|

市場調查報告書

商品編碼

2073583

英國暖氣設備:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)United Kingdom Heating Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

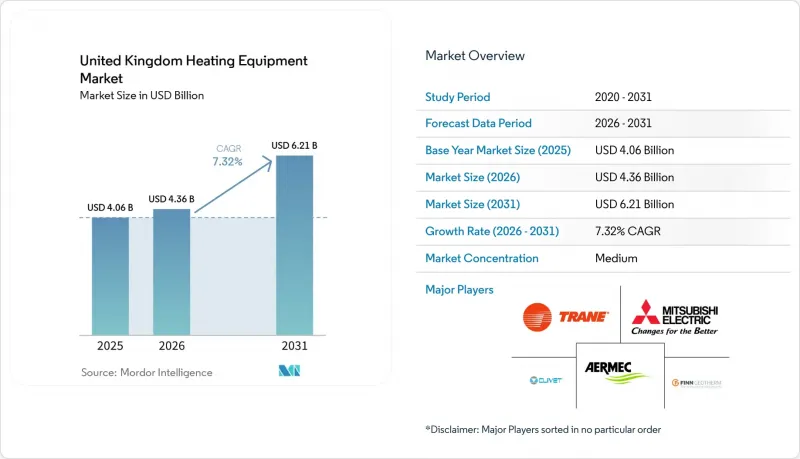

根據 Mordor Intelligence 預測,英國暖氣設備市場規模將從 2025 年的 40.6 億美元成長到 2026 年的 43.6 億美元,然後在 2031 年達到 62.1 億美元,2026 年至 2031 年的複合年成長率為 7.32%。

本報告按設備類型(鍋爐、爐灶、熱泵等)、終端用戶行業(住宅、商業等)、燃料類型(天然氣、電力、石油等)、技術(冷凝式、非冷凝式等)、安裝類型(新安裝、更換/維修)和地區進行細分。市場預測以美元計價。

英國暖氣設備市場趨勢與洞察

政府脫碳政策和獎勵

擴大津貼、放寬技術限制的資格要求以及靈活的租賃方案正在改變英國供暖市場的購買行為。在與能源安全與淨零排放部磋商後,政府擴大了鍋爐升級計劃的範圍,該計劃現已涵蓋空氣源熱泵和蓄熱電池,並根據不同的房產特徵提供量身定做的財政支持。此外,政府也承諾培訓18,000名維修承包商,這項政策組合既滿足了需求,也提升了供應能力。 2025年3月的申請量年增88%,顯示該政策的獎勵策略效果顯著。蘇格蘭先前設定的2045年淨零排放目標正在推動該地區的普及,使該政策成為最強勁的需求驅動力。

老舊鍋爐刺激了對新鍋爐的需求。

英國超過80%的住宅建於1960年以前,因此許多在燃氣鍋爐。隨著建築規範日益嚴格,每個鍋爐的使用壽命結束都標誌著一個轉折點,業主們開始權衡減少碳排放和提高效率之間的利弊,這不僅支撐了英國供暖設備市場的穩定銷售量,也推動了技術進步。

低碳暖氣系統的初始成本較高

根據愛丁堡大學的研究,過去十年間,熱泵的平均安裝價格一直保持穩定,即使有補貼,每戶家庭的實際安裝成本仍然在6500美元到14000美元之間。對於需要進行電氣維修或更換散熱器的房屋,總成本甚至更高,許多家庭往往等到鍋爐徹底損壞才考慮安裝熱泵。正是由於這種經濟障礙,儘管有政策支持,更換鍋爐的案例領先了預防性維修,這也阻礙了英國供暖設備市場的短期成長。

細分市場分析

熱泵市場正以11.24%的複合年成長率快速擴張,穩步燃氣鍋爐目前37.65%的市佔率。政府補貼以及高溫型號的推出(無需徹底更換散熱器即可進行維修)預計將進一步擴大英國英國市場,並加速其成長。燃氣鍋爐由於初始投資低且安裝人員熟悉其操作,仍然擁有強勁的需求,但即將訂定的能源效率法規預計將對利潤率構成壓力。結合兩種技術的混合產品代表了一種對沖策略,製造商可以透過該策略平衡當前銷售與未來需求。爐子和輔助散熱器在工業和大型商業設施中仍佔據著一定的市場佔有率,需求雖然有限但穩定。

