|

市場調查報告書

商品編碼

1821507

抗體發現市場 - 服務和平台:2035年前的產業趨勢和全球預測 - 抗體發現階段,各方法,性質,各抗體類型,各治療領域,各終端用戶,各地區Antibody Discovery Market - Focus on Services and Platforms: Industry Trends and Global Forecasts, till 2035 - Distribution by Antibody Discovery Step, Method, Nature of, Type of Antibody, Therapeutic Area, End-user and Geographical Regions |

||||||

抗體發現市場:概覽

預計到 2035 年,抗體發現市場規模將從目前的 24 億美元增長至 66 億美元,預測期內複合年增長率達 10.5%。

本市場細分按以下參數細分了市場規模與機會:

抗體發現步驟

- 標靶藥物生成

- 先導化合物篩選

- 先導化合物優化

抗體發現方法

- 基於雜交瘤的方法

- 噬菌體展示文庫方法

- 基因改造動物方法

- 基於酵母展示的方法方法

- 基於單細胞的方法

- 其他

抗體的性質

- 人抗體

- 人體化抗體

- 嵌合抗體

- 鼠標抗體

治療領域

- 腫瘤學的疾病

- 免疫疾病

- 感染疾病領域

- 循環系統疾病

- 神經疾病

- 其他的疾病

抗體類型

- 單株抗體

- 二特異性抗體

- 抗體藥物複合體

- 免疫複合體

- 其他的抗體

終端用戶

- 公司內部部門

- 受託研究機構

地區

- 北美

- 歐洲

- 亞太地區

- 中東·北非

- 南美

抗體發現服務市場成長與趨勢

抗體在辨識和中和外來物質方面發揮著至關重要的作用。由於其特異性高、安全性好等諸多優勢,這些分子已成為極具前景的選擇,尤其是在治療癌症、自體免疫疾病和傳染病方面。抗體目前是最大的生物製劑類別,迄今已有超過80個分子獲得批准,超過200個分子處於臨床前/發現階段。

儘管已獲得多項批准,但在設計、生產和臨床應用的多個階段仍存在各種尚未解決的挑戰。鑑於現代藥物開發的複雜性,許多公司正將外包作為優化研究工作的策略解決方案。這種預期轉變的原因多種多樣,包括縮短研發週期、降低與試驗失敗相關的財務風險以及加速工作流程。目前,約有 125 家公司提供各種抗體發現服務。

人工智慧和機器學習的進步是該領域的關鍵,它們有助於預測抗體-抗原相互作用,並提高先導化合物的鑑定效率。

在這些發展的推動下,抗體發現市場預計將在未來幾年蓬勃發展,惠及眾多持續推動該領域創新的利害關係人。

本報告深入探討了抗體發現市場的現狀,並識別了該行業的潛在成長機會。報告的主要發現包括:

- 目前,全球近 125 家公司聲稱提供客製化服務以支援抗體發現相關活動,其中大多數公司位於北美。

- 相當大比例的服務提供者(88%)提供抗體發現服務,其中57%採用基於文庫的方法來支持治療性抗體的發現。

- 目前,市面上有近265種抗體發現技術,透過加速高特異性抗體的鑑定和開發,徹底改變了抗體發現領域。

- 其中45%支持單株抗體的發現。

- 利害關係人正積極增強現有能力,提升競爭力,以在抗體發現服務領域取得優勢。

- 為了獲得競爭優勢,利害關係人正在積極創新和開發新的抗體發現技術/平台,以支持多種類型抗體的發現。

- 60% 的合作協議是在 2021 年之後簽署的,其中技術/產品授權協議成為最主要的合作模式。

- 由於預期獲得豐厚回報,許多公私投資者自 2020 年以來已投資了相當於 360 億美元的資金。

- 由於對標靶生物製劑和個人化醫療的需求不斷增長,預計到 2035 年,抗體發現市場將以 10.1% 的複合年增長率 (CAGR) 增長。

- 預計採用基於雜交瘤方法的服務提供者將獲得最大的市場機會。按抗體類型劃分,單株抗體細分市場預計將顯著成長。

- 從長遠來看,單株抗體發現平台有望成為主要貢獻者,預計亞太地區將經歷最快的成長。

抗體發現服務市場的主要細分市場

根據抗體發現步驟,抗體發現市場的服務細分市場分為先導化合物優化、先導化合物篩選和標靶化合物發現。目前,先導化合物優化細分市場佔了整體市場佔有率的大部分(61%)。值得注意的是,先導化合物優化能夠篩選出在親和力、穩定性和特異性方面均表現優異的高品質候選抗體,從而提高臨床成功的可能性。

抗體發現服務市場依發現方法分為:基於雜交瘤、基於噬菌體展示文庫、基於基因改造動物、基於酵母展示、單細胞和其他。

目前,基於雜交瘤的方法佔市場主導地位(35%)。其高效性和低複雜度使其在抗體發現領域越來越受歡迎。此外,基於雜交瘤的方法對於開髮用於治療癌症、自體免疫疾病和傳染病的治療性單株抗體至關重要。

依據抗體特性,抗體發現市場服務區隔市場分為人源抗體、人源化抗體、嵌合抗體和鼠源抗體。人源抗體細分市場目前佔全球服務市場的最大佔有率(53%)。人源抗體的諸多優勢,例如較低的免疫原性和單株抗體在人體內的血清半衰期延長,使其佔了較高的市場佔有率。

全球抗體發現服務市場規模依治療領域細分,包括腫瘤學、免疫學、傳染病、心血管疾病、神經系統疾病和其他疾病。目前,腫瘤學細分市場佔市場主導地位(48%)。這是由於全球腫瘤疾病發生率不斷上升,迫切需要開發和生產有效的治療方法,包括基於抗體的治療方法。

依抗體類型細分,全球抗體發現服務市場細分為單株抗體、雙特異性抗體和免疫偶聯物。目前,單株抗體(60%)佔市場主導地位,這一趨勢在未來不太可能改變。這是因為單株抗體具有高度的特異性、一致性和可重複性,使其成為標靶治療的理想選擇。此外,單株抗體已被證明在治療多種疾病方面非常有效,包括癌症、自體免疫疾病和傳染病。

同樣,依抗體類型,全球技術/平台市場細分為單株抗體、雙特異性抗體、抗體-藥物偶聯物和其他抗體。

技術/平台市場將成為預測期內成長最快的細分市場。

依最終用戶細分,抗體發現市場的技術/平台市場細分為兩大不同的終端用戶:內部參與者和合約研究組織。內部製造商細分市場 (98%) 佔最大市場佔有率。這是因為內部公司擁有專業團隊、豐富的內部資源以及對智慧財產權的控制,這使得他們能夠簡化藥物發現流程並保持競爭優勢。

此細分市場揭示了全球服務市場規模按地區分佈的情況,包括北美、歐洲、亞太地區、中東和北非以及拉丁美洲。我們估計,由於大型製藥公司的存在、完善的監管框架以及各種技術進步,北美(50%)今年將佔大部分市場佔有率。同時,亞太地區預計在預測期內將實現13.3%的複合年增長率的健康成長。

同樣,技術/平台市場細分為多個區域,包括北美、歐洲和亞太地區。我們的預測表明,鑑於總部位於北美的技術和平台提供商簽署的技術許可和整合協議數量最多,北美將佔整個市場的大多數佔有率。

此外,預計亞太市場在未來將以更快的速度成長(複合年增長率為9.30%)。

初步研究概述

本研究中提出的觀點和見解受到與市場中多個利害關係人討論的影響。本研究報告也包含與產業利害關係人(按資歷排序)的詳細訪談記錄。

- 美國,小規模企業,執行長兼最高科學負責人

- 德國,小規模企業,執行長兼總經理

- 美國,小規模企業,執行長

- 美國,大企業,原執行長

- 美國,中堅企業,執行長

- 美國,中堅企業,執行長

- 美國,中堅企業,原執行長

- 美國,大企業,原最高科學負責人

- 美國,中堅企業,社長兼最高執行負責人

- 美國,中堅企業,創業者兼技術長

- 美國,中堅企業,創業者兼社長

- 美國,中堅企業,商業服務部門副總統

- 美國,中堅企業,上級副社長

- 加拿大,大企業,共同創立者兼新興科學技術擔當董事

- 印度,小企業,共同成立者兼董事

- 美國,大企業,原網站董事

- 美國,小企業,事業開發管理者

抗體發現服務市場上參與企業案例

- Ablexis

- Abwiz Bio

- Abzena

- Aragen Life Sciences

- BIOTEM

- ChemPartner

- Creative Biolabs

- DetaiBio

- FairJourney Biologics

- Fusion Antibodies

- Genmab

- Harbour BioMed

- Immunome

- ImmunoPrecise Antibodies

- Integral Molecular

- Isogenica

- ProteoGenix

- Syd Labs

- Viva Biotech

- WuXi Biologics

抗體發現服務市場研究報告

- 抗體發現服務市場規模及機會分析:本報告按主要細分市場深入分析了全球抗體發現市場:[A] 抗體發現步驟,[B] 抗體發現方法,[C] 抗體特性,[D] 治療領域,[E] 抗體類型,[F] 地區。

