|

市場調查報告書

商品編碼

2073327

非洲飼料著色劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Africa Feed Pigments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

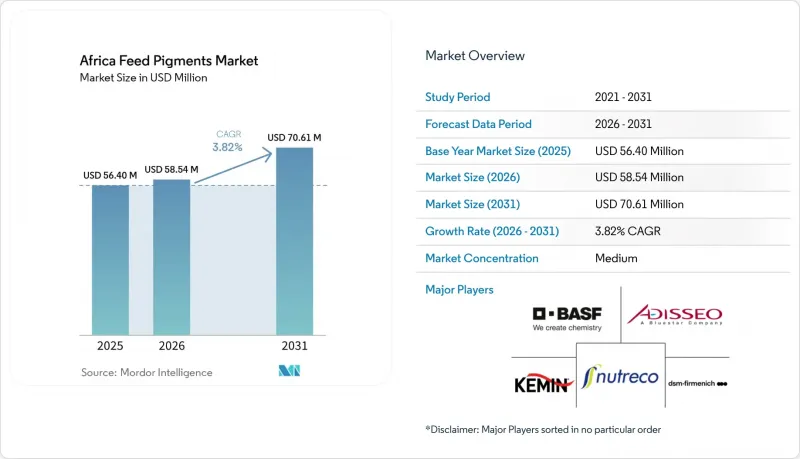

根據 Mordor Intelligence 預測,非洲飼料著色劑市場規模預計將在 2025 年達到 5,640 萬美元,從 2026 年的 5,854 萬美元成長到 2031 年的 7,061 萬美元,並在 2026 年至 2031 年的預測成長率內實現 3.82% 的複合年。

本報告按添加劑(類胡蘿蔔素、薑黃素、螺旋藻)、動物(水產養殖、家禽、反芻動物、豬及其他動物)和地區(埃及、肯亞、南非及其他非洲國家)進行細分。市場預測以價值(美元)和數量(公噸)呈現。

非洲飼料著色劑市場趨勢與洞察

家禽飼料需求不斷成長,以及對高品質雞蛋顏色的需求日益成長。

非洲飼料著色劑市場需求日益成長,尤其是在南非商業性家禽養殖業擴張的推動下。家禽業是南非農業部門最大的支柱產業,也是複合飼料的主要消費族群。根據美國農業部預測,在產業成長和飼料飼料提升的推動下,南非雞肉產量預計將從2025年的164萬噸成長至2026年的168萬噸。隨著家禽產量的成長,對類胡蘿蔔素等專用飼料添加劑的需求也上升。蛋雞養殖戶擴大在飼料中添加色素,以確保蛋黃顏色均勻,符合零售和品牌雞蛋項目的標準。由於蛋黃顏色對消費者的購買決策影響顯著,飼料色素已成為蛋雞飼料配方中不可或缺的成分,推動了整個家禽飼料行業的應用,並促進了非洲市場的成長。

商業飼料廠在非洲各地擴張

大規模商業飼料生產設施的建立正在鞏固非洲飼料色素市場的基礎。現代化的飼料廠配備了精準的配方和品管系統,能夠配製特種添加劑。例如,2026年2月,德赫斯(De Heus)在肯亞阿蒂河(Ati River)開設了一家飼料廠,初始年產能為24萬噸,服務於家禽、生豬、反芻動物和水產養殖業。此類投資透過工業化加工設施提高了飼料產量,並增強了飼料色素在畜禽生產中應用的潛力,從而提升產品品質和均勻性。隨著非洲商業性飼料產能的擴大,色素供應商受益於更廣泛的基本客群,這些客戶群體遵循標準化的飼料生產規範,推動了非洲飼料色素市場的成長。

對類胡蘿蔔素和色素預混合料的高度進口依賴

非洲飼料著色劑市場受到對進口特殊飼料添加劑(包括類胡蘿蔔素和色素預混合料)的嚴重依賴限制。這種高度依賴性增加了供應鏈中斷的風險,並導致採購成本上升。 2025年發表在《反芻動物》(Ruminants)雜誌上的一項研究指出,撒哈拉以南非洲地區飼料添加劑的高成本和取得難度是其引入畜牧系統的主要障礙。這些問題對於飼料著色劑而言尤其突出,因為飼料著色劑主要透過國際供應鏈採購,需要額外的物流和分銷系統。因此,在成本壓力較大的時期,飼料生產商可能會減少飼料配方中著色劑的添加量,從而限制市場滲透率,阻礙非洲飼料著色劑市場的成長。

