|

市場調查報告書

商品編碼

2073337

木塑複合材料(WPC)地板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Wood Plastic Composite Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

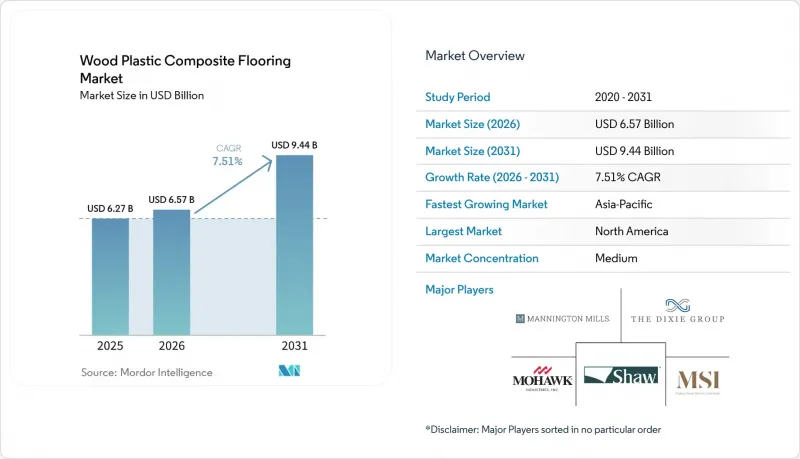

根據 Mordor Intelligence 預測,WPC(木塑複合材料)地板市場將從 2025 年的 62.7 億美元成長到 2026 年的 65.7 億美元,然後在 2031 年達到 94.4 億美元,2026 年至 2031 年的複合年成長率為 7.51%。

本報告按產品類型(聚乙烯、聚氯乙烯、聚丙烯及其他)、厚度(3.5–4毫米、5–6毫米、6.5–8毫米、8毫米及以上)、安裝方式(卡扣式、膠粘式及其他)、最終用戶、配銷通路(B2C、B2B)和地區(北美、南美、歐洲、亞太地區、中東和非洲)進行細分。市場預測以美元計價。

全球木塑複合材料(WPC)地板市場趨勢與洞察

卡扣式硬乙烯基地板材料非常適合 DIY 項目,正在加速住宅裝修。

卡扣式結構仍然是木塑複合材料(WPC)地板市場價值提案的核心要素,因為它能夠縮短安裝時間、簡化培訓流程,並降低在居住的住宅中進行返工的風險。知名品牌品牌不斷改進型材形狀和邊緣穩定性,以縮短安裝時間,同時保持成品地板的平整度,從而簡化了緊張的裝修工期安排。在零售層面,與卡扣系統相匹配的收邊條和底層地板套件系列,能夠幫助住宅和專業人士最大限度地減少從樣品選擇到最終完工的決策環節,從而提高轉換率和客戶滿意度。在近期的產品週期中,提供價格結構簡單、即裝即用的系統的製造商備受青睞,這表明安裝可靠性是裝修中的關鍵購買動機。能夠確保短前置作業時間和區域庫存的分銷計劃也為DIY裝修和專業裝修提供了支持,使承包商能夠自信地承諾交貨日期,並避免國際運輸帶來的延誤。

多層住宅防水與隔音的優勢

在多層住宅專案中,能夠抑制噪音傳播並提供溫暖腳感的地板產品備受青睞。因此,臥室、閣樓和夾層對木塑複合材料(WPC)地板的需求仍然強勁。此系列產品採用厚實的芯材和特殊處理的襯墊,打造出均衡的結構,既能彌補底層地板的不平整,又能提升隔音效果。這對於重建和地下室至關重要。高階WPC系列將高耐磨表面與發泡材結合,兼具舒適性和耐刮擦性,使其應用範圍擴展至家庭活動室和居住者等對靜音效果要求較高的場所。類似的標準也適用於商業和混合用途建築的特定區域。 WPC地板始終是理想之選,尤其是在那些更注重腳感柔軟和易於維護而非最大靜態承重能力的區域。產品資料表強調了其防潮性、隔熱性和隔音性,這進一步鞏固了WPC在對聲學舒適度要求極高的專案中的市場地位。

