|

市場調查報告書

商品編碼

2073352

美國宅配:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States Express Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

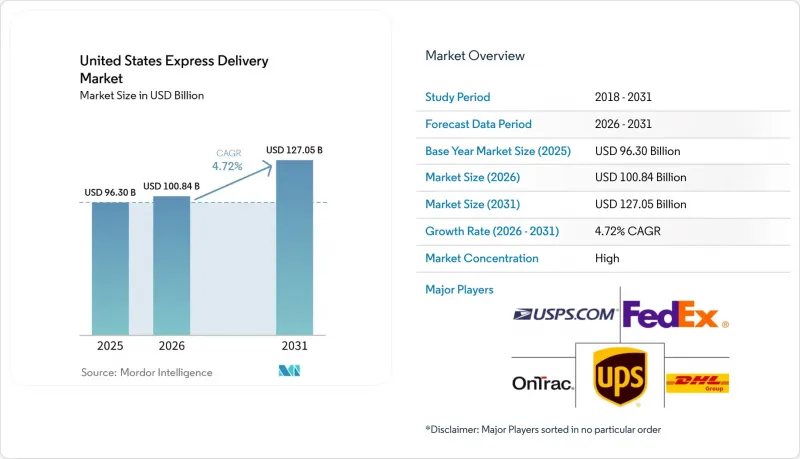

據 Mordor Intelligence 稱,2025 年美國快捷郵件市場價值 963 億美元,預計到 2031 年將達到 1270.5 億美元,而 2026 年為 1008.4 億美元,預測期(2026-2031 年)複合年成長率為 4.72%。

本報告按最終用戶行業(例如電子商務)、目的地(國內和國際)、交付承諾(限時快遞和指定日期快遞)、運輸方式(空運、陸運及其他)、貨物重量(重型貨物等)以及模式(B2B等)進行細分。市場預測以美元計價。

美國快遞市場趨勢與洞察

在排名前 60 的大都會區,電子商務小包裹的當日達和隔天達配送業務呈現爆炸性成長。

2024年,亞馬遜在美國國內處理了40億份當日達或隔天達訂單,這充分展現了以在地化服務為核心的履約模式對其營運的顯著影響。這項成功引發了連鎖反應,競爭對手紛紛要求提供類似的配送速度,美國當日達市場99%的主要參與者都計劃在2025年前提供某種形式的當日達服務。宅配公司正在加倍擴建其當日達配送設施,並將分類能力重新分配到都市區,以確保高利潤的配送路線。因此,美國宅配市場的資本集中在人口稠密的大都會圈,這給實現全國覆蓋帶來了挑戰。在農村地區,各公司正在試行使用無人機和自動駕駛貨車來取代成本高昂的卡車運輸路線,從而推動技術主導的全面服務覆蓋範圍的擴展。

零售商向微型倉配中心的轉變正在提升「0/1 區」的快遞量。

自動化微型倉配中心已將平均小包裹運輸距離縮短至5英里以內,即使是陸運包裹也能達到快遞等級的速度。亞馬遜的「Project Juniper」專案展示了模組化機器人技術如何在短短一小時內將閒置的零售門市維修成履約中心。快遞業者透過提供跨區域配送、預約取件和針對這些城市中心量身訂製的退貨管理服務,創造了額外的收入。然而,微型倉配中心的規模化發展仍需要大量的資本投入,而且隨著業務量的趨於正常化,最初的熱情,尤其是在食品雜貨領域,已經消退。儘管美國快遞市場繁榮的勢頭有所減弱,但隨著機器人技術和靈活貨架系統的不斷升級,投資回報率不斷提高,美國快遞市場仍然能夠滿足高階、高度本地化的配送需求。

