|

市場調查報告書

商品編碼

2029022

收入週期管理市場:按解決方案和服務類型、部署方式、系統類型、最終用戶和地區分類:產業趨勢和全球市場預測(至 2035 年)Revenue Cycle Management Market, Till 2035: Distribution by Type of Solution & Service, Type of Deployment, Type of System, Type of End User, and Geographical Regions: Industry Trends and Global Forecasts |

||||||

收入週期管理 (RCM) 市場展望

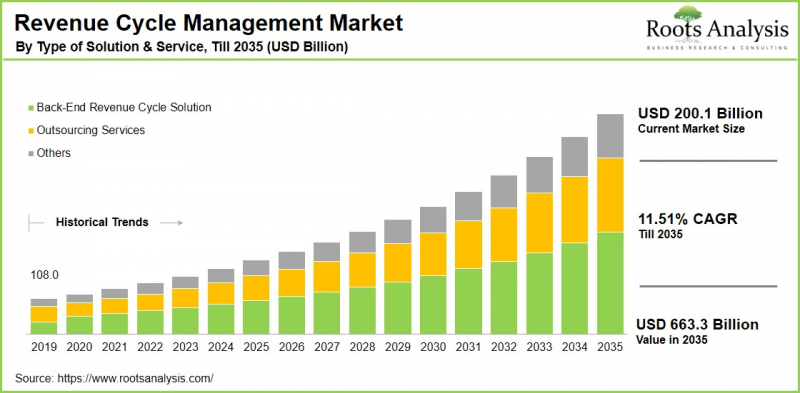

根據 Roots Analysis 的研究,全球收入週期管理 (RCM) 市場預計到 2035 年將以 11.51% 的複合年成長率成長,到 2035 年將達到 6,633 億美元,高於目前的 2,001 億美元。

收入週期管理 (RCM) 是一套醫療機構用於監督和最佳化與患者服務相關的財務活動的整合流程,涵蓋從首次預約安排、患者互動到最終收款的各個環節。這包括一系列旨在高效創造收入和收款的行政和臨床職能,例如病人參與、保險驗證、理賠處理和拒付管理。為了評估營運效率、識別挑戰並維持永續盈利,醫療產業對監測財務績效指標的需求日益成長,這正在加速採用先進的 RCM 解決方案。

此外,向基於價值的醫療保健和報銷模式的持續轉變,顯著提升了對複雜收入管理系統的需求。這種轉變增加了收入週期的複雜性,因為報銷與醫療品質和績效指標的關聯日益緊密。因此,需要更先進、更柔軟性的收入週期管理(RCM)架構。電子健康記錄(EHR)的日益普及也對市場成長起到了重要作用,從根本上改變了病患資料的取得、分析和管理方式。展望未來,隨著自動化和人工智慧技術的不斷進步,以及與病人參與平台的無縫整合,預計RCM市場將在整個預測期內保持強勁成長。

收入週期管理 (RCM) 市場成長的關鍵市場促進因素

推動收入週期管理 (RCM) 市場成長的關鍵因素有很多。其中最重要的是,電子健康記錄 (EHR) 系統的普及顯著提升了對整合式 RCM 解決方案的需求,這類解決方案能夠在統一的平台上管理臨床和財務數據。這促使醫療機構投資於先進的收入週期分析和計費服務。此外,從傳統的計量型模式轉向基於價值的醫療保健模式的轉變也進一步加速了市場擴張。這是因為醫療服務提供者的報酬越來越取決於患者的治療效果和醫療質量,而不是服務量。此外,不斷上漲的醫療成本、日益複雜的計費流程、政府的支援措施以及不斷變化的監管要求預計也將進一步推動 RCM 市場的成長。