- 抗體發現技術/平台市場:本報告按主要細分市場深入分析了全球抗體發現市場:[A] 抗體類型,[B] 最終用戶類型,[C] 地區。

- 市場模式:基於若干相關參數對參與抗體發現市場的公司進行深入評估,例如 A] 成立年份、[B] 公司規模、[C] 總部位置、[D] 提供的抗體發現服務類型、[E] 支援的抗體發現類型、[F] 抗體發現方法的類型、[G] 使用的動物模型以及 [H] 應用領域。

- 競爭分析:對抗體藥物合約製造商進行全面的競爭分析,考慮因素包括 A] 開發商實力、[B] 產品組合實力和 [C] 產品組合多樣性。

- 技術競爭分析:對抗體發現技術/平台進行全面的競爭分析,考察因素包括 A] 開發商實力、[B] 產品組合實力和 [C] 產品組合多樣性。

- 公司簡介:抗體發現市場主要開發商的詳細簡介,重點關注 A] 公司概況、[B] 財務資訊(如有)、[C] 抗體發現服務組合以及 [D] 近期發展和未來展望。

- 合作關係與合作:基於各種參數,例如 A) 合作年份、[B] 合作類型、[C] 抗體類型、[D] 地區等,對抗體發現市場中達成的各種合作關係與合作進行深入分析。

- 資金與投資分析:基於各種參數,例如 A) 融資年份、[B] 融資類型、[C] 地區等,對該領域報告的總體資金和投資進行深入分析。

目錄

章節I:報告概要

第1章 序文

第2章 調查手法

第3章 市場動態

- 章概要

- 預測調查手法

- 市場評估組成架構

- 預測工具和技巧

- 重要的考慮事項

- 限制事項

第4章 宏觀經濟指標

- 章概要

- 市場動態

- 結論

章節II:定性洞察

第5章 摘要整理

第6章 簡介

- 章概要

- 抗體結構

- 抗體發現的歷史

- 抗體的同型

- 抗體的作用機制

- 抗體的分類

- 單株抗體

- 多株抗體

- 雙特異性抗體

- 抗體的應用

- 結論

第7章 抗體發現:流程與方法

- 章概要

- 抗體發現流程

- 抗體發現方法

- 現有的抗體發現方法的優點和缺點

- 單株抗體的演進

- 結論

章節III:競爭情形

第8章 市場形勢:抗體發現服務供應商

- 章概要

- 抗體發現服務供應商:市場形勢

第9章 市場形勢:抗體發現技術/平台

- 章概要

- 抗體發現技術/平台:市場形勢

- 抗體發現技術/平台供應商的形勢

第10章 企業競爭力分析

- 章概要

- 前提主要的參數

- 調查手法

- Pierre群組概要

- 企業競爭力分析

- 北美設立總公司抗體發現服務供應商

- 歐洲為本部的抗體發現服務供應商

- 亞太地區設立總公司抗體發現服務供應商

第11章 技術競爭力分析

- 章概要

- 前提主要的參數

- 調查手法

- Pierre群組概要

- 技術競爭力分析

- 北美設立總公司企業所提供的抗體發現技術·平台

- 歐洲為本部的企業所提供的抗體發現技術·平台

- 亞太地區設立總公司企業所提供的抗體發現技術/平台

章節IV:企業簡介

第12章 抗體發現服務提供者:北美公司簡介

- 章概要

- Abwiz Bio

- Abzena

- Creative Biolabs

- DetaiBio

- ImmunoPrecise Antibodies

- Integral Molecular

- Syd Labs

第13章

- 章概要

- BIOTEM

- FairJourney Biologics

- Fusion Antibodies

- Proteogenix

第14章 抗體發現服務提供者:亞太地區公司簡介

- 章概要

- Aragen Life Sciences

- ChemPartner

- Viva Biotech

- WuXi Biologics

第15章 抗體發現技術/平台供應商:北美企業簡介

- 章概要

- Ablexis

- Harbour BioMed

- Immunome

第16章 抗體發現技術/平台供應商:歐洲企業簡介

- 章概要

- Genmab

- Isogenica

章節V:市場趨勢

第17章 夥伴關係和合作

- 章概要

- 夥伴關係模式

- 抗體發現服務和平台:夥伴關係和合作

第18章 資金籌措投資分析

- 章概要

- 資金籌措的種類

- 抗體發現服務及平台供應商:資金籌措和投資分析

- 投資摘要

章節VI:市場機會分析

第19章 市場影響分析:促進因素,阻礙因素,機會,課題

第20章 全球抗體發現服務市場

第21章 抗體發現服務市場(抗體發現階段)

第22章 抗體發現服務市場(各抗體發現方法)

第23章 抗體發現服務市場(抗體的性質)

第24章 抗體發現服務市場(各治療領域)

第25章 抗體發現服務市場(各抗體類型)

第26章 抗體發現服務市場(各地區)

第27章 全球抗體發現技術/平台市場

第28章 抗體發現技術/平台市場(各抗體類型)

第29章 抗體發現技術/平台市場(各終端用戶)

第30章 抗體發現技術/平台市場(各地區)

第31章 授權契約結構

第32章 案例:熱門抗體藥物研發流程

- 章概要

- Humira(Adalimumab)

- KEYTRUDA(Pembrolizumab)

- Stelara(Ustekinumab)

- Opdivo(Nivolumab)

- daruzarekkusu(Daratumumab)

第33章 抗體發現的未來的成長機會

章節VII:其他獨家洞察

第34章 結論

第35章 執行洞察

章節VIII:附錄

第36章 附錄I:表資料

第37章 附錄II:企業及組織的一覽

Antibody Discovery Market: Overview

As per Roots Analysis, the antibody discovery market is estimated to grow from USD 2.4 billion in the current year to USD 6.6 billion by 2035, representing a higher CAGR of 10.5% during the forecast period.

The market sizing and opportunity analysis has been segmented across the following parameters:

Antibody Discovery Step

- Hit Generation

- Lead Selection

- Lead Optimization

Antibody Discovery Method

- Hybridoma-based Methods

- Phage Display Library-based Methods

- Transgenic Animal-based Methods

- Yeast Display-based Methods

- Single Cell-based Methods

- Other Methods

Nature of Antibody

- Human Antibodies

- Humanized Antibodies

- Chimeric Antibodies

- Murine Antibodies

Therapeutic Area

- Oncological Disorders

- Immunological Disorders

- Infectious Diseases

- Cardiovascular Disorders

- Neurological Disorders

- Other Disorders

Type of Antibody

- Monoclonal Antibodies

- Bispecific Antibodies

- Antibody Drug Conjugates

- Immunoconjugates

- Other Antibodies

End-user

- In-house Players

- Contract Research Organizations

Geographical Regions

- North America

- Europe

- Asia Pacific

- Middle East and North Africa

- Latin America

Antibody Discovery Services Market: Growth and Trends

Antibodies play a pivotal role in the identification and neutralization of foreign substances. Owing to several beneficial features, such as high specificity, and a favorable safety profile, these molecules have emerged as a promising alternative, particularly for the treatment of cancer, autoimmune diseases, and infectious diseases. It is worth highlighting that, at present, antibodies represent the largest class of biologics, with over 80 molecules approved till date and over 200 molecules in the preclinical / discovery stages.

Despite multiple approvals, various challenges in the domain remain unaddressed across several stages of design, production, and clinical application. Therefore, given the complexities of modern drug development, several companies prefer to outsource as a strategic solution to optimize their research efforts. This expected shift can be attributed to various reasons, such as reduced timelines, lessened financial risks associated with failed trials and accelerated workflows. At present, around 125 players are offering a wide array of antibody discovery services.

This field possesses significant promise for future breakthroughs, wherein advances in artificial intelligence and machine learning is expected to be crucial, facilitating the prediction of antibody-antigen interactions and enhancing the efficiency of lead identification.

Fueled by these developments, the antibody discovery market is expected to progress in the coming years, benefiting multiple stakeholders who have consistently fostered innovation in this field

Antibody discovery market: Key Insights

The report delves into the current state of the antibody discovery market and identifies potential growth opportunities within industry. Some key findings from the report include:

- Presently, close to 125 players across the globe claim to offer customized services in order to support the operations related to antibody discovery; majority of these firms are based in North America.

