|

市場調查報告書

商品編碼

1833447

陀螺儀市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Gyroscope Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

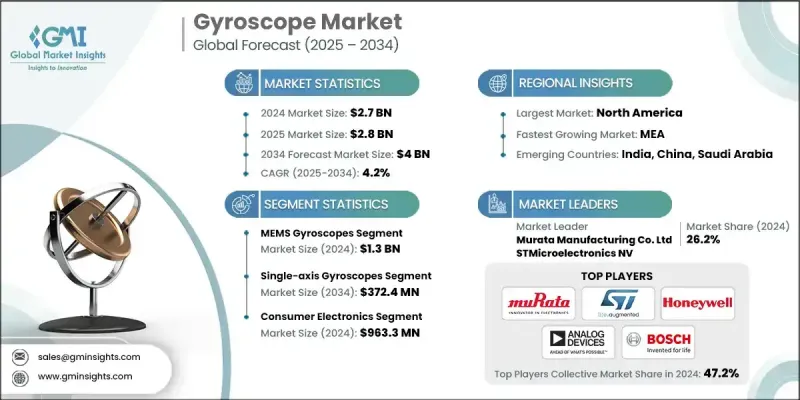

2024 年全球陀螺儀市場價值為 27 億美元,預計將以 4.2% 的複合年成長率成長,到 2034 年達到 40 億美元。

智慧型手機、平板電腦和穿戴式裝置已變得高度複雜,使用者體驗高度依賴運動感應功能。陀螺儀對於實現自動螢幕方向、步數追蹤、手勢控制和沈浸式擴增實境 (AR) 應用等功能至關重要。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 27億美元 |

| 預測值 | 40億美元 |

| 複合年成長率 | 4.2% |

MEMS陀螺儀的採用率不斷上升

MEMS陀螺儀憑藉其緊湊的尺寸、低功耗以及大眾市場應用的適用性,在2024年佔據了相當大的市場佔有率。這些微機電系統廣泛應用於行動裝置、穿戴式裝置、無人機和遊戲控制器,使其成為全球成長最快的細分市場之一。各大公司正在大力投資微型化、大量生產流程和多軸感測器融合,以提高性能和成本效益。

單軸陀螺儀的使用率不斷上升

單軸陀螺儀市場在2024年維持強勁成長。這類陀螺儀因其簡單易用、經久耐用且成本低廉而備受青睞,其價格通常在5美元到100美元之間,具體取決於規格。儘管多軸解決方案的需求日益成長,但在只需極少量感測的場景下,單軸陀螺儀仍然是首選。為了維持市場競爭力,各公司正致力於提升單軸陀螺儀的靈敏度和穩定性,並將其整合到模組化感測器套件中,以吸引新興市場和DIY技術平台。

消費性電子產品將獲得青睞

2024年,消費性電子領域將佔據相當大的佔有率,這主要得益於其在智慧型手機、AR/VR頭戴裝置、健身追蹤器和遊戲設備等領域的應用。隨著使用者體驗越來越沉浸式,並更加重視運動驅動,對緊湊、快速響應和低功耗陀螺儀的需求持續成長。為了保持競爭力,製造商優先考慮外形尺寸最佳化、大批量生產能力以及與OEM產品週期的緊密配合。

北美將成為推動力地區

受國防、航太和先進製造業強勁投資的推動,北美陀螺儀市場預計在2024年佔據顯著佔有率。該地區還擁有許多全球頂尖的科技和感測器公司,為創新與合作提供了肥沃的土壤。

陀螺儀市場的主要參與者有 Trimble Inc.、InvenSense Inc.、TE Connectivity Ltd.、EMCORE Corporation、Murata Manufacturing Co. Ltd、Systron Donner Inertial、Bosch Sensortec GmbH、InnaLabs、STMicroelectronics NV、Alog坦 Devices Inc.、Northnalogy. Inc. 和 NXP Semiconductors NV。

為了鞏固在全球陀螺儀市場的立足點,各公司正專注於創新、垂直整合和終端市場多元化。研發投入仍然是核心,尤其是在MEMS微型化、感測器融合和下一代材料方面。與航太、汽車和消費電子公司建立策略合作夥伴關係有助於確保長期業務,並推動特定應用陀螺儀的共同開發。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 消費性電子產品需求不斷成長

- 自動駕駛汽車和ADAS的普及

- 航太和國防應用領域的擴展

- 工業自動化和機器人技術的擴展

- 微機電系統 (MEMS) 技術的進步

- 產業陷阱與挑戰

- 製造成本上升

- 系統無縫整合困難

- 市場機會

- 增強物聯網連接性和用例

- 自動駕駛汽車的進步

- 連網穿戴技術設備

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 永續性措施

- 消費者情緒分析

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按技術類型,2021 - 2034 年

- 主要趨勢

- MEMS陀螺儀

- 光纖陀螺儀(FOG)

- 環形雷射陀螺儀(RLG)

- 動態調諧陀螺儀(DTG)

