external dependence and secure supply chains. Export potential and strategic partnerships further stimulate innovation and production. Together, these drivers reflect a global shift toward precision, flexibility, and strategic control, positioning cruise missiles as indispensable assets in contemporary defense planning.

Regional Trends in the Cruise Missile Systems

Regional trends in the cruise missile environment are shaped by distinct security priorities, geopolitical dynamics, and industrial capabilities. In technologically advanced regions, emphasis is placed on stealth enhancement, multi-mission adaptability, and seamless integration with existing command structures. Areas facing maritime security challenges prioritize sea-based and anti-ship variants to protect trade routes and territorial waters. Regions experiencing persistent border tensions focus on land-attack capabilities that provide rapid response and deterrence without extensive force deployment. Emerging defense markets increasingly pursue indigenous development programs, viewing cruise missile capability as a symbol of strategic maturity and autonomy. Collaborative development and licensed production are common where resource optimization and technology access are key considerations. Export regulations and alliance frameworks significantly influence regional availability and design choices. Overall, regional patterns reflect localized threat assessments rather than uniform global demand, resulting in diverse design philosophies and deployment strategies. This diversity underscores the adaptability of cruise missile systems to varied operational doctrines and regional security architectures.

Key Cruise Missile Program:

The upgrade and modernisation of the BrahMos cruise missile system is an ongoing effort, focused on eventually transitioning toward hypersonic technologies. Featuring advanced guidance and control systems, BrahMos is a supersonic cruise missile capable of being launched from submarines, surface vessels, aircraft, and land-based platforms.

Table of Contents

Cruise Missiles Market - Table of Contents

Cruise Missiles Market Report Definition

Cruise Missiles Market Segmentation

By Region

By Launch Platform

By Range

Cruise Missiles Market Analysis for next 10 Years

The 10-year cruise missiles market analysis would give a detailed overview of cruise missiles market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Cruise Missiles Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Cruise Missiles Market Forecast

The 10-year cruise missiles market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Cruise Missiles Market Trends & Forecast

The regional cruise missiles market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Cruise Missiles Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Cruise Missiles Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Cruise Missiles Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Launch Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Range, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Launch Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Range, 2026-2036

List of Figures

- Figure 1: Global Cruise Missiles Market Forecast, 2026-2036

- Figure 2: Global Cruise Missiles Market Forecast, By Region, 2026-2036

- Figure 3: Global Cruise Missiles Market Forecast, By Launch Platform, 2026-2036

- Figure 4: Global Cruise Missiles Market Forecast, By Range, 2026-2036

- Figure 5: North America, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 6: Europe, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 8: APAC, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 9: South America, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 10: United States, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 11: United States, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 12: Canada, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 14: Italy, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 16: France, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 17: France, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 18: Germany, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 24: Spain, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 30: Australia, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 32: India, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 33: India, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 34: China, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 35: China, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 40: Japan, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Cruise Missiles Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Cruise Missiles Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Cruise Missiles Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Cruise Missiles Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Cruise Missiles Market, By Launch Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Cruise Missiles Market, By Launch Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Cruise Missiles Market, By Range (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Cruise Missiles Market, By Range (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Cruise Missiles Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Cruise Missiles Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Cruise Missiles Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Cruise Missiles Market, By Region, 2026-2036

- Figure 58: Scenario 1, Cruise Missiles Market, By Launch Platform, 2026-2036

- Figure 59: Scenario 1, Cruise Missiles Market, By Range, 2026-2036

- Figure 60: Scenario 2, Cruise Missiles Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Cruise Missiles Market, By Region, 2026-2036

- Figure 62: Scenario 2, Cruise Missiles Market, By Launch Platform, 2026-2036

- Figure 63: Scenario 2, Cruise Missiles Market, By Range, 2026-2036

- Figure 64: Company Benchmark, Cruise Missiles Market, 2026-2036

2026年全球導引武器系統市場報告

2026年全球導引武器系統市場報告 巡航飛彈市場-全球產業規模、佔有率、趨勢、機會和預測:按發射平台、射程、速度、地區和競爭格局分類,2021-2031年

巡航飛彈市場-全球產業規模、佔有率、趨勢、機會和預測:按發射平台、射程、速度、地區和競爭格局分類,2021-2031年 巡航飛彈市場規模、佔有率和成長分析(按飛彈類型、零件、飛彈速度、發射平台、飛彈射程、導引技術和地區分類)-2026-2033年產業預測

巡航飛彈市場規模、佔有率和成長分析(按飛彈類型、零件、飛彈速度、發射平台、飛彈射程、導引技術和地區分類)-2026-2033年產業預測 固體火箭發動機市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2024-2032 年)

固體火箭發動機市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2024-2032 年) 固體火箭引擎市場(按組件、發射平台、推力等級、應用和最終用戶分類)—2025-2030 年全球預測2025年全球固體火箭引擎市場報告

固體火箭引擎市場(按組件、發射平台、推力等級、應用和最終用戶分類)—2025-2030 年全球預測2025年全球固體火箭引擎市場報告 固體火箭引擎市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

固體火箭引擎市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 固體火箭馬達市場:市場規模、趨勢分析 - 按平台、按最終用戶、按組件 - 區域展望、競爭策略、按細分市場預測(至 2034 年)

固體火箭馬達市場:市場規模、趨勢分析 - 按平台、按最終用戶、按組件 - 區域展望、競爭策略、按細分市場預測(至 2034 年)