隨著托運人降低服務等級以最佳化成本,陸運和快遞運輸方式之間的轉變正在發生。

為了緩解通膨壓力,托運人正轉向更經濟的服務級別,例如 UPS Ground Saver。消費者調查顯示,90% 的買家願意接受更長的等待時間以換取免費送貨,而曾經特有的快遞快遞 (FedEx) 和 UPS 計劃在 2025 年將整體費率上調 5.9% 至 6.6%,但同時也在整合地面運輸和快遞業務以維持服務可靠性。美國郵政 (USPS) 的 Ground Advantage 服務以極具競爭力的價格提供可靠的 2-5 天送達服務,進一步擠壓了利潤空間。整體貨運量向延遲送達方案的轉變正在減緩美國快遞市場的短期收入成長。

細分市場分析

到2025年,電子商務將占美國快遞市場39.62%的佔有率,成為每日貨運量預測的基礎。服裝和美妝產品將佔據貨運量的大部分,而退貨管理將成為至關重要的輔助服務。

預計批發和零售(線下)訂單將以5.62%的複合年成長率(2026-2031年)實現最快成長,實體連鎖店開始提供從門市到家的快遞服務,縮小與純線上競爭對手的服務差距。製造業依賴零件隔日達服務以最大程度地減少生產中斷,而醫療產業則受高價策略驅動,因為低溫運輸故障可能導致違規處罰。金融服務業儘管小包裹量較低,但由於需要嚴格的儲存歷史管理,因此仍保持著對高度安全快遞服務的快遞。因此,垂直專業化仍然是美國快遞市場保持獲利能力的永續策略。

國際快遞市場預計將以5.73%的複合年成長率成長(2026-2031年),而國內市場基數更大,到2025年將占美國快遞市場規模的62.10%。文件核查、關稅計算和退貨流量的增加,使在清關方面具有優勢的整合商獲得了定價優勢。在美墨加協定(USMCA)框架下,近岸外包正在加速區域內航運路線的發展,例如墨西哥到美國的航線,在不影響對加值服務需求的前提下,縮短了平均幹線運輸距離。

儘管國內市場成長放緩,但電子商務的整合、零件的緊迫性以及對溫度敏感型藥品(運輸延誤不可接受)的需求,都支撐著國內市場的發展。亞馬遜的區域庫存佈局提高了美國當地消費者對24小時內送達的期望。因此,美國快遞市場維持著一個由兩大因素驅動的模式:國內包裹量確保了網路密度,而國際小包裹則帶來更高的收入。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 人口統計數據

- 按經濟活動分類的GDP構成

- 按經濟活動分類的GDP成長率

- 通貨膨脹

- 經濟表現及概覽

- 電子商務產業的趨勢

- 製造業的發展趨勢

- 運輸和倉儲部門的GDP

- 出口趨勢

- 進口趨勢

- 燃油價格

- 物流績效

- 基礎設施

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 在排名前 60 的大都會區,當日達/隔日達電商務小包裹呈爆炸式成長(亞馬遜 Prime 效應)

- 零售商向微型倉配中心的轉變正在提升「0/1區」的宅配量。

- 隨著對醫療低溫運輸的監管越來越嚴格,高階快遞溫控服務有望從中受益。

- 受源自中國的跨境退貨量增加的推動,國際快遞進口服務蓬勃發展。

- 訂閱式電商和D2C品牌正在推動快遞貨運量的可預測成長。

- 「2 小時」無人機貨車混合網路正在 B2B 時效性強的備件配送專案中獲得認可。

- 市場限制因素

- 為了最佳化成本,托運人正在降低服務等級,導致運輸方式轉向陸路快遞。

- 與工會達成的協議增加了最後一公里每次配送的成本。

- 機場容量和夜間航班限制限制了一級樞紐夜間分類作業的擴展。

- 燃油成本上漲給配送的獲利能力和路線最佳化帶來了壓力。

- 市場上的技術創新

- 波特五力分析

第5章 市場規模與成長預測

- 目的地

- 國內的

- 國際的

- 路線

- 跨區域

- 在該地區

- 路線

- 保證交貨

- 限時快遞 (TDE)