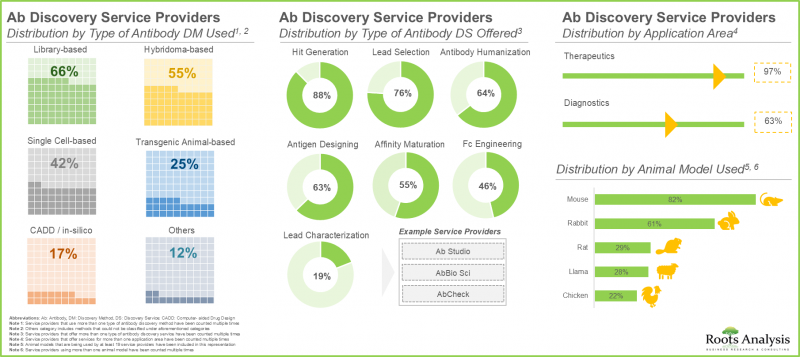

- A relatively large proportion (88%) of the service providers offer hit generation services; of these, 57% employ library-based methods in order to support the discovery of antibodies for different therapeutic purposes.

- Close to 265 antibody discovery technologies are currently available in the market; these have revolutionized the field of antibody discovery by accelerating the identification and development of highly specific antibodies.

- Nearly 60% of the technologies employ library-based methods for antibody discovery; of these, 45% of the technologies support the discovery of monoclonal antibodies.

- Stakeholders are actively enhancing their existing capabilities and strengthening their competencies in order to gain an edge in the antibody discovery services domain.

- In pursuit of gaining a competitive edge, industry stakeholders are actively innovating and developing novel antibody discovery technologies / platforms that can support the discovery of multiple type of antibodies.

- 60% of the partnership deals have been inked post-2021; technology / product licensing agreements have emerged as the most prominent types of partnership models

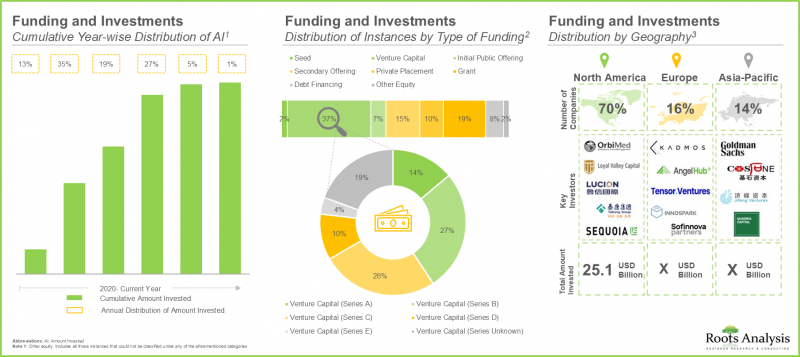

- Foreseeing lucrative returns, many public and private investors have made investments worth USD 36 billion since 2020; of this, 70% of the total amount was raised by players based in North America.

- Given the rising demand for targeted biologics and personalized medicine, the antibody discovery market is anticipated to grow at an annualized rate (CAGR) of 10.1% till 2035

- The market opportunity for service providers using hybridoma-based methods is likely to be the highest; in terms of type of antibody, monoclonal antibodies sub-segment is anticipated to grow substantially.

- In the long term, the antibody discovery platforms for monoclonal antibodies are likely to emerge as the key contributor; Asia-Pacific is anticipated to be the fastest growing region.

Antibody Discovery Services Market: Key Segments

Lead Optimization Segment Captures that Majority of the Market Share

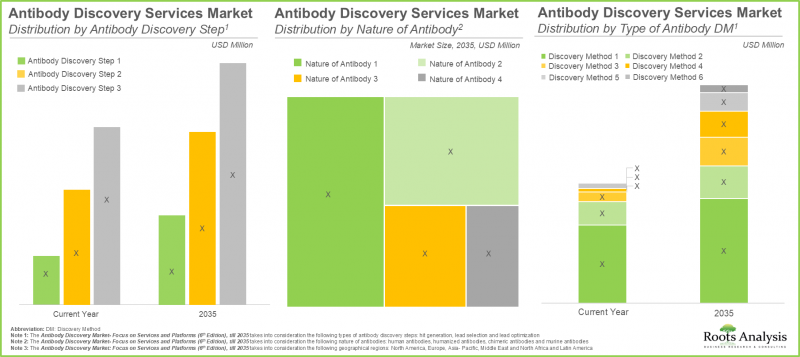

Based on the antibody discovery step, the services segment of antibody discovery market is distributed across lead optimization, lead selection and hit generation. Currently, the lead optimization sub-segment occupies the majority (61%) of the share in the overall market. It is worth highlighting that lead optimization ensures the selection of high-quality antibody candidates in terms of affinity, stability, and specificity, thereby increasing their likelihood of clinical success.

Antibody Discovery Services Segment is leading the Antibody Discovery Market

Based on the discovery method, the services segment of antibody discovery market is segmented into hybridoma-based methods, phage display library-based methods, transgenic animal-based methods, yeast display-based methods, single cell-based methods and other methods.

Presently, the market is dominated by hybridoma-based methods (35%) since the popularity of hybridoma-based methods for the discovery of antibodies has risen, owing to its efficiency and low complexity. Moreover, hybridoma-based methods have been crucial in developing therapeutic monoclonal antibodies used in treatment of diseases, including cancer, autoimmune disorders, and infections.

Based on Nature of Antibody, Human Antibodies Sub-Segment Occupies the Highest Share

Based on the nature of antibody, the services segment of antibody discovery market is segmented into human antibodies, humanized antibodies, chimeric antibodies and murine antibodies. The human antibodies sub-segment occupies the highest share (53%) in the current global services market. Several benefits associated with human antibodies, including reduced immunogenicity and the increased serum half-life of the monoclonal antibodies in humans, contribute to the high market share.

Oncological Disorders Dominate the Current Antibody Discovery Market

The global market value for services segment of antibody discovery market, based on different therapeutic areas, is segmented into oncological disorders, immunological disorders, infectious diseases, cardiovascular disorders, neurological disorders and other disorders. Currently, the market is dominated by oncological disorders sub-segment (48%). This can be attributed to the fact that incidence of oncological disorders has been on the rise globally, necessitating the development and production of effective treatments, including antibody-based therapeutics.

By Type of Antibody, Monoclonal Antibodies are Likely to Dominate the Market During the Forecast Period

Based on the type of antibody, the global services segment of antibody discovery market is segmented into monoclonal antibodies, bispecific antibodies and immunoconjugates. In the current year, the market is dominated by monoclonal antibodies (60%) and the trend is unlikely to change in the future as well. This can be attributed to the fact that monoclonal antibodies offer high specificity, consistency, and reproducibility, which makes them ideal for targeted therapies. In addition, mAbs have proven to be highly effective in treating a range of diseases, including cancer, autoimmune disorders, and infectious diseases.

Similarly, based on the type of antibody, the global technologies / platforms market is segmented into monoclonal antibodies, bispecific antibodies, antibody drug conjugates and other antibodies.

The Technologies / Platforms Market is the Fastest Growing Segment of the During the Forecast Period

In terms of end-user, the global technologies / platforms market segment of antibody discovery market is segmented across different end-users, namely in-house players and contract research organizations. In-house players' sub-segment (98%) occupies the highest market share. This can be attributed to the fact that in-house players mostly have dedicated teams, access to extensive in-house resources, and control over intellectual property, which enables them to streamline the discovery process and maintain competitive advantages.

North America Accounts for the Largest Share of the Market

This segment highlights the distribution of global services market size across geographical regions, such as North America, Europe, Asia-Pacific, Middle East and North Africa, and Latin America. Our estimates suggest that the majority share in the current year is captured by North America (50%) owing to the presence of big pharma players, well-established regulatory framework, and various technological advancements in this region. On the contrary, Asia-Pacific is poised for the healthy growth rate (with a CAGR of 13.3%) during the forecast period.

Likewise, technologies / platforms market is segmented across various geographies, including North America, Europe and Asia-Pacific. Our estimates suggest that, North America is likely to capture the majority of the overall market share driven by maximum number of technology licensing / integration deals inked by technology / platform providers headquartered in this region.

Further, the market in Asia-Pacific is anticipated to increase at a faster pace (CAGR of 9.30%) in the foreseen future.

