|

市場調查報告書

商品編碼

2043968

電動自行車電池管理系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Electric Three-wheeler Battery Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

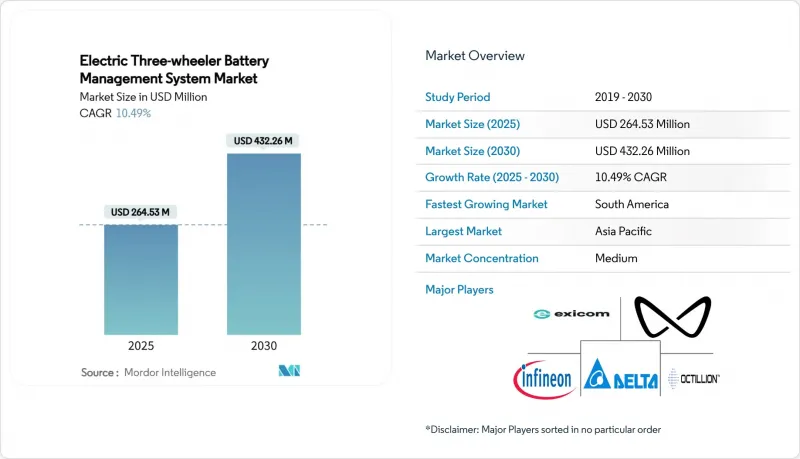

預計到 2025 年,電動三輪車電池管理系統 (BMS) 市場規模將達到 2.6453 億美元,並以 10.49% 的複合年成長率成長,到 2030 年達到 4.3226 億美元。

強力的政策獎勵、鋰離子電池價格的下降以及無線電池管理系統(BMS)架構的普及,正在推動電動三輪車電池管理系統市場的擴張。無線設計無需笨重的線束,支援模組化電池組,並縮短組裝時間,使供應商更容易從注重成本的三輪車製造商那裡獲得訂單。亞太地區的銷售領先,其中印度在補貼政策的推動下,其快速普及率的提升起到了決定性作用。同時,巴西的電動車推廣框架也為市場的快速成長開闢了新的機會。積體電路(IC)正在將功能整合到單一晶片上,隨著邊緣人工智慧和空中下載(OTA)更新在電動三輪車電池管理系統市場逐漸成為主流,通訊介面IC的成長速度最快。半導體巨頭、BMS專業廠商和人工智慧新創公司都在競相推廣無線設計,市場競爭日益激烈。

全球電動自行車電池管理系統市場趨勢與洞察

推廣主流電動車政策和購車獎勵

政府獎勵計畫正在從根本上改變電動三輪車的經濟格局。印度的「2024年電動三輪車計畫」(EMPS 2024)表明,有針對性的補貼如何超越自然市場力量,加速電池管理系統(BMS)的需求成長。泰國的「EV3.5包裝計畫」便是這一趨勢的例證,該計畫根據電池容量提供2.5萬至10萬泰銖的補貼,同時強制要求本地組裝,以促進整合式BMS解決方案的應用。這些政策框架推動了標準化需求,同時也人為地刺激了需求,對BMS供應鏈帶來了壓力。加州的「零排放車輛」(ZEV)計畫旨在2030年使美國35%的車輛為電動車,該計畫正在樹立一個監管先例,這將影響全球三輪車的部署模式,尤其是在續航里程問題較小的都市區配送應用領域。

鋰離子電池成本快速下降以及向磷酸鐵鋰電池的轉變

隨著磷酸鐵鋰(LFP)電池成本接近每千瓦時85美元,三輪車的總擁有成本(TCO)將在兩年內達到同一水平,這將從根本上改變電池管理系統(BMS)的設計重點,使其從成本最佳化轉向性能差異化。寧德時代(CATL)的「神星PLUS」技術實現了205瓦時/公斤的能量密度和4C充電能力,表明LFP化學技術的進步正在克服傳統能量密度電池的不足,同時保持了三輪車在熱帶地區運行所必需的熱穩定性優勢。這種化學成分的轉變透過LFP專用的剩餘容量估算演算法,為BMS的差異化提供了機遇,這些演算法可以解決諸如放電曲線平坦和滯後效應等挑戰。此外,更低的成本使得電池可以二次性利用,廢棄三輪車電池可以保留70-80%的容量,這為管理退化電池和在固定式儲能系統中進行安全監控的BMS供應商創造了新的收入來源。

