|

市場調查報告書

商品編碼

2073603

印度尿素市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Urea - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

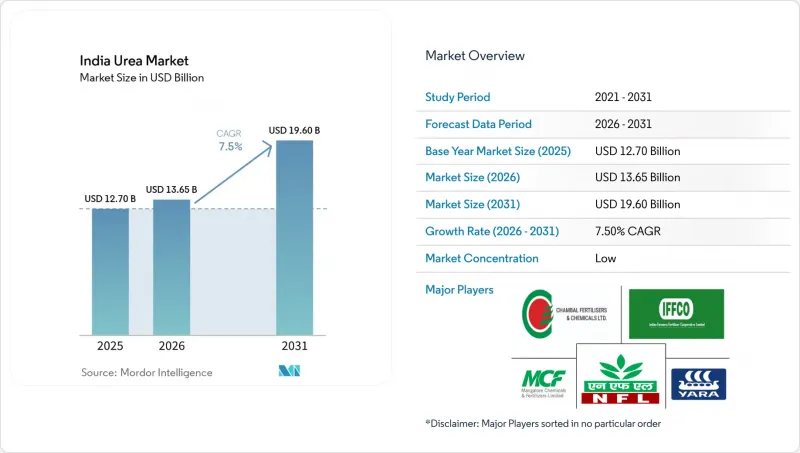

據 Mordor Intelligence 稱,2025 年印度尿素市場價值 127 億美元,預計到 2031 年將達到 196 億美元,而 2026 年為 136.5 億美元,預測期(2026-2031 年)複合年成長率為 7.50%。

本報告依特殊用途(緩釋肥、控釋肥、液體肥、水溶性肥料)、作物類型(田間作物、園藝作物、草坪和觀賞作物)以及形態(常規型和特殊型)進行分類。市場預測以價值(美元)和數量(公噸)表示。

印度尿素市場趨勢與洞察

氮是田間作物種植中最廣泛使用的營養元素。

氮肥平均施用量為223.5公斤/公頃,是使用最廣泛的營養元素。作為一種主要營養元素,氮肥對於種植高產量作物(包括印度農業的主要作物水稻)至關重要。然而,氮肥缺乏已成為全國性問題,導致水稻產量下降。 《生物肥料和有機肥料現狀》報告強調了印度土壤健康狀況令人擔憂的問題。報告指出,過度依賴化學肥料的趨勢令人擔憂,調查土壤中分別有97.0%、83.0%和71.0%的土壤有氮、磷、鉀缺乏的情況。小麥和稻米是印度乃至世界各地餐桌上的主食,它們面臨多種營養元素缺乏帶來的挑戰。作為田間作物,穀物對主要營養元素,尤其是氮肥,有持續的需求。由於這些作物在印度廣泛種植,土壤養分含量下降的問題日益突出。

微灌系統的引入提高了對水溶性肥料的需求。

基於「總理農業灌溉計畫」(Pradhan Mantri Krishi Sinchayee Yojana)的微灌技術推廣應用,正在引發水溶性肥料需求結構性轉變。這是因為滴灌和噴灌系統需要完全溶解的養分,以防止堵塞並確保均勻分佈。該計畫為2024-2025年度撥款4000卡印度盧比(約4.7806億美元),目標是覆蓋150萬公頃土地,這將直接影響對施肥灌溉的需求。 2024年,尿素價格為每噸328.25美元,但其特徵是養分利用率極高。對於投入成本僅佔總生產成本一小部分的高價值作物而言,這種高效率具有顯著的經濟吸引力。像海法集團(Haifa Group)這樣的公司已經證明,透過精準施肥方案,作物產量可提高15-20%,這證明了其技術可靠性,並鼓勵先進農戶採用該技術。

與傳統尿素相比,價格溢價較高

特種肥料與傳統尿素之間兩到四倍的價格差異是推廣應用的主要障礙,尤其對於佔印度農業人口86%、對價格高度敏感的小規模農戶而言更是如此。 2024年,尿素批發價徘徊在每噸328.20美元左右,即使養分利用效率提高,農民也不需要大幅增加流動資金。近十年來,實際價格一直保持穩定,人為地為高氮肥施用方案提供了成本優勢。要證明特種肥料的經濟效益,需要證明其產量提升足以抵銷投入成本的增加,但在商品價格劇烈波動時期,這種價值提案難以實現。小規模農戶的資金籌措進一步削弱了他們投資昂貴肥料的能力,儘管這些肥料可能對土壤健康帶來長期益處。

