|

市場調查報告書

商品編碼

1919790

癌症治療領域人工智慧 (AI) 市場——產業趨勢及全球預測(至 2040 年)——按癌症類型、最終用戶和地區劃分AI In Oncology Market, till 2040: Distribution by Type of Cancer, Type of End User, and Geographical Regions: Industry Trends and Global Forecasts |

||||||

癌症治療領域人工智慧市場展望

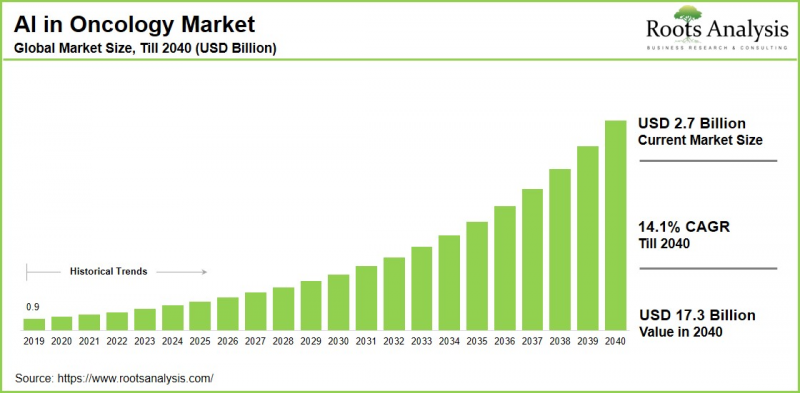

全球癌症治療領域人工智慧市場預計將從目前的 27 億美元增長至 2040 年的 173 億美元,在預測期內(至 2040 年)的複合年增長率 (CAGR) 為 14.1%。本研究提供有關市場規模、成長情境、產業趨勢和未來預測的資訊。

全球癌症發生率的不斷上升推動了對先進診斷和治療方法的需求。人工智慧 (AI) 正在改變腫瘤學,從早期檢測、影像和病理分析(例如乳房 X 光檢查和 CT 掃描)到個人化治療,人工智慧在患者治療的各個階段都能改善癌症護理。它還有助於預測患者預後,從而提高醫療服務的效率、準確性和可近性。

預計在預測期內,腫瘤領域的人工智慧市場將以顯著的速度成長。這主要得益於對早期精準檢測的迫切需求、精準醫療的興起,以及為應對日益增長的全球癌症負擔而需要優化且經濟有效的治療方案。

高階主管策略洞察

腫瘤領域人工智慧市場:競爭格局

腫瘤領域人工智慧市場的競爭格局呈現出來自大型企業和小型企業的激烈競爭。西門子醫療和通用電氣醫療透過將各種成像設備與 70 多種 FDA 批准的 AI 演算法相結合,建立了市場主導地位,從而創造了持續的軟體收入並確保了工作流程的整合。此外,IBM、NVIDIA、PathAI、ConcertAI、Tempus、Oracle、美敦力、飛利浦等主要廠商,以及 Azra AI 和 Paige AI 等新興公司,都在診斷、藥物研發、病理學和精準醫療領域提供專業解決方案。

人工智慧在癌症治療領域有哪些機會?

預計到 2040 年,全球癌症治療領域的人工智慧市場規模將達到 173 億美元。目前,實體瘤在癌症類型中佔據了大部分市場份額。

全球癌症發生率的上升以及對創新人工智慧驅動的早期檢測工具日益增長的需求,凸顯了人工智慧在癌症治療領域的重要作用。此外,人工智慧在腫瘤學和分子生物學領域個性化治療的日益廣泛應用,預計將在整個預測期內推動市場擴張。

人工智慧在癌症治療領域的演進:新興產業趨勢

腫瘤學領域人工智慧 (AI) 的新興趨勢強調精準診斷、個人化治療和加速藥物研發流程。人工智慧驅動的演算法透過先進的影像技術(例如 PET/CT 融合成像和組織病理學分析)顯著提高了早期癌症的檢測率,腫瘤檢測準確率高達 99%。在治療決策方面,人工智慧利用多組學資料集、基因組分析和全面的患者記錄來預測治療反應並模擬腫瘤微環境,從而指導精準幹預。此外,人工智慧還透過先進的平台優化臨床試驗參與者的招募,促進奈米載體工程,並利用奈米感測器實現即時監測。