半導體供應鏈的波動

汽車級半導體的短缺正在對整個電池管理系統 (BMS) 供應鏈產生連鎖反應,需要通過 ISO 26262 認證並符合汽車溫度範圍要求的專用電池監控積體電路 (IC) 的前置作業時間超過 52 週。這種波動迫使 BMS 製造商提高庫存水平,增加了營運資金需求,同時也為擁有自有半導體生產能力的垂直整合供應商創造了競爭優勢。供應限制也推動了可製造性設計 (DFM) 的發展,BMS 架構正轉向通用元件和軟體定義功能,以減少對專用 IC 的依賴。這種轉變為英飛凌和意法半導體等公司帶來了機遇,它們可以提供將電源管理、通訊和安全功能整合在單一晶片上的解決方案。

細分市場分析

積體電路 (IC) 將繼續引領市場,預計到 2024 年將佔據 41.26% 的市場佔有率。這主要歸功於積體電路將多種電池管理系統 (BMS) 功能整合到單一晶片上,從而降低系統複雜性,並透過減少連接數量來提高可靠性。溫度感測器和電量計設備的需求穩定成長,這主要受熱帶氣候下溫度控管需求以及磷酸鐵鋰電池專用充電狀態 (SOC) 演算法的推動,這些演算法旨在解決放電曲線平坦的問題。通訊介面 IC 正在成為成長最快的組件領域,預計到 2030 年複合年成長率 (CAGR) 將達到 27.43%,這反映了產業向無線架構和邊緣人工智慧 (AI) 能力的轉型,而這些轉型需要先進的資料處理和傳輸能力。

元件的發展趨勢正從傳統的離散元件轉向系統晶片(SoC) 解決方案,其中多功能積體電路 (IC) 整合了電池監控、均衡控制、通訊和安全功能。英飛凌的 TLE9012DQU 正是這一趨勢的典型代表,它在針對汽車應用最佳化的單一封裝中整合了全面的鋰離子電池監控和均衡控制功能。隨著電池管理系統 (BMS) 整合預測演算法和機器學習功能以進行電池健康評估和故障預測,微控制器的重要性日益凸顯。截止場效電晶體 (FET) 和驅動器作為安全關鍵型組件,由於其功率處理要求和散熱方面的限制,難以整合,因此需求仍然穩定。

到2024年,集中式系統將保持38.17%的市場佔有率,而無線、無電纜拓撲結構將以31.08%的複合年成長率成長,這標誌著向模組化架構的根本性轉變,模組化架構能夠實現靈活的電池組配置,同時消除複雜的線束。這種向無線架構的轉變解決了三輪車製造的關鍵挑戰,在三輪車製造中,空間限制和成本壓力要求簡化組裝流程,以減少人工需求和潛在故障點。分散式拓撲結構將服務於需要在電池單元層級進行精細監控的特定應用,而模組化系統將彌合集中式系統的成本優勢和分散式系統柔軟性優勢之間的差距。

恩智浦半導體的超寬頻 (UWB) 無線電池管理系統 (BMS) 展示了先進的通訊協定如何克服傳統無線技術的局限性,例如易受干擾和延遲問題,這些問題先前限制了無線技術在安全關鍵型應用中的部署。這種拓撲結構的演進創造了一個競爭環境,傳統的有線 BMS 供應商必須開發無線功能,否則將面臨市場佔有率被專業無線解決方案供應商蠶食的風險。無線拓撲結構在電池更換應用中尤其受歡迎,因為它能夠實現快速更換電池組,而無需擔心連接器磨損。這推動了基於服務的移動出行模式的發展,在這種模式下,電池所有權和車輛所有權是分離的。

《電動三輪車電池管理系統(BMS)報告》按組件(積體電路、其他)、拓樸結構(集中式、模組化、分散式、無線)、通訊技術(有線CAN、其他)、電池化學成分(磷酸鐵鋰電池、鎳鈷酸鋰電池、鉛酸鋰電池)、應用領域(乘用車、其他)、分銷管道(OEM、其他)和地區進行細分。市場預測以美元計價。