SPC的低成本和高抗凹陷性正在從WPC手中奪取市場佔有率。

在優先考慮抗滾動荷載和抗堆疊家具造成的凹陷的項目中,通常會選用硬礦物芯材產品或商用級LVT地板,這使得WPC地板在走廊和咖啡簡餐店場所與WPC地板形成競爭。醫療保健和教育行業的設施管理人員尋求能夠保證硬質地板和表面硬度的解決方案,以保持其在長期使用中的外觀,因此他們的選擇通常會縮小到成熟的硬質LVT產品系列。在預算固定的入門級住宅專案中,為了滿足入住時間要求,購屋者往往會犧牲腳感舒適度來降低材料成本並提高靜態荷載等級。儘管WPC地板在舒適性和隔音降噪方面具有優勢,但這種趨勢可能會減緩其在某些細分市場的普及。隨著產品線的不斷發展,WPC地板在居住者優先考慮保暖性和隔音降噪的房間中仍然保持著市場佔有率。另一方面,在高人流區域,使用硬質LVT或礦物芯材的產品仍然很常見,因此,WPC(木塑複合材料)地板市場根據使用情境呈現出實際的二元性。

細分市場分析

到2025年,聚乙烯基木塑複合材料(WPC)將佔產品組合的40%,成為市場主導產品,而聚丙烯預計到2031年將以8.15%的複合年成長率成長。在2031年之前的通用聚合物市場中,聚乙烯和聚丙烯都將成為定價結構的基石,涵蓋木塑複合材料(WPC)地板市場的入門級、中階和高階價格區間。在實際應用中,聚乙烯基產品因其密度和彈性的平衡性而備受青睞。這種特性使其腳步聲舒適,適用於二樓房間和人流量較大的住宅區域。注重尺寸穩定性的產品系列,尤其是在季節性波動的情況下,更受安裝人員的青睞,因為他們希望避免因縫隙和邊緣翹起而導致的返工,這也有助於聚乙烯基產品保持其市場佔有率。聚丙烯正逐漸受到關注,尤其是在陽光充足的房間和氣候溫暖的地區,這些地區對熱變形溫度的要求更高,其特性正在開拓新的安裝場所,並擴大整體目標市場。該品牌將高規格芯材與耐用耐磨層相結合,目標客戶是那些喜歡柔軟觸感而非最大抗壓痕性能的住宅,並在兩種聚合物中保持一致的產品系列邏輯。

法規環境正在推動材料選擇趨勢,製造商正在評估複合芯材彈性地板材料的塑化劑選擇和認證目標。根據該公司資訊披露,隨著品牌所有者探索如何在其所有產品系列中實現低碳彈性地板材料,回收材料含量和替代策略方面正穩步取得進展。在木塑複合材料 (WPC) 地板市場,產品經理正在建造具有清晰應用案例的產品線,以指導消費者根據房間和人流進行選擇,從而防止誤用導致保固索賠。當產品線中耐磨層的耐用性、芯材層的穩定性以及襯墊的整合得到協調一致時,這種組合能夠使用戶期望與實際性能相符,從而提高複購率和零售商的淨推薦值 (NPS)。這些聚合物定位、認證一致性和房間規格方面的模式將繼續決定品牌如何與價格重疊的礦物芯材替代品競爭,從而保持市場佔有率。

到2025年,5-6毫米厚度的地板將佔據56.72%的市場。這是因為注重成本的買家選擇這個厚度範圍,既能滿足他們對地板抗凹陷性和舒適性的期望,又能將總安裝成本控制在預算之內。這一厚度範圍在木塑複合材料(WPC)地板市場也依然佔據重要地位,因為它適用於工期較短的翻新工程。此厚度的產品通常帶有整合墊片和標準化的卡扣,最大限度地減少了準備工作,並能實現高效的逐間安裝。此外,這項標準也與中檔住宅中廣泛使用的門檻和裝飾條相匹配,最大限度地減少了木工改造,並幫助安裝人員每天完成更多房間的安裝。不同厚度產品系列擁有標準化的顏色和紋理,使零售商柔軟性提案升級到更高等級的產品,而無需改變客戶偏好的外觀,從而加強了產品組合管理。這些特點結合起來,意味著5-6毫米厚度的產品仍然是建築商和物業管理人員的核心選擇,他們追求的是可預測的成本和可靠的性能。