細分市場分析

水溶性肥料是最大的細分市場,預計到2025年將佔印度尿素市場佔有率的53.3%。這反映了它們與現代灌溉系統的兼容性以及卓越的養分利用效率,也因此支撐了其較高的價格。此細分市場的主導地位源自於其與微灌技術和保護性耕作的推廣同步發展,在這些技術中,精準的養分輸送對於最佳化作物產量至關重要。緩效肥料是成長最快的特種肥料,預計到2031年將以8.6%的複合年成長率成長,這得益於其能夠減少施肥頻率並最大限度地減少養分因淋溶和揮發造成的損失。緩釋肥料保持穩定的市場地位,儘管市場佔有率較小,主要用於草坪和觀賞植物的種植,這些作物需要較長的施肥週期。

液態肥料佔據一個細分市場,主要應用於葉面噴布和灌溉施肥系統,具有養分快速吸收和配方調整柔軟性等優點。 IFFCO 的奈米肥料代表著一個新興類別,有望徹底改變傳統的特殊肥料體系。該公司的奈米尿素和奈米磷酸二銨產品受 20 年專利保護,並已獲得政府批准上市。基於 1985 年《肥料管制令》的法規結構規定了產品規格和品質標準,而近期修訂案簡化了水溶性肥料的報名手續,從而加快了創新配方產品的市場推廣。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 主要農作物種植面積

- 大田作物

- 園藝作物

- 平均施肥量

- 主要營養素

- 田間作物

- 園藝作物

- 主要營養素

- 配備灌溉設施的農田

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 氮是農作物中最廣泛使用的營養元素。

- 微灌系統的引入促進了對水溶性產品的需求。

- 透過保護性栽培擴大園藝面積

- 農產品電子商務平台的成長正在改善最後一公里配送。

- 企業化和合約化農業模式優先考慮能最大限度提高產量的投入材料。

- 國內聚合物產能的提高導致控釋肥生產成本的下降。

- 市場限制因素

- 與傳統尿素相比,價格溢價較高

- 通路的碎片化助長了仿冒品。

- 農業技術指導不足,造成作物灼傷的風險。

- 對油漆進口的依賴和外匯波動

第5章 市場規模與成長預測

- 特殊目的

- CRF

- 聚合物塗層

- 聚合物硫塗層

- 其他

- 液體肥料

- SRF

- 水溶性

- CRF

- 按作物類型

- 田間作物

- 園藝作物

- 草坪和觀賞植物

- 按形式

- 傳統的

- 專業

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介。

- Indian Farmers Fertiliser Cooperative Limited

- Chambal Fertilizers and Chemicals Limited

- National Fertilizers Limited

- Coromandel International Limited

- Gujarat Narmada Valley Fertilizers and Chemicals Limited

- Mangalore Chemicals and Fertilizers Limited

- Yara International ASA

- Zuari Agro Chemicals Limited

- Deepak Fertilisers and Petrochemicals Corporation Limited

- Rashtriya Chemicals and Fertilizers Limited

- Nagarjuna Fertilizers and Chemicals Limited

- Haifa Group

- ICL Group

- Mosaic Company

- IPL Biologicals Limited

- Smartchem Technologies Limited

- Aries Agro Limited

- Hifield Organics Inc.

- Aries Agro Produce India Private Limited

- K+S Aktiengesellschaft

第7章 化肥產業執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the india urea market size was valued at USD 12.70 billion in 2025 and estimated to grow from USD 13.65 billion in 2026 to reach USD 19.60 billion by 2031, at a CAGR of 7.50% during the forecast period (2026-2031).

This report is Segmented by Specialty Type (Controlled-Release Fertilizers, Slow-Release Fertilizers, Liquid Fertilizers, and Water-Soluble Fertilizers), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Form (Conventional and Specialty). The Market Forecasts are Provided in Terms of Value (USD) and Volume (metric Tons).

