|

市場調查報告書

商品編碼

2063410

南美供應鏈諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)South America Supply Chain Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

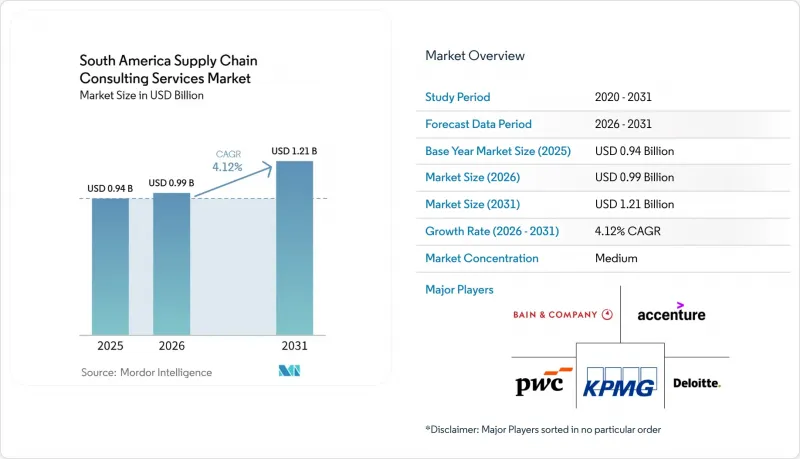

據 Mordor Intelligence 稱,2025 年南美供應鏈諮詢服務市值為 9.41 億美元,預計到 2031 年將從 2026 年的 9.87 億美元成長至 12.08 億美元,預測期(2026-2031 年)的複合年成長率為 4.12%。

本報告按服務類型(供應鏈策略和網路設計、採購和尋源等)、最終用戶行業(零售和電子商務、製造業等)、諮詢方式(企劃為基礎諮詢、管理服務等)、組織規模(大型企業、中小企業)和地區進行細分。市場預測以價值(美元)為單位。

南美洲供應鏈諮詢服務市場的趨勢與洞察

擴大數位化供應鏈轉型的應用

企業正將分散的ERP、採購和物流系統整合到雲端平台上,這些平台整合了人工智慧技術,用於流程編配和預測分析。淡水河谷(Vale)在Coupa平台上實施的整合20多種採購工具的項目,年支出高達140億美元,顯示大型資產密集型企業正從先導計畫轉向大規模實施。製藥公司Uniao KIMICA也採取了類似的策略,利用SAP Ariba平台,目標是在2026年5月運作一個具備智慧提案評估功能的系統。基於代理的人工智慧實驗也在該地區取得進展,YPF和Globant在其採購和庫存管理工作流程中部署了46個數位代理,使員工能夠專注於策略採購。顧問公司也從中受益,因為許多公司需要外部協助來設計資料架構、重新設計流程和實施變革管理方案。

公司整體成本最佳化的必要性

該地區物流效率低下持續從根本上影響盈利,成本幾乎是已開發經濟體的兩倍。亞馬遜巴西的 Cosmic Frog 等平台被用於情境建模,顯示托運人正在量化速度、服務和成本之間的權衡。一項針對零售業高管的調查發現,如果貿易相關成本上升,66% 的高階主管計劃重組其網路或實現供應商多元化,這催生了大量專注於網路設計和庫存最佳化的諮詢項目。美洲開發銀行 (IDB) 估計,數位化可以將物流成本降低高達 15%,這為顧問公司用來促成交易的具體投資報酬率 (ROI) 論點提供了佐證。

熟練的供應鏈專家短缺

根據經合組織的一項調查,中小企業承擔著許多極易被自動化取代的日常工作,但它們卻缺乏接受高級培訓的機會,導致數據分析和程式工程人才短缺。畢馬威會計師事務所警告稱,巴西和阿根廷的人才短缺限制了諮詢項目的擴充性,因為這些項目會延長工期並提高日薪。為了緩解這個問題,一些公司正在舉辦能力建構訓練營,並與大學合作開發初級分析師的培訓計畫。

細分市場分析

到2025年,數位化供應鏈轉型將佔南美供應鏈諮詢服務市場佔有率的21.78%,凸顯了企業對端到端可視性和人工智慧驅動決策引擎的重視。淡水河谷(Vale)旨在實現90多項內部控制自動化的項目,展現了其多年數位轉型工作的規模。亞馬遜巴西的即時網路孿生模型正在持續測試履約方案,進一步刺激了市場需求。儘管目前永續發展和綠色供應鏈舉措的規模仍然較小,但預計到2031年將以7.31%的複合年成長率成長。這主要得益於政府支持的綠色債券稅額扣抵以及以巴西幣的稅收抵免為脫碳藍圖提供的資金支持。因此,顧問公司正在將碳核算模組整合到其核心轉型工作中,從而縮短投資回收期,並擴大南美供應鏈諮詢服務市場中與環境、社會和治理(ESG)相關的服務。