收入週期管理 (RCM) 市場:競爭格局

在新興企業不斷湧入以及老牌全球企業的推動下,收入週期管理 (RCM) 市場的競爭格局正在迅速變化。 3M、Change Healthcare、Optum 和 McKesson 等主要企業正透過持續的技術創新、多元化的解決方案組合、強大的客戶服務能力以及策略聯盟和夥伴關係引領市場。這些公司優先推動人工智慧、機器學習、自動化和雲端平台等領域的技術進步,以提高其 RCM 服務的效率和效果。此外,它們還透過提供包括臨床文件服務、醫療編碼和合規工具、計費和支付管理系統在內的綜合解決方案來鞏固其市場地位,從而在競爭中脫穎而出。

高級醫療計費環境下的收入週期管理 (RCM)

收入週期管理 (RCM) 在現代醫療保健計費系統中發揮著至關重要的作用,它彌合了臨床服務提供與財務結果之間的差距,確保醫療服務提供者獲得準確及時的報酬。 RCM 涵蓋了從患者登記和保險驗證到編碼、發票提交、付款累計和收款的整個財務工作流程,從而實現了行政部門和臨床部門之間的無縫協作。

在當今複雜的醫療保健環境中,RCM(報告索賠管理)正發展成為一項策略職能,它能夠提高計費準確性、減少拒付、改善現金流並確保合規性。此外,將先進技術(例如自動化、分析和人工智慧)整合到RCM系統中,能夠進一步最佳化計費效率,並透過更透明的計費流程改善患者體驗。這為醫療機構的長期財務永續性奠定了基礎。

收入週期管理 (RCM) 市場的新趨勢

在快速的數位轉型和不斷變化的醫療保健需求的推動下,收入週期管理 (RCM) 市場正經歷一波新的趨勢。其中一個顯著的趨勢是人工智慧、自動化和先進分析技術的日益普及,這些技術提高了計費準確性,減少了拒付,並簡化了行政工作流程。此外,隨著向價值醫療模式的轉變,醫療服務提供者需要管理與患者治療結果相關的複雜報銷結構,這使得 RCM 成為一項策略性職能。

另一個關鍵趨勢是對整合式雲端收入周期管理 (RCM) 解決方案日益成長的需求。這些解決方案能夠實現即時數據存取、互通性以及臨床和財務系統之間更緊密的整合。此外,計費管理、監管合規和支付方要求的日益複雜化也推動了對更先進、擴充性的RCM 平台的需求。這些趨勢,加上醫療保健 IT 和數位基礎設施投資的增加,使得 RCM 成為提升現代醫療保健系統營運效率和病人參與的關鍵驅動力。

北美在收入週期管理(RCM)市場中佔據最大的市場佔有率。

今年,北美在全球收入週期管理(RCM)市場佔據最大佔有率。這一成長得益於其完善的醫療保健基礎設施和對先進技術的早期應用。此外,美國醫療保健體系的複雜性也支撐了該地區的市場主導地位。該體系融合了私人保險和政府資助項目,因此需要複雜的解決方案來管理索賠、報銷和拒付流程。同時,遍佈全部區域的醫院、診所和診斷檢查室組成的龐大網路也顯著提升了對綜合索賠和病患支付管理系統的需求。此外,主要企業的強大影響力,以及基於價值的醫療保健模式和收入收取解決方案的持續應用,使得北美市場的整體前景仍然強勁。

