|

市場調查報告書

商品編碼

1904998

全球國防陀螺儀市場(2026-2036)Global Defense Gyroscope Market 2026-2036 |

||||||

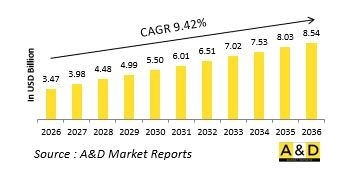

據估計,2026年全球國防陀螺儀市場規模為34.7億美元,預計到2036年將達到85.4億美元,2026年至2036年的複合年增長率(CAGR)為9.42%。

國防陀螺儀市場簡介

全球國防陀螺儀市場涵蓋用於測量和保持方位角和角速率的感測器,為軍事系統的導航、穩定和控制提供關鍵指標。這些設備基於多種物理原理運行,包括旋轉質量、光學干涉和量子效應等,無需外部參考即可檢測旋轉。陀螺儀是慣性測量單元、導引系統、平台穩定器和目標捕獲系統的關鍵組件。其應用範圍廣泛,從潛艇數週導航所需的極高精度,到需要快速響應和高過載耐受性的飛彈導引,再到士兵在無GPS環境下使用的手持導航系統。隨著軍事行動越來越多地在衛星導航覆蓋不到的地區進行,精確指向對於感測器和武器的有效部署至關重要,陀螺儀的性能直接影響戰略、作戰和戰術層面的作戰成敗。

國防陀螺儀市場的技術影響

國防陀螺儀的技術進步涵蓋多個性能類別和物理原理。 MEMS陀螺儀透過實現小型、低成本和堅固耐用的感測器的批量生產,徹底改變了戰術應用,但精度仍然有限。光纖陀螺儀 (FOG) 沒有移動部件,在相對緊湊的封裝中提供卓越的導航級應用效能。環形雷射陀螺儀 (RLG) 不斷發展,以滿足需要長時間高精度的戰略應用需求。新技術包括利用原子自旋特性的核磁共振陀螺儀和可實現量子級精度的冷原子乾涉儀。系統單晶片整合 (SoC) 正在實現完整的慣性解決方案,將陀螺儀、加速度計和處理電子裝置整合在一起。先進的校準演算法和多感測器融合技術可以補償單一感測器的誤差,從而實現超越標稱規格的性能。這些進步正在拓展應用範圍,並在尺寸、重量和功耗的限制下不斷突破精度極限。

國防陀螺儀市場的主要驅動因素

電子戰技術的擴散不斷幹擾和破壞 GPS,從而催生了對替代導航解決方案的根本性需求,而陀螺儀是慣性導航系統的核心。精確導引武器的擴展需要經濟高效、可大規模生產且能保持足夠精度以進行目標捕獲的陀螺儀。全局自主系統的開發依賴於可靠的姿態和航向參考,以便在位置更新之間進行車輛控制。移動車輛上武器、感測器和通訊設備的平台穩定推動了對高頻寬角速率測量的需求。高超音速武器的開發需要能夠承受極端振動和熱環境並保持精確度的陀螺儀技術。此外,戰略威懾力量的現代化需要不斷提高潛艦和飛彈的導航精度,從而維持對高性能陀螺儀的需求,無論成本如何。這些多樣化的需求需要對所有陀螺儀技術類別和性能等級進行持續投資。

國防陀螺儀市場的區域趨勢

區域陀螺儀生產能力通常與國內武器計畫和戰略自主目標相關。北美在所有陀螺儀技術類別中都擁有全面的生產能力,其產業基礎涵蓋從微機電系統(MEMS)量產到戰略級光纖陀螺儀/旋轉陀螺儀(FOG/RLG)系統。歐洲的研發重點是高性能航空航太應用,通常由多國合作推動,以分擔研發成本。亞太地區發展迅速,中國、日本和韓國正在建構涵蓋各個技術水準的完整本土陀螺儀生態系統。以色列在用於精確導引武器和無人機的戰術級系統方面積累了豐富的經驗。俄羅斯在維持其傳統機械陀螺儀生產能力的同時,也正在開發現代固態陀螺儀。高性能慣性技術的出口限制構成了一定的障礙,促使那些尋求戰略武器自主研發的地區進行本土化發展。然而,商用MEMS的普及正在降低全球高性能戰術系統的進入門檻。 本報告分析了全球國防陀螺儀市場,深入探討了影響該市場的技術、未來十年的預測以及區域趨勢。