預計到2031年,6.5-8毫米厚度的地板市場將以每年8.31%的速度成長,這主要得益於住宅對更舒適、更安靜的居住環境的需求,以及專業人士對帶襯墊的一體式結構的需求——這種結構無需自流平,且能容忍基層輕微的不平整。該系列的高階產品擁有更厚的芯材、更高規格的耐磨層以及更出色的外觀,使其在家庭活動頻繁的房間中,價格上漲也物有所值。產品頁面詳細介紹了地板的結構和耐磨性能,幫助承包商和客戶將這些產品合理地應用於客廳、家庭辦公室、書房以及其他對溫度舒適度和吸音效果要求較高的區域。這種趨勢也體現在小規模商業空間,例如私人辦公室和會議室,在這些空間中,柔軟的腳感和高階的外觀比最大的承重能力更為重要。這項成長策略得益於其產品系列的合理性:6.5-8毫米厚度的產品比入門級產品更厚,同時成本和安裝複雜度低於實木地板。

區域分析

預計到2025年,北美將佔整個市場的33%。這主要得益於翻新和地板材料更換的強勁需求,推動了WPC地板在臥室和起居空間(這些空間對保暖性和隔音性要求較高)的穩步普及。醫療保健和教育行業的設施業主繼續根據區域差異化設計,在某些區域使用觸感柔軟的產品,而在高人流量區域則採用硬質LVT或礦物芯材解決方案。與強迫勞動風險相關的貿易限制也影響採購趨勢,迫使進口商調整其原產地策略和文件處理方式,以避免貨物被扣押和延誤。國內和近岸地區對相關彈性地板材料系列的投資提高了整個品類的前置作業時間確定性,並改善了高運轉率設施的進度管理。在整個WPC地板市場,隨著各品牌努力協調產品教育和合規性,產品組合的多樣性和清晰的安裝指南仍然是零售市場的關鍵差異化因素。

預計到2031年,亞太地區將以8.60%的成長率成為該地區成長最快的市場,這反映了都市化、中檔住宅市場的擴張以及分銷基礎設施的持續改善。製造商正在全部區域實現生產能力多元化,以提高韌性並縮短運往主要出口目的地的運輸時間,從而降低地緣政治和政策風險。在區域供應鏈中,材料文件和低排放飾面對於維持進入監管市場至關重要,有助於簡化海關程序並增強客戶信心。加厚芯層和軟墊飾面的日益普及符合消費者在人口密集居住環境中對舒適性和降噪等需求。隨著主要城市線上線下銷售管道的日益成熟,符合流行室內風格並提供可靠交貨時間的產品系列正在推動全部區域彈性地板材料的轉換率不斷提高。

在歐洲,木塑複合材料(WPC)地板市場仍保持著相當大的佔有率,這主要得益於住宅存量的長期現代化改造以及優先考慮低排放產品和安全表面化學品的法規結構。這些因素正在影響彈性地板材料的規格。雖然WPC地板在二樓房間和某些商業空間仍然具有吸引力,但針對某些化學品類別的更嚴格監管正在促使人們重新評估飾面和黏合劑。在該地區銷售的品牌正在透過更嚴格地記錄材料選擇和利用第三方測試來簡化機構投資者的合規流程。強調性能、認證和美觀多樣性的產品線有利於在專業零售和承包商通路中獲得貨架空間。監管解釋和產品標籤的一致性正在推動WPC地板市場的可預測性規劃,這對跨境企業發展至關重要。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 卡扣式硬乙烯基地板材料非常適合 DIY 項目,正在加速住宅裝修。

- 多層住宅防水和隔音舒適性的優勢

- 入門級SPC產品品質出現問題,而高階WPC市場正呈現復甦趨勢。

- 全通路發現和視覺化可提高轉換率。

- 如果因洪水災害需要更換地板(通常由保險公司承保),則首選防水、硬質地板。

- 超厚 WPC(10-12 毫米,最大可達 19 毫米)可作為硬木的替代品,無需更換裝飾條。

- 市場限制因素

- SPC的低成本和高抗凹陷性正在從WPC手中奪取市場佔有率。

- 對聚氯乙烯化學品的更嚴格監管和貿易壁壘增加了合規成本。

- 依賴進口的WPC面臨UFLPA和物流方面的干擾。

- 在醫療和教育領域,用於行動負載的 WPC 在商業規範中的優先順序正在下降。

- 產業價值鏈分析

- 波特五力分析

- 洞察最新產業趨勢與創新

- 近期產業趨勢分析(新產品發布、策略性舉措、投資、合作、合資、業務擴張、併購等)