推動癌症治療領域人工智慧市場成長的關鍵因素

推動癌症治療領域人工智慧市場成長的關鍵因素有幾個。全球癌症發生率的不斷攀升推動了對先進診斷解決方案的需求,而人工智慧增強的成像和分析技術能夠實現超越人類能力的早期精準腫瘤檢測。此外,製藥和生物技術產業的巨額投資正透過預測建模加速藥物研發進程,從而降低臨床試驗的成本和時間。同時,FDA 等監管機構的批准、資金的增加以及醫療機構的廣泛應用,也使得人工智慧在診斷、治療方案製定和營運效率提升方面得以實際應用。

主要市場挑戰

腫瘤學領域的人工智慧市場面臨著許多挑戰,包括難以取得大型、高品質且具代表性的多模態資料集,這會影響模型的效能。資料收集、基礎設施建設以及與現有腫瘤工作流程整合的高昂前期成本,以及與傳統 IT 系統缺乏互通性,都限制了人工智慧的應用,尤其是在規模較小或資源有限的醫療機構中。此外,監管架構尚不明確且不斷演變,加之對敏感基因組和腫瘤資料安全保護的需求日益增長,都在減緩人工智慧解決方案在實際腫瘤治療中的審批和推廣。

腫瘤人工智慧市場:主要市場區隔

癌症類型

- 實體惡性腫瘤

- 乳癌

- 肺癌

- 前列腺癌

- 大腸直腸癌

- 腦腫瘤

- 其他

最終使用者類型

- 醫院

- 製藥公司

- 研究機構

- 其他

地理區域

- 北美

- 美國

- 加拿大

- 墨西哥

- 其他北美地區國家/地區

- 歐洲

- 奧地利

- 比利時

- 丹麥

- 法國

- 德國

- 愛爾蘭

- 義大利

- 荷蘭

- 挪威

- 俄羅斯

- 西班牙

- 瑞典

- 瑞士

- 英國

- 其他歐洲國家/地區

- 亞洲

- 中國

- 印度

- 日本

- 新加坡

- 韓國

- 其他亞洲國家/地區

- 拉丁美洲

- 巴西

- 智利

- 哥倫比亞

- 委內瑞拉

- 其他拉丁美洲國家/地區

- 中東和北非非洲

- 埃及

- 伊朗

- 伊拉克

- 以色列

- 科威特

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和北非國家

- 世界其他地區

- 澳大利亞

- 紐西蘭

人工智慧在癌症治療市場:關鍵市場份額洞察

以癌症類型劃分的市佔率

依癌症類型劃分,全球市場可分為實體惡性腫瘤、乳癌、肺癌、攝護腺癌、大腸癌、腦腫瘤和其他癌症。據我們估計,實體惡性腫瘤目前佔據了大部分市場份額。這是由於癌症發生率不斷上升,從而推動了對創新、可擴展且精準的工具的需求。

依地區劃分的市佔率

據我們估計,歐洲目前在腫瘤人工智慧市場中佔有較大份額。這主要歸功於製藥公司越來越多地使用基於人工智慧的工具進行藥物研發,以及旨在改善歐洲醫療保健體系的合作協議的增加。此外,值得注意的是,亞太地區的腫瘤人工智慧市場預計在預測期內將以更高的複合年增長率成長。

人工智慧癌症市場主要參與者

- Berg(BPGbio 旗下公司)

- CancerCenter.AI

- Concert AI

- GE Healthcare

- IBM Watson Health

- iCAD

- JLK Inspection

- Median Technologies

- Path AI

- Roche Diagnostics

人工智慧癌症市場:報告範圍

本報告對人工智慧癌症市場進行了詳細分析,涵蓋以下幾個方面:

- 市場規模與機會分析:對人工智慧癌症市場進行詳細分析,重點關注以下關鍵市場細分:[A] 癌症類型,[B] 最終用戶類型,以及 [C] 主要地區。

- 競爭格局:基於多個相關參數(包括成立年份、公司規模、總部所在地和所有權結構)對人工智慧癌症市場中的公司進行全面分析。

- 公司簡介:提供人工智慧癌症治療市場主要公司的詳細簡介,包括以下資訊:[A] 總部所在地,[B] 公司規模,[C] 企業理念,[D] 地理位置,[E] 管理團隊,[F] 聯絡方式,[G] 財務資訊,[H] 業務板塊,[I] 技術/平台組合,以及未來 [J] 近期發展和未來。

- 宏觀趨勢:評估人工智慧癌症治療產業的當前宏觀趨勢。

- 專利分析:基於相關參數(例如 [A] 專利類型,[B] 專利公開年份,[C] 專利年齡,以及 [D] 主要參與者)對與人工智慧癌症治療相關的已申請/已授權專利進行深入分析。

- 近期發展:概述人工智慧在癌症治療市場的最新發展,並基於相關參數進行分析,例如[A] 啟動年份、[B] 計畫類型、[C] 地理分佈和[D] 主要參與者。

- 波特五力分析:分析人工智慧在腫瘤治療市場中的五種競爭力量(新進入者的威脅、買方的議價能力、供應商的議價能力、替代品的威脅以及現有競爭對手之間的競爭)。

- SWOT 分析:深入剖析該領域的優勢、劣勢、機會和威脅。此外,還提供哈維鮑爾分析,突出每個 SWOT 參數的相對影響。

- 價值鏈分析:全面分析人工智慧在腫瘤治療市場的各個階段和利害關係人。

目錄

第一章:前言

第二章:執行摘要

第三章:導論

- 章節概述

- 人工智慧概述

- 人工智慧的類型

- 人工智慧在癌症治療中的作用

- 人工智慧應用的關鍵挑戰

- 未來展望

第四章:市場概述

- 章節概述

- 人工智慧在癌症治療的應用:軟體供應商的市場格局

- 人工智慧在癌症治療中的應用:軟體解決方案的市場格局

第五章:公司簡介

- 章節概述

- 羅氏診斷

- IBM Watson Health

- CancerCenter.AI

- GE Healthcare

- Concert AI

- Path AI

- Berg

- Median Technologies

- iCAD

- JLK Inspection

第六章:競爭分析

- 章節概述

- 假設和關鍵參數

- 研究方法

第七章:專利分析

- 章節概述

- 範圍與研究方法

- 人工智慧在癌症治療的應用:專利分析

- 人工智慧在癌症治療的應用:專利基準分析

第八章:合作與夥伴關係

- 章節概述

- 合作模式

- 人工智慧在癌症治療的應用:近期合作與夥伴關係合作

第九章 融資與投資分析

- 章節概述

- 融資模式類型

- 人工智慧在癌症治療的應用:融資與投資分析列表

- 投資總結

- 結論

第十章:藍海策略:新創企業進入競爭激烈市場的策略指南

- 章節概述

- 藍海策略概述

- 紅海

- 藍海

- 紅海策略與藍海策略的差異

- 人工智慧在癌症治療的應用:藍海策略與工具轉型

- 結論

第十一章 市場規模與機會分析

- 章節概述

- 關鍵資訊假設與研究方法

- 全球腫瘤人工智慧市場

- 癌症治療中的人工智慧:按癌症類型分析

- 癌症治療中的人工智慧:按最終用戶類型分析

- 癌症治療中的人工智慧:按主要地區分析

第十二章:結論

第十三章:高階主管洞察

第十四章:附錄 1:表格資料

第十五章:附錄 2:公司與組織清單

AI in Oncology Market Outlook

As per Roots Analysis, the global AI in oncology market size is estimated to grow from USD 2.7 billion in the current year to USD 17.3 billion by 2040, at a CAGR of 14.1% during the forecast period, till 2040. The new study provides information on market size, growth scenarios, industry trends and future forecasts.