現有燃氣鍋爐製造商正試圖透過推出氫氣兼容型原型產品來維持市場佔有率,例如Worcester Bosch的產品,該產品已獲得認證,可使用含20%氫氣的混合氣體。同時,熱泵專家在私募股權的支持下,正在擴大其國內產能,這表明他們對英國供暖設備市場長期電氣化趨勢充滿信心。

預計到2025年,住宅領域將佔銷售額的58.41%,並將在2031年之前以7.52%的複合年成長率成長。這反映了英國龐大的家庭數量以及現有設備的老化。針對新建築的能源效率法規迫使開發商從一開始就採用低碳方案,而住宅在更換老舊鍋爐時也正在利用補貼。在商業房地產領域,ESG(環境、社會和治理)措施正在推動辦公大樓、零售商店和飯店設施的維修,但專案的複雜性可能會延長決策週期,預計英國整體供暖市場在短期內將保持溫和成長。

住宅領域的需求正成為技術創新的試驗場。據報道,Heat Geek 的最佳化型住宅熱泵系統產品組合,其季節性能比英國的典型安裝方案提升了 50%。在公共部門細分領域(學校、醫院、市政設施等),框架協議正被用於大規模採購低碳設備並共用維護專業知識。工業用戶優先考慮製程熱需求和可整合式爐灶技術,而資料中心則擴大評估使用液冷進行熱回收的技術,這表明英國供暖設備市場相關領域未來蘊藏著巨大的商機。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府支持脫碳的政策和獎勵

- 老化的鍋爐設備刺激了更換設備的需求。

- 提高效率的技術創新

- 綠色住宅金融產品正在加速維修。

- 都市區區域供熱網路的擴建

- 「供熱即服務」訂閱模式的出現。

- 市場限制因素

- 低碳暖氣系統的初始成本較高

- 先進設備技術純熟勞工短缺

- 農村地區電網容量的限制

- 氫能基礎設施的不確定性

- 產業生態系分析

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依設備類型

- 鍋爐

- 爐

- 熱泵

- 散熱器和其他類型的加熱器

- 按最終用戶行業分類

- 住宅

- 商業

- 產業

- 公共機構

- 按燃料類型

- 天然氣

- 電力

- 油

- 生質能

- 與氫相容

- 透過技術

- 濃縮版

- 非冷凝型

- 空氣源熱泵

- 地源熱泵

- 混合系統

- 智慧互聯系統

- 按安裝類型

- 新推出

- 更換/維修

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Robert Bosch GmbH(Worcester Bosch Group)

- Vaillant GmbH

- Ideal Boilers Ltd.

- Baxi Heating UK Ltd.

- Viessmann Werke GmbH and Co. KG

- Mitsubishi Electric Europe BV

- Daikin Industries Ltd.

- Trane Technologies plc

- Danfoss A/S

- Aermec SpA

- Clivet SpA

- Finn Geotherm UK Ltd.

- Systemair AB

- Swegon Group AB

- Rhoss SpA

- Grant Engineering(UK)Ltd.

- Kensa Heat Pumps Ltd.

- LG Electronics UK Ltd.

- Panasonic Heating and Cooling Solutions

- Stiebel Eltron GmbH and Co. KG

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom heating equipment market size is expected to grow from USD 4.06 billion in 2025 to USD 4.36 billion in 2026 and is forecast to reach USD 6.21 billion by 2031 at 7.32% CAGR over 2026-2031.

This report is Segmented by Equipment Type (Boilers, Furnaces, Heat Pumps, and More), End-User Industry (Residential, Commercial, and More), Fuel Type (Natural Gas, Electricity, Oil, and More), Technology (Condensing, Non-Condensing, and More), Installation Type (New Installation, and Replacement/Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Heating Equipment Market Trends and Insights

Supportive Government Decarbonisation Policies and Incentives

Expanded grants, technology-neutral eligibility, and flexible leasing options are reshaping purchasing behavior across the United Kingdom heating equipment market. The Department for Energy Security and Net Zero's consultation to widen the Boiler Upgrade Scheme now covers air-to-air units and heat batteries, aligning financial support with diverse property profiles. Coupled with a pledge to train 18,000 additional retrofit installers, the policy mix addresses both demand creation and supply-side capacity. March 2025 applications surged 88% year on year, signaling effective stimulus. Scotland's earlier 2045 Net Zero deadline amplifies local uptake, positioning policy as the single most powerful demand accelerator.