- 定期交付(DDE)

- 交通工具

- 航空

- 路

- 其他

- 運輸重量

- 重型貨物

- 輕便運輸

- 中等重量貨物

- 模型

- 企業對企業 (B2B) 交易

- B2C(Business-to-Consumer)

- 個人對個人(C2C)交易

- 終端用戶產業

- 電子商務

- 金融服務(BFSI)

- 衛生保健

- 製造業

- 一級產業

- 批發和零售貿易(線下)

- 其他

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- American Expediting

- Breakaway Courier Systems

- Canada Post Corporation(Including Purolator, Inc.)

- Courier Express

- DHL Group

- Dropoff, Inc.

- ExpressIt Delivery

- FedEx

- International Distribution Services PLC(Inculding GLS)

- Jet Delivery, Inc.

- King Courier

- MedSpeed

- Need It Now Delivers(Formerly A1-SameDay)

- NOW Delivery

- OnTrac(Formerly LaserShip/OnTrac)

- Priority One Courier and Logistics

- Spee-Dee Delivery Service, Inc.

- TFI International, Inc.(Including TForce Logistics)

- United Parcel Service of America, Inc.(UPS)

- United States Postal Service(USPS)

- WeDo Logistics, Ltd.(Including Lone Star Overnight, Inc.)

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states express delivery market size was valued at USD 96.30 billion in 2025 and estimated to grow from USD 100.84 billion in 2026 to reach USD 127.05 billion by 2031, at a CAGR of 4.72% during the forecast period (2026-2031).

This report is Segmented by End User Industry (E-Commerce and More), by Destination (Domestic and International), by Delivery Commitment (Time-Definite-Express and Day-Definite-Express), by Mode of Transport (Air, Road and Others), by Shipment Weight (Heavy Weight Shipments and More), and by Model (Business-To-Business and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Express Delivery Market Trends and Insights

Explosive Growth of Same-Day and Next-Day E-Commerce Parcels in Top-60 MSAs

Amazon fulfilled 4 billion same-day or next-day orders domestically in 2024, showcasing the operational impact of its regionalized fulfillment model. This achievement created a cascading requirement for comparable velocity among competitors, with 99% of large players in the United States same day delivery market aiming to offer some form of same-day delivery by 2025. Express carriers are doubling same-day facilities and reallocating urban sortation capacity to protect high-yield corridors. The United States express delivery market is therefore concentrating capital in the densest metropolitan areas, leading to a two-tier service structure that challenges nationwide coverage economics. In rural zones, carriers are piloting drones and autonomous vans as viable substitutes for costly truck-based routes, highlighting a technology-led push for inclusive service reach.

Retailers' Shift to Micro-Fulfillment Centers Boosting "Zone-0/1" Express Volumes

Automated micro-fulfillment centers shorten average parcel miles to under five, enabling ground-priced shipments to meet express-level speed targets. Amazon's Project Juniper roll-out illustrates how modular robotics can retrofit underutilized retail footprints into sub-hour fulfillment nodes. Express providers gain incremental revenue by offering zone-skipping, scheduled pick-ups, and managed returns tailored to these urban nodes. Yet, scaling micro-fulfillment remains capital intensive, and early grocery-focused enthusiasm has moderated as volumes normalize. Continuous robotics upgrades and flexible racking are improving ROI, allowing the United States express delivery market to capture premium, ultra-local traffic despite cooling hype cycles.

Ground-Express Modal Substitution as Shippers Trade Down for Cost Optimization

Shippers are gravitating toward economical tiers such as UPS Ground Saver to mitigate inflationary pressures. Consumer research confirms that 90% of buyers accept longer waits in exchange for free shipping, eroding the urgency premium once unique to express. FedEx and UPS instituted 5.9-6.6% general rate increases for 2025 but are blending ground and express operations to preserve service dependability. USPS's Ground Advantage compounds the margin squeeze by offering reliable two-to-five-day options at aggressive pricing. Aggregate volume migration toward deferred tiers dampens near-term revenue expansion across the United States express delivery market.

