|

市場調查報告書

商品編碼

2073573

印度彈性辦公空間:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Flexible Office Space - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

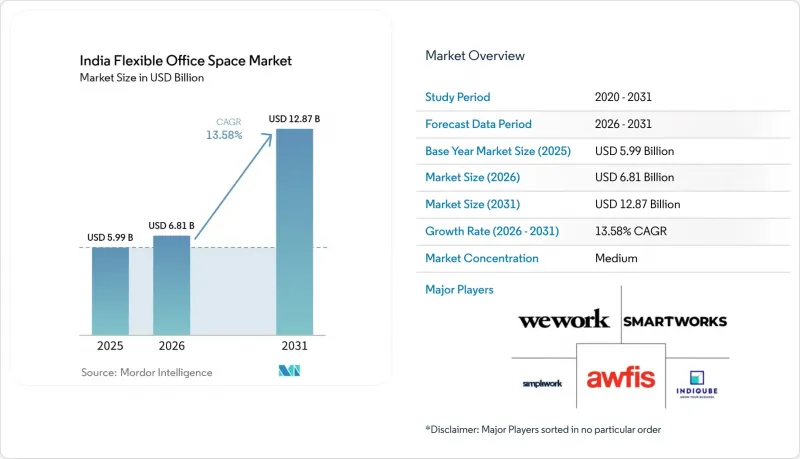

據 Mordor Intelligence 稱,印度靈活辦公空間市場預計到 2026 年價值 68.1 億美元,高於 2025 年的 59.9 億美元,預計到 2031 年將達到 128.7 億美元。

預計 2026 年至 2031 年的複合年成長率為 13.58%。

本報告按類型(共享辦公空間、服務式辦公室/行政套房等)、行業(資訊科技(IT 和 ITES)等)、最終用戶(企業、自由工作者、新創公司等)和城市(孟買大都會圈、班加羅爾、浦那等)進行細分。報告針對以上所有細分市場,提供了市場規模和預測(價值,美元)。

印度彈性辦公空間市場趨勢與洞察

新冠疫情後的混合辦公模式正在推動企業對彈性辦公空間的需求。

後疫情時代混合辦公模式的興起,大大改變了印度企業的辦公空間策略。印度企業越來越將彈性辦公空間視為不可或缺的基礎設施,而不僅僅是應急方案。為了適應混合辦公模式,需要現場分配座位,而傳統的租賃協議難以滿足這項需求。企業紛紛轉向配備佔用管理軟體的「即插即用」辦公中心,這些中心不僅能提供一流的設施,還能將每張辦公桌的房地產成本降低高達30%。曾經受制於九年租賃協議的跨國公司,如今更傾向於簽訂一至三年的辦公空間管理契約,將營運風險轉移給供應商,同時確保擴充性。最初在孟買和班加羅爾開展的試點項目,如今已擴展到五個以上的城市,涵蓋了完整的辦公空間組合。隨著總部空間擴大用於品牌推廣和客戶互動,這些靈活的辦公中心不僅在日常營運管理中發揮至關重要的作用,而且在競爭激烈的勞動力市場中也對人才保留至關重要。

創業生態系統的擴張正在推動按需辦公空間的成長。

印度的創業生態系統持續蓬勃發展,預計僅在2024年,哈里亞納邦就將有超過700家新創企業註冊,凸顯了全國創業熱潮的興起。這些公司正從沉重的資本支出(CAPEX)負擔的租賃協議轉向營運支出(OPEX)模式,並傾向於可按週或按月擴展的靈活辦公空間。創業融資通常會導致員工人數的快速成長。共享辦公室協議允許在不重新協商租賃協議的情況下快速增加座位容量。因此,營運商正在設計靈活的座位方案、動態定價和投資者休息區,以適應新創企業的文化。隨著新創公司從種子輪融資發展到B輪融資,它們傾向於遷移到同一園區內的託管辦公空間,這為營運商提供了與客戶生命週期相符的成長。

租金上漲給企業的盈利帶來了壓力。

租金上漲正日益擠壓黃金地段靈活辦公空間營運商的盈利。在孟買南部,A級辦公室的租金已超過每平方英尺每月2.40美元,即使最佳化了座位密度,也給靈活辦公空間營運商的利潤率帶來了壓力。雖然主租賃協議中的年度租金漲幅條款最高可達6%,但業者通常將轉嫁給客戶的租金漲幅限制在4%以內,導致利潤為負。自2023年以來,包括電力、清潔和網路在內的維護成本已飆升8-10%,進一步擠壓了營運利潤。為了應對這些壓力,業者正在轉向收益分成模式,並爭取更長的合約期限以獲得一次性折扣。然而,利潤率面臨的風險依然巨大,尤其是在中央商務區的關鍵區域。