Primary Research Overview

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders in the market. In addition, the research report features detailed transcripts of interviews held with the industry stakeholders (arranged in decreasing order of seniority level):

- Chief Executive Officer and Chief Scientific Officer, Small Company, US

- Chief Executive Officer and General Manager, Small Company, Germany

- Chief Executive Officer, Small Company, US

- Former Chief Executive Officer, Large Company, US

- Chief Business Officer, Mid-sized Company, US

- Chief Business Officer, Mid-sized Company, US

- Former Chief Business Officer, Small Company, US

- Former Chief Scientific Officer, Large Company, US

- President and Chief Operating Officer, Small Company, US

- Founder and Chief Technology Officer, Small Company, US

- Founder and President, Small Company, US

- Vice President of Commercial Services, Mid-sized Company, US

- Senior Vice President, Small Company, US

- Co-founder and Director of Emerging Science and Technology, Large Company, Canada

- Co-founder and Director, Small Company, India

- Former Site Director, Large Company, US

- Business Development Manager, Small Company, US

Example Players in the Antibody Discovery Services Market

- Ablexis

- Abwiz Bio

- Abzena

- Aragen Life Sciences

- BIOTEM

- ChemPartner

- Creative Biolabs

- DetaiBio

- FairJourney Biologics

- Fusion Antibodies

- Genmab

- Harbour BioMed

- Immunome

- ImmunoPrecise Antibodies

- Integral Molecular

- Isogenica

- ProteoGenix

- Syd Labs

- Viva Biotech

- WuXi Biologics

Antibody Discovery Services Market: Research Coverage

- Antibody Discovery Services Market Sizing and Opportunity Analysis: The report features a thorough analysis of the global antibody discovery market, in terms of the key market segments, namely [A] antibody discovery step [B] type of antibody discovery method, [C] and nature of antibody [D] therapeutic area [E] type of antibody and [F] geographical regions.

- Antibody Discovery Technologies / Platforms Market: The report features a thorough analysis of the global antibody discovery market, in terms of the key market segments, namely [A] type of antibody [B] type of end-user, [C] and geographical regions.

- Market Landscape: An in-depth assessment of the companies involved in antibody discovery market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters, [D] type of antibody discovery service offered, [E] type of antibody discovery supported, [F] type of antibody discovery method, [G] animal model used, [H] application area.

- Company Competitiveness Analysis: A comprehensive competitive analysis of antibody contract manufacturers, examining factors, such as [A] developer strength and [B] portfolio strength and [C] portfolio diversity.

- Technology Competitiveness Analysis: A comprehensive competitive analysis of antibody discovery technologies / platforms, examining factors, such as [A] developer strength and [B] portfolio strength and [C] portfolio diversity.

- Company Profiles: Detailed profiles of key developers engaged in the antibody discovery market, focused on [A] overview of the company, [B] financial information (if available), [C] antibody discovery service portfolio, and [D] recent developments and an informed future outlook.

- Partnerships and Collaborations: An insightful analysis of the various partnerships and collaborations signed in the antibody discovery market, based on various parameters, such as [A] year of partnership [B] type of partnership [C] type of antibody and [D] geography.

- Funding and Investment Analysis: An insightful analysis of the overall funding and investments reported in this domain, based on various parameters, such as [A] year of funding [B] type of funding and [C] geography.

Key Questions Answered in this Report

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Structure of Antibodies

- 6.3. History of Antibody Discovery

- 6.4. Antibody Isotypes

- 6.5. Mechanism of Action of Antibodies

- 6.6. Classification of Antibodies

- 6.6.1. Monoclonal Antibodies

- 6.6.2. Polyclonal Antibodies

- 6.6.3. Bispecific Antibodies

- 6.7. Applications of Antibodies

- 6.8. Concluding Remarks

7. ANTIBODY DISCOVERY: PROCESSES AND METHODS

- 7.1. Chapter Overview

- 7.2. Antibody Discovery Process

- 7.2.1. Target Selection and Validation

- 7.2.2. Hit Generation

- 7.2.3. Lead Selection

- 7.2.4. Lead Optimization

- 7.2.4.1. Humanization

- 7.2.4.2. Affinity Maturation

- 7.2.4.3. Fc Engineering

- 7.2.5. Lead Characterization

- 7.2.6. Candidate Selection

- 7.3. Antibody Discovery Methods

- 7.3.1. Hybridoma Method

- 7.3.2. In Vitro Display Method

- 7.3.2.1. Phage Display Method

- 7.3.2.2. Yeast Display Method

- 7.3.2.3. Ribosomal Display Method

- 7.3.3. Transgenic Animal-based Method

- 7.3.4. Single B Cell Based Method

- 7.4. Advantages and Disadvantages of Existing Antibody Discovery Methods

- 7.5. Evolution of Monoclonal Antibodies

- 7.5.1. Fully Human Monoclonal Antibodies

- 7.6. Concluding Remarks

SECTION III: COMPETITIVE LANDSCAPE

8. MARKET LANDSCAPE: ANTIBODY DISCOVERY SERVICE PROVIDERS

- 8.1. Chapter Overview

- 8.2. Antibody Discovery Service Providers: Market Landscape

- 8.2.1. Analysis by Year of Establishment

- 8.2.2. Analysis by Company Size

- 8.2.3. Analysis by Location of Headquarters

- 8.2.4. Analysis by Type of Antibody Discovery Service Offered

- 8.2.5. Analysis by Type of Antibody Discovery Supported

- 8.2.6. Analysis by Type of Antibody Discovery Method

- 8.2.7. Analysis by Animal Model Used

- 8.2.8. Analysis by Type of Antibody Discovery Method and Type of Antibody Discovery Supported

- 8.2.9. Analysis by Type of Antibody Discovery Service Offered and Location of Headquarters

- 8.2.10. Analysis by Application Area

9. MARKET LANDSCAPE: ANTIBODY DISCOVERY TECHNOLOGIES / PLATFORMS

- 9.1. Chapter Overview

- 9.2. Antibody Discovery Technologies / Platforms: Market Landscape

- 9.2.1. Analysis by Type of Antibody Discovery Method Used

- 9.2.2. Analysis by Type of Antibody Discovery Supported

- 9.2.3. Analysis by Animal Model Used

- 9.2.4. Analysis by Type of Antibody Discovery Method Used and Type of Antibody Discovery Supported

- 9.2.5. Analysis by Type of Antibody Discovery Method and Location of Headquarters of Technology / Platform Providers

- 9.3. Antibody Discovery Technology / Platform Providers Landscape

- 9.3.1. Analysis by Year of Establishment

- 9.3.2. Analysis by Company Size

- 9.3.3. Analysis by Location of Headquarters

- 9.3.4. Most Active Players: Analysis by Number of Technologies

10. COMPANY COMPETITIVENESS ANALYSIS

- 10.1. Chapter Overview

- 10.2. Assumptions and Key Parameters

- 10.3. Methodology

- 10.4. Overview of Peer Groups

- 10.5. Company Competitiveness Analysis

- 10.5.1. Antibody Discovery Service Providers Headquartered in North America

- 10.5.2. Antibody Discovery Service Providers Headquartered in Europe

- 10.5.3. Antibody Discovery Service Providers Headquartered in Asia-Pacific

11. TECHNOLOGY COMPETITIVENESS ANALYSIS

- 11.1. Chapter Overview

- 11.2. Assumptions and Key Parameters

- 11.3. Methodology

- 11.4. Overview of Peer Groups

- 11.5. Technology Competitiveness Analysis

- 11.5.1. Antibody Discovery Technologies / Platforms Provided by Players Headquartered in North America

- 11.5.2. Antibody Discovery Technologies / Platforms Provided by Players Headquartered in Europe

- 11.5.3. Antibody Discovery Technologies / Platforms Provided by Players Headquartered in Asia-Pacific