除了這兩個成長最快的領域之外,網路設計和採購最佳化仍然持續受到青睞。美洲開發銀行預測出口額可能增加780億美元,這推動了企業選址分析的更新,而YPF基於代理的人工智慧實驗表明,供應商評估正朝著自主化方向發展。風險和韌性建模進一步完善了服務組合,客戶要求部署數位雙胞胎模型,以疊加網路、氣候和地緣政治壓力測試。這些成長表明,南美洲供應鏈諮詢服務市場正持續從孤立的諮詢服務轉型為整合的平台驅動型解決方案。

到2025年,製造業將佔南美洲供應鏈諮詢服務市場的35.59%,主要得益於複雜的汽車和採礦價值鏈。 2024年,巴西汽車零件銷售額達到2,591億雷亞爾(約508億美元),引發了大量專注於供應商精簡和包裝重新設計的諮詢項目。礦業巨頭正致力於提升加工能力和數位化許可證獲取,秘魯價值515.5億美元的專案儲備便是最好的例證,這些專案正日益將數位化融入其供應鏈。能源和公共產業產業雖然規模較小,但卻是成長最快的產業,年複合成長率達6.02%。這主要歸功於國際可再生能源機構(IRENA)的預測,到2050年,每年需要5,000億美元的可再生能源投資。這一成長正在擴大南美洲供應鏈諮詢服務市場,該市場專注於電網物流、電解槽採購和氫能走廊規劃等領域。

零售和電商產業正經歷履約中心擴張的浪潮。 CEVA 為亞馬遜建造的 6.7 萬平方公尺的物流中心(日處理能力達 13.5 萬個包裹)充分展現了全通路品牌對流程設計和倉儲自動化的規模需求。製藥、食品和飲料公司也紛紛聘請顧問,以實現低溫運輸現代化、遵守有關再生材料含量的法規並整合序列化流程。即使產品市場週期放緩,多元化的客戶群也支撐著強勁的收入基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大數位化供應鏈轉型的應用

- 公司整體成本最佳化的必要性

- 區域貿易法規日益複雜

- 近岸外包趨勢推動區域供應鏈重組

- 區域城市電子商務履約中心的快速擴張

- 政府對綠色物流舉措的獎勵

- 市場限制因素

- 熟練的供應鏈專家短缺

- 中小企業諮詢費過高

- 政治不穩定可能會影響長期諮詢合約。

- 基礎設施碎片化限制了諮詢實施的投資報酬率。

- 宏觀經濟因素對市場的影響

- 產業生態系分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 供應鏈策略與網路設計

- 採購與尋源

- 最佳化物流和配送

- 庫存和需求計劃

- 數位化供應鏈轉型

- 永續性和綠色供應鏈

- 風險與韌性諮詢

- 其他服務類型

- 按最終用戶行業分類

- 零售與電子商務

- 製造業

- 食品/飲料

- 醫療和藥品

- 車

- 面向消費者的包裝商品

- 能源公用事業

- 其他終端用戶產業

- 透過諮商方法

- 企劃為基礎的諮詢

- 託管服務

- 培訓和技能發展

- 諮詢和基準測試

- 其他諮詢方法

- 按組織規模

- 大公司

- 小型企業

- 按地區

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- Deloitte Touche Tohmatsu Ltd

- KPMG International Ltd

- PricewaterhouseCoopers International Ltd

- Bain & Company Inc.

- Boston Consulting Group Inc.

- McKinsey & Company Inc.

- Ernst & Young Global Ltd

- International Business Machines Corporation(IBM Consulting)

- Capgemini SE

- Genpact Limited

- Chainalytics LLC

- NTT DATA Corporation

- Oliver Wyman Inc.

- AlixPartners LLP

- Kearney

- Infosys Limited

- Tata Consultancy Services Limited

- GEP Worldwide

- Alvarez & Marsal Holdings LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america supply chain consulting services market size was valued at USD 0.941 billion in 2025 and estimated to grow from USD 0.987 billion in 2026 to reach USD 1.208 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031).