細分市場分析

到2025年,共享辦公空間將佔印度彈性辦公空間市場47.92%的佔有率,這反映出市場對適合敏捷團隊的開放式協作環境的持續需求。同時,「混合辦公和虛擬辦公室」類別預計將以14.35%的複合年成長率成為所有辦公空間形式中成長最快的,因為企業正在探索將專屬管理套房與面向分散辦公員工的日租辦公模式相結合。在印度的彈性辦公空間市場,混合辦公服務整合了實體辦公桌、虛擬地址和按需會議室,使租戶能夠靈活地控制成本。像Awfis、Smartworks和Table Space這樣的公司目前已將其新增辦公空間的35%以上分配給混合辦公佈局。

技術至關重要。行動應用程式允許員工以15分鐘為單位預訂辦公桌,而人工智慧驅動的使用情況儀表板則支援即時空間重新配置。營運商正在投資聲學分區和空氣品質監測,以滿足環境、社會和治理 (ESG) 以及員工福祉指標的要求。隨著大型企業轉向中心輻射式網路,能夠在開放式和封閉式區域之間切換的混合型辦公中心正變得越來越重要,推動印度靈活辦公空間市場逐步向多元化服務模式轉型。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場趨勢與分析

- 市場概覽

- 市場促進因素

- 在後新冠疫情時代的混合辦公模式下,企業擴大採用靈活、即插即用的辦公室解決方案。

- 新創企業和中小企業的激增,推動了對按需、擴充性的共同工作空間的需求成長。

- WeWork、Awfis 和 Smartworks 等共同工作品牌在一二線城市的快速擴張正在提高辦公室的可及性。

- 為了支持地理位置分散的團隊,各公司正在郊區和衛星地點開設彈性辦公中心。

- 引入數位化設施(例如基於應用程式的預訂和智慧會議室)正在改善居民的體驗。

- Flexspace 已獲得 LEED 或 IGBC 認證,憑藉 ESG 政策吸引客戶,並能夠提供優質定價。

- 市場限制因素

- 孟買、新德里(NCR) 和班加羅爾不斷上漲的租金和高昂的維護成本給營運商的利潤率帶來了壓力。

- 主要大都市地區出現供應過剩的跡象,增加了房屋空置的風險,並給續租率帶來壓力。

- 各州對租賃和商業活動的規定各不相同,這使得跨城市運作變得複雜。

- 共用網路中的安全和資料隱私問題阻礙了企業採用這些解決方案。

- 價值供應鏈分析

- 概述

- 房地產開發商和資產所有者——關鍵的定量和定性見解

- 工作空間設計與技術顧問—關鍵的定量和定性見解

- 模組化家具和智慧辦公室解決方案供應商—關鍵定量和定性洞察

- 業界的政府法規和舉措

- 彈性辦公房地產市場的技術創新

- 辦公室房地產行業關鍵指標分析(供應量、租金、價格、運轉率/空置率(%))。

- 遠距辦公對辦公室需求的影響

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 共同工作空間

- 服務式辦公室/行政套房

- 其他(混合辦公、虛擬辦公)

- 按行業

- 資訊科技(IT 和 ITES)

- 銀行、金融服務和保險業 (BFSI)

- 商業諮詢和專業服務

- 其他服務(零售、生命科學、能源、法律服務)

- 最終用戶

- 自由工作者

- 公司

- 新創企業及其他

- 按城市

- 孟買大都會圈

- 德里首都區

- 普納

- 班加羅爾

- 海得拉巴

- 清奈

- 加爾各答

- 印度其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 公司簡介

- WeWork

- Awfis Space Solutions

- Smartworks

- IndiQube

- Simpliwork Offices

- CoWrks

- 91Springboard

- The Hive

- BHIVE Workspace

- Skootr

- Table Space

- Regus(IWG plc)

- 315Work Avenue

- Urban Vault

- MyHQ

- WorkEz

- GoodWorks Coworking

- OYO Workspaces(PowerStation+Innov8)

- Incuspaze

- Bangalore Alpha Lab

第7章 市場機會與未來展望

According to Mordor Intelligence, india flexible office space market size in 2026 is estimated at USD 6.81 billion, growing from 2025 value of USD 5.99 billion with 2031 projections showing USD 12.87 billion, growing at 13.58% CAGR over 2026-2031.

This report is Segmented by Type (Co-Working Spaces, Serviced Offices / Executive Suites, and More) by Sector (Information Technology (IT & ITES), and More), by End Use (Enterprises, Freelancers and Start Ups & Others), and by City (Mumbai Metropolitan Region, Bengaluru, Pune and More). The Report Provides Market Size and Forecasts in Value (USD) for all the Above Segments.

