|

市場調查報告書

商品編碼

2073431

碳纖維增強塑膠(CFRP):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Carbon Fiber Reinforced Plastic (CFRP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

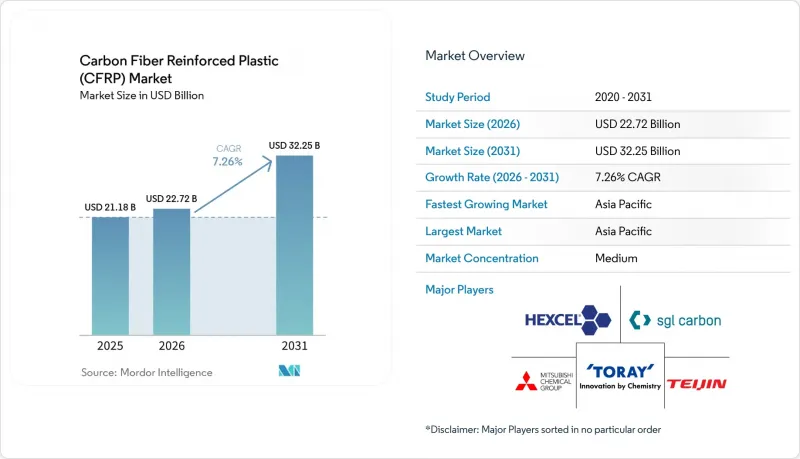

據 Mordor Intelligence 稱,2025 年碳纖維增強塑膠 (CFRP) 市場價值為 211.8 億美元,預計到 2031 年將達到 322.5 億美元,而 2026 年為 227.2 億美元,預測期(2026-2031 年)的複合年成長率為 7.26%。

本報告按樹脂類型(熱固性碳纖維增強複合材料和熱塑性碳纖維增強複合材料)、原料前體(聚丙烯腈、瀝青、人造絲等)及其他(木質素基等)、原料用戶產業(航太、汽車、風力發電等)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)對產業進行細分。市場預測以美元計價。

全球碳纖維增強塑膠(CFRP)市場趨勢及洞察

商用飛機訂單積壓激增。

民航領域前所未有的超過15,000份訂單訂單,導致碳纖維複合材料的需求持續強勁。飛機製造商正積極推動採用熱塑性二次結構材料,以提高生產速度,同時又不犧牲性能。為此,供應商正在認證多種纖維來源,以分散風險並防止供應中斷。

CFRP電池機殼正變得越來越電氣化。

電動車製造商目前正指定使用碳纖維電池外殼,與鋁製外殼相比,碳纖維機殼的重量最多可減輕91%。每減輕一公斤重量,就可以用來增加電池容量,從而在不增加車輛尺寸的情況下延長續航里程。憑藉阻燃熱塑性塑膠和整合的溫度控管,這種複合材料能夠滿足嚴格的安全標準,而碳纖維增強塑膠市場正進一步深入大眾汽車領域。

航太級PAN前驅體高成本

符合航太標準的聚丙烯腈(PAN)售價為每公斤33至66美元,這限制了其在對成本敏感產業的應用。能夠滿足嚴格的清潔度和均一性標準的供應商寥寥無幾,導致供應鏈集中化風險。儘管對水溶性前驅物的研究有望降低成本,但在保守的航太供應鏈中進行商業性驗證可能需要時間。

細分市場分析

到2025年,熱固性系統將佔據碳纖維增強塑膠市場72.15%的佔有率,這主要是由於航太領域長期以來對環氧樹脂預浸料的依賴。然而,熱塑性解決方案預計到2031年將以8.02%的複合年成長率成長,這反映出市場對快速加工和可回收性的需求日益成長。空中巴士的熱塑性機身面板實現了足以支援每月70架以上飛機生產的周期,而汽車零件供應商正在將沖壓週期縮短至僅幾秒鐘。