This report is Segmented by Service Type (Supply Chain Strategy and Network Design, Procurement and Sourcing, and More), End-User Industry (Retail and Ecommerce, Manufacturing, and More), Consulting Approach (Project-Based Consulting, Managed Services, and More), Organization Size (Large Enterprises, Smes), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America Supply Chain Consulting Services Market Trends and Insights

Rising Adoption of Digital Supply Chain Transformation

Enterprises are consolidating fragmented ERP, procurement, and logistics systems onto cloud platforms that embed AI for process orchestration and predictive analytics. Vale's program to unify more than 20 purchasing tools under Coupa, covering USD 14 billion in annual spend, showcases how large asset-heavy firms are moving from pilot projects to scaled execution. Pharmaceutical manufacturer Uniao Quimica is following a similar path with SAP Ariba, targeting a May 2026 go-live that adds intelligent proposal evaluation. The region is also experimenting with agentic AI, as YPF and Globant deployed 46 digital agents across procurement and inventory workflows, freeing staff for strategic sourcing. Consulting firms benefit because most enterprises need external support to blueprint data architecture, redesign processes, and run change-management programs.

Need for Cost Optimization Across Enterprises

Regional logistics inefficiencies remain a structural drain on profitability, with costs sitting at almost double those in developed economies. Platform deployments such as Amazon Brazil's use of Optilogic's Cosmic Frog for scenario modeling illustrate how shippers are quantifying trade-offs among speed, service, and cost. Surveys of retail executives indicate that 66% plan to reconfigure their networks or diversify suppliers if trade-related costs rise, feeding a robust pipeline of consulting engagements focused on network design and inventory rightsizing. The Inter-American Development Bank estimates digitalization can shave up to 15% off logistics costs, underscoring the tangible ROI narrative that consultants use to close deals.

Shortage of Skilled Supply Chain Professionals

OECD research shows that SMEs perform most routine tasks at high risk of automation yet lack access to advanced training programs, leaving a gap in data analytics and process-engineering talent. KPMG warns that staffing constraints lengthen project timelines and raise day rates across Brazil and Argentina, limiting the scalability of consulting engagements. To mitigate, firms are launching capacity-building boot camps and partnering with universities to create feeder programs for junior analysts.

Other drivers and restraints analyzed in the detailed report include:

- Nearshoring Trends Driving Regional Supply Chain Reconfiguration

- Government Incentives for Green Logistics Initiatives

- High Consulting Fees for Small and Medium Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital Supply Chain Transformation captured 21.78% of the South America supply chain consulting services market share in 2025, underscoring companies' prioritization of end-to-end visibility and AI-driven decision engines. Vale's program to automate more than 90 internal controls underscores the scale of multi-year digital mandates. Demand is reinforced by Amazon Brazil's real-time network twin, which continuously tests fulfillment scenarios. Sustainability and Green Supply Chain mandates, although smaller, are expanding at a 7.31% CAGR to 2031 as sovereign green-bond proceeds and BRL-denominated tax credits finance decarbonization roadmaps. Consultants are thus integrating carbon accounting modules into core transformation work, shortening payback horizons and widening the South America supply chain consulting services market size for ESG-linked offerings.

Beyond the two fastest-moving areas, network design and procurement optimization remain evergreen lines. IDB's projection of a potential USD 78 billion export uplift drives renewals of footprint analyses, while YPF's agentic AI experiment signals a pivot toward autonomous supplier evaluation. The service mix is rounded out by risk and resilience modeling, with clients requesting digital twins that overlay cyber, climate, and geopolitical stress tests. These expansions illustrate how the South America supply chain consulting services market continues to evolve from siloed advisory toward integrated, platform-enabled solutions.

Manufacturing commanded 35.59% of the South America supply chain consulting services market in 2025, led by complex automotive and mining value chains. Brazil's auto-parts revenue reached BRL 259.1 billion (USD 50.8 billion) in 2024, drawing consulting assignments in supplier rationalization and packaging redesign. Mining majors seek throughput gains and digital permitting, illustrated by Peru's USD 51.55 billion project pipeline that increasingly embeds supply-chain digitization. Energy and utilities, while smaller, is the fastest-growing vertical at 6.02% CAGR as IRENA forecasts USD 500 billion in annual renewable investment needs through 2050. This growth enlarges the South America supply chain consulting services market size devoted to grid logistics, electrolyser sourcing, and hydrogen corridor planning.

Retail and e-commerce engagements are riding a wave of fulfillment-center expansion. CEVA's 67,000 square-meter Amazon site, capable of 135,000 daily packages, showcases the scale at which omnichannel brands require process mapping and warehouse automation. Pharma, food, and beverage firms are likewise hiring consultants to modernize cold chains, comply with recycled-content mandates, and integrate serialization. The broadening client mix underpins a resilient revenue base even when commodity cycles soften.

List of Companies Covered in this Report:

- Accenture plc

- Deloitte Touche Tohmatsu Ltd

- KPMG International Ltd

- PricewaterhouseCoopers International Ltd

- Bain & Company Inc.

- Boston Consulting Group Inc.

- McKinsey & Company Inc.

