|

市場調查報告書

商品編碼

2073328

亞太地區SPC(石塑複合)地板:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific Stone Plastic Composite (SPC) Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

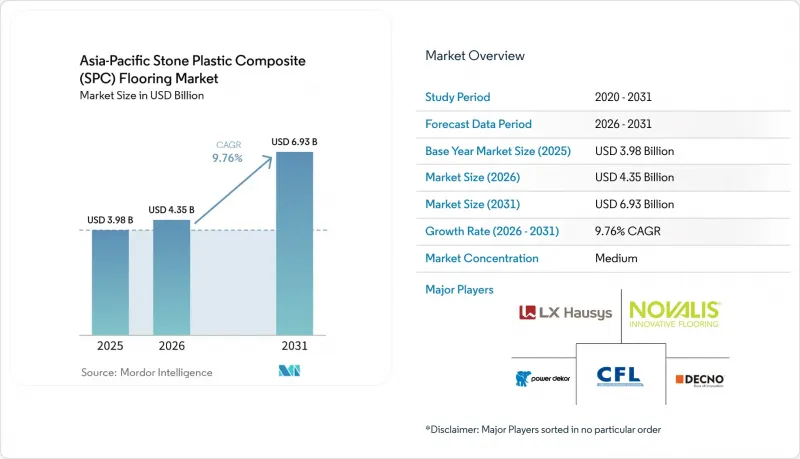

據 Mordor Intelligence 稱,2025 年亞太地區 SPC(石塑複合)地板市場價值為 39.8 億美元,預計到 2031 年將從 2026 年的 43.5 億美元成長至 69.3 億美元,預測期(2026-2031 年)複合成長率為 9.76%。

本報告按產品類型(SPC地磚、SPC板材)、產品厚度(4.0–5.0毫米、5.1–6毫米及其他)、安裝方式(互鎖/卡扣式及其他)、最終用戶(住宅、商業)、配銷通路(B2C/零售、B2B/承包商)和地區(印度、中國及其他)進行細分。市場預測以美元計價。

亞太地區SPC(石塑複合材料)地板市場的趨勢與見解。

中國的都市更新正在加速二線城市的地板材料更換週期。

中國推廣環保材料和低VOC(揮發性有機化合物)建築材料的政策,推動了剛性芯材地板在新建和翻新工程中的應用日益廣泛,從而支撐了大規模城市地區的地板材料更換週期。根據中國國家統計局數據顯示,中國都市化已超過65%,二線城市的住宅週轉率持續成長。在許多此類市場,公寓地板材料更換與房地產的二手房交易週期密切相關。防水卡扣式SPC系統(通常厚度為4-6毫米,耐磨層厚度為0.3-0.7毫米,符合ASTM F3261等彈性地板材料標準)相比瓷磚系統(需要24-72小時的黏合劑固化時間)可顯著縮短安裝工期。中國領先的製造商已投入研發更高密度的芯材和更厚的耐磨層。同時,一些企業集團正在越南和泰國等地增設平行生產基地,以更好地穩定受關稅影響的出口管道的供應。目前,河北和江蘇兩省的生產基地與東南亞的產能形成互補,平衡了前置作業時間,並增強了應對貿易政策波動的能力。這些供應方面的改善,加上中國穩步推進的翻新改造,正促使亞太地區內陸和沿海買家更廣泛地參與SPC地板市場。

防水剛性芯卡扣系統顯著縮短了維修前置作業時間。

SPC的防水石灰石和PVC芯材以及免工具卡扣式安裝系統顯著縮短了翻新工期,與粘合式PVC地板材料相比,安裝時間縮短了30-50%,這符合彈性地板材料安裝指南和基於ASTM F3261標準的安裝規範。這凸顯了其在公寓和高周轉率商業空間的重要性,因為運作會直接影響收入。住宅非常重視運作中、浴室和入口處的防水性能,而卡扣式安裝系統可以減少維修對居住在小型都市區公寓的家庭日常生活造成的干擾。這種硬芯產品直接安裝在現有基材上,最大限度地減少了拆除工作,並降低了對底層地面處理材料的需求,從而降低了人工成本,並使維修能夠在夜間或週末進行。因此,在亞太地區,SPC地板市場在住宅和商業房地產翻新項目中持續獲得認可,因為可預測的工期和順利的交接至關重要。

