|

市場調查報告書

商品編碼

2073581

亞太地區策略諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Asia Pacific Strategic Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

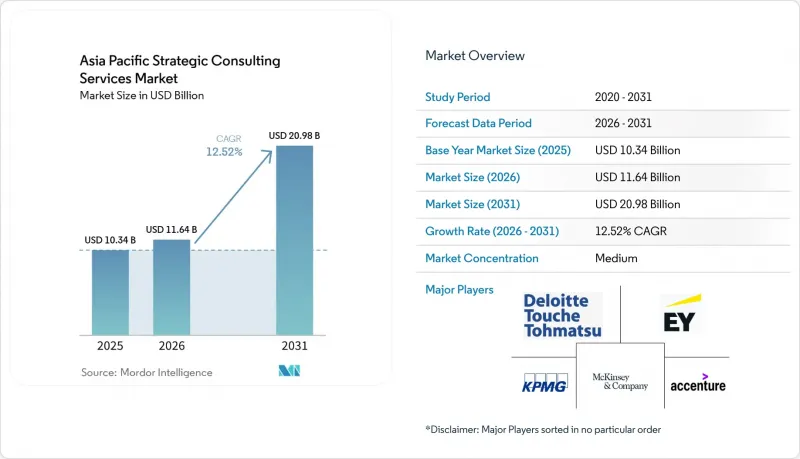

據 Mordor Intelligence 稱,亞太地區的策略諮詢服務市場預計到 2026 年將達到 116.4 億美元,高於 2025 年的 103.4 億美元,預計到 2031 年將達到 209.8 億美元。

預計 2026 年至 2031 年的複合年成長率為 12.52%。

本報告按服務類型(企業策略、數位化策略等)、終端用戶產業(金融服務、零售/消費品等)、公司規模(大型企業、中小企業)、交付模式(現場諮詢、遠端/虛擬諮詢等)和地區進行細分。市場預測以美元計價。

亞太地區策略諮詢服務市場趨勢及洞察。

席捲亞太地區的數位轉型浪潮

為因應疫情帶來的衝擊,亞太地區的企業正加速數位投入。先前一直處於線下營運狀態的企業中,有44%計畫在2025年實現超過一半非自動化流程的自動化。顧問公司正抓住這項機遇,將人工智慧融入整個專案生命週期,透過數據驅動的策略衝刺,將運轉率提升高達50%,並縮短專案週期。監管機構也積極引導市場需求。新加坡金融管理局發布了轉型規劃指南,日本金融廳也發布了人工智慧驅動的框架,鼓勵提供系統化的諮詢支援。由於客戶更傾向於擁有眾多專家的團隊,各公司正從金字塔形的人員結構轉向菱形結構,擴大對中層人才和專業人才的招聘,並重塑亞太地區整個戰略諮詢服務市場的人才經濟格局。

跨國併購和企業重組交易激增。

供應鏈多元化和地緣政治格局重組正推動該地區交易量在2024年達到多年來的最高水平,從而激發交易戰略工作的活力。應對不同監管法規和國家安全審查的複雜性,使得擁有紮實本地經驗和協作工具的諮詢團隊擁有明顯的優勢。以技術主導的收購,例如IBM以64億美元收購HashiCorp,凸顯了軟體能力對公司估值標準的影響。同時,與風險緩解策略相關的分拆和剝離進一步擴大了業務重組交易的範圍。因此,顧問公司正在正式組成地緣政治策略團隊,將宏觀風險訊號轉化為東協、日本和澳洲等地的董事會層面行動計畫。

大型企業客戶的價格敏感度正在提高。

為因應宏觀經濟的不確定性,高層採購人員正在重新協商收費系統,轉向基於結果的定價和更短的專案週期。企業則以固定價格模式應對,並輔以詳細的投資報酬率基準和人工智慧驅動的交付加速器,從而在綜合單位成本下降的情況下維持利潤率。對專業人才的日益重視進一步降低了對初級員工的需求,加劇了對中級人才的競爭,並促進了校友網路向自由工作者市場輸送人才。

細分市場分析

2025年,數位化策略領域將佔亞太地區策略諮詢服務市場規模的27.20%,並持續成為企業轉型專案的標竿。其主導地位源自於人工智慧的整合、數據現代化以及平台型經營模式,這些都帶來了可量化的收入成長和成本效益。環境、社會與治理(ESG)及永續發展諮詢雖然目前規模較小,但其複合年成長率(CAGR)高達13.05%,隨著揭露義務將環境指標納入董事會議程,預計將逐步蠶食傳統的企業策略預算。併購策略正受益於供應鏈和地緣政治重組的浪潮,推動了對綜合交易策略的需求。風險與合規工作依然強勁,這得益於亞太地區各司法管轄區日益嚴格的洗錢防制標準、網路安全法規以及不斷擴展的數位主權法律。