目錄

國防陀螺儀市場報告定義

國防陀螺儀市場區隔

按類型

按地區

按平台

未來十年國防陀螺儀市場分析

國防陀螺儀市場技術

全球國防陀螺儀市場預測

區域國防陀螺儀市場趨勢及預測

北美

驅動因素、限制因素與挑戰

PEST分析

市場預測及情境分析

主要公司

供應商等級

公司基準分析

歐洲

中東

亞太地區

南美洲

國防陀螺儀市場國家分析

美國

國防項目

最新資訊

專利

當前市場技術成熟度

市場預測及情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防陀螺儀市場機會矩陣

國防陀螺儀市場專家意見報告

結論

關於航空和國防市場報告

The Global Defense Gyroscope market is estimated at USD 3.47 billion in 2026, projected to grow to USD 8.54 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 9.42% over the forecast period 2026-2036.

Introduction to Defense Gyroscope Market

The Global Defense Gyroscope Market encompasses sensors that measure or maintain orientation and angular velocity, providing critical references for navigation, stabilization, and control across military systems. These devices operate on various physical principles-from spinning masses and optical interference to quantum effects-to detect rotation independently of external references. Gyroscopes form essential components within inertial measurement units, guidance systems, platform stabilizers, and targeting apparatus. Applications range from submarine navigation requiring extreme accuracy over weeks of submerged operation to missile guidance demanding rapid response and high g-tolerance, to soldier-worn systems providing dismounted navigation in GPS-denied environments. As military operations increasingly occur where satellite navigation is compromised and precise pointing is essential for sensor and weapon effectiveness, gyroscope performance directly influences mission success across strategic, operational, and tactical levels of warfare.

Technology Impact in Defense Gyroscope Market:

Technological evolution in defense gyroscopes spans multiple performance categories and physical principles. Micro-electromechanical systems (MEMS) gyroscopes have revolutionized tactical applications through mass production of small, affordable, rugged sensors, though with accuracy limitations. Fiber-optic gyroscopes (FOGs) offer excellent performance for navigation-grade applications with no moving parts and relatively compact packaging. Ring laser gyroscopes (RLGs) continue advancing for strategic applications requiring the highest accuracy over extended durations. Emerging technologies include nuclear magnetic resonance gyroscopes exploiting atomic spin properties and cold-atom interferometers offering quantum-level precision. System-on-chip integration combines gyroscopes with accelerometers and processing electronics for complete inertial solutions. Advanced calibration algorithms and multi-sensor fusion compensate for individual sensor errors, enabling performance beyond nominal specifications. These advancements expand applications while pushing accuracy boundaries across size, weight, and power constraints.

Key Drivers in Defense Gyroscope Market:

Electronic warfare proliferation that degrades or denies GPS availability creates fundamental demand for alternative navigation solutions, with gyroscopes serving as the core of inertial navigation systems. Precision-guided munitions expansion requires mass-producible, cost-effective gyroscopes that maintain sufficient accuracy for target engagement. Autonomous system development across all domains depends on reliable attitude and heading references for vehicle control between position updates. Platform stabilization for weapons, sensors, and communications equipment on moving vehicles drives demand for high-bandwidth angular rate measurement. Hypersonic weapon development pushes gyroscope technology to withstand extreme vibration and thermal environments while maintaining precision. Additionally, strategic deterrent modernization necessitates continuous improvement in submarine and missile navigation accuracy, sustaining demand for the highest performance gyroscopes regardless of cost considerations. These diverse requirements ensure sustained investment across all gyroscope technology categories and performance levels.

Regional Trends in Defense Gyroscope Market:

Regional gyroscope capabilities often correlate with indigenous weapons programs and strategic autonomy objectives. North America maintains comprehensive capabilities across all gyroscope technology categories, with industrial capacity spanning from MEMS mass production to strategic-grade FOG and RLG systems. European development emphasizes high-performance aerospace applications, frequently through multinational collaborations that share development costs. The Asia-Pacific region shows rapid advancement, with China, Japan, and South Korea developing complete indigenous gyroscope ecosystems across technology levels. Israel has cultivated specialized expertise in tactical-grade systems for precision munitions and unmanned applications. Russia maintains capabilities in traditional mechanical gyroscopes while developing modern solid-state alternatives. Export controls on high-performance inertial technology create barriers that encourage local development in regions seeking strategic weapons autonomy, though commercial MEMS availability has lowered barriers to entry for capable tactical systems worldwide.