收入週期管理 (RCM) 市場:主要市場細分

按解決方案和服務類型

- 後端收入周期解決方案

- 計費處理解決方案

- 其他

- 中期收入周期解決方案

- 臨床編碼解決方案

- 臨床文件改進方案

- 其他

- 患者准入解決方案

- 資格確認方案

- 預認證和核准

- 其他

- 外包服務

按實現類型

- 雲

- 現場

依系統類型

- 融合的

- 獨立型

按最終用戶類型

- 診斷實驗室

- 醫院

- 診所

- 其他

按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 奧地利

- 比利時

- 丹麥

- 法國

- 德國

- 愛爾蘭

- 義大利

- 荷蘭

- 挪威

- 俄羅斯

- 西班牙

- 瑞典

- 瑞士

- 英國

- 其他歐洲國家

- 亞洲

- 中國

- 印度

- 日本

- 新加坡

- 韓國

- 其他亞洲國家

- 拉丁美洲

- 巴西

- 智利

- 哥倫比亞

- 委內瑞拉

- 其他拉丁美洲國家

- 中東和北非

- 埃及

- 伊朗

- 伊拉克

- 以色列

- 科威特

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和北非國家

- 世界其他地區

- 澳洲

- 紐西蘭

- 其他國家

本報告研究了全球收入週期管理 (RCM) 市場,提供了概述、背景、市場影響因素分析、市場規模趨勢和預測、按各個細分市場進行的詳細分析、競爭格局以及主要企業的概況。

目錄

第一部分:報告概述

第1章:序言

第2章:調查方法

第3章 市場動態

第4章 宏觀經濟指標

第二部分:定性考量

第5章執行摘要

第6章:引言

第7章 監管情景

第三部分:市場概覽

第8章:主要企業綜合資料庫

第9章 競爭情勢

第10章:閒置頻段分析

第11章:企業競爭力分析

第12章:收入週期管理 (RCM) 市場中的Start-Ups生態系統

第四部分:公司簡介

第13章:公司簡介

- 章節概要

- 3M

- AdvantEdge Healthcare

- Athenahealth

- Cerner

- Change Healthcare

- Cognizant

- Conifer Health Solutions

- Epic Systems

- Experian

- GE Healthcare

- GeBBS Healthcare Solutions

- Huron Consulting Group

- McKesson

- MEDHOST

- Medical Information Technology

- Optum

- Oracle

- R1 RCM

- SSI Group

- Veradigm

第五部分:市場趨勢

第14章 大趨勢分析

第15章:未滿足需求的分析

第16章 專利分析

第17章 近期趨勢

第六部分:市場機會分析

第18章:全球收入週期管理(RCM)市場

第19章 按解決方案和服務類型分類的市場機會

第20章 依部署方式分類的市場機會

第21章 依系統類型分類的市場機會

第22章 最終用戶的市場機會

第23章 北美收入週期管理(RCM)的市場機會

第24章 歐洲收入週期管理(RCM)的市場機會

第25章 亞洲收入周期管理(RCM)的市場機會

第26章 中東和北非的收入週期管理(RCM)市場機會

第27章 拉丁美洲收入周期管理(RCM)的市場機會

第28章 世界其他地區收入週期管理(RCM)的市場機會

第29章 市場集中度分析:主要企業的分佈

第30章:鄰近市場分析

第七部分:戰略工具

第31章:制勝的關鍵策略

第32章:波特五力分析

第33章 SWOT分析

第34章 價值鏈分析

第35章:ROOTS的策略建議

第8章:其他獨家見解

第36章 來自初步調查的見解

第37章:報告結論

第九部分:附錄

第38章:表格形式數據

第3章⑨ 公司與組織列表

第40章:客製化的機會

第41章:ROOTS訂閱服務

第42章 作者信息

Revenue Cycle Management Market Outlook

As per Roots Analysis, the global revenue cycle management market size is estimated to grow from USD 200.1 billion in the current year to USD 663.3 billion by 2035, at a CAGR of 11.51% during the forecast period, till 2035.

Revenue cycle management (RCM) comprises an integrated set of processes utilized by healthcare organizations to oversee and optimize financial activities related to patient services, spanning from initial appointment scheduling or patient interaction to final payment realization. It includes a broad spectrum of administrative and clinical functions (such as patient engagement, insurance verification, medical billing, payment processing, and denial management), aimed at ensuring efficient revenue capture and collection. As the need to monitor financial performance metrics intensifies for evaluating operational effectiveness, identifying gaps, and maintaining sustainable profitability, the adoption of advanced RCM solutions is accelerating across the healthcare industry.