第5章 市場規模與成長預測

- 依產品類型

- 聚乙烯

- 高密度聚苯乙烯(HDPE)

- 低密度聚乙烯(LDPE)

- 聚氯乙烯

- 硬質PVC

- 軟PVC

- 聚丙烯

- 均聚聚丙烯

- 共聚物聚丙烯

- 其他產品類型

- 聚乙烯

- 按厚度

- 3.5~4 mm

- 5~6 mm

- 6.5~8 mm

- 8毫米或以上

- 透過安裝方法

- 托樑與夾扣系統

- 黏牢

- 互鎖/卡扣

- 其他

- 最終用戶

- 住宅

- 商業

- 透過分銷管道

- B2C/一般消費者

- 家居建材商店

- 地板材料專賣店

- 線上

- 當地金屬製品(非正規市場)

- 其他分銷管道

- B2B/承包商/建築公司

- B2C/一般消費者

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Shaw Industries(incl. Shaw Floors)

- COREtec Floors(USFloors/Shaw)

- Mannington Mills

- Mohawk Industries

- The Dixie Group(TRUCOR)

- Johnson Hardwood

- Lions Floor

- Southwind Floors

- MSI Surfaces

- AHF Products(Robbins)

- Metroflor(HMTX Industries)

- Karndean Designflooring

- Novalis Innovative Flooring

- Tarkett

- Karastan

- CFL Flooring

- Taizhou Huali New Materials

- Decno Group

- Provenza Floors

- Biyork

第7章 市場機會與未來展望

According to Mordor Intelligence, the wood plastic composite flooring market size is expected to grow from USD 6.27 billion in 2025 to USD 6.57 billion in 2026 and is forecast to reach USD 9.44 billion by 2031 at 7.51% CAGR over 2026-2031.

This report is Segmented by Product Type (Polyethylene, PVC, Polypropylene, Others), Thickness (3. 5-4 Mm, 5-6 Mm, 6. 5-8 Mm, Above 8 Mm), Installation Method (Click-Lock, Glue-Down, Others), End User, Distribution Channel (B2C, B2B), and Geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Wood Plastic Composite Flooring Market Trends and Insights

DIY-Friendly Click-Lock Rigid Vinyl Accelerates Residential Remodels

Click-lock construction remains central to the value proposition in the wood plastic composite flooring market because it reduces job duration, simplifies training, and lowers rework risk in occupied homes. Large brands continue to refine profile geometry and edge stability to support faster installs with consistent finished-floor flatness, which eases scheduling in tight remodel windows. At retail, collections that package locking systems with matched trims and underlayment kits help homeowners and pros move from sample to completion with fewer decision points, which benefits conversion and satisfaction. Manufacturers that offer installation-ready systems with one-price simplicity have seen strong reception in recent product cycles, indicating that execution certainty is a critical purchase driver for remodels. Distribution programs that guarantee short lead times and regional stock also support DIY and pro remodels, as contractors can commit to dates with confidence and avoid delays tied to transoceanic shipments.

Waterproof and Acoustic Comfort Advantages in Multi-Level Housing

Multi-level housing projects favor products that control sound transmission and deliver a warmer underfoot experience, which sustains demand for WPC in bedrooms, lofts, and mezzanines. Collections that integrate thicker cores with engineered pads offer a balanced footprint that helps manage subfloor variation while improving step-sound characteristics, which matters in conversions and basements. Premium WPC lines also bundle high-wear surfaces with attached foam to deliver comfort and scratch resistance, which broadens their use into family rooms and media rooms where occupants prioritize quiet floors. Commercial and mixed-use properties apply similar criteria for select zones, especially where a softer feel and low-maintenance cleaning profile are preferred over maximum static load resistance, which keeps WPC in the specification mix. Product data sheets that highlight thermal and acoustic performance, alongside moisture tolerance, support clear positioning in the wood-plastic composite flooring market for projects where acoustic comfort is critical.