強制性生產者責任延伸制度(EPR)和循環經濟規範增加了單位產品的合規負擔。

在整個東協地區,生產者延伸責任制(EPR)框架正在不斷加強,要求生產商收集、回收或資助管理項目,從而提高了塑膠價值鏈的合規義務。在越南,作為其EPR政策的一部分,回收是強制性的,否則必須向國家環境保護基金捐款,類似的舉措也正在影響鄰近市場的產業計畫。在菲律賓,EPR法案(第11898號共和國法案)正逐步提高大型企業的回收義務,要求在2028年分階段將回收率提高到80%。這直接影響進口彈性地板材料的包裝設計、標籤和產品管理。澳洲競爭監管機構已批准彈性地板材料的「ResiLoop」管理項目,該項目支持回收和再利用機制,並已成為許多規範制定者視為供應商資質要求的重要先例。這些變化為依賴PVC的供應鏈帶來了新的成本項目和流程要求,亞太地區的SPC地板材料市場正在對產品設計和文件進行審查,以符合公共採購和大型企業永續發展標準。

細分市場分析

2025年,SPC板材憑藉其親切的木紋外觀和便利的卡扣式安裝系統,在亞太SPC地板市場佔據主導地位,市佔率高達74.71%,尤其適用於住宅裝修專案。 SPC地磚採用「預先灌漿」表面技術,無需灌漿即可呈現類似磁磚的外觀,預計到2031年將以8.20%的複合年成長率成長。這加速了其在潮濕空間和商業浴室翻新中的應用。製造商正在授權採用整合式灌漿線表面處理技術,該技術可在一塊面板上模擬兩塊磁磚的效果,從而降低佈局複雜性,並縮短交錯鋪設的安裝步驟。在施工運作較為敏感的市場中,無需管道工程的卡扣式地磚是砂漿鋪貼瓷磚的實用替代方案,這也是亞太地區SPC地板市場在浴室、入口和其他潮濕區域持續成長的主要原因。隨著產品線擴展到新的尺寸和飾面,瓷磚形式的 SPC 增強了設計的連續性,尤其是在開放式空間和相鄰房間中與木板一起使用時。

在日本和韓國,隔音性能是產品選擇的關鍵因素,符合LL40或LL45標準的潮濕區域專用瓷磚式產品正逐漸成為多用戶住宅翻新的標準配置。開發商傾向於採用更重、密度更高的芯材,並內置發泡墊,以降低垂直居住環境中的撞擊噪音,因為這些區域的噪音傳播受到物業管理協會的嚴格監管。對於專案經理而言,無需拆除現有地板即可採用浮動式安裝SPC瓷磚,可以降低人事費用和工時,這比材料成本的細微差別更為重要。隨著這些技術和實用優勢的積累,瓷磚式產品擴大應用於潮濕區域。同時,在亞太地區的SPC地板市場,木板式產品仍在起居室、走廊和臥室等區域佔據主導地位。因此,一種清晰的「雙規格」策略已經形成,瓷磚和木板相互補充,在實現統一美感的同時,還能減少維護工作並縮短工期。

到2025年,5.1-6.0毫米厚度的產品將佔總銷售量的35.40%,對於那些不需要高階隔音層且僅需標準剛性的住宅和建築商而言,該厚度規格在成本和安裝方面都是最佳選擇。在翻新維修中,4.0-4.5毫米厚度的產品更受歡迎,尤其是在房間間距較小的公寓中,因為門和門檻的高度限制了地板厚度。許多供應商正在最佳化中等厚度的產品,這些產品具有穩定的芯材和耐磨保護層,能夠滿足日常住宅的性能需求,並支撐亞太地區SPC地板市場該細分領域的銷售量。對於聲學要求不高的住宅商而言,5.0-5.5毫米厚度的產品之所以仍保留在標準配置清單中,是因為它具有可預測的卡扣式安裝性能和較低的返工率。隨著中國和越南供應鏈的不斷擴展,大多數經銷商都提供該厚度範圍內的各種產品,以平衡區域市場的價格範圍和設計多樣性。

