|

市場調查報告書

商品編碼

2073658

德國暖通空調市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Germany HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

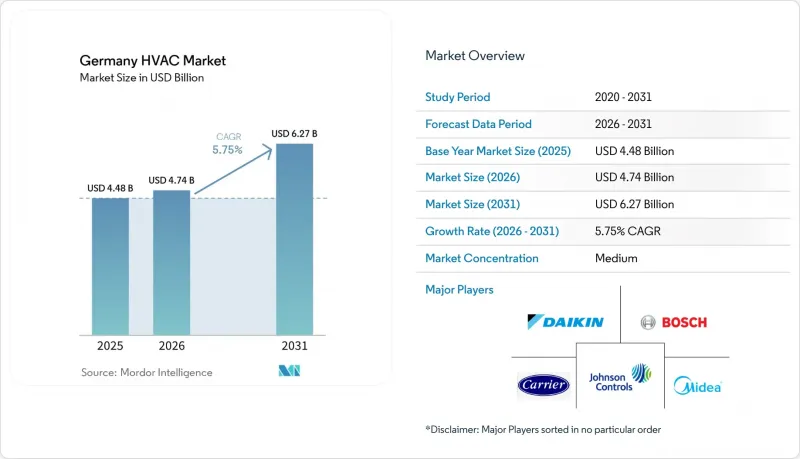

據 Mordor Intelligence 稱,2025 年德國 HVAC 市值為 44.8 億美元,預計到 2031 年將達到 62.7 億美元,而 2026 年為 47.4 億美元,預測期(2026-2031 年)的複合年成長率為 5.75%。

本報告按組件(暖通空調設備、暖通空調服務)、最終用戶行業(住宅、商業、工業、公共/機構)、部署類型(新建、維修)和地區(北部、南部、東部、西部、中部)進行細分。市場預測以美元計價。

德國暖通空調市場趨勢與洞察

根據《建築能源法》促進電氣化

2024年頒布的《建築能源法》規定,所有新建暖氣系統必須至少65%的能源來自可再生能源。這項立法加速了德國向熱泵的轉型,2024年近七成新建住宅計畫都採用了熱泵。該法規還創造了可預測的維修需求,因為石化燃料系統可以運作到其經濟壽命結束,但必須在2045年之前被受監管的替代方案取代。超過1萬個市政當局正在製定區域供熱計劃,優先考慮聯網熱泵和冷水區域供熱網路。這些措施共同確保了德國暖通空調市場的永續需求。

熱泵在新住宅領域的普及

自2024年以來,隨著系統總成本年減12%,而天然氣價格居高不下,熱泵的普及率大幅提升。空氣源熱泵因其初始投資低、選址簡便,佔新裝機量的78%,而地源熱泵則在對噪音敏感或空間受限的項目中得到應用。同時,用於提高熱泵效率的蓄熱系統、智慧溫控器以及建築圍護維修也在不斷發展。安裝人員正不斷提升其在冷媒處理、試運行和數位化控制方面的專業技能,從而強化了德國暖通空調市場的服務導向特徵。

熟練安裝技術人員短缺

到2024年,約有6萬個暖通空調相關職缺,學徒訓練課程的註冊人數在五年內下降了23%。由於熱泵的推廣應用需要額外的技能,例如電氣佈線、冷媒管理和數位化試運行,這給住宅和小規模商業項目帶來了瓶頸。由於培訓中心集中在都市區,農村地區受到的影響最為嚴重。為了彌補這一缺口,大金等製造商建立了大規模培訓基地,並部署了流動培訓中心,前往服務不足的地區進行培訓。

細分市場分析

預計2025年,德國暖通空調設備市場規模將達32.1億美元,佔總營收的71.75%。受消費者對合規性和長期成本節約的需求推動,僅熱泵的年銷量預計將成長超過34%。同時,由於《建築能源法》對天然氣使用前景的不確定性,鍋爐銷量下降了28%。變冷劑流量(VRF)系統因其能夠逐區控制溫度,在辦公大樓和零售場所的市場佔有率正在擴大。