SECTION IV: COMPANY PROFILES

12. ANTIBODY DISCOVERY SERVICE PROVIDERS: COMPANY PROFILES OF PLAYERS BASED IN NORTH AMERICA

- 12.1. Chapter Overview

- 12.2. Abwiz Bio

- 12.2.1. Company Overview

- 12.2.2. Antibody Discovery Service Portfolio

- 12.2.3. Recent Developments and Future Outlook

- 12.3. Abzena

- 12.3.1. Company Overview

- 12.3.2. Antibody Discovery Service Portfolio

- 12.3.3. Recent Developments and Future Outlook

- 12.4. Creative Biolabs

- 12.4.1. Company Overview

- 12.4.2. Antibody Discovery Service Portfolio

- 12.4.3. Recent Developments and Future Outlook

- 12.5. DetaiBio

- 12.5.1. Company Overview

- 12.5.2. Antibody Discovery Service Portfolio

- 12.5.3. Recent Developments and Future Outlook

- 12.6. ImmunoPrecise Antibodies

- 12.6.1. Company Overview

- 12.6.2. Financial Information

- 12.6.3. Antibody Discovery Service Portfolio

- 12.6.4. Recent Developments and Future Outlook

- 12.7. Integral Molecular

- 12.7.1. Company Overview

- 12.7.2. Antibody Discovery Service Portfolio

- 12.7.3. Recent Developments and Future Outlook

- 12.8. Syd Labs

- 12.8.1. Company Overview

- 12.8.2. Antibody Discovery Service Portfolio

- 12.8.3. Recent Developments and Future outlook

13. ANTIBODY DISCOVERY SERVICE PROVIDERS: COMPANY PROFILES OF PLAYERS BASED IN EUROPE

- 13.1. Chapter Overview

- 13.2. BIOTEM

- 13.2.1. Company Overview

- 13.2.2. Antibody Discovery Service Portfolio

- 13.2.3. Recent Developments and Future Outlook

- 13.3. FairJourney Biologics

- 13.3.1. Company Overview

- 13.3.2. Antibody Discovery Service Portfolio

- 13.3.3. Recent Developments and Future Outlook

- 13.4. Fusion Antibodies

- 13.4.1. Company Overview

- 13.4.2. Financial Information

- 13.4.3. Antibody Discovery Service Portfolio

- 13.4.4. Recent Developments and Future Outlook

- 13.5. Proteogenix

- 13.5.1. Company Overview

- 13.5.2. Antibody Discovery Service Portfolio

- 13.5.3. Recent Developments and Future Outlook

14. ANTIBODY DISCOVERY SERVICE PROVIDERS: COMPANY PROFILES OF PLAYERS BASED IN ASIA-PACIFIC

- 14.1. Chapter Overview

- 14.2. Aragen Life Sciences

- 14.2.1. Company Overview

- 14.2.2. Antibody Discovery Service Portfolio

- 14.2.3. Recent Developments and Future Outlook

- 14.3. ChemPartner

- 14.3.1. Company Overview

- 14.3.2. Antibody Discovery Service Portfolio

- 14.3.3. Recent Developments and Future Outlook

- 14.4. Viva Biotech

- 14.4.1. Company Overview

- 14.4.2. Financial Information

- 14.4.3. Antibody Discovery Service Portfolio

- 14.4.4. Recent Developments and Future Outlook

- 14.5. WuXi Biologics

- 14.5.1. Company Overview

- 14.5.2. Financial Information

- 14.5.3. Antibody Discovery Service Portfolio

- 14.5.4. Recent Developments and Future Outlook

15. ANTIBODY DISCOVERY TECHNOLOGY / PLATFORM PROVIDERS: COMPANY PROFILES OF PLAYERS BASED IN NORTH AMERICA

- 15.1. Chapter Overview

- 15.2. Ablexis

- 15.2.1. Company Overview

- 15.2.2. Antibody Discovery Technology / Platform Portfolio

- 15.2.3. Recent Developments and Future Outlook

- 15.3. Harbour BioMed

- 15.3.1. Company Overview

- 15.3.2. Antibody Discovery Technology / Platform Portfolio

- 15.3.3. Financial Information

- 15.3.4. Recent Developments and Future Outlook

- 15.4. Immunome

- 15.4.1. Company Overview

- 15.4.2. Antibody Discovery Technology / Platform Portfolio

- 15.4.3. Recent Developments and Future Outlook

16. ANTIBODY DISCOVERY TECHNOLOGY / PLATFORM PROVIDERS: COMPANY PROFILES OF PLAYERS BASED IN EUROPE

- 16.1. Chapter Overview

- 16.2. Genmab

- 16.2.1. Company Overview

- 16.2.2. Antibody Discovery Technology / Platform Portfolio

- 16.2.3. Financial Information

- 16.2.4. Recent Developments and Future Outlook

- 16.3. Isogenica

- 16.3.1. Company Overview

- 16.3.2. Antibody Discovery Technology / Platform Portfolio

- 16.3.3. Recent Developments and Future Outlook

SECTION V: MARKET TRENDS

17. PARTNERSHIPS AND COLLABORATIONS

- 17.1. Chapter Overview

- 17.2. Partnership Models

- 17.3. Antibody Discovery Services and Platforms: Partnerships and Collaborations

- 17.3.1. Analysis by Year of Partnership

- 17.3.2. Analysis by Type of Partnership

- 17.3.3. Analysis by Year and Type of Partnership

- 17.3.4. Analysis by Type of Antibody

- 17.3.5. Key Technologies: Analysis by Number of Partnerships

- 17.3.6. Most Active Players: Analysis by Number of Partnerships

- 17.3.7. Analysis by Geography

- 17.3.7.1. Local and International Agreements

- 17.3.7.2. Intracontinental and Intercontinental Agreements

18. FUNDING AND INVESTMENT ANALYSIS

- 18.1. Chapter Overview

- 18.2. Types of Funding

- 18.3. Antibody Discovery Service and Platform Providers: Funding and Investment Analysis

- 18.3.1. Analysis by Year of Funding

- 18.3.1.1. Cumulative Year-wise Trend of Funding Instances

- 18.3.1.2. Cumulative Year-wise Trend of Amount Invested

- 18.3.2. Analysis by Type of Funding

- 18.3.2.1. Analysis by Funding Instances

- 18.3.2.2. Analysis by Amount Invested

- 18.3.3. Analysis by Year and Type of Funding

- 18.3.4. Analysis by Number of Funding Instances and Type of Players

- 18.3.5. Analysis by Type of Player Amount Invested

- 18.3.6. Analysis by Geography

- 18.3.7. Most Active Players: Analysis by Number of Funding Instances

- 18.3.8. Most Active Players: Analysis by Amount Invested

- 18.3.9. Leading Investors: Analysis by Number of Funding Instances

- 18.3.1. Analysis by Year of Funding

- 18.4. Summary of Investments

SECTION VI: MARKET OPPORTUNITY ANALYSIS

19. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 19.1. Chapter Overview

- 19.2. Market Drivers

- 19.3. Market Restraints

- 19.4. Market Opportunities

- 19.5. Market Challenges

- 19.6. Conclusion

20. GLOBAL ANTIBODY DISCOVERY SERVICES MARKET

- 20.1. Chapter Overview

- 20.2. Assumptions and Methodology

- 20.3. Antibody Discovery Services Market, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 20.3.1. Scenario Analysis

- 20.3.1.1. Conservative Scenario

- 20.3.1.2. Optimistic Scenario

- 20.3.1. Scenario Analysis

- 20.4. Key Market Segmentations

21. ANTIBODY DISCOVERY SERVICES MARKET, BY ANTIBODY DISCOVERY STEP

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Antibody Discovery Services Market: Distribution by Antibody Discovery Step

- 21.3.1. Antibody Discovery Services Market for Hit Generation, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 21.3.2. Antibody Discovery Services Market for Lead Selection, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 21.3.3. Antibody Discovery Services Market for Lead Optimization, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 21.4. Data Triangulation and Validation

22. ANTIBODY DISCOVERY SERVICES MARKET, BY TYPE OF ANTIBODY DISCOVERY METHOD

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Antibody Discovery Services Market: Distribution by Type of Antibody Discovery Method

- 22.3.1. Antibody Discovery Services Market for Hybridoma-based Methods, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 22.3.2. Antibody Discovery Services Market for Phage Display Library-based Methods, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 22.3.3. Antibody Discovery Services Market for Transgenic Animal-based Methods, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 22.3.4. Antibody Discovery Services Market for Yeast Display-based Methods, Historical Trends (since 2020) and Forecasted Estimate, (till 2035)

- 22.3.5. Antibody Discovery Services Market for Single Cell-based Methods, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 22.3.6. Antibody Discovery Services Market for Other Methods, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 22.4. Data Triangulation and Validation

23. ANTIBODY DISCOVERY SERVICES MARKET, BY NATURE OF ANTIBODY

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Antibody Discovery Services Market: Distribution by Nature of Antibody

- 23.3.1. Antibody Discovery Services Market for Human Antibodies, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 23.3.2. Antibody Discovery Services Market for Humanized Antibodies, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 23.3.3. Antibody Discovery Services Market for Chimeric Antibodies, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 23.3.4. Antibody Discovery Services Market for Murine Antibodies, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 23.4. Data Triangulation and Validation

24. ANTIBODY DISCOVERY SERVICES MARKET, BY THERAPEUTIC AREA

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Antibody Discovery Services Market: Distribution by Therapeutic Area

- 24.3.1. Antibody Discovery Services Market for Oncological Disorders, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 24.3.2. Antibody Discovery Services Market for Immunological Disorders, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 24.3.3. Antibody Discovery Services Market for Infectious Diseases, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 24.3.4. Antibody Discovery Services Market for Cardiovascular Disorders, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 24.3.5. Antibody Discovery Services Market for Neurological Disorders, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 24.3.6. Antibody Discovery Services Market for Other Disorders, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 24.4. Data Triangulation and Validation

25. ANTIBODY DISCOVERY SERVICES MARKET, BY TYPE OF ANTIBODY

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Antibody Discovery Services Market: Distribution by Type of Antibody

- 25.3.1. Antibody Discovery Services Market for Monoclonal Antibodies, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 25.3.2. Antibody Discovery Services Market for Bispecific Antibodies, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 25.3.3. Antibody Discovery Services Market for Immunoconjugates, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 25.4. Data Triangulation and Validation

26. ANTIBODY DISCOVERY SERVICES MARKET, BY GEOGRAPHICAL REGIONS

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Antibody Discovery Services Market: Distribution by Geographical Regions