Moreover, the ongoing shift toward value-based care and reimbursement models is significantly increasing the demand for sophisticated revenue management systems. This transition adds complexity to revenue cycles, as reimbursement is increasingly tied to quality outcomes and performance indicators, thereby requiring more advanced and adaptable RCM frameworks. Additionally, the expanding integration of electronic health records (EHRs) is playing a pivotal role in market growth by transforming the way patient data is captured, analyzed, and managed. Looking ahead, continuous advancements in automation, artificial intelligence, and seamless integration with patient engagement platforms are expected to further enhance efficiency, positioning the RCM market for robust growth over the forecast period.

Strategic Insights for Senior Leaders

Key Drivers Propelling Growth of Revenue Cycle Management Market

Several key factors are driving the growth of the revenue cycle management market. Foremost among these is the widespread adoption of electronic health record (EHR) systems, which has significantly increased the demand for integrated RCM solutions capable of managing both clinical and financial data within a unified platform. This has encouraged healthcare organizations to invest in advanced revenue cycle analytics and billing services. Additionally, the ongoing transition from traditional fee-for-service models to value-based care is further accelerating market expansion, as providers are increasingly reimbursed based on patient outcomes and quality of care rather than service volume. Moreover, rising healthcare costs, growing billing complexities, supportive government initiatives, and evolving regulatory requirements are collectively expected to further propel the growth of the RCM market.

Revenue Cycle Management Market: Competitive Landscape of Companies in this Industry

The competitive landscape of the revenue cycle management (RCM) market is evolving rapidly, driven by the increasing presence of emerging entrants alongside established global players. Prominent companies such as 3M, Change Healthcare, Optum, and McKesson are shaping the market through continuous technological innovation, diverse solution portfolios, strong customer service capabilities, and strategic collaborations and partnerships. These organizations are prioritizing advancements in artificial intelligence, machine learning, automation, and cloud-based platforms to enhance the efficiency and effectiveness of their RCM offerings. To strengthen their market position, they are also differentiating themselves by delivering comprehensive solutions, including clinical documentation services, medical coding and compliance tools, claims processing, and payment management systems.

Revenue Cycle Management in Advanced Medical Billing Environments

Revenue cycle management (RCM) plays a critical role in modern medical billing systems by bridging the gap between clinical service delivery and financial outcomes, ensuring that healthcare providers are accurately and timely reimbursed. It encompasses the entire financial workflow, from patient registration and insurance verification to coding, claims submission, payment posting, and collections, thereby enabling seamless coordination between administrative and clinical functions.

In today's complex healthcare environment, RCM has evolved into a strategic function that enhances billing accuracy, reduces claim denials, improves cash flow, and ensures regulatory compliance. Moreover, the integration of advanced technologies (such as automation, analytics, and artificial intelligence) within RCM systems is further optimizing billing efficiency, improving patient experience through transparent billing processes. This is supporting the long-term financial sustainability of healthcare organizations.

Emerging Trends in Revenue Cycle Management Market

The revenue cycle management (RCM) market is experiencing a wave of emerging trends driven by rapid digital transformation and evolving healthcare requirements. A prominent trend is the increasing adoption of artificial intelligence (AI), automation, and advanced analytics, which are enhancing billing accuracy, reducing claim denials, and streamlining administrative workflows. Further, the growing shift toward value-based care models is transforming RCM into a strategic function, as healthcare providers must manage complex reimbursement structures linked to patient outcomes.

Another key trend is the rising demand for integrated and cloud-based RCM solutions, which enable real-time data access, interoperability, and improved coordination across clinical and financial systems. Additionally, increasing complexities in claims management, regulatory compliance, and payer requirements are driving the need for more advanced and scalable RCM platforms. Collectively, these trends, supported by growing investments in healthcare IT and digital infrastructure, are positioning RCM as a critical enabler of operational efficiency, and enhanced patient engagement in modern healthcare systems.