預計到2031年,厚度超過6.5毫米的超厚地板市場將以8.57%的複合年成長率成長。這主要是由於日本和韓國對地板衝擊聲學性能有嚴格的要求,因此消費者更傾向於選擇預裝IXPE或EVA墊層的產品。許多公寓管理協會和房地產管理公司在更換地板材料時,都要求地板達到LL40或LL45級別的性能標準,這促使規範制定者選擇高密度芯材和厚實底層地板的產品,以抑制衝擊聲的傳遞。厚度為6.5-7.0毫米、帶有整體模壓墊層的優質地板通常具備符合公寓通用規範的IIC和STC等級,這使得亞太地區SPC地板市場的買家更加關注高附加價值產品。在預算有限且聲學標準不那麼嚴格的情況下,6.0-6.5毫米的厚度範圍仍然是一個可行的折中選擇。然而,監管趨勢正在推動高層建築地板材料更換產品轉向更厚產品。因此,製造商們正不斷投資開發墊片安裝生產線和高密度芯材配方,以滿足這種高階需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中國城市更新帶動了房屋維修需求。

- 防水硬質內芯和卡扣式鎖定機制可快速維修。

- 醫療、飯店和零售業的實施狀況和設備升級

- 由於亞太地區SPC產能的擴張,供應正在改善。

- 由於公寓的隔音標準(LL45/LL40),需要使用更厚的SPC(結構塑膠混凝土)。

- 預灌漿SPC磁磚的創新應用,使得磁磚式安裝速度更快。

- 市場限制因素

- PVC永續性/因EPR而增加的合規成本

- 聚氯乙烯和塑化劑原料價格的波動

- 與瓷磚和工程木地板競爭。

- 公寓大樓的噪音管制規定增加了安裝音響系統的成本。

- 產業價值鏈分析

- 波特五力分析

- 洞察最新產業趨勢與創新

- 近期產業趨勢分析(新產品發布、策略性舉措、投資、合作、合資、業務擴張、併購等)

第5章 市場規模與成長預測

- 依產品類型

- SPC磁磚

- SPC板材

- 產品厚度(依類別)

- 4.0~5.0 mm

- 5.1~6.0 mm

- 6.1~6.5 mm

- 6.5毫米或以上

- 透過安裝方法

- 自黏式

- 黏牢

- 互鎖/卡扣

- 其他

- 最終用戶

- 住宅

- 商業

- 透過分銷管道

- B2C/零售

- 家居建材商店

- 地板材料專賣店

- 線上

- 當地金屬製品(非正規市場)

- 其他分銷管道

- B2B/承包商

- B2C/零售

- 按地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略性舉措(產能、合資企業、出口目的地轉變)

- 市佔率分析

- 公司簡介

- CFL Flooring(Creative Flooring Solutions)

- Power Dekor Group

- Novalis Innovative Flooring

- DECNO GROUP Ltd.

- Armstrong Flooring Asia

- LX Hausys(HFLOR)

- Zhejiang GIMIG Technology

- Protex Flooring(Changzhou)

- TopJoy Industrial

- Hanflor(Hanhent International)

- EFLOOR(E-Block JSC., Vietnam)

- HAODIBAN

- Proluxe Floor(Changzhou)

- Jiangsu Kentier Wood

- Zhangjiagang Yihua Rundong New Material

- Cicko Flooring

- Zhejiang Ballun Ecological Household

- Changzhou Aojia Decorate Material

- Changzhou Lexuan New Material

- Changzhou Yuhe New Construction Materials

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific stone plastic composite flooring market size was valued at USD 3.98 billion in 2025 and is estimated to grow from USD 4.35 billion in 2026 to reach USD 6.93 billion by 2031, at a CAGR of 9.76% during the forecast period (2026-2031).

