|

市場調查報告書

商品編碼

2073629

北美電池管理系統:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Battery Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

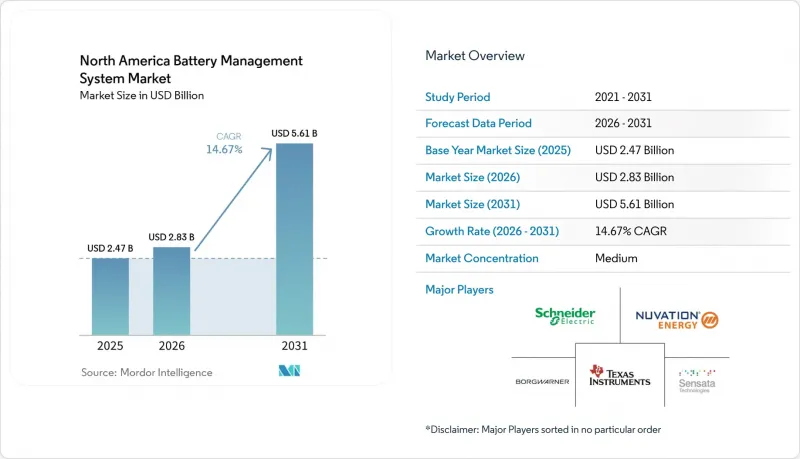

根據 Mordor Intelligence 預測,北美電池管理系統 (BMS) 市場規模將從 2025 年的 24.7 億美元和 2026 年的 28.3 億美元成長到 2031 年的 56.1 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 14.4.7%。

本報告按電池類型(鋰離子電池、鉛酸電池、鎳氫電池、液流電池、全固體)、拓撲結構(集中式、分散式、模組化、混合式)、組件(硬體、軟體)、電壓(低壓、中壓、高壓)、應用領域(汽車、固定式儲能、家用電子電器、工業/UPS等)和地區通訊(美國、加拿大地區)和墨西哥地區通訊。預測值以美元(USD)計價。

北美電池管理系統市場趨勢與洞察

加速推廣電動車和零排放法規

北美電池管理系統市場的電動車政策正從直接銷售壓力轉向購買支援和基礎設施建設。 2026年2月,加拿大恢復了高達5,000加元(約3,600美元)的電動車購買獎勵,並同時投資15億加元(約11億美元)用於充電基礎建設。此類需求驅動通常會帶來更穩定的車輛更換週期,並長期支撐對電池管理系統的持續需求。在美國,與汽車零件組成相關的關稅也促使汽車製造商進一步實現電動車平台和電池組的本地化組裝。這些協同效應正在推動電動車部署量的成長,並使越來越多的車輛在北美電池管理系統市場中接受先進的監控、溫度控管和品質保證分析。

聯邦和州政府的儲能獎勵

能源儲存獎勵仍然是北美電池管理系統市場成長的最顯著驅動力之一。 2026年啟動的項目,如果符合國內採購比例和勞動力條件要求,將有資格獲得高達50%的投資稅額扣抵。此外,聯邦實體成本(FEOC)回收規則使得採購決策更加謹慎,因為禁止向外國實體付款可能會危及資產使用壽命期間的初始稅收優惠。這增強了美國本土供應商(例如Nuvation Energy)的地位,該公司在美國和加拿大生產符合UL 1973認證的G5平台。加拿大各省政府的計畫也正在擴大對電錶支架的需求,而符合UL 1973和UL 9540標準仍然是北美電池管理系統市場採購決策的關鍵因素。

因熱失控而進行的安全召回

雖然安全召回會在短期內對電動車的普及造成聲譽壓力,但它們也推動了北美電池管理系統市場對更強大的控制邏輯的需求。 2025年10月,編號25V655的召回事件影響了美國19,077輛日產聆風(Nissan Leaf)汽車,原因是3級充電過程中存在過熱風險,這與鋰沉積物以及高充電條件下的控制不足有關。此類事件通常會促使原始設備製造商(OEM)和供應商加強對感測、熱建模和檢驗的投入。短期來看,召回事件可能會減緩消費者接受電動車的速度,並降低新車安裝速度。此外,符合ISO 26262和UL 2580標準會增加成本和開發時間,使規模較小的參與企業更難進入市場。

細分市場分析

到2025年,鋰離子電池將佔電池類型細分市場的68.4%,並繼續保持其在北美電池管理系統市場當前需求中的中心地位。這一地位反映了電動車平台的標準化、成熟的供應鏈以及基於鋰離子電池特性而累積的成熟軟體模型。此外,在已部署的系統中,擁有液態電解質電池荷電狀態(SOC)、均衡控制和熱行為模型成熟經驗的供應商將更具優勢。這些優勢表明,即使採購規則和新的化學成分開始改變發展計劃,鋰離子電池在短期內仍將在汽車和儲能項目中保持其主導地位。