- 26.3.1. Antibody Discovery Services Market in North America, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.1.1. Antibody Discovery Services Market in the US, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.1.2. Antibody Discovery Services Market in Canada, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.2. Antibody Discovery Services Market in Europe, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.2.1. Antibody Discovery Services Market in Germany, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.2.2. Antibody Discovery Services Market in the UK, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.2.3. Antibody Discovery Services Market in France, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.2.4. Antibody Discovery Services Market in Italy, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.2.5. Antibody Discovery Services Market in Spain, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.2.6. Antibody Discovery Services Market in Rest of Europe, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.3. Antibody Discovery Services Market in Asia-Pacific, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.3.1. Antibody Discovery Services Market in China, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.3.2. Antibody Discovery Services Market in Japan, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.3.3. Antibody Discovery Services Market in India, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.3.4. Antibody Discovery Services Market in South Korea, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.3.5. Antibody Discovery Services Market in Australia, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.4. Antibody Discovery Services Market in Middle East and North Africa, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.4.1. Antibody Discovery Services Market in Egypt, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.4.2. Antibody Discovery Services Market in Israel, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.4.3. Antibody Discovery Services Market in Saudi Arabia, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.4.4. Antibody Discovery Services Market in Rest of Middle East and North Africa, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.5. Antibody Discovery Services Market in Latin America, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.5.1. Antibody Discovery Services Market in Brazil, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.5.2. Antibody Discovery Services Market in Argentina, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.5.3. Antibody Discovery Services Market in Mexico, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.5.4. Antibody Discovery Services Market in Rest of Latin America, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.3.1. Antibody Discovery Services Market in North America, Historical Trends (since 2020) and Forecasted Estimates (till 2035)

- 26.4. Antibody Discovery Services Market, by Geographical Regions: Market Dynamics Assessment

- 26.4.1. Penetration Growth (P-G) Matrix

- 26.4.2. Market Movement Analysis

- 26.5. Data Triangulation and Validation

27. GLOBAL ANTIBODY DISCOVERY TECHNOLOGIES / PLATFORMS MARKET

- 27.1. Chapter Overview

- 27.2. Assumptions and Methodology

- 27.3. Antibody Discovery Technologies / Platforms Market: Forecasted Estimates, till 2035

- 27.3.1. Scenario Analysis

- 27.3.1.1. Conservative Scenario

- 27.3.1.2. Optimistic Scenario

- 27.3.1. Scenario Analysis

- 27.4. Key Market Segmentations

28. ANTIBODY DISCOVERY TECHNOLOGIES / PLATFORMS MARKET, BY TYPE OF ANTIBODY

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Antibody Discovery Technologies / Platforms Market: Distribution by Type of Antibody

- 28.3.1. Antibody Discovery Technologies / Platforms Market for Monoclonal Antibodies, Forecasted Estimates (till 2035)

- 28.3.2. Antibody Discovery Technologies / Platforms Market for Bispecific Antibodies, Forecasted Estimates (till 2035)

- 28.3.3. Antibody Discovery Technologies / Platforms Market for Antibody Drug Conjugates, Forecasted Estimates (till 2035)

- 28.3.4. Antibody Discovery Technologies / Platforms Market for Other Antibodies, Forecasted Estimates (till 2035)

- 28.4. Data Triangulation and Validation

29. ANTIBODY DISCOVERY TECHNOLOGIES / PLATFORMS MARKET, BY TYPE OF END-USER

- 29.1. Chapter Overview

- 29.2. Key Assumptions and Methodology

- 29.3. Antibody Discovery Technologies / Platforms Market: Distribution by Type of End-User

- 29.3.1. Antibody Discovery Technologies / Platforms Market for In-house, Forecasted Estimates (till 2035)

- 29.3.2. Antibody Discovery Technologies / Platforms Market for Contract Research Organizations, Forecasted Estimates (till 2035)

- 29.4. Data Triangulation and Validation

30. ANTIBODY DISCOVERY TECHNOLOGIES / PLATFORMS MARKET, BY GEOGRAPHICAL REGIONS

- 30.1. Chapter Overview

- 30.2. Key Assumptions and Methodology

- 30.3. Antibody Discovery Technologies / Platforms: Distribution by Geographical Regions

- 30.3.1. Antibody Discovery Technologies / Platforms Market in North America, Forecasted Estimates (till 2035)

- 30.3.1.1. Antibody Discovery Technologies / Platforms Market in the US, Forecasted Estimates (till 2035)

- 30.3.1.2. Antibody Discovery Technologies / Platforms Market in Canada, Forecasted Estimates (till 2035)

- 30.3.2. Antibody Discovery Technologies / Platforms Market in Europe, Forecasted Estimates (till 2035)

- 30.3.2.1. Antibody Discovery Technologies / Platforms Market in Switzerland, Forecasted Estimates (till 2035)

- 30.3.2.2. Antibody Discovery Technologies / Platforms Market in Germany, Forecasted Estimates (till 2035)

- 30.3.2.3. Antibody Discovery Technologies / Platforms Market in the UK, Forecasted Estimates (till 2035)

- 30.3.2.4. Antibody Discovery Technologies / Platforms Market in France, Forecasted Estimates (till 2035)

- 30.3.2.5. Antibody Discovery Technologies / Platforms Market in Rest of Europe, Forecasted Estimates (till 2035)

- 30.3.3. Antibody Discovery Technologies / Platforms Market in Asia-Pacific, Forecasted Estimates (till 2035)

- 30.3.3.1. Antibody Discovery Technologies / Platforms Market in China, Forecasted Estimates (till 2035)

- 30.3.3.2. Antibody Discovery Technologies / Platforms Market in Singapore, Forecasted Estimates (till 2035)

- 30.3.3.3. Antibody Discovery Technologies / Platforms Market in Japan, Forecasted Estimates (till 2035)

- 30.3.3.4. Antibody Discovery Technologies / Platforms Market in South Korea, Forecasted Estimates (till 2035)

- 30.3.1. Antibody Discovery Technologies / Platforms Market in North America, Forecasted Estimates (till 2035)

- 30.4. Market Dynamics Assessment

- 30.4.1. Penetration Growth (P-G) Matrix

- 30.5. Data Triangulation and Validation

31. LICENSING DEAL STRUCTURE

- 31.1. Chapter Overview

- 31.2. Key Parameters

- 31.3. Assumptions and Methodology

- 31.3.1. Overall Cash Flow for Licensee Companies

- 31.3.1.1. Total Expenses Incurred by a Licensee

- 31.3.1.2. Revenues Generated by a Licensee

- 31.3.2. Overall Cash Flow for Licensor

- 31.3.2.1. Total Expenses Incurred by the Licensor

- 31.3.2.2. Revenues by the Licensor

- 31.3.1. Overall Cash Flow for Licensee Companies

- 31.4. Key Analytical Outputs

- 31.4.1. Scenario 1: Variation of Upfront Payments and Milestone Payments

- 31.4.2. Scenario 2: Variation of Upfront Payments and Sales based Royalties

- 31.4.3. Scenario 1: Variation of Milestone Payments and Sales based Royalties

32. CASE IN POINT: DRUG DISCOVERY PROCESSES OF TOP SELLING ANTIBODIES

- 32.1. Chapter Overview

- 32.2. Humira (Adalimumab)

- 32.2.1. Drug Overview

- 32.2.2. Discovery Process and Method

- 32.2.3. Historical Sales

- 32.3. Keytruda (Pembrolizumab)

- 32.3.1. Drug Overview

- 32.3.2. Discovery Process and Method

- 32.3.3. Historical Sales

- 32.4. Stelara (Ustekinumab)

- 32.4.1. Drug Overview

- 32.4.2. Discovery Process and Method

- 32.4.3. Historical Sales

- 32.5. Opdivo (Nivolumab)

- 32.5.1. Drug Overview

- 32.5.2. Discovery Process and Method

- 32.5.3. Historical Sales

- 32.6. Darzalex (Daratumumab)

- 32.6.1. Drug Overview

- 32.6.2. Discovery Process and Method

- 32.6.3. Historical Sales

33. FUTURE GROWTH OPPORTUNITIES IN ANTIBODY DISCOVERY

- 33.1. Chapter Overview

- 33.2. Upcoming Trends in Drug Discovery

- 33.3. Anticipated Shift from Monoclonal Antibodies to Other Novel Antibody Formats

- 33.3.1. Technological Advancements to Overhaul Conventional Antibody Discovery Processes

- 33.3.2. Transition to CADD-based Approaches to Help Achieve Better Operational Efficiencies

- 33.3.3. Rising Demand for Antibody-based Treatment Options for Non-Oncological Indications