This report is Segmented by Product Type (SPC Tiles, SPC Planks), Product Thickness (4. 0-5. 0 Mm, 5. 1-6 Mm, and More), Installation Method (Interlocking/Click-lock, and More), End User (Residential, Commercial), Distribution Channel (B2C/Retail and B2B/Contractors), and Geography (India, China, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Stone Plastic Composite (SPC) Flooring Market Trends and Insights

China Urban Renewal Amplifies Tier-2 Replacement Cycles

China's policy direction for greener materials and lower-VOC construction products is encouraging wider use of rigid-core flooring in both newbuilds and renovations, which supports replacement cycles in large tier-2 and tier-3 city clusters. According to the National Bureau of Statistics of China, the country's urbanization rate has exceeded 65%, reinforcing sustained residential turnover in secondary cities. In many of these markets, apartment flooring replacement is closely linked to property resale cycles. Waterproof click-lock SPC systems (typically 4-6 mm thick with 0.3-0.7 mm wear layers, as defined in resilient flooring specifications such as ASTM F3261) reduce installation downtime compared with ceramic tile systems, which require adhesive curing periods of 24-72 hours. Leading Chinese manufacturers have invested in denser core profiles and higher-wear layers. At the same time, some groups have added parallel bases in Vietnam or Thailand to serve tariff-sensitive export lanes more predictably. Production footprints in Hebei and Jiangsu now complement Southeast Asian capacity, helping balance lead times and improving resilience to trade policy swings. As these supply-side improvements align with China's steady renovation cadence, the Asia-Pacific SPC flooring market is seeing broader geographic participation from both inland and coastal buyers.

Waterproof Rigid-Core Click Systems Collapse Refurbishment Lead Times

SPC's waterproof limestone-PVC core and tool-free click systems significantly shorten renovation projects, reducing installation times by 30-50% compared with glue-down vinyl systems, as indicated in resilient flooring installation guidelines and ASTM F3261-based application practices. This makes it important for occupied apartments and fast-turnover commercial spaces where downtime directly affects revenue. Residential buyers place a high value on waterproofing for kitchens, bathrooms, and entries, and click-lock installation lowers disruption for families in small urban flats during refurbishments. Rigid-core formats installed over existing substrates limit demolition and reduce the need for leveling compounds, cutting labor hours, and making overnight or weekend retrofits feasible. As a result, the Asia-Pacific SPC flooring market continues to win specifications in both residential and commercial refresh programs where predictable schedules and clean turnarounds are essential.

EPR Mandates and Circularity Specifications Inflate Per-Unit Compliance Burdens

Extended Producer Responsibility (EPR) frameworks are tightening across ASEAN, pushing producers to fund collection, recycling, or stewardship schemes and increasing compliance obligations for plastics value chains. In Vietnam, the EPR policy includes mandated recycling or financial contributions to a national environmental protection fund, and similar approaches are influencing business planning in neighboring markets. In the Philippines, the EPR Act (Republic Act No. 11898) sets escalating recovery obligations for large enterprises, with mandated recovery rates increasing progressively up to 80% by 2028, directly influencing packaging, labeling, and product stewardship design for imported resilient flooring materials. Australia's competition regulator authorized the ResiLoop stewardship program for resilient flooring, which supports a collection and recycling pathway and sets a precedent that many specifiers now look for in supplier credentials. These changes create new cost items and process requirements for supply chains that rely on PVC, and the Asia-Pacific SPC flooring market is adjusting product designs and documentation to align with public procurement and large-firm sustainability criteria.

Other drivers and restraints analyzed in the detailed report include:

- Healthcare, Hospitality, and Retail Prioritize Low-Lifecycle-Cost Surfaces

- APAC Capacity Build-Out Tightens Lead Times and Localizes Supply Chains

- Feedstock Price Surges Triggered by Supply Disruptions and Refinery Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SPC planks dominated the Asia-Pacific SPC flooring market with a 74.71% share in 2025, supported by familiar wood-look aesthetics and straightforward click installations for residential refresh projects. SPC tiles are projected to expand at a 8.20% CAGR through 2031, aided by pre-grouted surface technologies that deliver the look of ceramic without grout maintenance, accelerating adoption in wet-room retrofits and commercial bathrooms. Manufacturers are licensing integrated grout-line surface treatments that simulate two tiles on one panel, reducing layout complexity and potentially reducing installation steps for staggered patterns. In markets sensitive to downtime, tiles that click into place without wet trades are a practical alternative to mortar-set ceramic, which is a key reason the Asia-Pacific SPC flooring market continues to expand in bathrooms, entryways, and other wet zones. As product lines broaden into new sizes and finishes, tile-format SPC is improving design continuity alongside plank installations across open-plan spaces and adjacent rooms.