India Urea Market Trends and Insights

Nitrogen stands out as the most widely used nutrient in field crop cultivation

Nitrogen, with an average application rate of 223.5 kg/ha, stands out as the most widely utilized nutrient. As a primary nutrient, nitrogen is crucial for high-yield crops, notably rice, which dominates India's agricultural landscape. Yet, a nationwide struggle with nitrogen deficiencies is undermining rice productivity. Concerns about India's soil health are underscored in the "State of Biofertilizers and Organic Fertilizers" report. It highlights an alarming trend: a heavy dependence on chemical fertilizers, with 97.0%, 83.0%, and 71.0% of tested soils exhibiting deficiencies in nitrogen, phosphorus, and potassium, respectively. Wheat and rice, staples on both domestic and global tables, grapple with challenges stemming from multiple nutrient deficiencies. Grains and cereals, as field crops, have an insatiable demand for primary nutrients, especially nitrogen fertilizers. With these crops being extensively cultivated across India, the depletion of the soil's nutrient content is becoming increasingly pronounced.

Adoption of Micro-Irrigation Systems Boosting Water-Soluble Demand

Micro-irrigation coverage expansion under the Pradhan Mantri Krishi Sinchayee Yojana has created a structural demand shift toward water-soluble fertilizers, with drip and sprinkler systems requiring fully dissolved nutrients to prevent clogging and ensure uniform distribution. The scheme's allocation of INR 4,000 crore (USD 478.06 million) for 2024-25 targets coverage of 1.5 million hectares, directly translating to increased fertigation demand. In 2024, urea was priced at USD 328.25 per metric tonne, yet it boasts a high nutrient use efficiency. This efficiency becomes economically compelling for high-value crops where input costs represent a smaller share of total production expenses. Companies like Haifa Group have demonstrated yield improvements of 15-20% through precision fertigation protocols, establishing technical credibility that drives adoption among progressive farmers.

High Price Premium Versus Conventional Urea

The 2-4x price differential between specialty fertilizers and conventional urea creates a significant adoption barrier, particularly among price-sensitive smallholder farmers who represent 86% of India's agricultural population. In 2024, urea's wholesale price hovered around USD 328.2 per metric tonne, allowing farmers to avoid significant increases in working capital, even with enhanced nutrient use efficiency. For nearly a decade, the effective price has remained stable, granting nitrogen-heavy nutrition programs an artificial cost edge. The economic justification for specialty fertilizers requires demonstration of yield improvements that offset higher input costs, a value proposition that becomes challenging during periods of commodity price volatility. Credit constraints among smallholder farmers further limit their ability to invest in premium inputs, despite potential long-term soil health benefits.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Horticulture Acreage With Protected Cultivation

- Growth of Ag-Input E-Commerce Platforms Improving Last-Mile Access

- Fragmented Distribution Enabling Counterfeit Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-soluble fertilizers are the largest segment, command 53.3% of the India urea market share in 2025, reflecting their compatibility with modern irrigation systems and their superior nutrient-use efficiency, which justifies premium pricing. The segment's dominance stems from its alignment with the expansion of micro-irrigation and the growth of protected cultivation, where precise nutrient delivery becomes critical for optimizing crop performance. Controlled-release fertilizers represent the fastest-growing specialty type, with a 8.6% CAGR through 2031, driven by their ability to reduce application frequency and minimize nutrient losses from leaching and volatilization. Slow-release fertilizers maintain a smaller but stable market presence, primarily serving turf and ornamental applications where extended feeding periods are valued.

Liquid fertilizers occupy a niche position focused on foliar applications and fertigation systems, offering rapid nutrient uptake and flexibility in formulation adjustments. IFFCO's development of nano fertilizers represents an emerging category that could disrupt traditional specialty types, with their nano urea and nano DAP products demonstrating 20-year patent protection and government approval for commercial launch. The regulatory framework under the Fertilizer Control Order 1985 governs product specifications and quality standards, with recent amendments introducing streamlined registration processes for water-soluble fertilizers that enable faster market entry for innovative formulations.

Complete Report Scope:

- Speciality Type

- CRF

- Polymer Coated

- Polymer-Sulfur Coated

- Others

- Liquid Fertilizer

- SRF

- Water Soluble

- CRF

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

- Form

- Conventional

- Specialty

List of Companies Covered in this Report:

- Indian Farmers Fertiliser Cooperative Limited

- Chambal Fertilizers and Chemicals Limited

- National Fertilizers Limited

- Coromandel International Limited

- Gujarat Narmada Valley Fertilizers and Chemicals Limited

- Mangalore Chemicals and Fertilizers Limited

- Yara International ASA

- Zuari Agro Chemicals Limited

- Deepak Fertilisers and Petrochemicals Corporation Limited

- Rashtriya Chemicals and Fertilizers Limited

- Nagarjuna Fertilizers and Chemicals Limited

- Haifa Group

- ICL Group

- Mosaic Company

- IPL Biologicals Limited

- Smartchem Technologies Limited

- Aries Agro Limited

- Hifield Organics Inc.