Given the rising incidence of cancer globally, there has been an increased demand for advanced diagnostic and treatment methods to care for patients. Artificial Intelligence (AI) is transforming oncology by improving cancer care at every stage of the patient's journey, from early detection through imaging and pathology analysis (such as mammograms and CT scans) to personalized treatment. It also aids in predicting patient outcomes, thereby enhancing efficiency, accuracy, and accessibility of care.

AI in oncology market is expected to rise at a significant rate throughout the forecast period. This is due to urgent demand for early, accurate detection, the shift toward precision medicine, and the need for optimized, cost-effective treatment planning to manage a rising global cancer burden.

Strategic Insights for Senior Leaders

AI in Oncology Market: Competitive Landscape of Companies in this Industry

The competitive landscape of AI in oncology market is characterized by intense competition, featuring a combination of large and smaller firms. Siemens Healthineers and GE Healthcare hold dominant positions through extensive imaging equipment, using >70 FDA-cleared AI algorithms to generate recurring software revenue and ensure workflow integration. Further, other key players, such as IBM, NVIDIA, PathAI, ConcertAI, Tempus, Oracle, Medtronic, and Philips, along with emerging players like Azra AI, Paige AI, offer targeted solutions in diagnostics, drug discovery, pathology, and precision medicine.

What is the Opportunity for AI in Oncology?

The global AI in oncology market is projected to reach USD 17.3 billion by 2040. Solid tumors currently dominate the market share among other cancer types.

Rising cancer prevalence worldwide, along with the need for innovative AI-driven early detection tools, highlights the critical role of AI in oncology. Additionally, expanding AI applications in oncology and molecular biology for personalized therapies are likely to fuel market expansion throughout the forecast period.

AI in Oncology Evolution: Emerging Trends in the Industry

Emerging trends in artificial intelligence (AI) within the oncology sector emphasize precision diagnostics, personalized therapies, and expedited drug development pipelines. AI-driven algorithms significantly improve early-stage cancer identification via advanced imaging modalities such as PET / CT fusion and histopathological analysis, attaining tumor detection accuracies to 99%. For therapeutic decision-making, AI leverages multi-omics datasets, genomic profiling, and comprehensive patient records to forecast treatment efficacy, and model tumor microenvironments to advance precision interventions. Further, AI optimizes clinical trial recruitment via advanced platforms, facilitates nanocarrier engineering, and enables real-time surveillance with nano sensors.

Key Drivers Propelling Growth of AI in Oncology Market

The growth of the AI in oncology market is propelled by several pivotal drivers. The escalating global incidence of cancer has heightened demand for advanced diagnostic solutions, where AI-enhanced imaging and analytics enable earlier and more accurate tumor detection beyond human capabilities. Further, substantial investments from pharmaceutical and biotechnology sectors have accelerated drug discovery processes through predictive modeling, thereby reducing clinical trial expenses and timelines. Furthermore, regulatory endorsements such as FDA approvals, coupled with increased funding and widespread adoption in healthcare institutions, have enabled the practical deployment of AI across diagnostics, treatment planning, and operational efficiencies.

Key Market Challenges

The market for AI in oncology faces significant challenges, including limited access to large, high-quality, and representative multimodal datasets which affect model performance. High upfront costs for data acquisition, infrastructure, and integration into existing oncology workflows, combined with a lack of interoperability with legacy IT systems, also limits the adoption, especially in smaller or resource-limited centers. Additionally, unclear and evolving regulatory frameworks, coupled with heightened requirements for data security and protection of sensitive genomic and oncology data, slow approvals and scale-up of AI solutions in real-world oncology practice.

AI in Oncology Market: Key Market Segmentation

Type of Cancer

- Solid malignancies

- Breast cancer

- Lung cancer

- Prostate cancer

- Colorectal cancer

- Brain tumor

- Others

Type of End User

- Hospitals

- Pharmaceutical companies

- Research Institutes

- Others

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

AI in Oncology Market: Key Market Share Insights

Market Share by Type of Cancer

Based on the type of cancer, the global market is segmented into solid malignancies, breast cancer, lung cancer, prostate cancer, colorectal cancer, brain tumor and others. According to our estimates, currently, solid malignancies segment captures majority share of the market. This is due to the increasing prevalence of cancer, which creates the need for innovative, scalable, and precise tools.