Acoustic compliance in Japan and South Korea is central to product selection, and wet-area tile formats that meet LL40 or LL45 standards are becoming a staple of multi-family retrofits. Developers lean toward heavier, denser cores with integrated foam pads to manage impact sound in vertical living arrangements where noise transmission is regulated by building associations. For project managers, the ability to install SPC tiles as a floating system over existing surfaces without demolition reduces labor and time, which can matter more than small differences in material costs. As these technical and practical features stack up, tiles are capturing more wet-room specifications. At the same time, planks continue to dominate living areas, corridors, and bedrooms across the Asia-Pacific SPC flooring market. The net effect is a clear two-format strategy where tiles complement planks to deliver a uniform aesthetic with lower maintenance and faster project turnover.

The 5.1-6.0 mm thickness category accounted for 35.40% of 2025 revenues, serving as a cost-and-handling sweet spot for homeowners and builders who need standard rigidity without premium acoustic layers. In overlay retrofits, thinner 4.0-4.5 mm products are preferred where door and threshold heights limit build-up, especially in apartments with tight tolerances between rooms. Many suppliers are optimizing mid-thickness SKUs with stable cores and protective wear layers that meet everyday residential performance needs, which sustains volume in this segment across the Asia-Pacific SPC flooring market. Residential installers cite predictable click performance and low call-back rates as reasons to keep 5.0-5.5 mm on standard spec lists where acoustic constraints are moderate. As supply chains scale in China and Vietnam, most distributors carry deep assortments in this thickness range to balance price points and design variety for regional markets.

Ultra-thick formats above 6.5 mm are forecast to grow at 8.57% CAGR through 2031, lifted by strict floor impact sound requirements in Japan and South Korea that favor pre-attached IXPE or EVA pads. Many condo associations and property managers enforce LL40 or LL45 equivalents for replacements, which point specifiers to higher-density cores and thicker underlayment layers to control impact transmission. Premium 6.5-7.0 mm planks with integrated pads often advertise IIC and STC ratings that meet common condominium rules, which shifts buyers toward higher-value SKUs within the Asia-Pacific SPC flooring market. The 6.0-6.5 mm tier remains a viable middle ground for budgets that are tighter and acoustic standards that are less prescriptive. Still, regulatory momentum is tilting replacements toward higher thicknesses in high-rise applications. As a result, manufacturers continue to invest in pad-attachment lines and denser core formulations to serve this premium demand profile.

Complete Report Scope:

- By Product Type

- SPC Tiles

- SPC Planks

- By Product Thickness

- 4.0-5.0 mm

- 5.1-6.0 mm

- 6.1-6.5 mm

- Above 6.5 mm

- By Installation Method

- Self-Adhesive

- Glue-Down

- Interlocking/Click-lock

- Others

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Flooring Stores

- Online

- Local Hardware Shops (unorganized market)

- Other Distribution Channels

- B2B/Contractors

- B2C/Retail

- By Geography

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines)

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- CFL Flooring (Creative Flooring Solutions)

- Power Dekor Group

- Novalis Innovative Flooring

- DECNO GROUP Ltd.

- Armstrong Flooring Asia

- LX Hausys (HFLOR)

- Zhejiang GIMIG Technology

- Protex Flooring (Changzhou)

- TopJoy Industrial

- Hanflor (Hanhent International)

- EFLOOR (E-Block JSC., Vietnam)

- HAODIBAN

- Proluxe Floor (Changzhou)

- Jiangsu Kentier Wood

- Zhangjiagang Yihua Rundong New Material

- Cicko Flooring

- Zhejiang Ballun Ecological Household

- Changzhou Aojia Decorate Material

- Changzhou Lexuan New Material

- Changzhou Yuhe New Construction Materials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 China urban renewal-fueled renovation demand

- 4.2.2 Waterproof rigid-core and click-lock enabling fast refurb

- 4.2.3 Adoption in healthcare, hospitality, retail upgrades

- 4.2.4 APAC SPC capacity expansions improving availability

- 4.2.5 Apartment sound insulation standards (LL45/LL40) push thicker SPC

- 4.2.6 Pre-grouted SPC tile innovations speeding tile-look installs

- 4.3 Market Restraints

- 4.3.1 PVC sustainability/EPR raising compliance costs

- 4.3.2 PVC/plasticizer feedstock price volatility

- 4.3.3 Competition from ceramic tile and engineered wood

- 4.3.4 Condo acoustic rules increasing installed system cost

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Industry

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD Billion)