North America Holding the Largest Share in the Revenue Cycle Management Market

According to our analysis, in the current year, North America captures the highest share of the global revenue cycle management market. This growth is due to its well-established healthcare infrastructure and early adoption of advanced technologies. Further, the region's dominance is driven by the complexity of the US healthcare system, which encompasses a mix of private insurance and government-funded programs, thereby necessitating sophisticated solutions for managing claims, reimbursements, and denial processes. Additionally, the large network of hospitals, physician practices, and diagnostic laboratories across the region significantly increases the demand for comprehensive billing and patient payment management systems. Furthermore, the strong presence of major market players, coupled with the ongoing introduction of value-based care models and revenue recovery solutions, continues to strengthen the overall market outlook in North America.

Key Challenges in the Revenue Cycle Management Market

Despite strong growth prospects, the market may face constraints due to frequently evolving regulatory requirements and high implementation costs. Government bodies and insurance providers regularly revise reimbursement policies, creating a dynamic compliance environment that can be challenging for healthcare organizations to navigate. Additionally, the significant upfront investment required for deploying healthcare financial management systems (including software, hardware, and supporting tools) can place considerable financial pressure on providers. Consequently, the combined impact of regulatory complexity and high adoption costs may hinder market growth during the forecast period.

Revenue Cycle Management Market: Key Market Segmentation

By Type of Solutions & Services

- Back-end Revenue Cycle Solution

- Claims Processing Solutions

- Others

- Mid-Revenue Cycle Solutions

- Clinical Coding Solutions

- Clinical Documentation Improvement Solutions

- Others

- Patient Access Solutions

- Eligibility Verification Solutions

- Pre-certification & Authorization

- Others

- Outsourcing Services

By Type of Deployment

- Cloud

- On-Premises

By Type of System

- Integrated

- Standalone

By Type of End-User

- Diagnostics Laboratories

- Hospital

- Physician's Office

- Other

By Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

Example Players in Revenue Cycle Management Market

- 3M

- AdvantEdge Healthcare

- Athenahealth

- Cerner

- Change Healthcare

- Cognizant

- Conifer Health Solutions

- Epic systems

- Experian

- GE Healthcare

- GeBBS Healthcare Solutions

- Huron Consulting Group

- McKesson

- MCKesson

- MEDHOST

- Medical Information

- Optum

- Oracle

- R1 RCM

- SSI Group

- Veradigm

Revenue Cycle Management Market: Report Coverage

The report on the revenue cycle management market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the revenue cycle management market, focusing on key market segments, including [A] type of solution & service, [B] type of deployment, [C] type of system, [D] type of end user, and [E] geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the revenue cycle management market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the revenue cycle management market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] product / technology portfolio, [J] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in the revenue cycle management industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the revenue cycle management domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the revenue cycle management market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the revenue cycle management market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

Key Questions Answered in this Report

- What is the current and future market size?

- Who are the leading companies in this market?

- What are the growth drivers that are likely to influence the evolution of this market?

- What are the key partnership and funding trends shaping this industry?

- Which region is likely to grow at higher CAGR till 2035?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- Detailed Market Analysis: The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- In-depth Analysis of Trends: Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. Each report maps ecosystem activity across partnerships, funding, and patent landscapes to reveal growth hotspots and white spaces in the industry.

- Opinion of Industry Experts: The report features extensive interviews and surveys with key opinion leaders and industry experts to validate market trends mentioned in the report.

- Decision-ready Deliverables: The report offers stakeholders with strategic frameworks (Porter's Five Forces, value chain, SWOT), and complimentary Excel / slide packs with customization support.