- 半球諧振陀螺儀(HRG)

- 其他

第6章:市場估計與預測:按軸配置,2021 - 2034 年

- 主要趨勢

- 單軸陀螺儀

- 雙軸陀螺儀

- 三軸陀螺儀

- 多軸陀螺儀

第7章:市場估計與預測:按應用,2021 - 2034

- 主要趨勢

- 運動感應和手勢控制

- 導航與慣性測量

- 穩定與控制系統

- 其他

第 8 章:市場估計與預測:按最終用途產業,2021 年至 2034 年

- 主要趨勢

- 消費性電子產品

- 智慧型手機和平板電腦

- 穿戴式裝置

- 擴增實境/虛擬實境

- 攝影機穩定系統

- 其他

- 汽車和運輸

- 搭乘用車

- 商用車

- 軌道運輸和地鐵系統

- 其他

- 航太和國防

- 飛機

- 無人機

- 太空船

- 船舶和潛水艇

- 其他

- 工業和機器人

- 工業機器人

- 工業機械及設備

- 其他

- 醫療保健和醫療器械

- 手術導航系統

- 醫學影像設備

- 其他

- 其他

第9章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多邊環境協定

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球關鍵參與者

- Honeywell International Inc.

- Northrop Grumman Corporation

- STMicroelectronics NV

- Analog Devices Inc.

- NXP Semiconductors NV

- 區域關鍵參與者

- 北美洲

- InvenSense Inc.

- TE Connectivity Ltd.

- Trimble Inc.

- EMCORE Corporation

- SiTime Corporation

- PNI Sensor Technology

- 歐洲

- Murata Manufacturing Co. Ltd

- Bosch Sensortec GmbH

- Safran Electronics & Defense

- 亞太地區

- Epson America Inc.

- InnaLabs

- 北美洲

- 利基市場參與者/顛覆者

- Silicon Sensing Systems Ltd.

- Systron Donner Inertial

- KVH Industries

The Global Gyroscope Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 4 billion by 2034.

Smartphones, tablets, and wearable devices have become highly sophisticated, with user experiences that depend heavily on motion-sensing capabilities. Gyroscopes are central to enabling features such as automatic screen orientation, step tracking, gesture control, and immersive augmented reality (AR) applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $4 billion |

| CAGR | 4.2% |

Rising Adoption of MEMS Gyroscopes

The MEMS gyroscopes segment held a sizeable share in 2024, owing to their compact size, low power consumption, and suitability for mass-market applications. These micro-electromechanical systems are widely used in mobile devices, wearables, drones, and game controllers, making them one of the fastest-growing segments globally. Companies are investing heavily in miniaturization, batch manufacturing processes, and multi-axis sensor fusion to improve performance and cost-efficiency.

Rising Usage of Single-Axis Gyroscopes

The single-axis gyroscopes segment held robust growth in 2024. These gyroscopes are valued for their simplicity, durability, and low-cost implementation, with pricing generally ranging from USD 5 to USD 100 depending on specifications. While the demand for multi-axis solutions is growing, single-axis units are still preferred in scenarios where minimal sensing is sufficient. To stay relevant, companies are focusing on enhancing the sensitivity and stability of single-axis models while integrating them into modular sensor kits to appeal to emerging markets and DIY technology platforms.

Consumer Electronics to Gain Traction

The consumer electronics segment held a sizeable share in 2024, driven by their use in smartphones, AR/VR headsets, fitness trackers, and gaming devices. As user experiences become more immersive and motion-driven, demand for compact, fast-responding, and low-power gyroscopes continues to rise. To stay competitive, manufacturers are prioritizing form factor optimization, high-volume production capabilities, and close alignment with OEM product cycles.

North America to Emerge as a Propelling Region

North America gyroscopes market is poised to witness a significant share in 2024, fueled by robust investments in defense, aerospace, and advanced manufacturing. The region also hosts many of the world's top tech and sensor companies, offering a fertile ground for innovation and collaboration.

Major players in the gyroscopes market are Trimble Inc., InvenSense Inc., TE Connectivity Ltd., EMCORE Corporation, Murata Manufacturing Co. Ltd, Systron Donner Inertial, Bosch Sensortec GmbH, InnaLabs, STMicroelectronics NV, Analog Devices Inc., Northrop Grumman Corporation, Silicon Sensing Systems Ltd., Epson America Inc., Honeywell International Inc., and NXP Semiconductors NV.