- 5.1 By Product Type

- 5.1.1 SPC Tiles

- 5.1.2 SPC Planks

- 5.2 By Product Thickness

- 5.2.1 4.0-5.0 mm

- 5.2.2 5.1-6.0 mm

- 5.2.3 6.1-6.5 mm

- 5.2.4 Above 6.5 mm

- 5.3 By Installation Method

- 5.3.1 Self-Adhesive

- 5.3.2 Glue-Down

- 5.3.3 Interlocking/Click-lock

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C/Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Local Hardware Shops (unorganized market)

- 5.5.1.5 Other Distribution Channels

- 5.5.2 B2B/Contractors

- 5.5.1 B2C/Retail

- 5.6 By Geography

- 5.6.1 India

- 5.6.2 China

- 5.6.3 Japan

- 5.6.4 Australia

- 5.6.5 South Korea

- 5.6.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines)

- 5.6.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (capacity, JV, export shifts)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 CFL Flooring (Creative Flooring Solutions)

- 6.4.2 Power Dekor Group

- 6.4.3 Novalis Innovative Flooring

- 6.4.4 DECNO GROUP Ltd.

- 6.4.5 Armstrong Flooring Asia

- 6.4.6 LX Hausys (HFLOR)

- 6.4.7 Zhejiang GIMIG Technology

- 6.4.8 Protex Flooring (Changzhou)

- 6.4.9 TopJoy Industrial

- 6.4.10 Hanflor (Hanhent International)

- 6.4.11 EFLOOR (E-Block JSC., Vietnam)

- 6.4.12 HAODIBAN

- 6.4.13 Proluxe Floor (Changzhou)

- 6.4.14 Jiangsu Kentier Wood

- 6.4.15 Zhangjiagang Yihua Rundong New Material

- 6.4.16 Cicko Flooring

- 6.4.17 Zhejiang Ballun Ecological Household

- 6.4.18 Changzhou Aojia Decorate Material

- 6.4.19 Changzhou Lexuan New Material

- 6.4.20 Changzhou Yuhe New Construction Materials

7 Market Opportunities & Future Outlook

- 7.1 Acoustic-compliant thick SPC systems for Japan/Korea multi-family

- 7.2 Pre-grouted SPC tile systems for wet-room retrofits across China/SEA

2026年全球彈性地板材料市場報告

2026年全球彈性地板材料市場報告 彈性地板材料市場:2026-2032年全球市場預測(依產品類型、安裝方式、價格範圍、應用及通路分類)

彈性地板材料市場:2026-2032年全球市場預測(依產品類型、安裝方式、價格範圍、應用及通路分類) 豪華乙烯基板材(LVS)市場規模、佔有率和成長分析:按產品類型、最終用戶、分銷管道和地區分類-2026-2033年產業預測

豪華乙烯基板材(LVS)市場規模、佔有率和成長分析:按產品類型、最終用戶、分銷管道和地區分類-2026-2033年產業預測 全球抗衝擊地板材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球商用彈性地板材料市場報告

全球抗衝擊地板材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球商用彈性地板材料市場報告 彈性地板市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

彈性地板市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 彈性地板:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

彈性地板:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年) 彈性地板市場規模、佔有率和成長分析(按產品類型、應用和地區)- 產業預測 2025-2032

彈性地板市場規模、佔有率和成長分析(按產品類型、應用和地區)- 產業預測 2025-2032 全球彈性地板市場:市場規模、佔有率、趨勢、行業分析(依產品、應用、通路和地區)、未來預測(2025-2034年)德國彈性地板材料:市場佔有率分析、產業趨勢、成長預測(2025-2030)

全球彈性地板市場:市場規模、佔有率、趨勢、行業分析(依產品、應用、通路和地區)、未來預測(2025-2034年)德國彈性地板材料:市場佔有率分析、產業趨勢、成長預測(2025-2030)