服務收入成長最為顯著,預計複合年成長率將達到7.02%。複雜的試運行、遠端監控和預測性維護是推動支出成長的主要因素,其成本在整個生命週期中往往超過設備的初始成本。商業建築能源管理專案的平均成本在4.5萬歐元至6.5萬歐元(4.8萬美元至6.9萬美元)之間,約為標準預防性保養合約成本的三倍。隨著熱泵的日益普及,專業的洩漏測試和符合氟化氣體法規的合規性檢查正成為持續的收入來源,進一步深化了德國暖通空調市場的服務領域。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 建築和維修活動的增加將提振需求。

- 透過《建築能源法》(GEG)的目標促進電氣化

- 熱泵在新住宅領域迅速普及。

- 智慧暖通空調和建築自動化維修市場的成長

- 熱浪期間,對能夠抵禦氣候變遷的空調的需求激增。

- 企業對淨零排放的承諾正在推動商用暖通空調系統的升級。

- 市場限制因素

- 節能系統的初始成本較高

- 熟練的暖通空調安裝人員和技術人員短缺

- 關於補貼是否繼續以及GEG計畫時間表的政策不確定性。

- 關鍵零件(壓縮機、電子元件)供應鏈的波動

- 產業價值鏈分析

- 波特五力分析

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 按組件

- 暖通空調設備

- 加熱設備

- 熱泵

- 鍋爐

- 散熱器

- 冷卻設備

- 空調

- 冷卻器

- 可變冷媒流量系統

- 通風設備

- 空氣調節機

- 能源回收通風系統

- 加熱設備

- 暖通空調服務

- 安裝

- 維護/修理

- 能源管理和建築自動化

- 暖通空調設備

- 按最終用戶行業分類

- 住宅

- 商業

- 產業

- 公共機構

- 按實現類型

- 新建工程

- 改裝

- 按地區

- 北

- 南

- 東方

- 西方

- 中心

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Carrier Corporation

- Robert Bosch GmbH

- Midea Group Co. Ltd

- Johnson Controls International PLC

- Daikin Industries Ltd

- Systemair AB

- LG Electronics Inc.

- Mitsubishi Electric Hydronics And IT Cooling Systems SpA

- FlaktGroup Holding GmbH

- Danfoss A/S

- Vaillant Group

- Viessmann Climate Solutions SE

- Stiebel Eltron GmbH & Co. KG

- NIBE Industrier AB

- BDR Thermea Group BV

- Panasonic Holdings Corporation

- Trane Technologies plc

- Fujitsu General Limited

- Gree Electric Appliances Inc. of Zhuhai

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany HVAC market size was valued at USD 4.48 billion in 2025 and estimated to grow from USD 4.74 billion in 2026 to reach USD 6.27 billion by 2031, at a CAGR of 5.75% during the forecast period (2026-2031).

This report is Segmented by Component (HVAC Equipment, HVAC Services), End-User Industry (Residential, Commercial, Industrial, Public and Institutional), Implementation Type (New Construction, Retrofit), and Geography (North, South, East, West, Central). The Market Forecasts are Provided in Terms of Value (USD).

Germany HVAC Market Trends and Insights

Building Energy Act Electrification Push

The Building Energy Act took effect in 2024, obligating every new heating system to source at least 65% of its energy from renewables. Enforcement triggered a rapid shift toward heat pumps in Germany, which powered nearly seven in ten new residential projects in 2024. The rule also created a predictable retrofit pipeline because fossil-fuel systems may operate until their economic end of life, but must be replaced with compliant alternatives by 2045. More than 10,000 municipalities are drafting local heat plans that favor networked heat pumps and low-temperature district grids. Together, these measures lock in sustained demand across the Germany HVAC market.

Heat Pump Uptake in New-Build Residential Segment

Heat pump penetration skyrocketed after 2024 as total system cost dropped 12% year over year while gas prices stayed elevated. Air-source units claim 78% of new installations because of their lower capex and easier siting, whereas ground-source models serve noise-sensitive or space-constrained projects. The transition fuels parallel growth in thermal storage, smart thermostats, and envelope upgrades that maximize heat-pump efficiency. Contractors deepen specialization in refrigerant handling, commissioning, and digital controls, reinforcing the service orientation of the Germany HVAC market.