預計到2031年,固態電池的電池管理系統市場將以31.8%的複合年成長率成長,成為北美電池管理系統市場中成長最快的電池類型轉型。固體電解質需要不同的感測方法,傳統的庫侖計數法和開路電壓法對其電阻特性而言並不可靠,這促使供應商儘早進入該領域。鉛酸電池、鎳基電池和液流電池仍在工業UPS、混合動力傳動系統和多小時儲能等有限應用中使用,但其作為平台的勢頭遠不及固態電池。 IEC 62619和ISO 26262標準的早期演算法認證將推高認證成本,但隨著固態電池專案進入量產階段,也將為供應商設定更高的轉型門檻。

預計到2025年,分散式拓樸結構將佔該細分市場39.3%的佔有率,複合年成長率(CAGR)為21.1%。這在北美電池管理系統市場的主要設計中實屬罕見。電力公司青睞這種架構,因為它能抑制故障傳播並支援模組化擴展。隨著買家越來越重視系統隔離性、彈性和故障發生時的部分運作,這一趨勢正在進一步加強。此外,該設計還有助於降低大規模儲能資產的保險和營運風險,因為單一故障可能會對昂貴的設備造成影響。

由於集中式拓樸結構面積小,且在車輛安全法規下易於通過型式認證,因此仍適用於許多汽車專案。模組化系統在800V電動車電池組和改造後的儲能系統中越來越受歡迎,因為它們可以根據特定應用場景更有效地調整通道數量。博格華納的模組化電池管理系統(BMS)平台展示了汽車零件供應商如何將這種柔軟性轉化為乘用車和商用車專案的跨平台優勢。混合式設計也正在興起,以滿足客戶對集中控制的低成本和分散式感測的容錯能力的雙重需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速推廣電動車和零排放法規

- 聯邦和州政府的儲能獎勵

- 降低鋰離子電池的成本

- 電力公司主導的V2G 示範實驗需要複雜的建築管理系統 (BMS)。

- 寒冷氣候溫度控管新創公司(加拿大)

- 雲端整合BaaS收入模式

- 市場限制因素

- 因熱失控而進行的安全召回

- 對導入細胞的依賴性

- 墨西哥的功能安全實驗室非常少。

- 與SoC演算法相關的專利相互交織

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 投資和資金籌措趨勢

第5章 市場規模與成長預測

- 依電池類型

- 鋰離子

- 鉛酸

- 鎳基

- 液流電池

- 固態電池

- 拓樸

- 集中

- 去中心化

- 模組化的

- 混合

- 按組件

- 硬體

- 軟體

- 按電壓範圍

- 低電壓(36伏特或以下)

- 中壓(36-60伏特)

- 高電壓(60伏特或更高)

- 透過使用

- 車

- 固定式儲能

- 家用電子產品

- 工業和通訊用UPS

- 醫療器材

- 航太/海洋

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介{包括全球概覽、市場概覽、關鍵細分市場、現有財務資訊、策略資訊、主要公司的市場排名和佔有率、產品和服務以及近期發展動態}

- Texas Instruments Inc.

- Sensata Technologies Inc.

- BorgWarner Inc.

- Nuvation Energy

- Eberspaecher Vecture Inc.

- Schneider Electric SE

- Johnson Controls plc

- Analog Devices Inc.

- STMicroelectronics NV

- Continental AG

- Renesas Electronics Corp.

- Panasonic Corp.

- Leclanche SA

- Navitas Systems

- Cummins Inc.

- Lithium Balance A/S

- LG Energy Solution

- ION Energy

- Romeo Power Inc.

- Ewert Energy Systems Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america battery management system market size is projected to expand from USD 2.47 billion in 2025 and USD 2.83 billion in 2026 to USD 5.61 billion by 2031, registering a CAGR of 14.67% between 2026 and 2031.

This report is Segmented by Battery Type (Li-Ion, Lead-Acid, Nickel, Flow, Solid-State), Topology (Centralized, Distributed, Modular, Hybrid), Component (Hardware, Software), Voltage (Low, Medium, High), Application (Automotive, Stationary Storage, Consumer Electronics, Industrial/Telecom UPS, and More), Geography (United States, Canada, Mexico). Forecasts are in Terms of Value (USD).