SPC's Lower Cost and Higher Dent Resistance Cannibalize WPC

Projects that prioritize dent resistance under rolling loads and stacked furniture often specify mineral-core rigid products or commercial-grade LVT, which creates competition for WPC in corridors and cafeterias. Facility managers in healthcare and education seek hard-surface warranties and surface-hardness solutions that maintain appearance over long service intervals, which typically narrow the field to rigid LVT families with proven track records. In entry-price residential projects where the total budget is fixed, buyers often trade underfoot comfort for lower material cost and higher static-load ratings to satisfy move-in schedules. That dynamic can slow WPC adoption in specific sub-segments, despite its strengths in comfort and impact sound control. As product lines evolve, WPC continues to retain share in rooms where dwellers prioritize warmth and noise control. At the same time, rigid LVT and mineral-core options remain common in heavy-traffic zones, which sustains a pragmatic split of use cases in the wood plastic composite flooring market.

Other drivers and restraints analyzed in the detailed report include:

- Premium WPC Rebound Amid Quality Issues in Entry-Level SPC Tiers

- Omnichannel Discovery and Visualization Improve Conversion

- Tightening PVC Chemical Policies and Trade Barriers Raise Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene-based WPC led the product mix with 40% in 2025, while polypropylene is projected to grow at an 8.15% CAGR to 2031. Among commodity polymers through 2031, positioning both as anchors for pricing ladders that cover entry, mid, and premium tiers in the wood plastic composite flooring market. In practice, polyethylene variants are selected for their balanced density and resilience, which support comfortable step-sound performance and make them a fit for upstairs rooms and mixed-traffic residential zones. Product lines that emphasize dimensional stability across seasonal swings gain favor with installers who want to avoid callbacks related to gapping and edge telegraphing, which helps polyethylene families maintain mindshare. Polypropylene draws attention where higher heat-deflection tolerance is desired, particularly in sun-exposed rooms or warmer geographies, and that characteristic opens new placements, widening the overall addressable set. Brands that blend higher-spec cores with durable wear layers direct these collections toward homeowners who prefer a softer feel over maximum indentation resistance, keeping the portfolio logic consistent across both polymers.

The regulatory context reinforces material selection patterns as manufacturers evaluate plasticizer choices and certification targets for resilient surfaces above composite cores. Company disclosures suggest steady progress on recycled content and substitution strategies as brand owners seek routes to lower-carbon resilience across adjacent product families. In the wood-plastic composite flooring market, product managers are also shaping assortments so that clear use-case narratives guide selection by room and traffic level, limiting misapplications that can trigger warranty events. Where portfolios connect wear-layer durability to core stability and pad integration, the combination aligns user expectations with delivered performance, which supports repeat business and higher NPS scores for retailers. This pattern of polymer positioning, certification alignment, and room-by-room specification continues to define how brands defend share against mineral-core alternatives in overlapping price bands.

The 5-6mm band accounted for 56.72% in 2025, as buyers in cost-sensitive projects selected options that meet indentation and comfort expectations without pushing total installed cost above budget, and the tier's fit with quick-turn remodels keeps it prominent in the wood-plastic composite flooring market. Lines at this thickness typically integrate attached pads and consistent click profiles, which minimize prep and enable efficient room-by-room installs. The format also aligns with a large installed base of thresholds and trims in mid-market homes, limiting carpentry changes and helping installers finish more rooms per day. Portfolios that match colorways and textures across thicknesses give retailers flexibility to step customers up without changing the visual they fell in love with, which strengthens mix management. These features combine to keep the 5-6mm category central for builders and property managers who require predictable cost and reliable performance.

The 6.5-8mm tier is projected to grow at 8.31% through 2031, supported by homeowners who want more comfort and a quieter floor, and by pros who value pad integration that tolerates small subfloor variances without self-leveling. Premium lines in this range highlight thicker cores, higher-spec wear layers, and stronger visuals to justify a step-up ticket for rooms where families spend more time. Product pages that detail construction and wear performance help both installers and customers place these SKUs correctly in living rooms, home offices, and dens where thermal comfort and sound absorption are valued. The narrative also holds in light-commercial pockets, such as private offices and conference rooms, where a softer step and a premium look win out over maximum load capacity. This growth thesis is sustained by a portfolio logic that slots 6.5-8mm above entry tiers while staying under hardwood in cost and complexity.

