|

市場調查報告書

商品編碼

2073655

亞太地區資料中心電力市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

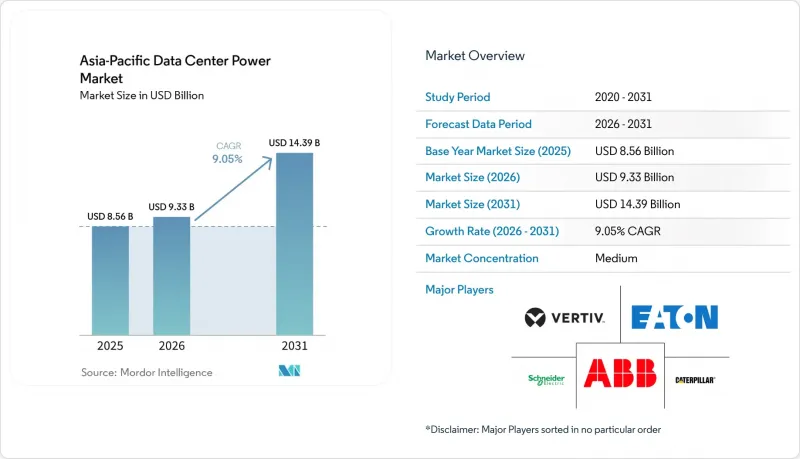

據 Mordor Intelligence 稱,亞太地區資料中心電力市場在 2025 年的價值為 85.6 億美元,預計到 2031 年將從 2026 年的 93.3 億美元成長到 143.9 億美元,在預測期(2026-2031 年成長率)內的複合年成長率為 9.05%。

本報告按組件(電氣解決方案和服務)、資料中心類型(超大規模資料中心業者中心/雲端服務供應商、主機服務供應商等)、資料中心規模(小規模資料中心、中型資料中心、大型資料中心等)、等級(Tier I 和 Tier II、Tier III、Tier IV)以及國家/地區進行細分。市場預測以美元 (USD) 計價。

亞太地區資料中心電力市場趨勢及洞察。

興建超大規模和人工智慧主導的巨型園區

如今,人工智慧訓練叢集每個機架需要 40-50 千瓦的電力,是先前部署所需電力的五倍以上。這需要對配電拓撲結構和冗餘方案進行徹底的重新設計。寬能隙功率半導體(例如碳化矽 (SiC))正在使新型機房的液冷成為標準配置,以降低轉換損耗並保持熱穩定性(橡樹嶺國家實驗室)。像新加坡電信的榕樹園二期這樣的項目,正在採用抗震母線槽和機架級液冷歧管,以應對未來不斷成長的人工智慧負載。這些系統整合了電池,用於提供持續供電、平滑電網瞬態,並實現更快速的負載階躍變化而無需啟動發電機。隨著租戶對人工智慧就緒容量的需求不斷成長,這種連鎖反應正在提高整個託管設施的規格標準。

政府對數位經濟和數據主權的獎勵

中國和印度的政策強制要求資料居住國內,這要求雲端服務供應商運作本地超大規模園區,並升級其配電基礎設施以滿足更高的可用性需求。在新加坡,一項與Equinix合作的公私合營調查計畫已投資400萬美元,用於開發針對熱帶運作環境的永續電力原型。東協框架鼓勵整合可再生能源,預計2030年,再生能源可滿足資料中心30%的能源需求。馬來西亞和越南的獎勵計畫為安裝現場太陽能發電和高效能UPS系統的設施提供補貼。隨著相關法規制定明確的採購計劃,開關設備和儲能設備的採購量正在增加,促進了可預測供應鏈的擴展。

高效率電力系統的初始資本投資

先進的UPS和碳化矽(SiC)轉換器比傳統設備貴40%,這對資金有限的中小型供應商構成了障礙。液冷系統的實施需要工廠預製的匯流排和泵浦歧管,這增加了安裝的複雜性和前置作業時間。在新興市場,平均機架負載約為8kW,營運商通常會推遲升級,直到客戶需求出現。雖然能源即服務(EaaS)合約等資金籌措機制正在逐漸普及,但其應用並不均衡,限制了最高效架構的快速推廣。

細分市場分析

至2025年,UPS系統將佔據亞太地區資料中心電力市場31.65%的收入佔有率,凸顯其在保障運作數位服務運作方面發揮的關鍵作用。鋰離子電池和碳化矽(SiC)動力傳動系統的應用,使得UPS的線上效率超過96%,儘管單位成本較高,但營運成本卻得以降低。隨著整合式UPS和電池模組的出現,組件配置也在發生變化,這些模組縮小了面積,簡化了維護。智慧型PDU是成長最快的細分市場,複合年成長率達10.3%,它整合了每個輸出口的功率計量功能,並利用這些數據透過人工智慧分析最佳化工作負載配置,從而降低閒置功率容量。雖然發電機仍然是重要的備用電源選擇,但燃料電池原型正作為試點項目受到永續性的超大規模資料中心業者資料中心營運商的關注。