服務供應商正透過利用特定產業的加速器和獨特的數據資產來縮短洞察時間,從而實現差異化競爭。例如,碳核算平台正被整合到ESG(環境、社會和治理)計劃中,而數位雙胞胎技術正在加速製造策略的發展。這些工具透過訂閱和管理服務模式產生持續的收入來源,逐步改變收入結構,使其不再僅基於時間和材料計費。同時,在亞太戰略諮詢服務市場,顧問公司正在剝離專注於數位策略和永續發展等細分領域的專業分支機構,以維持高階定價和品牌清晰度。

2025年,隨著銀行、保險公司和資本市場營運商巧妙應對數位化變革和監管挑戰,金融機構將在亞太地區策略諮詢服務市場佔據24.12%的佔有率。金融科技合作、開放銀行介面和嵌入式金融生態系統需要整合技術、營運和合規層面的複雜轉型計畫。同時,在人口結構變化、遠端醫療普及和生物技術投資增加的推動下,生命科學和醫療保健產業正以13.70%的複合年成長率加速成長。科技、媒體和電信(TMT)公司持續尋求關於5G平台、人工智慧驅動的內容產生和資料隱私要求的指導,而製造業客戶則要求制定包含脫碳里程碑的工業4.0藍圖。

產業專業化正在重塑服務交付團隊的性質。例如,在臨床研究和資料科學、支付系統和網路安全等兩個領域擁有專業知識的顧問,如今收費高昂。政府客戶選擇性地委託智慧城市和公共財政轉型項目,但整體成長受到預算限制。在所有行業中,貸款發放速度、患者用藥依從率和減排放等績效指標正被納入合約條款,基於結果的合約模式正在亞太地區的策略諮詢服務市場中逐漸確立。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 亞太地區的數位轉型浪潮

- 跨國併購和企業重組交易激增。

- ESG和永續發展藍圖的需求日益成長

- 嵌入式金融帶來的變革正在推動支付策略的發展。

- 自由職業顧問的供需不匹配正在催生新的服務交付模式。

- 重工業供應鏈脫碳(CBAM 的連鎖反應)

- 市場限制因素

- 大型企業客戶對價格的敏感度提高

- 大型科技公司和IT服務公司之間的競爭日益激烈。

- 客戶對生成式人工智慧諮詢的投資報酬率持懷疑態度。

- 區域人才流失(人才流失到自由工作者或內部策略團隊)

- 產業生態系分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 按服務類型

- 企業策略

- 數位策略

- 商業策略

- 併購和業務重組

- 永續發展與ESG戰略

- 風險與合規策略

- 按最終用戶行業分類

- 金融服務

- 生命科學與醫療保健

- 零售商和消費者

- 政府/公共部門

- 能源公用事業

- 製造業

- 科技、媒體與通訊

- 其他終端用戶產業

- 按公司規模

- 大公司

- 中小企業

- 按型號提供

- 現場諮詢

- 遠端/虛擬諮詢

- 混合諮詢

- 國家

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 新加坡

- 印尼

- 馬來西亞

- 泰國

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- McKinsey and Company

- Boston Consulting Group

- Bain and Company

- AT Kearney Inc.

- Deloitte Touche Tohmatsu Limited

- Ernst and Young Global Limited

- KPMG International Limited

- PricewaterhouseCoopers International Limited

- Accenture plc

- Mercer LLC

- Oliver Wyman Group

- Roland Berger Holding GmbH

- LEK Consulting LLC

- Capgemini Invent

- IBM Consulting

- Monitor Deloitte

- Arthur D. Little

- Nomura Research Institute Ltd.

- Frost and Sullivan Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, asia pacific strategic consulting services market size in 2026 is estimated at USD 11.64 billion, growing from 2025 value of USD 10.34 billion with 2031 projections showing USD 20.98 billion, growing at 12.52% CAGR over 2026-2031.

This report is Segmented by Service Type (Corporate Strategy, Digital Strategy, and More), End-User Industry (Financial Services, Retail and Consumer, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Delivery Model (On-Site Consulting, Remote/Virtual Consulting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific Strategic Consulting Services Market Trends and Insights

Digital-transformation wave across Asia Pacific

Enterprises in the region accelerated digital spending following pandemic disruptions, with 44% of previously offline organizations planning to automate over half their non-automated processes by 2025. Consulting firms are seizing the opportunity by embedding AI throughout project lifecycles, raising utilization rates by up to 50% and enabling data-rich strategy sprints that shorten engagement timelines. Regulators are also shaping demand: Singapore's Monetary Authority issued transition planning guidelines, and Japan's Financial Services Agency published AI use frameworks that encourage structured advisory support. As clients favor expert-heavy teams, firms are migrating from pyramid to diamond staffing, pushing mid-level and specialist hiring higher and redefining talent economics across the Asia Pacific strategic consulting services market.