Other drivers and restraints analyzed in the detailed report include:

- As Healthcare Cold-Chain Compliance Tightens, Premium Express Services Stand to Gain

- International Inbound Growth on Cross-Border Returns from China-Origin Marketplaces

- Labor Union Agreements Escalating Last-Mile Cost per Stop

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

E-Commerce held a 39.62% share of the United States express delivery market size in 2025, anchoring daily volume expectations. Apparel and beauty items dominate shipment counts, and returns management is a critical ancillary service.

Wholesale and Retail Trade (Offline) bookings are expected to grow fastest at 5.62% CAGR (2026-2031) as brick-and-mortar chains launched store-to-door express fulfillment, narrowing the service gap with online-only rivals. Manufacturing relies on overnight parts to minimize production disruption, while healthcare drives premium yields because cold chain failures carry compliance penalties. Financial services send fewer parcels but require ironclad chain-of-custody controls, sustaining a niche premium for secure express. Vertical specialization thus remains a durable strategy for margin preservation in the United States express delivery market.

International express is projected to record a 5.73% CAGR (2026-2031) trajectory, while the domestic channel sustained a larger base with 62.10% of the United States express delivery market size in 2025. Increased document verification, tariff calculations, and return logistics confer pricing power on integrators possessing brokerage depth. Nearshoring under the USMCA framework accelerates intra-regional lanes such as Mexico-United States, producing shorter average line-haul distances yet not eroding premium service demand.

Domestic growth, though slower, benefits from e-commerce densification, spare-parts urgency, and temperature-controlled pharmaceuticals that cannot tolerate deferred transit. Amazon's regional inventory placement elevated customer expectations for 24-hour delivery windows across the continental footprint. The United States express delivery market, therefore, maintains a dual-engine model in which domestic volume secures network density and international parcels deliver a higher yield.

Complete Report Scope:

- Destination

- Domestic

- International

- By Route

- Inter-Region

- Intra-Region

- By Route

- Delivery Commitment

- Time-Definite-Express (TDE)

- Day-Definite-Express (DDE)

- Mode of Transport

- Air

- Road

- Others

- Shipment Weight

- Heavy Weight Shipments

- Light Weight Shipments

- Medium Weight Shipments

- Model

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Consumer-to-Consumer (C2C)

- End User Industry

- E-Commerce

- Financial Services (BFSI)

- Healthcare

- Manufacturing

- Primary Industry

- Wholesale and Retail Trade (Offline)

- Others

List of Companies Covered in this Report:

- American Expediting

- Breakaway Courier Systems

- Canada Post Corporation (Including Purolator, Inc.)

- Courier Express

- DHL Group

- Dropoff, Inc.

- ExpressIt Delivery

- FedEx

- International Distribution Services PLC (Inculding GLS)

- Jet Delivery, Inc.

- King Courier

- MedSpeed

- Need It Now Delivers (Formerly A1-SameDay)

- NOW Delivery

- OnTrac (Formerly LaserShip/OnTrac)

- Priority One Courier and Logistics

- Spee-Dee Delivery Service, Inc.

- TFI International, Inc. (Including TForce Logistics)

- United Parcel Service of America, Inc. (UPS)

- United States Postal Service (USPS)

- WeDo Logistics, Ltd. (Including Lone Star Overnight, Inc.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 Explosive Growth of Same-Day and Next-Day E-commerce Parcels in Top-60 MSAs (Amazon Prime Effect)

- 4.15.2 Retailers' Shift to Micro-Fulfillment Centers Boosting "Zone-0/1" Express Volumes

- 4.15.3 As Healthcare Cold-Chain Compliance Tightens, Premium Express Temperature-Controlled Services Stand to Gain

- 4.15.4 International Express Inbound Thrives on Rising Cross-Border Returns from China-Origin Marketplaces