外部壓力,例如電價波動,正在加速電池能源儲存系統既能提供電力保障,又能降低按需付費。開關設備的創新重點在於電弧閃光安全和遠距離診斷,從而減少現場維護次數。在技術人員稀缺且運作接受度嚴格的邊緣環境中,遠端配電盤的部署日益增加。亞太地區資料中心電力產業也反映出現代電網日益複雜,隨著營運商擴大將基於數位雙胞胎技術的預測性維護外包給原始設備製造商 (OEM),業務收益正在成長。

透過整合企業需求並利用規模經濟,託管服務供應商預計到 2025 年將佔據亞太資料中心電力市場 53.85% 的佔有率。他們的經營模式支援大規模多租戶機房,這些機房採用模組化的 2-3 兆瓦電源模組,實現了電力設計的標準化,從而縮短了建造時間。同時,在主權雲端指令的推動下,超大規模雲端服務供應商正以 10.05% 的複合年成長率快速擴張,這些指令促使全球平台進行在地化建置。這些資料中心整合了高密度人工智慧叢集,需要晶片直接液冷和專用的 400 伏特交流母線槽,而傳統的託管佈局難以滿足這些需求。

企業正在採用混合架構,在本地維護對延遲敏感的工作負載,同時從託管和超大規模平台租用突發容量。 5G 基地台周圍的邊緣節點數量正在迅速成長,這需要緊湊而可靠的電源架,並且這些電源架的設計理念共用與大型設施保持一致。因此,供應商正在建立涵蓋千瓦級邊緣機架到 150 兆瓦超大規模資料中心的產品組合,從而促進亞太地區資料中心電源市場的跨領域技術轉移。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 超大規模和人工智慧主導的巨型園區建設

- 政府對數位經濟和數據主權的獎勵

- 雲/5G流量的激增正在推高功率密度。

- 高電費推動了對高效能UPS和PDU的需求。

- 電網連接延遲正在推動現場微電網的普及。

- 企業為實現100%可再生能源(現場太陽能發電和電池儲能系統)所採取的舉措

- 市場限制因素

- 高效率電力系統的初始資本投資

- 亞太地區一級樞紐城市的電網和土地限制

- 柴油價格波動推高了發電機的運作成本。

- 液冷式電源設備安裝方面技術純熟勞工短缺。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 投資分析

第5章 市場規模與成長預測

- 按組件

- 電氣解決方案

- UPS系統

- 發電機

- 柴油發電機

- 瓦斯發電機

- 氫燃料電池發電機

- 配電單元

- 切換裝置

- 傳輸開關

- 遠端電源面板

- 能源儲存系統

- 服務

- 安裝和試運行

- 維護和支援

- 培訓和諮詢

- 電氣解決方案

- 依資料中心類型

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 託管服務提供者

- 企業和邊緣資料中心

- 按資料中心規模

- 小規模資料中心

- 中型資料中心

- 大型資料中心

- 超大型資料中心

- 超大型資料中心

- 層級類型

- 一級和二級

- Tier III

- Tier IV

- 國家

- 澳洲

- 中國

- 印度

- 印尼

- 菲律賓

- 新加坡

- 馬來西亞

- 日本

- 紐西蘭

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ABB

- Schneider Electric

- Vertiv

- Eaton

- Huawei Digital Power

- Caterpillar

- Cummins

- Rolls-Royce Power Systems(MTU)

- Delta Electronics

- Legrand

- Mitsubishi Electric

- Socomec

- Piller Power Systems

- Rittal

- Kohler Power

- Cisco(DCIM and Smart-UPS integration)

- Fujitsu(facility services)

- AEG Power Solutions

- Tripp Lite

- Generac

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific data center power market size was valued at USD 8.56 billion in 2025 and estimated to grow from USD 9.33 billion in 2026 to reach USD 14.39 billion by 2031, at a CAGR of 9.05% during the forecast period (2026-2031).

This report is Segmented by Component (Electrical Solutions and Services), Data Center Type (Hyperscaler/Cloud Service Providers, Colocation Providers, and More), Data Center Size (Small Size Data Centers, Medium Size Data Centers, Large Size Data Centers and More), Tier Type (Tier I and II, Tier III, Tier IV) and by Country. The Market Forecasts are Provided in Terms of Value (USD)

Asia-Pacific Data Center Power Market Trends and Insights

Hyperscale & AI-led Mega-Campus Build-out

AI training clusters now demand 40-50 kW per rack, more than five times traditional deployments, forcing total redesigns of distribution topologies and redundancy schemes. Wide-bandgap power semiconductors such as silicon carbide reduce conversion losses, while liquid cooling becomes standard in new halls to maintain thermal stability, Oak Ridge National Laboratory. Projects like Singtel's Banyan Park II in Singapore specify seismic-resilient busways and rack-level liquid manifolds to future-proof against higher AI loads. These systems integrate battery storage for ride-through support, smoothing grid transients, and enabling more aggressive load step changes without generator starts. The cascading effect raises specification levels across colocation builds as tenants request AI-ready capacity.