此外,熱塑性複合材料在移動出行、電動垂直起降飛行器(eVTOL)和氫氣儲存等領域擴大了碳纖維增強塑膠的市場規模,因為它們在組裝過程中可以焊接和重熔。碳纖維增強聚醚醚酮(CF-PEEK)零件的拉伸強度為425 MPa,而碳纖維增強環氧樹脂(CF-epoxy)零件的拉伸強度為311 MPa,而CF-PEEK零件仍能承受更高的連續工作溫度。雖然這種變化遠遠不能取代飛機機翼中的熱固性樹脂,但它使其能夠在眾多領域中得到應用,例如二級結構和汽車零件,在這些領域,每個部件的成本是材料選擇的關鍵因素。

區域分析

預計到2025年,亞太地區將佔全球碳纖維增強塑膠市場的42.05%,並在2031年之前維持8.43%的複合年成長率,成為成長最快的地區。光是中國在2023年就消耗了約6.9萬噸複合材料,主要得益於風電、電動車和氫能基礎建設計畫的推動。然而,T1000級碳纖維持續供不應求以及出口限制的不利影響可能會減緩航太領域的成長動能。

北美正充分利用航太計畫和氫能出行試點計畫。波音公司的訂單積壓以及新興的電動垂直起降飛行器(eVTOL)公司支撐著強勁的需求基礎,而對回收工廠和替代前體的投資也加強了國內供應。儘管面臨物流挑戰,Hexel公司2024年第一季的商業航太部門收入仍成長了5.2%。

歐洲已成為永續性的領導中心。空中巴士在熱塑性塑膠領域的努力以及歐盟的回收法規正在推動循環經濟的發展。該地區在氫氣罐製造(大量使用碳纖維)和離岸風力發電的投資也在增加。索爾維與波音簽署的長期供應協議表明,隨著歐洲生產商加強在該地區創造附加價值,跨大西洋合作仍在繼續。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 商用飛機訂單積壓激增。

- 汽車電氣化程度的不斷提高,推動了對碳纖維增強塑膠(CFRP)製成的電池機殼的需求不斷成長。

- 採用碳纖維強化塑膠(CFRP)支架帽的巨型葉片風力發電機(小於100公尺)。

- 開發用於氫氣運輸的壓力容器

- 熱塑性碳纖維增強複合材料在電動垂直起降飛行器和城市空中運輸平台的應用日益廣泛

- 透過閉合迴路回收實現低成本再生碳纖維(rCF)。

- 市場限制因素

- 航太用聚丙烯腈(PAN)前驅物高成本

- 工業纖維產能瓶頸

- 高模量纖維的出口限制

- 廢舊產品回收基礎設施不足

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 熱固性碳纖維增強塑膠(CFRP)

- 熱塑性碳纖維增強塑膠(CFRP)

- 透過原料前驅體

- 聚丙烯腈(PAN)

- 瀝青

- 人造絲

- 其他(木質素基、再生碳纖維)

- 按最終用戶行業分類

- 航太

- 車

- 風力發電產業

- 運動休閒

- 建築/施工

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 其他亞太國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Toray Industries Inc.

- Hexcel Corporation

- SGL Carbon

- Mitsubishi Chemical Corporation

- Teijin Limited

- Solvay

- DowAksa

- Formosa Plastics Corporation, USA

- Gurit Services AG

- TPI Composites

- HS HYOSUNG ADVANCED MATERIALS

- Nippon Graphite Fiber Co., Ltd.

- Rochling

第7章 市場機會與未來展望

According to Mordor Intelligence, the carbon fiber reinforced plastic market size was valued at USD 21.18 billion in 2025 and estimated to grow from USD 22.72 billion in 2026 to reach USD 32.25 billion by 2031, at a CAGR of 7.26% during the forecast period (2026-2031).

This report Segments the Industry by Resin Type (Thermoset CFRP and Thermoplastic CFRP), Raw-Material Precursor (PAN, Pitch, Rayon) and Others (Lignin-Based, Etc. ), End-User Industry (Aerospace, Automotive, Wind Power Industry, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD)..

Global Carbon Fiber Reinforced Plastic (CFRP) Market Trends and Insights

Surge in Commercial Aircraft Backlog

The commercial aviation sector's unprecedented order backlog exceeding 15,000 aircraft creates sustained demand for carbon fiber composites. Air-framer push for thermoplastic secondary structures aims at faster build rates without sacrificing performance. Suppliers respond by qualifying multiple fiber sources to diversify risk and assure uninterrupted deliveries.