區域分析

亞太地區引領市場,預計2024年將佔全球銷售量的64.72%。這主要得益於印度市場滲透率的提升,預計到2026年,印度市場滲透率將從5%成長至26-28%,這得益於補貼政策的明確和在地採購率相關規定的完善。泰米爾納德邦和古吉拉突邦的本土電池工廠透過保障供應和降低物流成本,使電池組價格每度電降低了12美元。儘管2023年中國電池產量下降了8%至32萬台,但中國仍是技術先鋒。寧德時代的「神星PLUS」和比亞迪的「刀鋒電池」正在提升全球電池管理系統(BMS)的標竿水平,迫使區域BMS供應商在升級熱電池型號和麵臨產品過時的風險之間做出選擇。

在北美和歐洲,政策主導的市場穩定成長。儘管美國聯邦稅額扣抵政策引發爭議,造成不確定性,但加州35%的零排放車輛(ZEV)目標為市場需求奠定了基礎。車隊營運商強烈要求產品符合ISO 26262和ISO/SAE 21434標準,網路安全和功能安全也日益成為進入的必要條件。在歐洲,電池法規要求每次交易都必須報告電池健康狀態(SOH),因此雲端連接的電池管理系統(BMS)架構至關重要。循環經濟原則鼓勵透過二次利用累積收益,這一趨勢正日益融入電動三輪車電池管理系統市場。

儘管電動送貨三輪車在中東和非洲仍處於小規模規模應用階段,但海灣國家的城市已開始引入此類車輛,用於生鮮電商業務。政府競標中包含太陽能座艙罩和電池更換服務,旨在減輕電網負載。為了應對極端溫度,需要一種降額演算法,當環境溫度超過 45 度C時,演算法會降低充電電流。目前,高階電池管理系統 (BMS)韌體已將此功能作為標準配置。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 將電動車政策和購車獎勵納入主流

- 鋰離子電池成本快速下降以及向磷酸鐵鋰電池的轉變

- OEM廠商向自主研發的無線BMS過渡

- 印度CAN-FD協議的標準化

- 邊緣人工智慧預測性維護在可互換組件的應用

- 可充電電池商業化模式

- 市場限制因素

- 半導體供應鏈的波動性

- 熱帶地區使用的熱裕度限制

- 低成本電池管理系統中的網路安全漏洞

- 二級維修承包商的技能差距

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模及成長預測(價值(美元))

- 按組件

- 積體電路

- 截止場效電晶體和驅動器

- 溫度感測器

- 燃油表/電流測量裝置

- 微控制器

- 通訊介面軟體

- 其他

- 拓樸

- 集中

- 模組化的

- 去中心化

- 無線(無電纜)

- 透過通訊技術

- 有線 CAN

- 有線以太網

- 無線射頻

- 電池化學成分

- LFP

- NMC

- 鉛酸

- 透過使用

- 搭乘用車

- 貨物/裝卸車輛

- 透過分銷管道

- 原廠正品零件

- 售後/維修安裝

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Exicom Tele-Systems

- Delta Electronics Inc.

- Octillion Power Systems

- Infineon Technologies AG

- Mahindra Electric Mobility

- Piaggio Group

- Atul Auto Ltd.

- Kinetic Green Energy

- Saft(TotalEnergies)

- Trontek Batteries

- Lithium Balance A/S

- Sensata Technologies

- NXP Semiconductors

- Texas Instruments

- Renesas Electronics

- Panasonic Industry

- LG Energy Solution

- CATL

- Infineon Technologies

- BYD Co. Ltd.

- Bosch Mobility Solutions

- AVL List GmbH

第7章 市場機會與未來展望

The Electric three-wheeler battery management system market size reached USD 264.53 million in 2025 and is forecast to advance at a 10.49% CAGR to USD 432.26 million by 2030.