Additional Benefits

- Complimentary Dynamic Excel Dashboards for Analytical Modules

- Exclusive 15% Free Content Customization

- Personalized Interactive Report Walkthrough with Our Expert Research Team

- Free Report Updates for Versions Older than 6-12 Months

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Revenue Cycle Management Market

- 6.2.1. Type of Solution & Service

- 6.2.2. Type of Deployment

- 6.2.3. Type of System

- 6.2.4. Type of End User

- 6.3. Future Perspective

7. REGULATORY SCENARIO

SECTION III: MARKET OVERVIEW

8. COMPREHENSIVE DATABASE OF LEADING PLAYERS

9. COMPETITIVE LANDSCAPE

- 9.1. Chapter Overview

- 9.2. Revenue Cycle Management: Overall Market Landscape

- 9.2.1. Analysis by Year of Establishment

- 9.2.2. Analysis by Company Size

- 9.2.3. Analysis by Location of Headquarters

- 9.2.4. Analysis by Ownership Structure

10. WHITE SPACE ANALYSIS

11. COMPANY COMPETITIVENESS ANALYSIS

12. STARTUP ECOSYSTEM IN THE REVENUE CYCLE MANAGEMENT MARKET

- 12.1. Revenue Cycle Management: Market Landscape of Startups

- 12.1.1. Analysis by Year of Establishment

- 12.1.2. Analysis by Company Size

- 12.1.3. Analysis by Company Size and Year of Establishment

- 12.1.4. Analysis by Location of Headquarters

- 12.1.5. Analysis by Company Size and Location of Headquarters

- 12.1.6. Analysis by Ownership Structure

- 12.2. Key Findings

SECTION IV: COMPANY PROFILES

13. COMPANY PROFILES

- 13.1. Chapter Overview

- 13.2. 3M *

- 13.2.1. Company Overview

- 13.2.2. Company Mission

- 13.2.3. Company Footprint

- 13.2.4. Management Team

- 13.2.5. Contact Details

- 13.2.6. Financial Performance

- 13.2.7. Operating Business Segments

- 13.2.8. Service / Product Portfolio (project specific)

- 13.2.9. MOAT Analysis

- 13.2.10. Recent Developments and Future Outlook

- 13.3. AdvantEdge Healthcare

- 13.4. Athenahealth

- 13.5. Cerner

- 13.6. Change Healthcare

- 13.7. Cognizant

- 13.8. Conifer Health Solutions

- 13.9. Epic Systems

- 13.10. Experian

- 13.11. GE Healthcare

- 13.12. GeBBS Healthcare Solutions

- 13.13. Huron Consulting Group

- 13.14. McKesson

- 13.15. MEDHOST

- 13.16. Medical Information Technology

- 13.17. Optum

- 13.18. Oracle

- 13.19. R1 RCM

- 13.20. SSI Group

- 13.21. Veradigm

SECTION V: MARKET TRENDS

14. MEGA TRENDS ANALYSIS

15. UNMEET NEED ANALYSIS

16. PATENT ANALYSIS

17. RECENT DEVELOPMENTS

- 17.1. Chapter Overview

- 17.2. Recent Funding

- 17.3. Recent Partnerships

- 17.4. Other Recent Initiatives

SECTION VI: MARKET OPPORTUNITY ANALYSIS

18. GLOBAL REVENUE CYCLE MANAGEMENT MARKET

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Trends Disruption Impacting Market

- 18.4. Demand Side Trends

- 18.5. Supply Side Trends

- 18.6. Global Revenue Cycle Management Market, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.7. Multivariate Scenario Analysis

- 18.7.1. Conservative Scenario

- 18.7.2. Optimistic Scenario

- 18.8. Investment Feasibility Index

- 18.9. Key Market Segmentations

19. MARKET OPPORTUNITIES BASED ON TYPE OF SOLUTION & SERVICE

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Revenue Cycle Management Market for Back-end Revenue Cycle Solution: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.7. Revenue Cycle Management Market for Mid-Revenue Cycle Solutions: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.8. Revenue Cycle Management Market for Patient Access Solutions: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.9. Revenue Cycle Management Market for Outsourcing Services: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.10. Data Triangulation and Validation