Electrification Accelerating CFRP Battery Enclosures

Electric-vehicle makers now specify carbon-fiber battery housings that cut enclosure weight by up to 91% versus aluminum. Each kilogram saved can be redeployed as extra battery capacity, extending range without enlarging the vehicle footprint. Flame-retardant thermoplastics and integrated thermal-management layers help composites meet strict safety codes, moving the carbon fiber reinforced plastic market deeper into high-volume automotive production.

High Cost of Aerospace-grade PAN Precursor

Aerospace-qualified polyacrylonitrile (PAN) sells for USD 33-66 per kg, limiting crossover into cost-sensitive sectors. Few suppliers meet stringent cleanliness and consistency norms, creating supply concentration risk. Water-soluble precursor research promises cost cuts, yet commercial validation in conservative aerospace supply chains will take time.

Other drivers and restraints analyzed in the detailed report include:

- Mega-blade Wind Turbines (>100 m) Adopting CFRP Spar Caps

- Hydrogen Mobility Pressure-vessel Build-out

- Industrial-grade Fibre Capacity Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermoset systems commanded 72.15% of the carbon fiber reinforced plastic market share in 2025, cemented by aerospace's long reliance on epoxy prepregs. Yet thermoplastic solutions record an 8.02% CAGR through 2031, reflecting rising needs for fast processing and recyclability. Airbus's thermoplastic fuselage panels show cycle-time savings compatible with monthly production rates above 70 airframes, while automotive suppliers cut stamping cycles to seconds.

Thermoplastic composites also expand the carbon fiber reinforced plastic market size in mobility, eVTOL, and hydrogen storage because they can be welded or re-melted during assembly. CF-PEEK parts deliver tensile strength of 425 MPa versus 311 MPa for CF-epoxy, together with higher continuous-use temperatures. The shift is far from replacing thermosets in primary aircraft wings, but it unlocks a broad set of secondary structures and automotive parts where cost per component dictates material choice.

Complete Report Scope:

- By Resin Type

- Thermoset Carbon Fiber Reinforced Plastics (CFRP)

- Thermoplastic Carbon Fiber Reinforced Plastics (CFRP)

- By Raw-Material Precursor

- Polyacrylonitrile (PAN)

- Pitch

- Rayon

- Others (Lignin-based, Recycled CF (Carbon Fiber))

- By End-user Industry

- Aerospace

- Automotive

- Wind Power Industry

- Sports and Leisure

- Building and Construction

- Other End-user Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific captured 42.05% of the carbon fiber reinforced plastic market in 2025 and exhibits the highest 8.43% CAGR through 2031. China alone consumed about 69,000 t of composites in 2023, propelled by wind, EV, and hydrogen infrastructure projects. Yet lingering gaps in T1000-level fibers and export-control headwinds could temper its aerospace momentum.

North America leverages aerospace programs and hydrogen-mobility pilots. Boeing's backlog plus emerging eVTOL firms sustain a robust demand base, while investments in recycling plants and alternative precursors aim to fortify domestic supply. Hexcel reported 5.2% commercial-aerospace revenue growth in Q1 2024 despite logistics challenges.

Europe anchors sustainability leadership. Airbus's thermoplastic initiatives and EU recycling regulations spur circular-economy advances. The region also channels investment into hydrogen tank manufacturing and offshore wind, both heavy carbon-fiber users. Solvay's long-term supply deal with Boeing underlines transatlantic collaboration even as European producers tighten local value retention.

- Toray Industries Inc.

- Hexcel Corporation

- SGL Carbon

- Mitsubishi Chemical Corporation

- Teijin Limited

- Solvay

- DowAksa

- Formosa Plastics Corporation, U.S.A.

- Gurit Services AG

- TPI Composites

- HS HYOSUNG ADVANCED MATERIALS

- Nippon Graphite Fiber Co., Ltd.