- Ernst & Young Global Ltd

- International Business Machines Corporation (IBM Consulting)

- Capgemini SE

- Genpact Limited

- Chainalytics LLC

- NTT DATA Corporation

- Oliver Wyman Inc.

- AlixPartners LLP

- Kearney

- Infosys Limited

- Tata Consultancy Services Limited

- GEP Worldwide

- Alvarez & Marsal Holdings LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Digital Supply Chain Transformation

- 4.2.2 Need for Cost Optimization Across Enterprises

- 4.2.3 Increasing Complexity of Regional Trade Regulations

- 4.2.4 Nearshoring Trends Driving Regional Supply Chain Reconfiguration

- 4.2.5 Rapid Growth of E-commerce Fulfillment Hubs in Secondary Cities

- 4.2.6 Government Incentives for Green Logistics Initiatives

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Supply Chain Professionals

- 4.3.2 High Consulting Fees for Small and Medium Enterprises

- 4.3.3 Political Instability Affecting Long-Term Consulting Contracts

- 4.3.4 Fragmented Infrastructure Limiting Consulting Implementation ROI

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Ecosystem Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Supply Chain Strategy and Network Design

- 5.1.2 Procurement and Sourcing

- 5.1.3 Logistics and Distribution Optimization

- 5.1.4 Inventory and Demand Planning

- 5.1.5 Digital Supply Chain Transformation

- 5.1.6 Sustainability and Green Supply Chain

- 5.1.7 Risk and Resilience Consulting

- 5.1.8 Other Service Types

- 5.2 By End-User Industry

- 5.2.1 Retail and E-commerce

- 5.2.2 Manufacturing

- 5.2.3 Food and Beverage

- 5.2.4 Healthcare and Pharmaceuticals

- 5.2.5 Automotive

- 5.2.6 Consumer Packaged Goods

- 5.2.7 Energy and Utilities

- 5.2.8 Other End-User Industries

- 5.3 By Consulting Approach

- 5.3.1 Project-Based Consulting

- 5.3.2 Managed Services

- 5.3.3 Training and Capacity Building

- 5.3.4 Advisory and Benchmarking

- 5.3.5 Other Consulting Approaches

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Deloitte Touche Tohmatsu Ltd

- 6.4.3 KPMG International Ltd

- 6.4.4 PricewaterhouseCoopers International Ltd

- 6.4.5 Bain & Company Inc.

- 6.4.6 Boston Consulting Group Inc.

- 6.4.7 McKinsey & Company Inc.

- 6.4.8 Ernst & Young Global Ltd

- 6.4.9 International Business Machines Corporation (IBM Consulting)

- 6.4.10 Capgemini SE

- 6.4.11 Genpact Limited

- 6.4.12 Chainalytics LLC

- 6.4.13 NTT DATA Corporation

- 6.4.14 Oliver Wyman Inc.

- 6.4.15 AlixPartners LLP

- 6.4.16 Kearney

- 6.4.17 Infosys Limited

- 6.4.18 Tata Consultancy Services Limited

- 6.4.19 GEP Worldwide

- 6.4.20 Alvarez & Marsal Holdings LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球營運諮詢市場報告

2026年全球營運諮詢市場報告 諮詢4.0市場:2026-2032年全球預測(依產品類型、技術、應用、最終用戶及通路分類)

諮詢4.0市場:2026-2032年全球預測(依產品類型、技術、應用、最終用戶及通路分類) 保險諮詢服務市場規模、佔有率和趨勢分析報告:按服務類型、保險類型、最終用戶、地區和細分市場預測(2026-2033 年)企業敏捷轉型服務市場:2026-2032年全球市場預測(依服務類型、調查方法、轉型階段、合約模式、部署模式、產業及組織規模分類)2026年全球IT諮詢市場報告2026年全球企業敏捷轉型服務市場報告

保險諮詢服務市場規模、佔有率和趨勢分析報告:按服務類型、保險類型、最終用戶、地區和細分市場預測(2026-2033 年)企業敏捷轉型服務市場:2026-2032年全球市場預測(依服務類型、調查方法、轉型階段、合約模式、部署模式、產業及組織規模分類)2026年全球IT諮詢市場報告2026年全球企業敏捷轉型服務市場報告 企業敏捷轉型服務市場規模、佔有率、趨勢和預測:按方法論、服務類型、組織規模、產業和地區分類,2026-2034 年2026年全球公司秘書服務市場報告2026年全球房地產諮詢服務市場報告2026年全球精算諮詢服務市場報告

企業敏捷轉型服務市場規模、佔有率、趨勢和預測:按方法論、服務類型、組織規模、產業和地區分類,2026-2034 年2026年全球公司秘書服務市場報告2026年全球房地產諮詢服務市場報告2026年全球精算諮詢服務市場報告