Skilled Installer Shortage

Roughly 60,000 HVAC positions were vacant in 2024, and apprenticeship enrollment fell 23% in five years. Heat pumps demand additional competencies in electrical wiring, refrigerant management, and digital commissioning, creating bottlenecks in residential and small-commercial projects. Rural districts feel the pinch most acutely because training centers cluster in urban areas. To bridge the gap, manufacturers such as Daikin opened large training campuses and rolled out mobile academies that travel to underserved regions.

Other drivers and restraints analyzed in the detailed report include:

- Smart HVAC and Building-Automation Retrofits

- Corporate Net-Zero Commitments Boosting Commercial Upgrades

- Supply-Chain Volatility for Key Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Germany HVAC market size for equipment stood at USD 3.21 billion in 2025, equal to 71.75% of total revenue. Heat pumps alone added more than 34% annual unit growth as consumers chased compliance and long-term savings. Boilers slipped 28% because gas options face an uncertain future under the Building Energy Act. Variable refrigerant flow systems won a greater share in offices and retail centers owing to zone-specific temperature control.

Service income recorded the highest trajectory at a 7.02% forecast CAGR. Complex commissioning, remote monitoring, and predictive maintenance drive spending that frequently exceeds original equipment cost over the life cycle. Energy-management projects in commercial buildings average EUR 45,000 to 65,000 (USD 48,000 to 69,000), roughly triple a standard preventive-maintenance contract. As heat-pump density grows, specialized leak testing and F-gas compliance checks become recurring revenue streams, further deepening the service dimension of the Germany HVAC market.

Complete Report Scope:

- By Component

- HVAC Equipment

- Heating Equipment

- Heat Pumps

- Boilers

- Radiators

- Cooling Equipment

- Air Conditioners

- Chillers

- Variable Refrigerant Flow Systems

- Ventilation Equipment

- Air Handling Units

- Energy Recovery Ventilators

- Heating Equipment

- HVAC Services

- Installation

- Maintenance and Repair

- Energy Management and Building Automation

- HVAC Equipment

- By End-User Industry

- Residential

- Commercial

- Industrial

- Public and Institutional

- By Implementation Type

- New Construction

- Retrofit

- By Region

- North

- South

- East

- West

- Central

List of Companies Covered in this Report:

- Carrier Corporation

- Robert Bosch GmbH

- Midea Group Co. Ltd

- Johnson Controls International PLC

- Daikin Industries Ltd

- Systemair AB

- LG Electronics Inc.

- Mitsubishi Electric Hydronics And IT Cooling Systems S.p.A.

- FlaktGroup Holding GmbH

- Danfoss A/S

- Vaillant Group

- Viessmann Climate Solutions SE

- Stiebel Eltron GmbH & Co. KG

- NIBE Industrier AB

- BDR Thermea Group B.V.

- Panasonic Holdings Corporation

- Trane Technologies plc

- Fujitsu General Limited

- Gree Electric Appliances Inc. of Zhuhai

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Construction and Retrofit Activity to Aid Demand

- 4.2.2 Electrification Push via Building Energy Act (GEG) Targets

- 4.2.3 Rapid Uptake of Heat Pumps in New-Build Residential Segment

- 4.2.4 Growth of Smart HVAC and Building Automation Retrofits

- 4.2.5 Surge in Climate-Resilient Cooling Demand During Heatwaves

- 4.2.6 Corporate Net-Zero Commitments Boosting Commercial HVAC Upgrades

- 4.3 Market Restraints

- 4.3.1 High Initial Cost of Energy Efficient Systems

- 4.3.2 Shortage of Skilled HVAC Installers and Technicians

- 4.3.3 Policy Uncertainty Around Subsidy Continuity and GEG Timelines

- 4.3.4 Supply Chain Volatility for Key Components (Compressors, Electronics)