- Rochling

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in commercial aircraft backlog

- 4.2.2 Electrification accelerating Carbon Fiber Reinforced Plastics (CFRP) battery enclosures

- 4.2.3 Mega-blade wind turbines (less than 100 m) adopting Carbon Fiber Reinforced Plastics (CFRP) spar caps

- 4.2.4 Hydrogen mobility pressure-vessel build-out

- 4.2.5 eVTOL & urban-air-mobility platforms favouring thermoplastic CFRP

- 4.2.6 Closed-loop recycling unlocking low-cost recycled Carbon Fiber (rCF)

- 4.3 Market Restraints

- 4.3.1 High cost of aerospace-grade Polyacrylonitrile (PAN) precursor

- 4.3.2 Industrial-grade fibre capacity bottlenecks

- 4.3.3 Export controls on high-modulus fibre

- 4.3.4 Immature end-of-life recycling infrastructure

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Thermoset Carbon Fiber Reinforced Plastics (CFRP)

- 5.1.2 Thermoplastic Carbon Fiber Reinforced Plastics (CFRP)

- 5.2 By Raw-Material Precursor

- 5.2.1 Polyacrylonitrile (PAN)

- 5.2.2 Pitch

- 5.2.3 Rayon

- 5.2.4 Others (Lignin-based, Recycled CF (Carbon Fiber))

- 5.3 By End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Automotive

- 5.3.3 Wind Power Industry

- 5.3.4 Sports and Leisure

- 5.3.5 Building and Construction

- 5.3.6 Other End-user Industry

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Toray Industries Inc.

- 6.4.2 Hexcel Corporation

- 6.4.3 SGL Carbon

- 6.4.4 Mitsubishi Chemical Corporation

- 6.4.5 Teijin Limited

- 6.4.6 Solvay

- 6.4.7 DowAksa

- 6.4.8 Formosa Plastics Corporation, U.S.A.

- 6.4.9 Gurit Services AG

- 6.4.10 TPI Composites

- 6.4.11 HS HYOSUNG ADVANCED MATERIALS

- 6.4.12 Nippon Graphite Fiber Co., Ltd.

- 6.4.13 Rochling

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Introduction of Carbon Nanomaterials in Carbon Fiber Reinforced Plastics (CFRP)

碳纖維增強塑膠市場報告:按原料、類型、製造流程、應用和地區分類(2026-2034 年)

碳纖維增強塑膠市場報告:按原料、類型、製造流程、應用和地區分類(2026-2034 年) 碳纖維增強塑膠市場:依產品形式、纖維類型、基體樹脂和應用分類-2026-2032年全球市場預測碳-碳複合材料市場:依纖維類型、製造流程、等級和應用分類-2026-2032年全球市場預測按產品類型、纖維類型、形態、銷售管道和應用分類的增強碳材料市場-全球預測,2026-2032年

碳纖維增強塑膠市場:依產品形式、纖維類型、基體樹脂和應用分類-2026-2032年全球市場預測碳-碳複合材料市場:依纖維類型、製造流程、等級和應用分類-2026-2032年全球市場預測按產品類型、纖維類型、形態、銷售管道和應用分類的增強碳材料市場-全球預測,2026-2032年 全球碳纖維增強塑膠市場規模、佔有率、趨勢和成長分析報告(2026-2034)碳纖維增強塑膠市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測

全球碳纖維增強塑膠市場規模、佔有率、趨勢和成長分析報告(2026-2034)碳纖維增強塑膠市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測 2026年全球碳纖維增強塑膠(CFRP)市場報告碳纖維增強PPS市場按類型、等級、形狀、應用和最終用途產業分類-全球預測,2026-2032年碳纖維增強塑膠帶材市場:按類型、製造流程、纖維類型和最終用途產業分類,全球預測(2026-2032)

2026年全球碳纖維增強塑膠(CFRP)市場報告碳纖維增強PPS市場按類型、等級、形狀、應用和最終用途產業分類-全球預測,2026-2032年碳纖維增強塑膠帶材市場:按類型、製造流程、纖維類型和最終用途產業分類,全球預測(2026-2032) 碳-碳複合材料市場預測至2032年:按產品類型、原料、製造流程、最終用戶和地區分類的全球分析

碳-碳複合材料市場預測至2032年:按產品類型、原料、製造流程、最終用戶和地區分類的全球分析