Market Share by Geography

According to our estimates Europe currently captures a significant share of the AI in oncology market. This is due to the increasing utilization of AI-based tools by pharmaceutical companies for drug discovery and the rise in partnership agreements aimed at improving healthcare system in Europe. It is also important to note that the AI in oncology market in the Asia-Pacific region is expected to grow at a higher CAGR over the forecast period.

Example Players in AI in Oncology Market

- Berg (A part of BPGbio)

- CancerCenter.AI

- Concert AI

- GE Healthcare

- IBM Watson Health

- iCAD

- JLK Inspection

- Median Technologies

- Path AI

- Roche Diagnostics

AI in Oncology Market: Report Coverage

The report on the AI in oncology market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the AI in oncology market, focusing on key market segments, including [A] type of cancer, [B] type of end user, and [C] key geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the AI in oncology market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the AI in oncology market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] technology / platform portfolio, [J] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in the AI in oncology industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the AI in oncology domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the AI in oncology market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the AI in oncology market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

- Value Chain Analysis: A comprehensive analysis of the value chain, providing information on the different phases and stakeholders involved in the AI in oncology market.

Key Questions Answered in this Report

- What is the current and future market size?

- Who are the leading companies in this market?

- What are the growth drivers that are likely to influence the evolution of this market?

- What are the key partnership and funding trends shaping this industry?

- Which region is likely to grow at higher CAGR till 2040?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- Detailed Market Analysis: The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- In-depth Analysis of Trends: Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. Each report maps ecosystem activity across partnerships, funding, and patent landscapes to reveal growth hotspots and white spaces in the industry.

- Opinion of Industry Experts: The report features extensive interviews and surveys with key opinion leaders and industry experts to validate market trends mentioned in the report.

- Decision-ready Deliverables: The report offers stakeholders with strategic frameworks (Porter's Five Forces, value chain, SWOT), and complimentary Excel / slide packs with customization support.

Additional Benefits

- Complimentary Dynamic Excel Dashboards for Analytical Modules

- Exclusive 15% Free Content Customization

- Personalized Interactive Report Walkthrough with Our Expert Research Team

- Free Report Updates for Versions Older than 6-12 Months

TABLE OF CONTENTS

1. PREFACE

- 1.1. Overview

- 1.2. Scope of the Report

- 1.3. Market Segmentation

- 1.4. Research Methodology

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. EXECUTIVE SUMMARY

- 2.1 Chapter Overview

3. INTRODUCTION

- 3.1. Chapter Overview

- 3.2. Overview of Artificial Intelligence

- 3.3. Types Of Artificial Intelligence

- 3.4. Role of AI in Oncology

- 3.5. Key Challenges Associated with Use of AI

- 3.6. Future Perspectives

4. MARKET OVERVIEW

- 4.1. Chapter Overview

- 4.2. AI in Oncology: Market Landscape of Software providers

- 4.2.1. Analysis by Year of Establishment

- 4.2.2. Analysis by Company Size

- 4.2.3. Analysis by Location of Headquarters (Region-wise)

- 4.2.4. Analysis by Location of Headquarters (Country-wise)

- 4.2.5. Analysis by Type of End-User

- 4.2.6. Analysis by Year of Establishment, Company size and Location of Headquarters

- 4.3. AI in Oncology: Market Landscape of Software Solutions

- 4.3.1. Analysis by Type of Service(s) Offered

- 4.3.2. Analysis by Type of AI Technology Used

- 4.3.3. Analysis by Type of Platform

- 4.3.4. Analysis by Type of Service(s) Offered and Type of End-User

- 4.3.5. Analysis by Type of Platform and Type of AI Technology Used

- 4.3.6. Analysis by Type of Service(s) Offered, Location of Headquarters and Type of AI Technology Used