Ageing Boiler Stock Triggering Replacement Demand

More than 80% of U.K. homes were built before 1960, and many gas boilers installed during the 1990s now near end-of-life . This aging stock secures a baseline of predictable replacement volumes, driving 71.21% of current sales. Manufacturers exploit the cycle by offering hybrid packages that couple familiar gas units with add-on heat pumps compatible with existing pipework. As building codes tighten, each end-of-life event becomes an inflection point where owners weigh carbon and efficiency gains, sustaining both volume stability and technology upgrading within the United Kingdom heating equipment market.

High Upfront Cost of Low-Carbon Heating Systems

University of Edinburgh research found that average installed heat-pump prices have stagnated for a decade, leaving households with net costs of USD 6,500-14,000 even after grants. Properties needing electrical upgrades or radiator swaps see higher totals, deterring many until outright boiler failure. The economic barrier explains why replacement outpaces proactive retrofits despite policy support, curbing near-term acceleration of the United Kingdom heating equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Efficiency-Boosting Technology Innovations

- Green-Home Finance Products Accelerating Upgrades

- Skilled Labour Shortage for Advanced Installations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heat pumps are expanding at an 11.24% CAGR, steadily eroding the 37.65% share currently held by gas boilers. The United Kingdom heating equipment market size for heat pumps is set to widen as government rebates and high-temperature models enable retrofits without full radiator replacement. strengthening growth in the United Kingdom heat pumps market. Gas boilers persist due to lower capital outlay and installer familiarity, but forthcoming efficiency mandates tighten margins. Hybrid offerings combine both technologies, granting manufacturers a hedging strategy that balances present sales with future readiness. Furnaces and ancillary radiators maintain niche roles in industrial and large-commercial settings, providing steady though limited demand.

Gas-fired incumbents seek relevance through hydrogen-ready prototypes, exemplified by Worcester Bosch units certified for 20% hydrogen blends. Meanwhile, heat-pump specialists leverage private-equity backing to scale domestic capacity, signaling confidence in the long-term electrification trajectory of the United Kingdom heating equipment market.

The residential sector owned 58.41% revenue share in 2025 and is projected to expand at a 7.52% CAGR to 2031, reflecting both the sheer number of households and an aging installed base. Energy-efficiency rules for new builds are pushing developers toward low-carbon options from day one, while homeowners take advantage of grants when they replace legacy boilers. In commercial real estate, ESG commitments spur retrofits in offices, retail outlets, and hospitality venues, although project complexity can elongate decision cycles, moderating immediate growth rates across the United Kingdom heating equipment market.

Residential demand has become a proving ground for technology innovation. Heat Geek's portfolio of optimized residential heat-pump systems reportedly achieves 50% better seasonal performance than typical U.K. installations. The public-sector subsegment-schools, hospitals, and council buildings-leans on framework agreements to procure low-carbon equipment at scale and share maintenance expertise. Industrial users prioritize furnace technologies that can integrate with process heat requirements, whereas data centers increasingly evaluate liquid-cooling heat recovery, hinting at future adjacency opportunities within the United Kingdom heating equipment market.

Complete Report Scope:

- By Equipment Type

- Boilers

- Furnaces

- Heat Pumps

- Radiators and Other Heater Types

- By End-User Industry

- Residential

- Commercial

- Industrial

- Public/Institutional

- By Fuel Type

- Natural Gas

- Electricity

- Oil

- Biomass

- Hydrogen-Ready

- By Technology

- Condensing

- Non-Condensing

- Air Source Heat Pumps

- Ground Source Heat Pumps

- Hybrid Systems

- Smart Connected Systems

- By Installation Type

- New Installation

- Replacement/Retrofit

List of Companies Covered in this Report:

- Robert Bosch GmbH (Worcester Bosch Group)

- Vaillant GmbH

- Ideal Boilers Ltd.

- Baxi Heating UK Ltd.

- Viessmann Werke GmbH and Co. KG

- Mitsubishi Electric Europe B.V.

- Daikin Industries Ltd.

- Trane Technologies plc

- Danfoss A/S

- Aermec S.p.A.

- Clivet S.p.A.

- Finn Geotherm UK Ltd.

- Systemair AB

- Swegon Group AB

- Rhoss S.p.A.

- Grant Engineering (UK) Ltd.

- Kensa Heat Pumps Ltd.

- LG Electronics UK Ltd.