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 HVAC Equipment

- 5.1.1.1 Heating Equipment

- 5.1.1.1.1 Heat Pumps

- 5.1.1.1.2 Boilers

- 5.1.1.1.3 Radiators

- 5.1.1.2 Cooling Equipment

- 5.1.1.2.1 Air Conditioners

- 5.1.1.2.2 Chillers

- 5.1.1.2.3 Variable Refrigerant Flow Systems

- 5.1.1.3 Ventilation Equipment

- 5.1.1.3.1 Air Handling Units

- 5.1.1.3.2 Energy Recovery Ventilators

- 5.1.1.1 Heating Equipment

- 5.1.2 HVAC Services

- 5.1.2.1 Installation

- 5.1.2.2 Maintenance and Repair

- 5.1.2.3 Energy Management and Building Automation

- 5.1.1 HVAC Equipment

- 5.2 By End-User Industry

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Public and Institutional

- 5.3 By Implementation Type

- 5.3.1 New Construction

- 5.3.2 Retrofit

- 5.4 By Region

- 5.4.1 North

- 5.4.2 South

- 5.4.3 East

- 5.4.4 West

- 5.4.5 Central

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Carrier Corporation

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Midea Group Co. Ltd

- 6.4.4 Johnson Controls International PLC

- 6.4.5 Daikin Industries Ltd

- 6.4.6 Systemair AB

- 6.4.7 LG Electronics Inc.

- 6.4.8 Mitsubishi Electric Hydronics And IT Cooling Systems S.p.A.

- 6.4.9 FlaktGroup Holding GmbH

- 6.4.10 Danfoss A/S

- 6.4.11 Vaillant Group

- 6.4.12 Viessmann Climate Solutions SE

- 6.4.13 Stiebel Eltron GmbH & Co. KG

- 6.4.14 NIBE Industrier AB

- 6.4.15 BDR Thermea Group B.V.

- 6.4.16 Panasonic Holdings Corporation

- 6.4.17 Trane Technologies plc

- 6.4.18 Fujitsu General Limited

- 6.4.19 Gree Electric Appliances Inc. of Zhuhai

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

暖通空調系統市場:2026-2032年全球市場預測(依設備類型、設備配置、最終用途、通路及安裝類型分類)

暖通空調系統市場:2026-2032年全球市場預測(依設備類型、設備配置、最終用途、通路及安裝類型分類) 測試、調整和平衡服務市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、最終用途、地區和競爭對手分類,2021-2031 年

測試、調整和平衡服務市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、最終用途、地區和競爭對手分類,2021-2031 年 暖通空調幫浦市場規模、佔有率和成長分析:按泵浦類型、應用、容量、技術、終端用戶產業、分銷管道和地區分類-2026-2033年產業預測

暖通空調幫浦市場規模、佔有率和成長分析:按泵浦類型、應用、容量、技術、終端用戶產業、分銷管道和地區分類-2026-2033年產業預測 空調和通風系統市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)

空調和通風系統市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年) 暖氣片市場規模、佔有率和成長分析:按產品類型、材質、應用和地區分類-2026-2033年產業預測

暖氣片市場規模、佔有率和成長分析:按產品類型、材質、應用和地區分類-2026-2033年產業預測 2026-2030年全球工業暖通空調市場

2026-2030年全球工業暖通空調市場 2026-2030年全球暖氣、通風和空調(HVAC)售後市場

2026-2030年全球暖氣、通風和空調(HVAC)售後市場 HVAC市場商機、成長要素、產業趨勢分析及2026-2035年預測。暖通空調租賃設備市場:按設備類型、租賃期限、動力來源和最終用戶分類-2026-2032年全球預測

HVAC市場商機、成長要素、產業趨勢分析及2026-2035年預測。暖通空調租賃設備市場:按設備類型、租賃期限、動力來源和最終用戶分類-2026-2032年全球預測 2026年全球氫動力攜帶式可攜式空調市場報告

2026年全球氫動力攜帶式可攜式空調市場報告