5. COMPANY PROFILES

- 5.1. Chapter Overview

- 5.2. Roche Diagnostics

- 5.2.1. Company Overview

- 5.2.2. Financial Information

- 5.2.3. Service Portfolio

- 5.2.4. Recent Developments and Future Outlook

- 5.3. IBM Watson Health

- 5.3.1. Company Overview

- 5.3.2. Financial Information

- 5.3.3. Service Portfolio

- 5.3.4. Recent Developments and Future Outlook

- 5.4. CancerCenter.AI

- 5.4.1. Company Overview

- 5.4.2. Service Portfolio

- 5.4.3. Recent Development and Future Outlooks

- 5.5. GE Healthcare

- 5.5.1. Company Overview

- 5.5.2. Financial Information

- 5.5.3. Service Portfolio

- 5.5.4. Recent Development and Future Outlook

- 5.6. Concert AI

- 5.6.1. Company Overview

- 5.6.2. Service Portfolio

- 5.6.3. Recent Developments and Future Outlook

- 5.7. Path AI

- 5.7.1. Company Overview

- 5.7.2. Service portfolio

- 5.7.3. Recent Development and Future Outlook

- 5.8. Berg

- 5.8.1. Company Overview

- 5.8.2. Service Portfolio

- 5.8.3. Recent Development and Future Outlook

- 5.9. Median Technologies

- 5.9.1. Company Overview

- 5.9.2. Financial Information

- 5.9.3. Service Portfolio

- 5.9.4. Recent Development and Future Outlook

- 5.10. iCAD

- 5.10.1. Company Overview

- 5.10.2. Financial Information

- 5.10.3. Service Portfolio

- 5.10.4. Recent Developments and Future Outlook

- 5.11. JLK Inspection

- 5.11.1. Company Overview

- 5.11.2. Service Portfolio

- 5.11.3. Recent Development and Future Outlook

6. COMPANY COMPETITIVENESS ANALYSIS

- 6.1. Chapter Overview

- 6.2. Assumptions and Key Parameters

- 6.3. Methodology

- 6.3.1. Company Competitiveness: Small Companies in North America

- 6.3.2. Company Competitiveness: Small Companies in Europe

- 6.3.3. Company Competitiveness: Small Companies in Asia Pacific

- 6.3.4. Company Competitiveness: Mid-sized companies in North America

- 6.3.5. Company Competitiveness: Mid-sized companies in Europe

- 6.3.6. Company Competitiveness: Mid-sized companies in Asia Pacific

- 6.3.7. Company Competitiveness: Large companies in North America and Europe

7. PATENT ANALYSIS

- 7.1. Chapter Overview

- 7.2. Scope and Methodology

- 7.3. AI in Oncology: Patent Analysis

- 7.3.1. Analysis by Type of Patent

- 7.3.2. Analysis by Patent Publication Year

- 7.3.3. Analysis by Year-wise Trend of Filed Patent Applications and Granted Patents