Key Defense Gyroscope Program:

SMPP Group's November 2025 teaming agreement with Germany's KNDS France for KATANA 155mm precision-guided artillery ammunition integrates MEMS-based defense gyroscopes with GNSS-IMU for sub-10m CEP accuracy. The ₹500 crore initial order for 50,000 rounds targets Indian Army's Shakti program, with tech transfer for Pune manufacturing. Gyroscopes stabilize rounds in Mach 2+ flights, countering EW jamming. Trials at Pokhran exceeded specs, enabling 40km+ ranges. This replaces ageing Russian Smelchak stocks, with full indigenization by 2028. KNDS provides gyro IP, boosting SMPP's sensor portfolio amid 2025 DAC push for smart munitions.

Table of Contents

Defense Gyroscope Market Report Definition

Defense Gyroscope Market Segmentation

By Type

By Region

By Platform

Defense Gyroscope Market Analysis for next 10 Years

The 10-year Defense Gyroscope Market analysis would give a detailed overview of Defense Gyroscope Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Gyroscope Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Gyroscope Market Forecast

The 10-year Defense Gyroscope Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Gyroscope Market Trends & Forecast

The regional Defense Gyroscope Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Gyroscope Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Gyroscope Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Gyroscope Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Platform, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Platform, 2025-2035

List of Figures

- Figure 1: Global Defense Gyroscope Market Forecast, 2025-2035

- Figure 2: Global Defense Gyroscope Market Forecast, By Region, 2025-2035

- Figure 3: Global Defense Gyroscope Market Forecast, By Type, 2025-2035

- Figure 4: Global Defense Gyroscope Market Forecast, By Platform, 2025-2035

- Figure 5: North America, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 6: Europe, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 8: APAC, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 9: South America, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 10: United States, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 11: United States, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 12: Canada, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 14: Italy, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 16: France, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 17: France, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 18: Germany, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 20: Netherland, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 21: Netherland, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 24: Spain, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 30: Australia, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 32: India, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 33: India, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 34: China, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 35: China, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 40: Japan, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Defense Gyroscope Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Defense Gyroscope Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Defense Gyroscope Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Defense Gyroscope Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Defense Gyroscope Market, By Type (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Defense Gyroscope Market, By Type (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Defense Gyroscope Market, By Platform (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Defense Gyroscope Market, By Platform (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Defense Gyroscope Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Defense Gyroscope Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Defense Gyroscope Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Defense Gyroscope Market, By Region, 2025-2035

- Figure 58: Scenario 1, Defense Gyroscope Market, By Type, 2025-2035

- Figure 59: Scenario 1, Defense Gyroscope Market, By Platform, 2025-2035

- Figure 60: Scenario 2, Defense Gyroscope Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Defense Gyroscope Market, By Region, 2025-2035

- Figure 62: Scenario 2, Defense Gyroscope Market, By Type, 2025-2035

- Figure 63: Scenario 2, Defense Gyroscope Market, By Platform, 2025-2035

- Figure 64: Company Benchmark, Defense Gyroscope Market, 2025-2035

雙軸陀螺穩定平台市場(按平台類型、技術、安裝類型、應用和最終用戶分類),全球預測,2026-2032年

雙軸陀螺穩定平台市場(按平台類型、技術、安裝類型、應用和最終用戶分類),全球預測,2026-2032年 全球國防陀螺羅盤市場:2026-2036藍寶石球面和半球面透鏡市場:按透鏡類型、材料、應用、最終用戶和銷售管道,全球預測,2026-2032年

全球國防陀螺羅盤市場:2026-2036藍寶石球面和半球面透鏡市場:按透鏡類型、材料、應用、最終用戶和銷售管道,全球預測,2026-2032年 陀螺儀市場規模、佔有率和成長分析(按技術類型、產品類型、最終用戶和地區分類)-2026-2033年產業預測

陀螺儀市場規模、佔有率和成長分析(按技術類型、產品類型、最終用戶和地區分類)-2026-2033年產業預測 環形雷射陀螺儀 (RLG) 市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測 (2024-2032)陀螺儀市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,以及2024-2032年預測

環形雷射陀螺儀 (RLG) 市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測 (2024-2032)陀螺儀市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,以及2024-2032年預測 雙軸陀螺穩定平台:全球市佔率及排名、總收入及需求預測(2025-2031年)

雙軸陀螺穩定平台:全球市佔率及排名、總收入及需求預測(2025-2031年) 陀螺儀市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測陀螺儀市場按類型、軸、輸出訊號、應用、分銷管道和銷售管道分類—2025-2030 年全球預測

陀螺儀市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測陀螺儀市場按類型、軸、輸出訊號、應用、分銷管道和銷售管道分類—2025-2030 年全球預測 全球陀螺儀感測器市場

全球陀螺儀感測器市場