- 33.4. Future Growth Opportunities in Emerging Economies

- 33.5. Concluding Remarks

SECTION VII: OTHER EXCLUSIVE INSIGHTS

34. CONCLUDING INSIGHTS

35. EXECUTIVE INSIGHTS

SECTION VIII: APPENDICES

36. APPENDIX I: TABULATED DATA

37. APPENDIX II: LIST OF COMPANIES AND ORGANIZATIONS

List of Tables

- Table 6.1 Features of Different Isotypes of Antibodies

- Table 6.2 Mechanism of Action of Therapeutic Antibodies Against Different Target Classes

- Table 6.3 Differences Between Polyclonal and Monoclonal Antibodies

- Table 7.1 Antibody Discovery Methods: Advantages and Disadvantages

- Table 7.2 List of Approved Monoclonal Antibodies

- Table 7.3 Approval Timeline: Fully Human Monoclonal Antibodies

- Table 8.1 Antibody Discovery Service Providers: Information on Year of Establishment, Company Size and Location of Headquarters

- Table 8.2 Antibody Discovery Service Providers: Information on Type of Antibody Discovery Service Offered

- Table 8.3 Antibody Discovery Service Providers: Information on Type of Antibody Discovery Supported

- Table 8.4 Antibody Discovery Service Providers: Information on Type of Antibody Discovery Method Used

- Table 8.5 Antibody Discovery Service Providers: Information on Animal Model Used

- Table 8.6 Antibody Discovery Service Providers: Information on Application Area

- Table 9.1 List of Antibody Discovery Technologies / Platforms

- Table 9.2 Antibody Discovery Technologies / Platforms: Information on Antibody Discovery Method Used

- Table 9.3 Antibody Discovery Technologies / Platforms: Information on Type of Antibody Discovery Supported

- Table 9.4 Antibody Discovery Technologies / Platforms: Information on Animal Model Used

- Table 9.5 Antibody Discovery Technology / Platform Providers: Information on Year of Establishment, Company Size and Location of Headquarters

- Table 10.1 Company Competitiveness Scores Allotted to Service Providers based in North America (Peer Group I)

- Table 10.2 Company Competitiveness Scores Allotted to Service Providers based in Europe (Peer Group II)

- Table 10.3 Company Competitiveness Scores Allotted to Service Providers based in Asia-Pacific (Peer Group III)

- Table 11.1 Technology Competitiveness Analysis: Antibody Discovery Technologies / Platforms Provided by Players Headquartered in North America (Peer Group I)

- Table 11.2 Company Competitiveness Scores Allotted to Service Providers based in Europe (Peer Group II)

- Table 11.3 Company Competitiveness Scores Allotted to Service Providers based in Asia-Pacific (Peer Group III)

- Table 12.1 Antibody Discovery Service Providers in North America: List of Companies Profiled

- Table 12.2 Abwiz Bio: Company Snapshot

- Table 12.3 Abwiz Bio: Antibody Discovery Service Portfolio

- Table 12.4 Abzena: Company Snapshot

- Table 12.5 Abzena: Antibody Discovery Service Portfolio

- Table 12.6 Abzena: Recent Developments and Future Outlook

- Table 12.7 Creative Biolabs: Company Snapshot

- Table 12.8 Creative Biolabs: Antibody Discovery Service Portfolio

- Table 12.9 Creative Biolabs: Recent Developments and Future Outlook

- Table 12.10 DetaiBio: Company Snapshot

- Table 12.11 DetaiBio: Antibody Discovery Service Portfolio

- Table 12.12 DetaiBio: Recent Developments and Future Outlook

- Table 12.13 ImmunoPrecise Antibodies: Company Snapshot

- Table 12.14 ImmunoPrecise Antibodies: Antibody Discovery Service Portfolio

- Table 12.15 ImmunoPrecise Antibodies: Recent Developments and Future Outlook

- Table 12.16 Integral Molecular: Company Snapshot

- Table 12.17 Integral Molecular: Antibody Discovery Service Portfolio

- Table 12.18 Integral Molecular: Recent Developments and Future Outlook

- Table 12.19 Syd Labs: Company Snapshot

- Table 12.20 Syd Labs: Antibody Discovery Service Portfolio

- Table 13.1 Antibody Discovery Service Providers in Europe: List of Companies Profiled

- Table 13.2 BIOTEM: Company Snapshot

- Table 13.3 BIOTEM: Antibody Discovery Service Portfolio

- Table 13.4 BIOTEM: Recent Developments and Future Outlook

- Table 13.5 FairJourney Biologics: Company Snapshot

- Table 13.6 FairJourney Biologics: Antibody Discovery Service Portfolio

- Table 13.7 FairJourney Biologics: Recent Developments and Future Outlook

- Table 13.8 Fusion Antibodies: Company Snapshot

- Table 13.9 Fusion Antibodies: Antibody Discovery Service Portfolio

- Table 13.10 Fusion Antibodies: Recent Developments and Future Outlook

- Table 13.11 ProteoGenix: Company Snapshot

- Table 13.12 ProteoGenix: Antibody Discovery Service Portfolio

- Table 13.13 ProteoGenix: Recent Developments and Future Outlook

- Table 14.1 Antibody Discovery Service Providers in Asia-Pacific: List of Companies Profiled

- Table 14.2 Aragen Life Sciences: Company Snapshot

- Table 14.3 Aragen Life Sciences: Antibody Discovery Service Portfolio

- Table 14.4 Aragen Life Sciences: Recent Developments and Future Outlook

- Table 14.5 ChemPartner: Company Snapshot

- Table 14.6 ChemPartner: Antibody Discovery Service Portfolio

- Table 14.7 ChemPartner: Recent Developments and Future Outlook

- Table 14.8 Viva Biotech: Company Snapshot

- Table 14.9 Viva Biotech: Antibody Discovery Service Portfolio

- Table 14.10 Viva Biotech: Recent Developments and Future Outlook

- Table 14.11 WuXi Biologics: Company Snapshot

- Table 14.12 WuXi Biologics: Antibody Discovery Service Portfolio

- Table 14.13 WuXi Biologics: Recent Developments and Future Outlook

- Table 15.1 Antibody Discovery Technology / Platform Providers in North America: List of Companies Profiled

- Table 15.2 Ablexis: Company Snapshot

- Table 15.3 Ablexis: Antibody Discovery Platform Portfolio

- Table 15.4 Ablexis: Recent Developments and Future Outlook

- Table 15.5 Harbour BioMed: Company Snapshot

- Table 15.6 Harbour BioMed: Antibody Discovery Platform Portfolio

- Table 15.7 Harbour BioMed: Recent Development and Future Outlook

- Table 15.8 Immunome: Company Snapshot

- Table 15.9 Immunome: Antibody Discovery Platform Portfolio

- Table 15.10 Immunome: Recent Developments and Future Outlook

- Table 16.1 Antibody Discovery Technology / Platform Providers in Europe: List of Companies Profiled

- Table 16.2 Genmab: Company Snapshot

- Table 16.3 Genmab: Antibody Discovery Platform Portfolio

- Table 16.4 Genmab: Recent Developments and Future Outlook

- Table 16.5 Isogenica: Company Snapshot

- Table 16.6 Isogenica: Antibody Discovery Platform Portfolio

- Table 16.7 Isogenica: Recent Developments and Future Outlook

- Table 17.1 Antibody Discovery Services and Platforms Market: List of Partnerships and Collaborations, Since 2021

- Table 17.2 Partnerships and Collaborations: Information on Type of Agreement

- Table 18.1 Antibody Discovery Services and Platforms Market: List of Funding and Investments, Since 2021

- Table 27.1 Antibody Discovery Technologies Market: Average Upfront Payment and Average Milestone Payment, Since 2021 (USD Million)

- Table 27.2 Licensing Deals: Tranches of Milestone Payments

- Table 31.1 Scenario 1: Multiple Cases of Varying Upfront and Milestone Payments

- Table 31.2 Scenario 2: Multiple Cases of Varying Upfront Payment and Sales based Royalties

- Table 31.3 Multiple Cases of Varying Milestone Payment and Sales based Royalties

- Table 32.1 Top Seven Selling Therapeutic Antibodies, 2024

- Table 33.1 Antibody Discovery Services and Platform Providers Headquartered in Asia-Pacific

- Table 35.1 Antibody Solutions: Company Snapshot

- Table 35.2 Adimab: Company Snapshot

- Table 35.3 ImmunoPrecise Antibodies: Company Snapshot

- Table 35.4 Abveris Antibody: Company Snapshot

- Table 35.5 Nidus BioSciences: Company Snapshot

- Table 35.6 AvantGen: Company Snapshot

- Table 35.7 Single Cell Technology: Company Snapshot

- Table 35.8 Distributed Bio (acquired by Charles River): Company Snapshot

- Table 35.9 AbCellera: Company Snapshot

- Table 35.10 AbGenics Life Sciences: Company Snapshot

- Table 35.11 CDI Laboratories: Company Snapshot

- Table 35.12 AP Biosciences: Company Snapshot

- Table 35.13 YUMAB: Company Snapshot

- Table 35.14 Antibody Solutions: Company Snapshot

- Table 35.15 Ligand Pharmaceuticals: Company Snapshot

- Table 35.16 LakePharma (acquired by Curia): Company Snapshot

- Table 36.1 Antibody Discovery Service Providers: Distribution by Year of Establishment