India Flexible Office Space Market Trends and Insights

Post-COVID Hybrid Work Models Drive Enterprise Flexibility Demand

The shift to hybrid work models post-COVID-19 has significantly transformed workspace strategies for Indian corporates. Indian corporates are increasingly viewing flexible workspaces as essential infrastructure rather than mere contingency options. The demands of hybrid work schedules necessitate on-the-fly seat allocations, a feat that traditional leases struggle to provide. Companies are turning to plug-and-play centers, armed with occupancy-management software, allowing them to slash real estate costs by up to 30% per desk, all while enjoying top-tier amenities. Once bound by nine-year leases, multinationals are now favoring one- to three-year managed-office contracts, shifting operational risks to the providers but ensuring scalability. What began as experimental projects in Mumbai and Bengaluru has now expanded to encompass full portfolios in five or more cities. As head-office spaces become predominantly reserved for branding and client interactions, these flexible hubs are not only managing daily operations but also playing a pivotal role in talent retention amidst a competitive labor market.

Startup Ecosystem Expansion Fuels On-Demand Workspace Growth

India's start-up ecosystem continues to thrive, with Haryana alone witnessing the registration of over 700 new start-ups in 2024, underscoring nationwide entrepreneurial momentum. These firms prize operational-expenditure models over capex-heavy leases and migrate to flex space that scales in weekly or monthly blocks. Venture funding rounds often translate into sudden head-count jumps; coworking contracts provide rapid seat additions without lease renegotiation. Operators, therefore, design variable seat packs, dynamic pricing, and investor lounge zones aligned with start-up cultures. As start-ups move from seed to Series B, they tend to graduate into managed offices within the same campus, giving operators built-in customer life-cycle growth.

Rental Cost Inflation Pressures Operator Profitability

Rising rental costs are increasingly challenging the profitability of flex-space operators in prime locations. In South Mumbai, Grade-A office rents have crossed the USD 2.40 per sq ft per month mark, putting a pinch on flex-operator margins, even with optimised seat density. While annual step-up clauses in master leases can hit 6%, operators frequently limit client escalations to 4%, leading to a negative spread. Since 2023, maintenance costs-covering power, cleaning, and internet-have surged by 8-10%, further constraining operating profits. To counteract these pressures, operators are pivoting to revenue-share models and seeking longer lock-ins for bulk discounts. However, the risk to margins remains significant, especially in prime CBD areas.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Metro Expansion by Brands Enhances Tier-2 Market Penetration

- Corporate Suburban and Satellite Hubs Support Distributed Teams

- Oversupply Conditions Threaten Pricing Power

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Co-working spaces accounted for 47.92% India flexible office market share in 2025, underscoring enduring demand for open, collaborative environments that suit agile teams. Meanwhile, the Hybrid & Virtual Office category is forecast to post a 14.35% CAGR, the fastest among formats, as corporates look to blend private managed suites with day-pass access for distributed staff. Within the India flexible office market size, hybrid products bundle physical seats, virtual addresses, and on-demand meeting rooms, giving tenants modular cost control. Awfis, Smartworks, and Table Space now allocate more than 35% of new supply to hybrid layouts.

Technology is the linchpin: mobile apps let employees reserve desks in 15-minute increments, while AI-driven utilisation dashboards inform real-time space reconfiguration. Operators invest in acoustic zoning and air-quality monitoring to meet ESG and employee-wellbeing metrics. As large enterprises pivot to hub-and-spoke networks, hybrid centres capable of toggling between open and enclosed zones gain strategic relevance, reinforcing the India flexible office market's gradual tilt toward multi-format service lines.

Complete Report Scope:

- By Type

- Co-Working Space

- Serviced offices / Executive suites

- Others (Hybrid, Virtual Office)

- By Sector

- Information Technology (IT and ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Service

- Other Services (Retail, Lifesciences, Energy, Legal Services)

- By End Use

- Freelancers

- Enterprises

- Start Ups and Others

- By City

- Mumbai Metropolitan Region

- Delhi NCR

- Pune

- Bengaluru

- Hyderabad

- Chennai

- Kolkata

- Rest of India

List of Companies Covered in this Report:

- WeWork

- Awfis Space Solutions

- Smartworks

- IndiQube

- Simpliwork Offices

- CoWrks

- 91Springboard

- The Hive

- BHIVE Workspace

- Skootr

- Table Space

- Regus (IWG plc)

- 315Work Avenue

- Urban Vault

- MyHQ

- WorkEz

- GoodWorks Coworking

- OYO Workspaces (PowerStation + Innov8)

- Incuspaze

- Bangalore Alpha Lab

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-COVID hybrid work models are driving enterprises to adopt flexible plug-and-play office solutions.

- 4.2.2 A boom in startups and SMEs is increasing demand for on-demand, scalable coworking spaces.