- 7.3.4. Analysis by Jurisdiction

- 7.3.5. Analysis by Type of Industry

- 7.3.6. Analysis by Patent Age

- 7.3.7. Analysis by Legal Status

- 7.3.8. Analysis by CPC Symbols

- 7.3.9. Most Active Players: Analysis by Number of Patents

- 7.3.10. Analysis by Key Inventors

- 7.4. AI in Oncology: Patent Benchmarking Analysis

- 7.4.1. Analysis by Patent Characteristics

- 7.4.2. AI in Oncology: Patent Valuation Analysis

8. PARTNERSHIPS AND COLLABORATIONS

- 8.1. Chapter Overview

- 8.2. Partnership Models

- 8.3 AI in Oncology: Recent Partnerships and Collaborations

- 8.3.1. Analysis by Year of Partnership

- 8.3.2. Analysis by Type of Partnership

- 8.3.3. Analysis by Year and Type of Partnership

- 8.3.4. Analysis by Company Size and Type of Partnership

- 8.3.5. Most Active Partners: Analysis by Number of Partnerships

- 8.3.6. Most Active Players: Analysis by Type of Partnership

- 8.3.7. Analysis by Type of Cancer

- 8.3.8. Analysis by Type of Partner

- 8.3.9. Analysis by Year and Type of Partner

- 8.3.10. Intercontinental and Intracontinental Agreements

- 8.3.11. Local and International Agreements

- 8.3.12. Country-Wise Distribution

- 8.3.13. Analysis by Region

9. FUNDING AND INVESTMENT ANALYSIS

- 9.1. Chapter Overview

- 9.2. Types of Funding Models

- 9.3. AI in Oncology: List of Funding and Investment Analysis

- 9.3.1. Analysis by Year and Number of Funding Instances

- 9.3.2. Analysis by Year and Amount Invested

- 9.3.3 Analysis by Type of Funding and Number of Instances

- 9.3.4. Analysis by Year, Type of Funding and Amount Invested

- 9.3.5. Analysis by Type of Funding and Amount Invested

- 9.3.6. Analysis by Area of Application

- 9.3.7. Analysis by Focus Area

- 9.3.8. Analysis by Type of Cancer Indication

- 9.3.9. Analysis by Geography

- 9.3.10. Most Active Players by Number of Instances

- 9.3.11. Most Active Players by Amount Invested

- 9.3.12. Analysis by Type of Investors

- 9.3.13. Analysis by Lead Investors

- 9.4. Summary of Investments

- 9.5. Concluding Remarks

10. BLUE OCEAN STRATEGY: A STRATEGIC GUIDE FOR START-UPS TO ENTER INTO HIGHLY COMPETITIVE MARKET

- 10.1. Chapter Overview

- 10.2. Overview of Blue Ocean Strategy

- 10.2.1 Red Ocean

- 10.2.2 Blue Ocean

- 10.2.3 Difference between Red Ocean Strategy and Blue Ocean Strategy

- 10.2.4. AI in Oncology: Blue Ocean Strategy and Shift Tools

- 10.2.4.1. Value Innovation

- 10.2.4.2. Strategy Canvas

- 10.2.4.3. Four Action Framework

- 10.2.4.4. Eliminate-Raise-Reduce-Create (ERRC) Grid

- 10.2.4.5. Six Path Framework

- 10.2.4.6. Pioneer-Migrator-Settler (PMS) Map

- 10.2.4.7. Three Tiers of Noncustomers

- 10.2.4.8. Sequence of Blue Ocean Strategy

- 10.2.4.9. Buyer Utility Map

- 10.2.4.10. The Price Corridor of the Mass

- 10.2.4.11. Four Hurdles to Strategy Execution

- 10.2.4.12. Tipping Point Leadership

- 10.2.4.13. Fair Process

- 10.3. Conclusion

11. MARKET SIZING AND OPPORTUNITY ANALYSIS

- 11.1. Chapter Overview

- 11.2 Key Assumptions and Methodology

- 11.3. Global Artificial Intelligence in Oncology Market

- 11.4. Artificial Intelligence in Oncology Market: Analysis by Type of Cancer

- 11.4.1. Artificial Intelligence in Oncology Market for Breast Cancer

- 11.4.2. Artificial Intelligence in Oncology Market for Lung Cancer

- 11.4.3. Artificial Intelligence in Oncology Market for Prostate Cancer

- 11.4.4. Artificial Intelligence in Oncology Market for Colorectal Cancer

- 11.4.5. Artificial Intelligence in Oncology Market for Brain Tumor

- 11.4.6. Artificial Intelligence in Oncology Market for Solid Malignancies

- 11.4.7. Artificial Intelligence in Oncology Market for Other Cancers

- 11.5. Artificial Intelligence in Oncology Market: Analysis by Type of End-User

- 11.5.1. Artificial Intelligence in Oncology Market for Hospitals

- 11.5.2. Artificial Intelligence in Oncology Market for Pharmaceutical Companies

- 11.5.3. Artificial Intelligence in Oncology Market for Research Institutes

- 11.5.4. Artificial Intelligence in Oncology Market for Other End-Users

- 11.6. Artificial Intelligence in Oncology Market: Analysis by Key Geographical Regions

- 11.6.1. Artificial Intelligence in Oncology Market for North America

- 11.6.2. Artificial Intelligence in Oncology Market for Europe

- 11.6.3. Artificial Intelligence in Oncology Market for Asia Pacific

- 11.6.4. Artificial Intelligence in Oncology Market for Rest of the World

12. CONCLUSION

- 12.1. Chapter Overview