North America Battery Management System Market Trends and Insights

Accelerating EV Penetration & Zero-Emission Mandates

EV policy in the North America battery management system market is moving from direct sales pressure toward purchase support and infrastructure buildout. Canada reinstated EV purchase incentives of up to CAD 5,000 (USD 3,600) in February 2026 and paired that decision with CAD 1.5 billion (USD 1.1 billion) for charging infrastructure. This kind of demand pull usually produces steadier vehicle replacement cycles, which supports repeat BMS demand over a longer period. In the United States, tariffs tied to vehicle content are also pushing automakers to localize more EV platforms and pack assembly. The combined effect is a larger installed EV base and a wider addressable fleet for advanced monitoring, thermal management, and warranty analytics in the North America battery management system market.

Federal/Provincial Energy-Storage Incentives

Energy-storage incentives remain one of the clearest growth supports for the North America battery management system market. Projects that begin construction in 2026 can qualify for investment tax credits of up to 50% when domestic content and labor conditions are met. FEOC recapture rules also make sourcing decisions more sensitive because payments to prohibited foreign entities can jeopardize the original tax benefit over the life of the asset. That is improving the position of domestic suppliers such as Nuvation Energy, whose UL 1973-certified G5 platform is manufactured in the United States and Canada. Provincial programs in Canada are also building behind-the-meter demand and keeping UL 1973 and UL 9540 compliance at the center of procurement decisions in the North America battery management system market.

Safety Recalls From Thermal Runaway

Safety recalls are raising demand for stronger control logic in the North America battery management system market, even though they also create short-term reputational pressure on EV adoption. In October 2025, recall number 25V655 covered 19,077 Nissan LEAF units in the United States because rapid overheating risk during Level 3 charging was linked to lithium deposits and weak control under high charge conditions. Events like this often push OEMs and suppliers to spend more on sensing, thermal models, and validation. The near-term problem is that recall headlines can slow consumer adoption and reduce the pace of new vehicle installations. Compliance with ISO 26262 and UL 2580 also adds cost and engineering time, which makes entry harder for smaller participants.

Other drivers and restraints analyzed in the detailed report include:

- Declining Li-Ion Battery Costs

- Utility-Led V2G Pilots Need Advanced BMS

- Dependence On Imported Cells

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion held 68.4% of the battery type segment in 2025, which kept it at the center of current demand in the North America battery management system market. That position reflects EV platform standardization, mature supply chains, and software models already trained around lithium-ion behavior. The installed base also favors suppliers with proven state-of-charge, balancing, and thermal models for liquid-electrolyte cells. These advantages should keep lithium-ion dominant in near-term vehicle and storage programs, even as sourcing rules and new chemistries begin to change development plans.

Solid-state battery management systems are forecast to grow at a 31.8% CAGR through 2031, making this the fastest-moving battery type shift in the North America battery management system market. Suppliers are engaging early because solid electrolytes need different sensing approaches, and conventional Coulomb-counting and open-circuit voltage methods are less reliable against these resistance profiles. Lead-acid, nickel-based, and flow batteries still serve narrower uses such as industrial UPS, hybrid powertrains, and multi-hour storage, but they do not carry the same platform momentum. Early algorithm certification under IEC 62619 and ISO 26262 raises qualification cost, yet it also creates a stronger switching barrier for suppliers once solid-state programs move into scaled production.

Distributed topology held 39.3% of the segment in 2025 and is also projected to grow at a 21.1% CAGR, which is unusual for a leading design in the North America battery management system market. Utilities prefer this architecture because it limits fault propagation and supports modular expansion. That preference has strengthened as buyers place more value on system isolation, resilience, and partial uptime during failures. The design also helps reduce insurance and operations exposure on large storage assets where a single fault can affect a high-value installation.

Centralized topology still fits many automotive programs because it offers a compact footprint and a simpler homologation path under vehicle safety rules. Modular systems are gaining ground in 800-volt EV packs and repurposed battery storage because channel counts can be adjusted more efficiently to the use case. BorgWarner's modular BMS platform shows how vehicle suppliers are turning that flexibility into a cross-platform advantage across passenger and commercial programs. Hybrid designs are also emerging where customers want the lower cost of central control and the fault tolerance of distributed sensing in the same installation.

Complete Report Scope:

- By Battery Type

- Lithium-ion

- Lead-acid

- Nickel-based

- Flow Batteries

- Solid-state

- By Topology

- Centralized

- Distributed

- Modular

- Hybrid

- By Component

- Hardware

- Software

- By Voltage Range

- Low (Up to 36 V)

- Medium (36 to 60 V)

- High (Above 60 V)

- By Application

- Automotive

- Stationary Energy Storage

- Consumer Electronics

- Industrial and Telecom UPS

- Medical Devices

- Aerospace and Marine

- By Country

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Texas Instruments Inc.

- Sensata Technologies Inc.

- BorgWarner Inc.

- Nuvation Energy

- Eberspaecher Vecture Inc.