- Table 36.2 Antibody Discovery Service Providers: Distribution by Company Size

- Table 36.3 Antibody Discovery Service Providers: Distribution by Location of Headquarters (Region)

- Table 36.4 Antibody Discovery Service Providers: Distribution by Location of Headquarters (Country)

- Table 36.5 Antibody Discovery Service Providers: Distribution by Type of Antibody Discovery Service Offered

- Table 36.6 Antibody Discovery Service Providers: Distribution by Type of Antibody Discovery Supported

- Table 36.7 Antibody Discovery Service Providers: Distribution by Type of Antibody Discovery Method Used

- Table 36.8 Antibody Discovery Service Providers: Distribution by Animal Model Used

- Table 36.9 Antibody Discovery Service Providers: Distribution by Type of Antibody Discovery Method Used and Type of Antibody Discovery Supported

- Table 36.10 Antibody Discovery Service Providers: Distribution by Type of Antibody Discovery Service Offered and Location of Headquarters

- Table 36.11 Antibody Discovery Service Providers: Distribution by Application Area

- Table 36.12 Antibody Discovery Technologies / Platforms: Distribution by Type of Antibody Discovery Method Used

- Table 36.13 Antibody Discovery Technologies / Platforms: Distribution by Type of Antibody Discovery Supported

- Table 36.14 Antibody Discovery Technologies / Platforms: Distribution by Animal Model Used

- Table 36.15 Antibody Discovery Technologies / Platforms: Distribution by Antibody Discovery Method Used and Type of Antibody Discovery Supported

- Table 36.16 Antibody Discovery Technologies / Platforms: Distribution by Type of Antibody Discovery Method and Location of Headquarters of the Technology / Platform Provider

- Table 36.17 Antibody Discovery Technology / Platform Providers: Distribution by Year of Establishment

- Table 36.18 Antibody Discovery Technology / Platform Providers: Distribution by Company Size

- Table 36.19 Antibody Discovery Technology / Platform Providers: Distribution by Location of Headquarters (Region)

- Table 36.20 Antibody Discovery Technology / Platform Providers: Distribution by Location of Headquarters (Country)

- Table 36.21 Most Active Players: Distribution by Number of Technologies / Platforms

- Table 36.22 ImmunoPrecise Antibodies: Consolidated Financial Details (CAD Million), Since 2022

- Table 36.23 Fusion Antibodies: Business Segment-wise Revenues and Consolidated Financial Details (GBP Million), Since 2021

- Table 36.24 Viva Biotech: Consolidated Financial Details (RMB Billion), Since 2021

- Table 36.25 WuXi Biologics: Business Segment-wise Revenues and Consolidated Financial Details (RMB Billion), Since 2021

- Table 36.26 Genmab: Consolidated Financial Details (DKK Billion), Since 2021

- Table 36.27 Harbour BioMed: Consolidated Financial Details (USD Million), FY 2021-H1 FY 2024

- Table 36.28 Partnerships and Collaborations: Cumulative Year-wise Trend, Since 2021

- Table 36.29 Partnerships and Collaborations: Distribution by Type of Partnership

- Table 36.30 Partnerships and Collaborations: Distribution by Year and Type of Partnership, Since 2021

- Table 36.31 Partnerships and Collaborations: Distribution by Type of Antibody

- Table 36.32 Key Technologies: Distribution by Number of Partnerships

- Table 36.33 Most Active Players: Distribution by Number of Partnerships

- Table 36.34 Partnerships and Collaborations: Distribution by Country

- Table 36.35 Partnerships and Collaborations: Distribution by Region

- Table 36.36 Funding and Investment Analysis: Cumulative Year-wise Trend, Since 2020

- Table 36.37 Funding and Investment Analysis: Cumulative Year-wise Trend of Amount Invested, Since 2020 (USD Million)

- Table 36.38 Funding and Investment Analysis: Distribution of Funding Instances by Type of Funding

- Table 36.39 Funding and Investment Analysis: Distribution of Amount Invested by Type of Funding (USD Million)

- Table 36.40 Funding and Investment Analysis: Distribution by Year and Type of Funding, Since 2020

- Table 36.41 Funding and Investment Analysis: Distribution by Number of Funding Instances and Type of Player

- Table 36.42 Funding and Investment Analysis: Distribution by Type of Player and Amount Invested

- Table 36.43 Funding and Investment Analysis: Distribution by Geography

- Table 36.44 Most Active Players: Distribution by Number of Funding Instances

- Table 36.45 Most Active Players: Distribution by Amount Invested (USD Million)

- Table 36.46 Leading Investors: Distribution by Number of Funding Instances

- Table 36.47 Global Antibody Discovery Services Market, Historical Trends (since 2020) and Forecasted Estimates (till 2035): Base Scenario (USD Million)

- Table 36.48 Global Antibody Discovery Services Market, Forecasted Estimates (till 2035): Conservative Scenario (USD Million)

- Table 36.49 Global Antibody Discovery Services Market, Forecasted Estimates (till 2035): Optimistic Scenario (USD Million)

- Table 36.50 Global Antibody Discovery Services Market: Distribution by Type of Antibody Discovery Step

- Table 36.51 Antibody Discovery Services Market for Hit Generation: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.52 Antibody Discovery Services Market for Lead Selection: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.53 Antibody Discovery Services Market for Lead Optimization; Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.54 Global Antibody Discovery Services Market: Distribution by Type of Antibody Discovery Method

- Table 36.55 Antibody Discovery Services Market for Hybridoma-based Methods: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.56 Antibody Discovery Services Market for Phage Display-based Methods: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.57 Antibody Discovery Services Market for Transgenic Animal-based Methods: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.58 Antibody Discovery Services Market for Yeast Display-based Methods; Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.59 Antibody Discovery Services Market for Single Cell-based Methods: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.60 Antibody Discovery Services Market for Other Methods: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.61 Global Antibody Discovery Services Market: Distribution by Nature of Antibody

- Table 36.62 Antibody Discovery Services Market for Human Antibodies: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.63 Antibody Discovery Services Market for Humanized Antibodies: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.64 Antibody Discovery Services Market for Chimeric Antibodies: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.65 Antibody Discovery Services Market for Murine Antibodies: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.66 Global Antibody Discovery Services Market: Distribution by Therapeutic Area

- Table 36.67 Antibody Discovery Services Market for Oncological Disorders: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.68 Antibody Discovery Services Market for Immunological Disorders: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.69 Antibody Discovery Services Market for Infectious Diseases: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.70 Antibody Discovery Services Market for Cardiovascular Disorders: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.71 Antibody Discovery Services Market for Neurological Disorders: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.72 Antibody Discovery Services Market for Other Disorders: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.73 Antibody Discovery Services Market: Distribution by Type of Antibody

- Table 36.74 Antibody Discovery Services Market for Monoclonal Antibodies: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.75 Antibody Discovery Services Market for Bispecific Antibodies: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.76 Antibody Discovery Services Market for Immunoconjugates: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.77 Antibody Discovery Services Market: Distribution by Geographical Regions

- Table 36.78 Antibody Discovery Services Market in North America: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.79 Antibody Discovery Services Market in the US: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.80 Antibody Discovery Services Market in Canada: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.81 Antibody Discovery Services Market in Europe: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.82 Antibody Discovery Services Market in Germany: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.83 Antibody Discovery Services Market in the UK: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.84 Antibody Discovery Services Market in France: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.85 Antibody Discovery Services Market in Italy: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.86 Antibody Discovery Services Market in Spain: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.87 Antibody Discovery Services Market in the Rest of Europe: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.88 Antibody Discovery Services Market in Asia-Pacific: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.89 Antibody Discovery Services Market in China: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.90 Antibody Discovery Services Market in Japan: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.91 Antibody Discovery Services Market in India: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.92 Antibody Discovery Services Market in South Korea: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.93 Antibody Discovery Services Market in Australia: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.94 Antibody Discovery Services Market in Middle East and North Africa: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.95 Antibody Discovery Services Market in Egypt: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.96 Antibody Discovery Services Market in Israel: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.97 Antibody Discovery Services Market in Saudi Arabia: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.98 Antibody Discovery Services Market in the Rest of Middle East and North Africa: Historical Trends (since 2020) and Forecasted Estimates (till 2035) (USD Million)

- Table 36.99 Antibody Discovery Services Market in Latin America: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.100 Antibody Discovery Services Market in Brazil: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)

- Table 36.101 Antibody Discovery Services Market in Argentina: Historical Trends (since 2020) and Forecasted Estimates (till 2035), Conservative, Base and Optimistic Scenarios (USD Million)