- Panasonic Heating and Cooling Solutions

- Stiebel Eltron GmbH and Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Supportive government decarbonisation policies and incentives

- 4.2.2 Ageing boiler stock triggering replacement demand

- 4.2.3 Efficiency-boosting technology innovations

- 4.2.4 Green-home finance products accelerating upgrades

- 4.2.5 Urban district-heat network expansion

- 4.2.6 Emergence of heat-as-a-service subscription models

- 4.3 Market Restraints

- 4.3.1 High upfront cost of low-carbon heating systems

- 4.3.2 Skilled labour shortage for advanced installations

- 4.3.3 Rural grid-capacity constraints

- 4.3.4 Hydrogen-infrastructure uncertainty

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Boilers

- 5.1.2 Furnaces

- 5.1.3 Heat Pumps

- 5.1.4 Radiators and Other Heater Types

- 5.2 By End-User Industry

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Public/Institutional

- 5.3 By Fuel Type

- 5.3.1 Natural Gas

- 5.3.2 Electricity

- 5.3.3 Oil

- 5.3.4 Biomass

- 5.3.5 Hydrogen-Ready

- 5.4 By Technology

- 5.4.1 Condensing

- 5.4.2 Non-Condensing

- 5.4.3 Air Source Heat Pumps

- 5.4.4 Ground Source Heat Pumps

- 5.4.5 Hybrid Systems

- 5.4.6 Smart Connected Systems

- 5.5 By Installation Type

- 5.5.1 New Installation

- 5.5.2 Replacement/Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Robert Bosch GmbH (Worcester Bosch Group)

- 6.4.2 Vaillant GmbH

- 6.4.3 Ideal Boilers Ltd.

- 6.4.4 Baxi Heating UK Ltd.

- 6.4.5 Viessmann Werke GmbH and Co. KG

- 6.4.6 Mitsubishi Electric Europe B.V.

- 6.4.7 Daikin Industries Ltd.

- 6.4.8 Trane Technologies plc

- 6.4.9 Danfoss A/S

- 6.4.10 Aermec S.p.A.

- 6.4.11 Clivet S.p.A.

- 6.4.12 Finn Geotherm UK Ltd.

- 6.4.13 Systemair AB

- 6.4.14 Swegon Group AB

- 6.4.15 Rhoss S.p.A.

- 6.4.16 Grant Engineering (UK) Ltd.

- 6.4.17 Kensa Heat Pumps Ltd.

- 6.4.18 LG Electronics UK Ltd.

- 6.4.19 Panasonic Heating and Cooling Solutions

- 6.4.20 Stiebel Eltron GmbH and Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

加熱設備市場:2026-2032年全球市場預測(依燃料類型、產品類型、機制、最終用戶及銷售管道分類)

加熱設備市場:2026-2032年全球市場預測(依燃料類型、產品類型、機制、最終用戶及銷售管道分類) 全球工業製程加熱市場:按燃氣加熱和電加熱、按地區分類 - 預測至 2032 年

全球工業製程加熱市場:按燃氣加熱和電加熱、按地區分類 - 預測至 2032 年 低頻加熱系統市場預測至2034年-按產品類型、類別、應用和地區分類的全球分析

低頻加熱系統市場預測至2034年-按產品類型、類別、應用和地區分類的全球分析 暖氣設備市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

暖氣設備市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 2026年全球熱泵混合式熱水箱市場報告熱風加熱器市場:2026-2032年全球市場預測(依燃料類型、安裝方式、容量範圍、最終用戶和銷售管道)熱水地暖系統市場:依產品類型、地板材料類型、最終用戶、應用和分銷管道分類-2026年至2032年全球預測分離式熱水熱泵市場:按類型、容量、安裝方式、效率、最終用戶和分銷管道分類,全球預測,2026-2032年

2026年全球熱泵混合式熱水箱市場報告熱風加熱器市場:2026-2032年全球市場預測(依燃料類型、安裝方式、容量範圍、最終用戶和銷售管道)熱水地暖系統市場:依產品類型、地板材料類型、最終用戶、應用和分銷管道分類-2026年至2032年全球預測分離式熱水熱泵市場:按類型、容量、安裝方式、效率、最終用戶和分銷管道分類,全球預測,2026-2032年 亞太地區工業供熱系統市場按應用、產品和國家分類-分析與預測(2025-2035 年)

亞太地區工業供熱系統市場按應用、產品和國家分類-分析與預測(2025-2035 年) 歐洲工業暖氣系統市場按應用、產品和國家分類-分析與預測(2025-2035 年)

歐洲工業暖氣系統市場按應用、產品和國家分類-分析與預測(2025-2035 年)