- Schneider Electric SE

- Johnson Controls plc

- Analog Devices Inc.

- STMicroelectronics N.V.

- Continental AG

- Renesas Electronics Corp.

- Panasonic Corp.

- Leclanche SA

- Navitas Systems

- Cummins Inc.

- Lithium Balance A/S

- LG Energy Solution

- ION Energy

- Romeo Power Inc.

- Ewert Energy Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating EV penetration & zero-emission mandates

- 4.2.2 Federal / provincial energy-storage incentives

- 4.2.3 Declining Li-ion battery costs

- 4.2.4 Utility-led V2G pilots need advanced BMS

- 4.2.5 Cold-climate thermal-management start-ups (Canada)

- 4.2.6 Cloud-connected BaaS revenue models

- 4.3 Market Restraints

- 4.3.1 Safety recalls from thermal runaway

- 4.3.2 Dependence on imported cells

- 4.3.3 Few functional-safety labs in Mexico

- 4.3.4 SoC-algorithm patent thicket

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment & Funding Landscape

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-acid

- 5.1.3 Nickel-based

- 5.1.4 Flow Batteries

- 5.1.5 Solid-state

- 5.2 By Topology

- 5.2.1 Centralized

- 5.2.2 Distributed

- 5.2.3 Modular

- 5.2.4 Hybrid

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.4 By Voltage Range

- 5.4.1 Low (Up to 36 V)

- 5.4.2 Medium (36 to 60 V)

- 5.4.3 High (Above 60 V)

- 5.5 By Application

- 5.5.1 Automotive

- 5.5.2 Stationary Energy Storage

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial and Telecom UPS

- 5.5.5 Medical Devices

- 5.5.6 Aerospace and Marine

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments}

- 6.4.1 Texas Instruments Inc.

- 6.4.2 Sensata Technologies Inc.

- 6.4.3 BorgWarner Inc.

- 6.4.4 Nuvation Energy

- 6.4.5 Eberspaecher Vecture Inc.

- 6.4.6 Schneider Electric SE

- 6.4.7 Johnson Controls plc

- 6.4.8 Analog Devices Inc.

- 6.4.9 STMicroelectronics N.V.

- 6.4.10 Continental AG

- 6.4.11 Renesas Electronics Corp.

- 6.4.12 Panasonic Corp.

- 6.4.13 Leclanche SA

- 6.4.14 Navitas Systems

- 6.4.15 Cummins Inc.

- 6.4.16 Lithium Balance A/S

- 6.4.17 LG Energy Solution

- 6.4.18 ION Energy

- 6.4.19 Romeo Power Inc.

- 6.4.20 Ewert Energy Systems Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

雲端連接電池管理系統(BMS)最佳化軟體市場機會、成長要素、產業趨勢分析及2026-2035年預測

雲端連接電池管理系統(BMS)最佳化軟體市場機會、成長要素、產業趨勢分析及2026-2035年預測 電池管理系統(BMS)半導體市場:預測(至2034年)-按組件、電池類型、應用和地區分類的全球分析

電池管理系統(BMS)半導體市場:預測(至2034年)-按組件、電池類型、應用和地區分類的全球分析 電池管理系統市場:按電池化學成分、解決方案類型、電池電壓範圍、容量範圍和最終用戶分類-2026-2032年全球市場預測

電池管理系統市場:按電池化學成分、解決方案類型、電池電壓範圍、容量範圍和最終用戶分類-2026-2032年全球市場預測 電池管理系統市場規模、佔有率和趨勢分析報告:按電池類型、拓撲、應用、地區和細分市場預測(2026-2033 年)

電池管理系統市場規模、佔有率和趨勢分析報告:按電池類型、拓撲、應用、地區和細分市場預測(2026-2033 年) 電池管理系統市場:依拓樸結構、組件、產業及地區分類

電池管理系統市場:依拓樸結構、組件、產業及地區分類 電動自行車電池管理系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

電動自行車電池管理系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 快速充電技術市場:策略性洞察與預測(2026-2031年)電池生命週期代幣化市場預測至2034年-全球分析(按代幣類型、電池類型、平台類型、服務類型、應用程式、最終用戶和地區分類)電池管理系統(BMS)市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

快速充電技術市場:策略性洞察與預測(2026-2031年)電池生命週期代幣化市場預測至2034年-全球分析(按代幣類型、電池類型、平台類型、服務類型、應用程式、最終用戶和地區分類)電池管理系統(BMS)市場規模、佔有率、成長率和全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 2026-2030年全球汽車用鋰離子電池管理系統(BMS)市場

2026-2030年全球汽車用鋰離子電池管理系統(BMS)市場