Strong policy incentives, falling lithium-ion prices and the switch to wireless BMS architectures underpin this expansion of the Electric three-wheeler battery management system market. Wireless designs remove bulky harnesses, allow modular packs and cut assembly time, helping suppliers win orders from cost-sensitive three-wheeler manufacturers. Asia Pacific leads volumes, India's subsidy-driven penetration jump is decisive, while Brazil's pro-EV framework opens a fast-growth frontier. Integrated circuits consolidate functions on a single chip, and communication interface ICs grow quickest as edge-AI and over-the-air updates become mainstream in the Electric three-wheeler battery management system market. Competitive intensity rises because semiconductor giants, niche BMS specialists and AI start-ups all target wireless design wins.

Global Electric Three-wheeler Battery Management System Market Trends and Insights

Mainstream EV-Policy Push and Purchase Incentives

Government incentive structures fundamentally reshape three-wheeler electrification economics, with India's EMPS 2024 demonstrating how targeted subsidies accelerate BMS demand beyond organic market forces. Thailand's EV3.5 package exemplifies this trend, offering THB 25,000-100,000 subsidies based on battery capacity while mandating local assembly requirements favoring integrated BMS solutions. The policy framework creates artificial demand spikes that strain BMS supply chains while simultaneously driving standardization requirements. California's Zero Emission Vehicle program, targeting 35% of US EVs by 2030, establishes regulatory precedents that influence global three-wheeler adoption patterns, particularly in urban delivery applications with minimal range anxiety concerns.

Rapid Lithium-Ion Cost Decline and LFP Shift

Lithium Iron Phosphate battery costs approaching USD 85 per kWh enable three-wheeler total cost of ownership parity within 2 years, fundamentally altering BMS design priorities from cost optimization to performance differentiation. CATL's Shenxing PLUS technology, achieving 205 Wh/kg energy density with 4C charging capabilities, demonstrates how LFP chemistry advances eliminate traditional energy density disadvantages while maintaining thermal stability benefits crucial for tropical three-wheeler operations. The chemistry shift creates BMS differentiation opportunities through LFP-specific fuel gauging algorithms that address flat discharge curve challenges and hysteresis effects. Cost declines also enable secondary-life applications where retired three-wheeler batteries retain 70-80% capacity, creating new revenue streams for BMS providers who can manage degraded cell performance and safety monitoring in stationary storage applications.

Semiconductor Supply-Chain Volatility

Automotive-grade semiconductor shortages create cascading effects throughout BMS supply chains, with lead times extending beyond 52 weeks for specialized battery monitoring ICs that require ISO 26262 certification and automotive temperature range compliance. The volatility forces BMS manufacturers to maintain higher inventory levels, increasing working capital requirements while creating competitive advantages for vertically integrated suppliers with captive semiconductor capacity. Supply constraints also drive design-for-manufacturability initiatives where BMS architectures migrate toward commodity components and software-defined functionality to reduce dependence on specialized ICs. This shift creates opportunities for companies like Infineon and STMicroelectronics, which can provide integrated solutions combining power management, communication, and safety functions on single chips.

Other drivers and restraints analyzed in the detailed report include:

- OEM Migration to In-House Wireless BMS

- Standardization of CAN-FD protocols in India

- Cyber-Security Vulnerabilities in Low-Cost BMS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated Circuits maintain market leadership with 41.26% share in 2024, benefiting from the consolidation of multiple BMS functions onto single chips that reduce system complexity while improving reliability through reduced interconnections. Temperature Sensors and Fuel-Gauge devices experience steady demand growth driven by thermal management requirements in tropical climates and LFP-specific state-of-charge algorithms that address flat discharge curve challenges. Communication Interface ICs emerge as the fastest-growing component segment at 27.43% CAGR through 2030, reflecting the industry's migration toward wireless architectures and edge-AI capabilities that require sophisticated data processing and transmission functions.

The component landscape shifts toward system-on-chip solutions where traditional discrete components integrate into multifunctional ICs that combine battery monitoring, balancing, communication, and safety functions. Infineon's TLE9012DQU exemplifies this trend, providing comprehensive Li-ion battery monitoring and balancing capabilities in a single package optimized for automotive applications. Microcontrollers gain importance as BMS systems incorporate predictive algorithms and machine learning capabilities for battery health estimation and fault prediction. Cut-off FETs and Drivers maintain stable demand as safety-critical components that cannot be easily integrated due to power handling requirements and thermal considerations.