- Aries Agro Produce India Private Limited

- K+S Aktiengesellschaft

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Nitrogen stands out as the most widely used nutrient in field crop cultivation

- 4.6.2 Adoption of micro-irrigation systems boosting water-soluble demand

- 4.6.3 Expansion of horticulture acreage with protected cultivation

- 4.6.4 Growth of ag-input e-commerce platforms improving last-mile access

- 4.6.5 Corporate/contract farming models favoring yield-maximizing inputs

- 4.6.6 Domestic polymer capacity additions lowering CRF production cost

- 4.7 Market Restraints

- 4.7.1 High price premium versus conventional urea

- 4.7.2 Fragmented distribution enabling counterfeit products

- 4.7.3 Limited agronomic advisory causing crop-burn risk

- 4.7.4 Import-dependence for coating materials and FX volatility

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Form

- 5.3.1 Conventional

- 5.3.2 Specialty

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Indian Farmers Fertiliser Cooperative Limited

- 6.4.2 Chambal Fertilizers and Chemicals Limited

- 6.4.3 National Fertilizers Limited

- 6.4.4 Coromandel International Limited

- 6.4.5 Gujarat Narmada Valley Fertilizers and Chemicals Limited

- 6.4.6 Mangalore Chemicals and Fertilizers Limited

- 6.4.7 Yara International ASA

- 6.4.8 Zuari Agro Chemicals Limited

- 6.4.9 Deepak Fertilisers and Petrochemicals Corporation Limited

- 6.4.10 Rashtriya Chemicals and Fertilizers Limited

- 6.4.11 Nagarjuna Fertilizers and Chemicals Limited

- 6.4.12 Haifa Group

- 6.4.13 ICL Group

- 6.4.14 Mosaic Company

- 6.4.15 IPL Biologicals Limited

- 6.4.16 Smartchem Technologies Limited

- 6.4.17 Aries Agro Limited

- 6.4.18 Hifield Organics Inc.

- 6.4.19 Aries Agro Produce India Private Limited

- 6.4.20 K+S Aktiengesellschaft

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

尿素市場規模、佔有率和趨勢分析報告:按形態、應用、最終用途、地區和細分市場分類(2026-2033 年)

尿素市場規模、佔有率和趨勢分析報告:按形態、應用、最終用途、地區和細分市場分類(2026-2033 年) 顆粒尿素:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

顆粒尿素:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 工業尿素市場規模、佔有率和成長分析:按等級/純度、應用、終端用戶產業、包裝、銷售管道和地區分類-2026-2033年產業預測

工業尿素市場規模、佔有率和成長分析:按等級/純度、應用、終端用戶產業、包裝、銷售管道和地區分類-2026-2033年產業預測 尿素市場:2026-2032年全球市場預測(依最終用途、形態、應用、等級、通路及生產流程分類)

尿素市場:2026-2032年全球市場預測(依最終用途、形態、應用、等級、通路及生產流程分類) 顆粒尿素市場:按應用、產品類型和地區分類尿素市場:依形態、等級、純度、通路(間接/直接)及地區分類

顆粒尿素市場:按應用、產品類型和地區分類尿素市場:依形態、等級、純度、通路(間接/直接)及地區分類 尿素市場分析及預測(至2035年):類型、產品、應用、最終用戶、形態、技術、製程、材料類型、安裝類型

尿素市場分析及預測(至2035年):類型、產品、應用、最終用戶、形態、技術、製程、材料類型、安裝類型 全球硫包覆尿素市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球硫包覆尿素市場規模、佔有率、趨勢及成長分析報告(2026-2034) 尿素市場規模、佔有率、趨勢及預測(依等級、應用、最終用途產業及地區分類),2026-2034年

尿素市場規模、佔有率、趨勢及預測(依等級、應用、最終用途產業及地區分類),2026-2034年 2026年全球尿素市場報告

2026年全球尿素市場報告