Complete Report Scope:

- By Product Type

- Polyethylene

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polyvinylchloride

- Rigid PVC

- Flexible PVC

- Polypropylene

- Homopolymer Polypropylene

- Copolymer Polypropylene

- Other Product Types

- Polyethylene

- By Thickness

- 3.5-4 mm

- 5-6 mm

- 6.5-8 mm

- Above 8 mm

- By Installation Method

- Joist-and-Clip System

- Glue-Down

- Interlocking/Click-lock

- Others

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C / Retail Consumers

- Home Centers

- Specialty Flooring Stores

- Online

- Local Hardware Shops (unorganized market)

- Other Distribution Channels

- B2B / Contractors / Builders

- B2C / Retail Consumers

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Geography Analysis

North America accounted for 33% in 2025 as resilient demand from remodeling and replacement sustained steady placements for WPC in bedrooms and living spaces where warmth and sound control matter. Owners in healthcare and education continue to split specifications by zone, reserving softer-feel formats for select areas while using rigid LVT or mineral-core solutions under heavier loads. Trade enforcement related to forced-labor risk has also shaped procurement, prompting importers to adjust origin strategies and documentation practices to avoid detentions and delays. Domestic and nearshore investments in adjacent resilient families strengthen lead-time assurance across the broader category, which improves scheduling for high-utilization facilities. Portfolio variety and clear installation guidance remain points of differentiation in retail, as brands work to align product education with compliance readiness across the wood plastic composite flooring market.

Asia-Pacific is projected to post the fastest regional growth at 8.60% through 2031, reflecting urbanization, mid-market housing expansion, and ongoing improvements in channel infrastructure. Manufacturers continue to diversify capacity across the region to improve resilience and shorten transit times to key export destinations, which mitigates geopolitical and policy risk. Regional supply chains increasingly emphasize materials documentation and low-emission finishes to maintain access to regulated markets, and these efforts support smoother customs clearance and customer confidence. Growing adoption of thicker cores and attached pads aligns with buyer priorities for comfort and noise control in higher-density living. As online and offline channels mature in key cities, assortments that match popular interior styles and provide reliable delivery windows lift conversion for resilient floors across the region.

Europe maintains a substantial share driven by long-term modernization of housing stock and regulatory frameworks that prioritize low-emission products and safer surface chemistries, which influence specification criteria for resilient flooring. WPC's appeal in upstairs rooms and select commercial settings remains consistent, while stricter rules around certain chemical classes are steering reformulation in finishes and adhesives. Brands selling into the region are documenting materials choices with greater rigor and leaning on third-party testing to streamline compliance for institutional buyers. Portfolios that emphasize performance, certification, and aesthetic range are well placed to hold shelf space in specialty retail and builder channels. Consistency in regulatory interpretation and product labeling supports predictable planning in the wood plastic composite flooring market, which is valuable for cross-border programs.

- Shaw Industries (incl. Shaw Floors)

- COREtec Floors (USFloors/Shaw)

- Mannington Mills

- Mohawk Industries

- The Dixie Group (TRUCOR)

- Johnson Hardwood

- Lions Floor

- Southwind Floors

- MSI Surfaces

- AHF Products (Robbins)

- Metroflor (HMTX Industries)

- Karndean Designflooring

- Novalis Innovative Flooring

- Tarkett

- Karastan

- CFL Flooring

- Taizhou Huali New Materials

- Decno Group

- Provenza Floors

- Biyork

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 DIY-friendly click-lock rigid vinyl accelerates residential remodels

- 4.2.2 Waterproof and acoustic comfort advantages in multi-level housing

- 4.2.3 Premium WPC rebound amid quality issues in entry-level SPC tiers

- 4.2.4 Omnichannel discovery and visualization improve conversion

- 4.2.5 Insurance-driven water-loss replacements favor waterproof rigid floors

- 4.2.6 Extra-thick WPC (10-12 mm; up to 19 mm) as hardwood substitute without trim changes