Centralized systems maintain a 38.17% share in 2024, while wireless cable-less topologies accelerate at a 31.08% CAGR, indicating a fundamental shift toward modular architectures that eliminate complex wiring harnesses while enabling flexible battery pack configurations. The wireless transition addresses key pain points in three-wheeler manufacturing where space constraints and cost pressures favor simplified assembly processes that reduce labor requirements and potential failure points. Distributed topologies serve niche applications requiring granular cell-level monitoring, while modular systems bridge the gap between centralized cost advantages and distributed flexibility benefits.

NXP's Ultra-Wideband wireless BMS demonstrates how advanced communication protocols overcome traditional wireless limitations, including interference susceptibility and latency concerns that previously restricted wireless adoption in safety-critical applications. The topology evolution creates competitive dynamics where traditional wired BMS providers must develop wireless capabilities or risk market share erosion to specialized wireless solution providers. Battery swapping applications particularly favor wireless topologies that enable rapid pack exchanges without connector wear concerns, supporting the growth of service-based mobility models where battery ownership separates from vehicle ownership.

The Electric Three-Wheeler Battery Management System Report is Segmented by Component (Integrated Circuits and More), Topology (Centralized, Modular, Distributed, and Wireless), Communication Technology (Wired CAN and More), Battery Chemistry (LFP, NMC, and Lead-Acid), Application (Passenger Carrier and More), Sales Channel (OEM-Fitted and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific dominated 2024 revenue with a 64.72% share as India's penetration rose from 5% to an expected 26-28% by fiscal 2026, catalysed by subsidy clarity and local-content rules. Domestic cell factories in Tamil Nadu and Gujarat secure supply and cut logistics costs, lowering pack prices by USD 12 kWh. China, even after an 8% dip to 320,000 units in 2023, remains the technology pacesetter. CATL's Shenxing PLUS and BYD's blade battery push global benchmarks, compelling regional BMS suppliers to upgrade thermal models or risk obsolescence.

North America and Europe show steady, policy-driven adoption. The US federal tax-credit debate injects uncertainty, but California's 35% ZEV target anchors demand. Fleets insist on ISO 26262 and ISO/SAE 21434 compliance, elevating cybersecurity and functional safety as ticket-to-play attributes. In Europe, the Battery Regulation enforces state-of-health reporting at each transaction, forcing cloud-linked BMS architectures. Circular-economy rules foster secondary-life revenue stacking that the Electric three-wheeler battery management system market increasingly internalises.

Middle East and Africa begin from a small base yet deploy electric delivery trikes for e-grocery ventures in Gulf cities. Government tenders bundle solar canopies with battery swapping, reducing grid stress. Temperature extremes demand derating algorithms that de-rate charge current above 45 °C ambient, a capability now standard on premium BMS firmware.

- Exicom Tele-Systems

- Delta Electronics Inc.

- Octillion Power Systems

- Infineon Technologies AG

- Mahindra Electric Mobility

- Piaggio Group

- Atul Auto Ltd.

- Kinetic Green Energy

- Saft (TotalEnergies)

- Trontek Batteries

- Lithium Balance A/S

- Sensata Technologies

- NXP Semiconductors

- Texas Instruments

- Renesas Electronics

- Panasonic Industry

- LG Energy Solution

- CATL

- Infineon Technologies

- BYD Co. Ltd.

- Bosch Mobility Solutions

- AVL List GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream EV-Policy Push and Purchase Incentives

- 4.2.2 Rapid Lithium-Ion Cost Decline and LFP Shift

- 4.2.3 OEM Migration to In-House Wireless BMS

- 4.2.4 Standardisation of CAN-FD Protocols in India

- 4.2.5 Edge-AI Prognostics for Swap-Ready Packs

- 4.2.6 Secondary-Life Battery Monetisation Models

- 4.3 Market Restraints

- 4.3.1 Semiconductor Supply-Chain Volatility

- 4.3.2 Limited Thermal Envelope in Tropical Use

- 4.3.3 Cyber-Security Vulnerabilities in Low-Cost BMS

- 4.3.4 Skills Gap in Tier-2 Retrofit Installers

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Component

- 5.1.1 Integrated Circuits

- 5.1.2 Cut-off FETs and Drivers

- 5.1.3 Temperature Sensors

- 5.1.4 Fuel-Gauge/Current-Measurement Devices

- 5.1.5 Microcontrollers

- 5.1.6 Communication Interface ICs

- 5.1.7 Other Components

- 5.2 By Topology

- 5.2.1 Centralized

- 5.2.2 Modular

- 5.2.3 Distributed

- 5.2.4 Wireless (Cable-less)