Surge in cross-border M and A and restructuring mandates

Supply-chain diversification and geopolitical realignment lifted regional deal volumes to multi-year highs in 2024, energizing transaction strategy practices. The complexity of navigating disparate regulatory codes and national security reviews gives a distinct edge to advisory teams with deep local credentials and collaborative toolsets. Technology-driven acquisitions such as IBM's USD 6.4 billion HashiCorp purchase underscore how software capabilities influence valuation thresholds, while spin-offs and carve-outs linked to de-risking strategies further expand restructuring pipelines. As a result, consultancies are formalizing geostrategy cells that translate macro risk signals into board-level action plans across ASEAN, Japan, and Australia.

Rising price sensitivity among large enterprise clients

C-suite buyers are renegotiating fee structures in response to macro uncertainty, shifting toward outcome-based pricing and shorter project cycles. Firms are countering with fixed-fee models underpinned by detailed ROI baselines and AI-enabled delivery accelerators that sustain margins even at lower blended rates. The emphasis on specialist staffing further compresses junior demand, intensifying the search for mid-level talent and fostering alumni networks that feed freelance marketplaces.

Other drivers and restraints analyzed in the detailed report include:

- Escalating demand for ESG / sustainability road-maps

- Embedded-finance disruption driving payments strategy work

- Intensifying competition from Big Tech and IT-services firms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The digital strategy segment contributed 27.20% to Asia Pacific strategic consulting services market size in 2025 and remains the reference point for enterprise reinvention programs. Its dominance is rooted in AI integration, data modernization, and platform business model expansion that deliver quantifiable revenue lifts and cost efficiencies. ESG and sustainability consulting, though smaller today, is posting a 13.05% CAGR and is expected to chip away at traditional corporate strategy budgets, as disclosure mandates embed environmental metrics into boardroom agendas. M and A strategy rides the wave of supply-chain and geopolitical realignments, reinforcing demand for integrative transaction playbooks. Risk and compliance work remains resilient, fueled by tightening anti-money-laundering standards, cyber regulations, and digital sovereignty laws proliferating across Asia Pacific jurisdictions.

Service providers are differentiating by sector-specific accelerators and proprietary data assets that compress time to insight. For example, carbon-accounting platforms are embedded into ESG engagements, while digital twins accelerate manufacturing strategy design. These tools create recurring revenue streams via subscription or managed-service models, subtly shifting revenue mixes away from pure time-and-materials billing. In parallel, the Asia Pacific strategic consulting services market is witnessing consultancies spinning off specialist boutiques to maintain premium pricing and brand clarity in digital strategy and sustainability niches.

Financial institutions captured 24.12% of Asia Pacific strategic consulting services market share in 2025 as banks, insurers, and capital-market operators navigated digital disruption and regulatory tightrope walks. Fintech collaborations, open-banking interfaces, and embedded finance ecosystems require intricate transition blueprints that integrate technology, operations, and compliance layers. Life sciences and healthcare, meanwhile, is accelerating at a 13.70% CAGR, underpinned by demographic shifts, telehealth diffusion, and rising biotech investment. TMT players continue to seek guidance on 5G-enabled platforms, AI content generation, and data-privacy imperatives, while manufacturing clients demand Industry 4.0 roadmaps with decarbonization milestones.

Sector specialization is redefining delivery teams: consultants with dual backgrounds in, for instance, clinical research and data science, or payments operations and cybersecurity, now command premium billing rates. Government clients are selectively commissioning smart-city and public-finance transformation projects, although budget constraints temper overall growth. Across sectors, outcome metrics such as loan origination speed, patient adherence, or emissions reduction are baked into contracting terms, reinforcing result-based engagement models in the Asia Pacific strategic consulting services market.

Complete Report Scope:

- By Service Type

- Corporate Strategy

- Digital Strategy

- Operations Strategy

- M&A and Restructuring

- Sustainability and ESG Strategy

- Risk and Compliance Strategy

- By End-User Industry

- Financial Services

- Life Sciences and Healthcare

- Retail and Consumer

- Government and Public Sector

- Energy and Utilities

- Manufacturing

- Technology Media and Telecommunications

- Other End-User Industries

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Delivery Model

- On-site Consulting

- Remote / Virtual Consulting

- Hybrid Consulting

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Singapore

- Indonesia

- Malaysia

- Thailand

- Rest of Asia Pacific

List of Companies Covered in this Report:

- McKinsey and Company

- Boston Consulting Group

- Bain and Company

- A.T. Kearney Inc.