- 4.3 Market Restraints

- 4.3.1 SPC's lower cost and higher dent resistance cannibalize WPC

- 4.3.2 Tightening PVC chemical policies and trade barriers raise compliance costs

- 4.3.3 Import-reliant WPC faces UFLPA and logistics disruptions

- 4.3.4 Commercial specs de-prioritize WPC for rolling loads in healthcare/education

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Industry

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD Billion)

- 5.1 By Product Type

- 5.1.1 Polyethylene

- 5.1.1.1 High-Density Polyethylene (HDPE)

- 5.1.1.2 Low-Density Polyethylene (LDPE)

- 5.1.2 Polyvinylchloride

- 5.1.2.1 Rigid PVC

- 5.1.2.2 Flexible PVC

- 5.1.3 Polypropylene

- 5.1.3.1 Homopolymer Polypropylene

- 5.1.3.2 Copolymer Polypropylene

- 5.1.4 Other Product Types

- 5.1.1 Polyethylene

- 5.2 By Thickness

- 5.2.1 3.5-4 mm

- 5.2.2 5-6 mm

- 5.2.3 6.5-8 mm

- 5.2.4 Above 8 mm

- 5.3 By Installation Method

- 5.3.1 Joist-and-Clip System

- 5.3.2 Glue-Down

- 5.3.3 Interlocking/Click-lock

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C / Retail Consumers

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Local Hardware Shops (unorganized market)

- 5.5.1.5 Other Distribution Channels

- 5.5.2 B2B / Contractors / Builders

- 5.5.1 B2C / Retail Consumers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South-East Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Shaw Industries (incl. Shaw Floors)

- 6.4.2 COREtec Floors (USFloors/Shaw)

- 6.4.3 Mannington Mills

- 6.4.4 Mohawk Industries

- 6.4.5 The Dixie Group (TRUCOR)

- 6.4.6 Johnson Hardwood

- 6.4.7 Lions Floor

- 6.4.8 Southwind Floors

- 6.4.9 MSI Surfaces

- 6.4.10 AHF Products (Robbins)

- 6.4.11 Metroflor (HMTX Industries)

- 6.4.12 Karndean Designflooring

- 6.4.13 Novalis Innovative Flooring

- 6.4.14 Tarkett

- 6.4.15 Karastan

- 6.4.16 CFL Flooring

- 6.4.17 Taizhou Huali New Materials

- 6.4.18 Decno Group

- 6.4.19 Provenza Floors

- 6.4.20 Biyork

7 Market Opportunities & Future Outlook

- 7.1 Domestic/nearshore WPC capacity to mitigate tariff/UFLPA risk and shorten lead times

- 7.2 Ultra-thick WPC (>=10-12 mm; 19 mm) for premium hardwood replacement in remodels

木塑複合材料市場報告:按類型、應用和地區分類(2026-2034 年)

木塑複合材料市場報告:按類型、應用和地區分類(2026-2034 年) 木塑複合材料市場:按材料類型、形狀、製造技術、應用和分銷管道分類-2026-2032年全球市場預測

木塑複合材料市場:按材料類型、形狀、製造技術、應用和分銷管道分類-2026-2032年全球市場預測 2026年全球木塑複合地板材料市場報告

2026年全球木塑複合地板材料市場報告 木塑複合材料市場:按類型、應用和地區分類木塑複合材料機械市場:按機器類型、自動化類型、產能、應用、最終用戶分類,全球預測(2026-2032年)

木塑複合材料市場:按類型、應用和地區分類木塑複合材料機械市場:按機器類型、自動化類型、產能、應用、最終用戶分類,全球預測(2026-2032年) 木塑複合材料(WPC):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

木塑複合材料(WPC):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球木塑複合材料地板市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球木塑複合材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本木塑複合材料市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年

全球木塑複合材料地板市場規模、佔有率、趨勢及成長分析報告(2026-2034)全球木塑複合材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本木塑複合材料市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年 木塑複合材料市場-全球產業規模、佔有率、趨勢、機會及預測(按塑膠材料、最終用途產業、地區和競爭格局分類,2021-2031年)

木塑複合材料市場-全球產業規模、佔有率、趨勢、機會及預測(按塑膠材料、最終用途產業、地區和競爭格局分類,2021-2031年)