- 4.2.3 Rapid metro expansion by coworking brands like WeWork, Awfis, and Smartworks in Tier-1/2 cities is enhancing accessibility.

- 4.2.4 Corporates are launching suburban and satellite flex hubs to support geographically distributed teams.

- 4.2.5 Integration of digital amenities (e.g., app-based bookings, smart conference rooms) is improving occupier experience.

- 4.2.6 LEED or IGBC-certified flex spaces are attracting clients with ESG mandates and commanding premium prices.

- 4.3 Market Restraints

- 4.3.1 High rental escalation and maintenance costs in Mumbai, Delhi NCR, and Bangalore are compressing operator margins.

- 4.3.2 Emerging oversupply in major metros is increasing vacancy risk and pressuring renewal rates.

- 4.3.3 Diverse state-level lease and commercial regulations are complicating multi-city rollouts.

- 4.3.4 Security and data privacy concerns in shared networks are limiting corporate adoption.

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Overview

- 4.4.2 Real Estate Developers and Asset Owners - Key Quantitative and Qualitative Insights

- 4.4.3 Workspace Design and Technology Consultants - Key Quantitative and Qualitative Insights

- 4.4.4 Modular Furniture and Smart Office Solutions Providers - Key Quantitative and Qualitative Insights

- 4.5 Government Regulations and Initiatives in the Industry

- 4.6 Technological Innovations in the Flexible Office Real Estate Market

- 4.7 Insights into the Key Office Real Estate Industry Metrics (Supply, Rentals, Prices, Occupancy/Vacancy (%))

- 4.8 Impact of Remote Working on Space Demand

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value USD)

- 5.1 By Type

- 5.1.1 Co-Working Space

- 5.1.2 Serviced offices / Executive suites

- 5.1.3 Others (Hybrid, Virtual Office)

- 5.2 By Sector

- 5.2.1 Information Technology (IT and ITES)

- 5.2.2 BFSI (Banking, Financial Services and Insurance)

- 5.2.3 Business Consulting & Professional Service

- 5.2.4 Other Services (Retail, Lifesciences, Energy, Legal Services)

- 5.3 By End Use

- 5.3.1 Freelancers

- 5.3.2 Enterprises

- 5.3.3 Start Ups and Others

- 5.4 By City

- 5.4.1 Mumbai Metropolitan Region

- 5.4.2 Delhi NCR

- 5.4.3 Pune

- 5.4.4 Bengaluru

- 5.4.5 Hyderabad

- 5.4.6 Chennai

- 5.4.7 Kolkata

- 5.4.8 Rest of India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 WeWork

- 6.3.2 Awfis Space Solutions

- 6.3.3 Smartworks

- 6.3.4 IndiQube

- 6.3.5 Simpliwork Offices

- 6.3.6 CoWrks

- 6.3.7 91Springboard

- 6.3.8 The Hive

- 6.3.9 BHIVE Workspace

- 6.3.10 Skootr

- 6.3.11 Table Space

- 6.3.12 Regus (IWG plc)

- 6.3.13 315Work Avenue

- 6.3.14 Urban Vault

- 6.3.15 MyHQ

- 6.3.16 WorkEz

- 6.3.17 GoodWorks Coworking

- 6.3.18 OYO Workspaces (PowerStation + Innov8)

- 6.3.19 Incuspaze

- 6.3.20 Bangalore Alpha Lab

7 Market Opportunities & Future Outlook

辦公空間市場規模、佔有率和成長分析:按物業類型、等級、租賃類型、公司規模、最終用途產業、用途和地區分類-2026-2033年產業預測

辦公空間市場規模、佔有率和成長分析:按物業類型、等級、租賃類型、公司規模、最終用途產業、用途和地區分類-2026-2033年產業預測 共享辦公空間市場:按類型、產品類型、營運模式、產業和最終用戶分類-2026-2032年全球市場預測

共享辦公空間市場:按類型、產品類型、營運模式、產業和最終用戶分類-2026-2032年全球市場預測 辦公空間市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

辦公空間市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 2026年全球公用廚房預約平台市場報告

2026年全球公用廚房預約平台市場報告 共享辦公空間預訂平台市場預測至2034年——全球平台類型、工作空間類型、定價模式、功能、應用、最終用戶和區域分析2026年全球共享辦公桌市場報告2026年全球共享辦公空間市場報告

共享辦公空間預訂平台市場預測至2034年——全球平台類型、工作空間類型、定價模式、功能、應用、最終用戶和區域分析2026年全球共享辦公桌市場報告2026年全球共享辦公空間市場報告 全球共享辦公空間市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球共享辦公空間市場規模、佔有率、趨勢和成長分析報告(2026-2034) 共享辦公空間市場:按空間類型和區域分類

共享辦公空間市場:按空間類型和區域分類 英國共享辦公空間:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

英國共享辦公空間:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)