- 4.15.5 Subscription Commerce and Direct-to-Consumer Brands Driving Predictable Express Volume Growth

- 4.15.6 "2-hour" Drone/Van Hybrid Networks Gain Traction in B2B Time-Critical Spare-Parts Programs

- 4.16 Market Restraints

- 4.16.1 Ground-Express Modal Substitution as Shippers Trade-Down for Cost Optimization

- 4.16.2 Labor Union Agreements Escalating Last-Mile Cost per Stop

- 4.16.3 Airport Capacity Curfews Limiting Night-Sort Expansion in Tier-1 Hubs

- 4.16.4 Rising Fuel Costs Pressuring Delivery Economics and Route Optimization

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Suppliers

- 4.18.3 Bargaining Power of Buyers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.1.2.1 By Route

- 5.1.2.1.1 Inter-Region

- 5.1.2.1.2 Intra-Region

- 5.1.2.1 By Route

- 5.2 Delivery Commitment

- 5.2.1 Time-Definite-Express (TDE)

- 5.2.2 Day-Definite-Express (DDE)

- 5.3 Mode of Transport

- 5.3.1 Air

- 5.3.2 Road

- 5.3.3 Others

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Model

- 5.5.1 Business-to-Business (B2B)

- 5.5.2 Business-to-Consumer (B2C)

- 5.5.3 Consumer-to-Consumer (C2C)

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 American Expediting

- 6.4.2 Breakaway Courier Systems

- 6.4.3 Canada Post Corporation (Including Purolator, Inc.)

- 6.4.4 Courier Express

- 6.4.5 DHL Group

- 6.4.6 Dropoff, Inc.

- 6.4.7 ExpressIt Delivery

- 6.4.8 FedEx

- 6.4.9 International Distribution Services PLC (Inculding GLS)

- 6.4.10 Jet Delivery, Inc.

- 6.4.11 King Courier

- 6.4.12 MedSpeed

- 6.4.13 Need It Now Delivers (Formerly A1-SameDay)

- 6.4.14 NOW Delivery

- 6.4.15 OnTrac (Formerly LaserShip/OnTrac)

- 6.4.16 Priority One Courier and Logistics

- 6.4.17 Spee-Dee Delivery Service, Inc.

- 6.4.18 TFI International, Inc. (Including TForce Logistics)

- 6.4.19 United Parcel Service of America, Inc. (UPS)

- 6.4.20 United States Postal Service (USPS)

- 6.4.21 WeDo Logistics, Ltd. (Including Lone Star Overnight, Inc.)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

全球快遞服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球快遞服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球快遞市場報告

2026年全球快遞市場報告 快遞市場:依遞送方式、遞送模式、服務類型、重量類別和最終用戶分類-2026-2032年全球市場預測

快遞市場:依遞送方式、遞送模式、服務類型、重量類別和最終用戶分類-2026-2032年全球市場預測 快遞運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

快遞運輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 快遞市場規模、佔有率和成長分析(按目的地、遞送方式、包裝類型、應用、最終用途和地區分類):產業預測(2026-2033 年)德國快遞:市場佔有率分析、產業趨勢、成長預測(2025-2030)

快遞市場規模、佔有率和成長分析(按目的地、遞送方式、包裝類型、應用、最終用途和地區分類):產業預測(2026-2033 年)德國快遞:市場佔有率分析、產業趨勢、成長預測(2025-2030) 印度的快遞市場:各類服務,各產業,地址,各終端用戶,各地區,機會,預測,2018年~2032年快捷郵件的全球市場的評估:各類服務,商務,目的地,各終端用戶,各地區,機會,預測(2017年~2031年)

印度的快遞市場:各類服務,各產業,地址,各終端用戶,各地區,機會,預測,2018年~2032年快捷郵件的全球市場的評估:各類服務,商務,目的地,各終端用戶,各地區,機會,預測(2017年~2031年) 全球快遞市場

全球快遞市場