- 5.3 By Communication Technology

- 5.3.1 Wired CAN

- 5.3.2 Wired Ethernet

- 5.3.3 Wireless RF

- 5.4 By Battery Chemistry

- 5.4.1 LFP

- 5.4.2 NMC

- 5.4.3 Lead-acid

- 5.5 By Application

- 5.5.1 Passenger Carrier

- 5.5.2 Cargo/Load Carrier

- 5.6 By Sales Channel

- 5.6.1 OEM-fitted

- 5.6.2 Aftermarket/Retrofit

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Australia and New Zealand

- 5.7.4.6 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 South Africa

- 5.7.5.5 Egypt

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Exicom Tele-Systems

- 6.4.2 Delta Electronics Inc.

- 6.4.3 Octillion Power Systems

- 6.4.4 Infineon Technologies AG

- 6.4.5 Mahindra Electric Mobility

- 6.4.6 Piaggio Group

- 6.4.7 Atul Auto Ltd.

- 6.4.8 Kinetic Green Energy

- 6.4.9 Saft (TotalEnergies)

- 6.4.10 Trontek Batteries

- 6.4.11 Lithium Balance A/S

- 6.4.12 Sensata Technologies

- 6.4.13 NXP Semiconductors

- 6.4.14 Texas Instruments

- 6.4.15 Renesas Electronics

- 6.4.16 Panasonic Industry

- 6.4.17 LG Energy Solution

- 6.4.18 CATL

- 6.4.19 Infineon Technologies

- 6.4.20 BYD Co. Ltd.

- 6.4.21 Bosch Mobility Solutions

- 6.4.22 AVL List GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

電動車電池管理系統市場預測至2034年—按組件、電池類型、拓撲結構、車輛類型、應用和地區分類的全球分析

電動車電池管理系統市場預測至2034年—按組件、電池類型、拓撲結構、車輛類型、應用和地區分類的全球分析 電池管理系統市場:按電池化學成分、解決方案類型、電池電壓範圍、容量範圍和最終用戶分類-2026-2032年全球市場預測

電池管理系統市場:按電池化學成分、解決方案類型、電池電壓範圍、容量範圍和最終用戶分類-2026-2032年全球市場預測 兩輪和三輪電動車的電池管理系統市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、功能、安裝配置、解決方案

兩輪和三輪電動車的電池管理系統市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、功能、安裝配置、解決方案 北美電池管理系統:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美電池管理系統:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 雲端連接電池管理系統(BMS)最佳化軟體市場機會、成長要素、產業趨勢分析及2026-2035年預測電池管理系統(BMS)半導體市場:預測(至2034年)-按組件、電池類型、應用和地區分類的全球分析

雲端連接電池管理系統(BMS)最佳化軟體市場機會、成長要素、產業趨勢分析及2026-2035年預測電池管理系統(BMS)半導體市場:預測(至2034年)-按組件、電池類型、應用和地區分類的全球分析 電池管理系統市場規模、佔有率和趨勢分析報告:按電池類型、拓撲、應用、地區和細分市場預測(2026-2033 年)

電池管理系統市場規模、佔有率和趨勢分析報告:按電池類型、拓撲、應用、地區和細分市場預測(2026-2033 年) 電池管理系統市場:依拓樸結構、組件、產業及地區分類

電池管理系統市場:依拓樸結構、組件、產業及地區分類 快速充電技術市場:策略性洞察與預測(2026-2031年)電池生命週期代幣化市場預測至2034年-全球分析(按代幣類型、電池類型、平台類型、服務類型、應用程式、最終用戶和地區分類)

快速充電技術市場:策略性洞察與預測(2026-2031年)電池生命週期代幣化市場預測至2034年-全球分析(按代幣類型、電池類型、平台類型、服務類型、應用程式、最終用戶和地區分類)