Government Digital-Economy & Data-Sovereignty Incentives

Policies in China and India require domestic data residency, obliging cloud providers to commission local hyperscale campuses and upgrade power distribution for higher availability tiers. Singapore's public-private research program with Equinix funds USD 4 million in sustainable power prototypes targeting tropical operating conditions. ASEAN frameworks encourage renewable integration that could meet 30% of data-center demand by 2030. Incentive schemes in Malaysia and Vietnam grant tariff rebates for facilities that deploy on-site solar and high-efficiency UPS. As regulation sets clear procurement timelines, volume commitments for switchgear and energy storage rise, supporting predictable supply-chain scaling.

Up-front Capex for High-Efficiency Power Systems

Advanced UPS and silicon-carbide converters cost up to 40% more than legacy equipment, a hurdle for smaller providers with constrained balance sheets. Liquid-cooling integration demands factory-prefabricated busbar and pump manifolds, raising installation complexity and lead times. In emerging economies where average rack loads still hover near 8 kW, operators often delay upgrades until customer demand materializes. Financing mechanisms such as energy-as-a-service contracts are beginning to spread, but adoption remains uneven, limiting near-term penetration of the most efficient architectures.

Other drivers and restraints analyzed in the detailed report include:

- Cloud/5G Traffic Surge Elevating Power Density

- High Electricity Tariffs Boosting Demand for Efficient UPS & PDUs

- Grid & Land Constraints in Tier-1 APAC Hubs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UPS systems held the largest 31.65% revenue share in 2025 within the Asia-Pacific data center power market, underscoring their role in safeguarding always-on digital services. Adoption of lithium-ion batteries and silicon-carbide power trains pushes online efficiency above 96%, trimming operating expenditures despite higher unit prices. The component mix is changing as integrated UPS-battery modules reduce footprint and simplify maintenance. Intelligent PDUs, the fastest-growing sub-segment with a 10.3% CAGR, embed per-outlet metering that feeds AI analytics for workload placement, reducing stranded power capacity. Generators retain critical backup status but fuel-cell prototypes are gaining pilot traction among sustainability-focused hyperscalers.

External pressures from electricity-price volatility accelerate the deployment of battery energy storage that doubles as ride-through support and demand-charge mitigation. Switchgear advances concentrate on arc-flash safety and remote diagnostics that lower truck rolls. Remote power panels rise in edge deployments where technicians are scarce and uptime tolerance is low. Service revenue grows as operators contract OEMs for predictive maintenance tied to digital twins, reflecting the rising complexity of modern power trains across the Asia-Pacific data center power industry.

Colocation operators commanded 53.85% of the Asia-Pacific data center power market in 2025 by aggregating enterprise demand and leveraging economies of scale. Their business model supports large multitenant halls where modular 2-3 MW blocks standardize power design and shorten build schedules. Hyperscale cloud providers, however, are expanding at 10.05% CAGR as sovereign-cloud mandates drive local build commitments from global platforms. These sites integrate high-density AI clusters, necessitating direct-to-chip liquid cooling and dedicated 400 VAC busways that traditional colocation layouts rarely accommodate.

Enterprises adopt hybrid architectures, retaining latency-sensitive workloads on-premises while renting burst capacity from colo and hyperscale platforms. Edge nodes proliferate near 5G towers, requiring compact yet highly reliable power shelves that share design DNA with large facilities. Consequently, solutions vendors tailor portfolios that span kilowatt-class edge racks to 150 MW hyperscale farms, reinforcing cross-segment technology transfer within the Asia-Pacific data center power market.

Complete Report Scope:

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

- By Country

- Australia

- China

- India

- Indonesia

- Philippines

- Singapore

- Malaysia

- Japan

- New Zealand

- Other Asia-Pacific Countries

List of Companies Covered in this Report:

- ABB

- Schneider Electric

- Vertiv

- Eaton

- Huawei Digital Power

- Caterpillar

- Cummins

- Rolls-Royce Power Systems (MTU)

- Delta Electronics

- Legrand

- Mitsubishi Electric

- Socomec

- Piller Power Systems

- Rittal

- Kohler Power

- Cisco (DCIM and Smart-UPS integration)

- Fujitsu (facility services)

- AEG Power Solutions

- Tripp Lite

- Generac

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale and AI-led mega-campus build-out