- Deloitte Touche Tohmatsu Limited

- Ernst and Young Global Limited

- KPMG International Limited

- PricewaterhouseCoopers International Limited

- Accenture plc

- Mercer LLC

- Oliver Wyman Group

- Roland Berger Holding GmbH

- L.E.K. Consulting LLC

- Strategy& (part of PwC)

- Capgemini Invent

- IBM Consulting

- Monitor Deloitte

- Arthur D. Little

- Nomura Research Institute Ltd.

- Frost and Sullivan Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital-transformation wave across Asia Pacific

- 4.2.2 Surge in cross-border M&A and restructuring mandates

- 4.2.3 Escalating demand for ESG/sustainability road-maps

- 4.2.4 Embedded-finance disruption driving payments strategy work

- 4.2.5 Freelance-consultant supply mismatch enabling new delivery models

- 4.2.6 Heavy-industry supply-chain decarbonisation (CBAM spill-overs)

- 4.3 Market Restraints

- 4.3.1 Rising price sensitivity among large enterprise clients

- 4.3.2 Intensifying competition from Big Tech and IT-services firms

- 4.3.3 Client skepticism on Gen-AI consulting ROI

- 4.3.4 Regional talent drain to freelance / in-house strategy teams

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Corporate Strategy

- 5.1.2 Digital Strategy

- 5.1.3 Operations Strategy

- 5.1.4 M&A and Restructuring

- 5.1.5 Sustainability and ESG Strategy

- 5.1.6 Risk and Compliance Strategy

- 5.2 By End-User Industry

- 5.2.1 Financial Services

- 5.2.2 Life Sciences and Healthcare

- 5.2.3 Retail and Consumer

- 5.2.4 Government and Public Sector

- 5.2.5 Energy and Utilities

- 5.2.6 Manufacturing

- 5.2.7 Technology Media and Telecommunications

- 5.2.8 Other End-User Industries

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Delivery Model

- 5.4.1 On-site Consulting

- 5.4.2 Remote / Virtual Consulting

- 5.4.3 Hybrid Consulting

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Australia

- 5.5.5 South Korea

- 5.5.6 Singapore

- 5.5.7 Indonesia

- 5.5.8 Malaysia

- 5.5.9 Thailand

- 5.5.10 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 McKinsey and Company

- 6.4.2 Boston Consulting Group

- 6.4.3 Bain and Company

- 6.4.4 A.T. Kearney Inc.

- 6.4.5 Deloitte Touche Tohmatsu Limited

- 6.4.6 Ernst and Young Global Limited

- 6.4.7 KPMG International Limited

- 6.4.8 PricewaterhouseCoopers International Limited

- 6.4.9 Accenture plc

- 6.4.10 Mercer LLC

- 6.4.11 Oliver Wyman Group

- 6.4.12 Roland Berger Holding GmbH

- 6.4.13 L.E.K. Consulting LLC

- 6.4.14 Strategy& (part of PwC)

- 6.4.15 Capgemini Invent

- 6.4.16 IBM Consulting

- 6.4.17 Monitor Deloitte

- 6.4.18 Arthur D. Little

- 6.4.19 Nomura Research Institute Ltd.

- 6.4.20 Frost and Sullivan Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

2026年全球營運諮詢市場報告

2026年全球營運諮詢市場報告 諮詢4.0市場:2026-2032年全球預測(依產品類型、技術、應用、最終用戶及通路分類)

諮詢4.0市場:2026-2032年全球預測(依產品類型、技術、應用、最終用戶及通路分類) 南美供應鏈諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

南美供應鏈諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 保險諮詢服務市場規模、佔有率和趨勢分析報告:按服務類型、保險類型、最終用戶、地區和細分市場預測(2026-2033 年)企業敏捷轉型服務市場:2026-2032年全球市場預測(依服務類型、調查方法、轉型階段、合約模式、部署模式、產業及組織規模分類)2026年全球IT諮詢市場報告2026年全球企業敏捷轉型服務市場報告

保險諮詢服務市場規模、佔有率和趨勢分析報告:按服務類型、保險類型、最終用戶、地區和細分市場預測(2026-2033 年)企業敏捷轉型服務市場:2026-2032年全球市場預測(依服務類型、調查方法、轉型階段、合約模式、部署模式、產業及組織規模分類)2026年全球IT諮詢市場報告2026年全球企業敏捷轉型服務市場報告 企業敏捷轉型服務市場規模、佔有率、趨勢和預測:按方法論、服務類型、組織規模、產業和地區分類,2026-2034 年2026年全球公司秘書服務市場報告2026年全球房地產諮詢服務市場報告

企業敏捷轉型服務市場規模、佔有率、趨勢和預測:按方法論、服務類型、組織規模、產業和地區分類,2026-2034 年2026年全球公司秘書服務市場報告2026年全球房地產諮詢服務市場報告