- 19.10.1. Secondary Sources

- 19.10.2. Primary Sources

- 19.10.3. Statistical Modeling

20. MARKET OPPORTUNITIES BASED ON TYPE OF DEPLOYMENT

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Revenue Cycle Management Market for Cloud Printing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.7. Revenue Cycle Management Market for On-Premises: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.8. Data Triangulation and Validation

- 20.8.1. Secondary Sources

- 20.8.2. Primary Sources

- 20.8.3. Statistical Modeling

21. MARKET OPPORTUNITIES BASED ON TYPE OF SYSTEM

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Revenue Cycle Management Market for Integrated: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.7. Revenue Cycle Management Market for Standalone: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.8. Data Triangulation and Validation

- 21.8.1. Secondary Sources

- 21.8.2. Primary Sources

- 21.8.3. Statistical Modeling

22. MARKET OPPORTUNITIES BASED ON TYPE OF END USER

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Revenue Cycle Management Market for Diagnostics Laboratories: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.7. Revenue Cycle Management Market for Hospitals: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.8. Revenue Cycle Management Market for Physician's Office: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.9. Revenue Cycle Management Market for Other: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.10. Data Triangulation and Validation

- 22.10.1. Secondary Sources

- 22.10.2. Primary Sources

- 22.10.3. Statistical Modeling

23. MARKET OPPORTUNITIES FOR REVENUE CYCLE MANAGEMENT IN NORTH AMERICA

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Revenue Cycle Management Market in North America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.1. Revenue Cycle Management Market in the US: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.2. Revenue Cycle Management Market in Canada: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.3. Revenue Cycle Management Market in Mexico: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.4. Revenue Cycle Management Market in Other North American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.7. Data Triangulation and Validation

24. MARKET OPPORTUNITIES FOR REVENUE CYCLE MANAGEMENT IN EUROPE

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Revenue Cycle Management Market in Europe: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.1. Revenue Cycle Management Market in Austria: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.2. Revenue Cycle Management Market in Belgium: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.3. Revenue Cycle Management Market in Denmark: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.4. Revenue Cycle Management Market in France: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.5. Revenue Cycle Management Market in Germany: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.6. Revenue Cycle Management Market in Ireland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.7. Revenue Cycle Management Market in Italy: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.8. Revenue Cycle Management Market in Netherlands: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.9. Revenue Cycle Management Market in Norway: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.10. Revenue Cycle Management Market in Russia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.11. Revenue Cycle Management Market in Spain: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.12. Revenue Cycle Management Market in Sweden: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.13. Revenue Cycle Management Market in Switzerland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.14. Revenue Cycle Management Market in the UK: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.15. Revenue Cycle Management Market in Other European Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.7. Data Triangulation and Validation

25. MARKET OPPORTUNITIES FOR REVENUE CYCLE MANAGEMENT IN ASIA

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Revenue Cycle Management Market in Asia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.1. Revenue Cycle Management Market in China: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.2. Revenue Cycle Management Market in India: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.3. Revenue Cycle Management Market in Japan: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.4. Revenue Cycle Management Market in Singapore: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.5. Revenue Cycle Management Market in South Korea: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.6. Revenue Cycle Management Market in Other Asian Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.7. Data Triangulation and Validation

26. MARKET OPPORTUNITIES FOR REVENUE CYCLE MANAGEMENT IN MIDDLE EAST AND NORTH AFRICA (MENA)

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Revenue Cycle Management Market in Middle East and North Africa (MENA): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.1. Revenue Cycle Management Market in Egypt: Historical Trends (Since 2019) and Forecasted Estimates (Till 205)