- 4.2.2 Government digital-economy and data-sovereignty incentives

- 4.2.3 Cloud/5G traffic surge elevating power density

- 4.2.4 High electricity tariffs boosting demand for efficient UPS and PDUs

- 4.2.5 Grid-connection delays driving onsite micro-grids

- 4.2.6 Corporate 100 %-renewable commitments (on-site solar and BESS)

- 4.3 Market Restraints

- 4.3.1 Up-front capex for high-efficiency power systems

- 4.3.2 Grid and land constraints in Tier-1 APAC hubs

- 4.3.3 Diesel-price volatility inflating generator OPEX

- 4.3.4 Skilled-labour gap for liquid-cooling power installs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Electrical Solutions

- 5.1.1.1 UPS Systems

- 5.1.1.2 Generators

- 5.1.1.2.1 Diesel Generators

- 5.1.1.2.2 Gas Generators

- 5.1.1.2.3 Hydrogen Fuel-cell Generators

- 5.1.1.3 Power Distribution Units

- 5.1.1.4 Switchgear

- 5.1.1.5 Transfer Switches

- 5.1.1.6 Remote Power Panels

- 5.1.1.7 Energy-storage Systems

- 5.1.2 Service

- 5.1.2.1 Installation and Commissioning

- 5.1.2.2 Maintenance and Support

- 5.1.2.3 Training and Consulting

- 5.1.1 Electrical Solutions

- 5.2 By Data Center Type

- 5.2.1 Hyperscaler/Cloud Service Providers

- 5.2.2 Colocation Providers

- 5.2.3 Enterprise and Edge Data Center

- 5.3 By Data Center Size

- 5.3.1 Small Size Data Centers

- 5.3.2 Medium Size Data Centers

- 5.3.3 Large Size Data Centers

- 5.3.4 Massive Size Data Centers

- 5.3.5 Mega Size Data Centers

- 5.4 By Tier Level

- 5.4.1 Tier I and II

- 5.4.2 Tier III

- 5.4.3 Tier IV

- 5.5 By Country

- 5.5.1 Australia

- 5.5.2 China

- 5.5.3 India

- 5.5.4 Indonesia

- 5.5.5 Philippines

- 5.5.6 Singapore

- 5.5.7 Malaysia

- 5.5.8 Japan

- 5.5.9 New Zealand

- 5.5.10 Other Asia-Pacific Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB

- 6.4.2 Schneider Electric

- 6.4.3 Vertiv

- 6.4.4 Eaton

- 6.4.5 Huawei Digital Power

- 6.4.6 Caterpillar

- 6.4.7 Cummins

- 6.4.8 Rolls-Royce Power Systems (MTU)

- 6.4.9 Delta Electronics

- 6.4.10 Legrand

- 6.4.11 Mitsubishi Electric

- 6.4.12 Socomec

- 6.4.13 Piller Power Systems

- 6.4.14 Rittal

- 6.4.15 Kohler Power

- 6.4.16 Cisco (DCIM and Smart-UPS integration)

- 6.4.17 Fujitsu (facility services)

- 6.4.18 AEG Power Solutions

- 6.4.19 Tripp Lite

- 6.4.20 Generac

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

美國資料中心電力:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

美國資料中心電力:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 資料中心電力基礎設施市場機會、成長促進因素、產業趨勢分析及2026-2035年預測

資料中心電力基礎設施市場機會、成長促進因素、產業趨勢分析及2026-2035年預測 資料中心電源市場:按組件、最終用戶、資料中心規模、產業和地區分類

資料中心電源市場:按組件、最終用戶、資料中心規模、產業和地區分類 資料中心電源市場:按組件類型、層級、資料中心類型和行業分類 - 全球市場預測(2026-2032 年)

資料中心電源市場:按組件類型、層級、資料中心類型和行業分類 - 全球市場預測(2026-2032 年) 資料中心電源市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案、交付模式

資料中心電源市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、解決方案、交付模式 2026年全球資料中心電力市場報告2026年全球資料中心電源管理市場報告伺服器電源市場:依產品類型、組件、額定功率、外形規格、應用、最終用戶和通路分類-2026-2030年全球預測資料中心以AC-DC電源市場:按組件、電源類型、冗餘方式和應用分類-2026-2032年全球預測資料中心電源系統氮化鎵市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、形式、材料類型、裝置及部署方式分類

2026年全球資料中心電力市場報告2026年全球資料中心電源管理市場報告伺服器電源市場:依產品類型、組件、額定功率、外形規格、應用、最終用戶和通路分類-2026-2030年全球預測資料中心以AC-DC電源市場:按組件、電源類型、冗餘方式和應用分類-2026-2032年全球預測資料中心電源系統氮化鎵市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、形式、材料類型、裝置及部署方式分類