To strengthen their foothold in the global gyroscopes market, companies are focusing on a mix of innovation, vertical integration, and end-market diversification. R&D investment remains central, especially in MEMS miniaturization, sensor fusion, and next-generation materials. Strategic partnerships with aerospace, automotive, and consumer electronics firms help secure long-term business and drive co-development of application-specific gyros.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Technology type trends

- 2.2.2 Axis configuration trends

- 2.2.3 Application trends

- 2.2.4 End use industry trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand in consumer electronics

- 3.2.1.2 Proliferation of autonomous vehicles & ADAS

- 3.2.1.3 Expansion in aerospace & defense applications

- 3.2.1.4 Expansion of industrial automation and robotics

- 3.2.1.5 Advancements in micro-electro-mechanical systems (MEMS) technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising manufacturing costs

- 3.2.2.2 Difficulty in seamless system integration

- 3.2.3 Market opportunities

- 3.2.3.1 Increased IoT connectivity and use cases

- 3.2.3.2 Advances in autonomous vehicles

- 3.2.3.3 Connected wearable technology devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability Measures

- 3.13 Consumer sentiment analysis

- 3.14 Patent and IP analysis

- 3.15 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 MEMS gyroscopes

- 5.3 Fiber optic gyroscopes (FOG)

- 5.4 Ring laser gyroscopes (RLG)

- 5.5 Dynamically tuned gyroscopes (DTG)

- 5.6 Hemispherical resonator gyroscopes (HRG)

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Axis Configuration, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Single-axis gyroscopes

- 6.3 Dual-axis gyroscopes

- 6.4 Three-axis gyroscopes

- 6.5 Multi-axis gyroscopes

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Motion sensing & gesture control

- 7.3 Navigation & inertial measurement

- 7.4 Stabilization & control systems

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By End use Industry, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.2.1 Smartphones and tablets

- 8.2.2 Wearable devices

- 8.2.3 AR/VR

- 8.2.4 Camera stabilization systems

- 8.2.5 Others

- 8.3 Automotive and transportation

- 8.3.1 Passenger vehicles

- 8.3.2 Commercial vehicles

- 8.3.3 Rail transport and metro systems

- 8.3.4 Others

- 8.4 Aerospace and defense

- 8.4.1 Aircrafts

- 8.4.2 UAVs

- 8.4.3 Spacecrafts

- 8.4.4 Ships & submarines

- 8.4.5 Others

- 8.5 Industrial and robotics

- 8.5.1 Industrial robots

- 8.5.2 Industrial machines & equipments

- 8.5.3 Others

- 8.6 Healthcare and medical devices

- 8.6.1 Surgical navigation systems

- 8.6.2 Medical imaging equipment

- 8.6.3 Others

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Honeywell International Inc.

- 10.1.2 Northrop Grumman Corporation

- 10.1.3 STMicroelectronics NV

- 10.1.4 Analog Devices Inc.

- 10.1.5 NXP Semiconductors NV

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 InvenSense Inc.

- 10.2.1.2 TE Connectivity Ltd.

- 10.2.1.3 Trimble Inc.

- 10.2.1.4 EMCORE Corporation

- 10.2.1.5 SiTime Corporation

- 10.2.1.6 PNI Sensor Technology

- 10.2.2 Europe

- 10.2.2.1 Murata Manufacturing Co. Ltd

- 10.2.2.2 Bosch Sensortec GmbH

- 10.2.2.3 Safran Electronics & Defense

- 10.2.3 Asia Pacific

- 10.2.3.1 Epson America Inc.

- 10.2.3.2 InnaLabs

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Silicon Sensing Systems Ltd.

- 10.3.2 Systron Donner Inertial

- 10.3.3 KVH Industries

陀螺儀市場:按類型、軸數、輸出訊號、應用、通路和銷售管道分類-2026-2032年全球市場預測

陀螺儀市場:按類型、軸數、輸出訊號、應用、通路和銷售管道分類-2026-2032年全球市場預測 2026年全球環形雷射陀螺儀市場報告2026年全球陀螺儀市場報告雙軸陀螺穩定平台市場(按平台類型、技術、安裝類型、應用和最終用戶分類),全球預測,2026-2032年

2026年全球環形雷射陀螺儀市場報告2026年全球陀螺儀市場報告雙軸陀螺穩定平台市場(按平台類型、技術、安裝類型、應用和最終用戶分類),全球預測,2026-2032年 全球國防陀螺羅盤市場:2026-2036藍寶石球面和半球面透鏡市場:按透鏡類型、材料、應用、最終用戶和銷售管道,全球預測,2026-2032年

全球國防陀螺羅盤市場:2026-2036藍寶石球面和半球面透鏡市場:按透鏡類型、材料、應用、最終用戶和銷售管道,全球預測,2026-2032年 全球環形雷射陀螺儀市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球環形雷射陀螺儀市場規模、佔有率、趨勢和成長分析報告(2026-2034) 陀螺儀市場規模、佔有率和成長分析(按技術類型、產品類型、最終用戶和地區分類)-2026-2033年產業預測環形雷射陀螺儀 (RLG) 市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測 (2024-2032)陀螺儀市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,以及2024-2032年預測

陀螺儀市場規模、佔有率和成長分析(按技術類型、產品類型、最終用戶和地區分類)-2026-2033年產業預測環形雷射陀螺儀 (RLG) 市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測 (2024-2032)陀螺儀市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,以及2024-2032年預測