- 26.6.2. Revenue Cycle Management Market in Iran: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.3. Revenue Cycle Management Market in Iraq: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.4. Revenue Cycle Management Market in Israel: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.5. Revenue Cycle Management Market in Kuwait: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.6. Revenue Cycle Management Market in Saudi Arabia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.7. Neuromorphic Computing Marke in United Arab Emirates (UAE): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.8. Revenue Cycle Management Market in Other MENA Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.7. Data Triangulation and Validation

27. MARKET OPPORTUNITIES FOR REVENUE CYCLE MANAGEMENT IN LATIN AMERICA

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Revenue Cycle Management Market in Latin America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.1. Revenue Cycle Management Market in Argentina: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.2. Revenue Cycle Management Market in Brazil: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.3. Revenue Cycle Management Market in Chile: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.4. Revenue Cycle Management Market in Colombia Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.5. Revenue Cycle Management Market in Venezuela: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.6. Revenue Cycle Management Market in Other Latin American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.7. Data Triangulation and Validation

28. MARKET OPPORTUNITIES FOR REVENUE CYCLE MANAGEMENT IN REST OF THE WORLD

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Revenue Shift Analysis

- 28.4. Market Movement Analysis

- 28.5. Penetration-Growth (P-G) Matrix

- 28.6. Revenue Cycle Management Market in Rest of the World: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.1. Revenue Cycle Management Market in Australia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.2. Revenue Cycle Management Market in New Zealand: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.3. Revenue Cycle Management Market in Other Countries

- 28.7. Data Triangulation and Validation

29. MARKET CONCENTRATION ANALYSIS: DISTRIBUTION BY LEADING PLAYERS

30. ADJACENT MARKET ANALYSIS

SECTION VII: STRATEGIC TOOLS

31. KEY WINNING STRATEGIES

32. PORTER'S FIVE FORCES ANALYSIS

33. SWOT ANALYSIS

34. VALUE CHAIN ANALYSIS

35. ROOTS STRATEGIC RECOMMENDATIONS

SECTION VIII: OTHER EXCLUSIVE INSIGHTS

36. INSIGHTS FROM PRIMARY RESEARCH

37. REPORT CONCLUSION

SECTION IX: APPENDIX

38. TABULATED DATA

39. LIST OF COMPANIES AND ORGANIZATIONS

40. CUSTOMIZATION OPPORTUNITIES

41. ROOTS SUBSCRIPTION SERVICES

42. AUTHOR DETAILS

2026年全球扣款管理市場報告

2026年全球扣款管理市場報告 醫療保健收入週期管理市場規模、佔有率和成長分析:按組件、交付方式、最終用戶和地區分類-2026-2033年產業預測

醫療保健收入週期管理市場規模、佔有率和成長分析:按組件、交付方式、最終用戶和地區分類-2026-2033年產業預測 收入週期管理市場:按組件、流程、部署模式和最終用戶分類 - 2026-2032 年全球市場預測

收入週期管理市場:按組件、流程、部署模式和最終用戶分類 - 2026-2032 年全球市場預測 收益管理市場(至2035年):依組件、解決方案、服務、部署模式、產業和地區劃分:產業趨勢和全球預測

收益管理市場(至2035年):依組件、解決方案、服務、部署模式、產業和地區劃分:產業趨勢和全球預測 2026-2030年全球醫療保健收入週期管理(RCM)軟體市場2026年全球捆綁支付管理軟體市場報告

2026-2030年全球醫療保健收入週期管理(RCM)軟體市場2026年全球捆綁支付管理軟體市場報告 收入週期管理市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、模組、部署類型和功能分類

收入週期管理市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、模組、部署類型和功能分類 收入週期管理市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球收入週期管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

收入週期管理市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球收入週期管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2034年按類型、組件、部署類型、最終用戶和地區分類的收入週期管理市場規模、佔有率、趨勢和預測

2026-2034年按類型、組件、部署類型、最終用戶和地區分類的收入週期管理市場規模、佔有率、趨勢和預測