細分市場分析

到2025年,薑黃素和螺旋藻將佔據非洲飼料著色劑市場51.4%的最大佔有率。薑黃素和螺旋藻憑藉其著色效果和功能性營養特性,深受商業性畜牧和水產養殖戶的青睞,並保持領先地位。它們的使用順應了人們對天然飼料成分日益成長的偏好,這些成分既能增強著色效果,又能提高動物生產力。這種雙重提案正在推動其在各種動物中的應用,並支撐著對天然著色解決方案的需求。

在非洲飼料著色劑市場中,類胡蘿蔔素市場預計將以4.0%的複合年成長率(CAGR)從2026年到2031年實現最高成長。這一成長主要得益於類胡蘿蔔素在水產養殖和家禽飼料應用的不斷擴大。在這些領域,魚肉、蝦、蛋黃和家禽皮的顏色是至關重要的品質指標。此外,類胡蘿蔔素還具有抗氧化特性,有助於促進動物健康和提高生產力。商業飼料生產的擴張和對優質動物蛋白產品需求的成長進一步推動了類胡蘿蔔素添加劑的應用。這些因素共同支撐了該細分市場長期強勁的成長前景。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 飼養的動物數量

- 家禽

- 反芻動物

- 豬

- 飼料生產

- 水產養殖

- 家禽

- 反芻動物

- 豬

- 法律規範

- 埃及

- 肯亞

- 南非

- 其他非洲國家

- 價值鍊和通路分析

- 市場促進因素

- 家禽飼料需求不斷成長,以及對顏色更佳、品質更高的雞蛋的需求不斷增加。

- 非洲各地商業飼料廠的擴張

- 擴大埃及、奈及利亞和東非的水產養殖規模

- 品牌雞肉產品逐步過渡到天然色素

- 現代零售和餐飲服務業對顏色一致性的要求

- 針對特定市場特種飼料原料的稅收和增值稅減免措施

- 市場限制因素

- 對類胡蘿蔔素和色素預混合料進口的高度依賴

- 出於成本考慮,家禽養殖方式限制了色素的添加量。

- 由於外匯短缺,添加劑的供應受到延誤。

- 分散物流網路中的溫度和儲存不穩定

- 波特五力分析

第5章 市場規模與成長預測

- 透過輔助添加劑

- 類胡蘿蔔素

- 薑黃素和螺旋藻

- 依動物類型

- 水產養殖

- 魚

- 蝦

- 其他養殖物種

- 家禽

- 肉雞

- 產蛋母雞

- 其他家禽

- 反芻動物

- 牛

- 牛

- 其他反芻動物

- 豬

- 其他動物

- 水產養殖

- 按地區

- 埃及

- 肯亞

- 南非

- 其他非洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF SE

- dsm-firmenich AG

- Kemin Industries, Inc.

- EW Nutrition GmbH(EW Group)

- Nutreco NV

- Adisseo(China National Bluestar(Group)Co., Ltd.)

- Kalsec, Inc.

- Synthite Industries Private Limited

- Divi's Laboratories Limited

- ROHA Dyechem Private Limited

- Industrias Vepinsa, SA de CV

- Innov Ad NV/SA(PAI Partners)

- Bioergex SA

- Behn Meyer Holding AG

- Phytobiotics Futterzusatzstoffe GmbH

第7章:執行長面臨的關鍵策略問題

According to Mordor Intelligence, the africa feed pigments market was valued at USD 56.40 million in 2025 and is projected to grow from USD 58.54 million in 2026 to USD 70.61 million by 2031, registering a CAGR of 3.82% during the forecast period from 2026 to 2031.

This report is Segmented by Sub-Additive (Carotenoids, and Curcumin and Spirulina), by Animal (Aquaculture, Poultry, Ruminants, Swine, and Other Animals), and by Geography (Egypt, Kenya, South Africa, and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Africa Feed Pigments Market Trends and Insights

Rising Poultry Feed Demand and Premium Egg Color Requirements

The Africa feed pigments market is witnessing growing demand driven by the expansion of commercial poultry production, particularly in South Africa. Poultry is the largest contributor to South Africa's agricultural sector and a major consumer of compound feed. According to the United States Department of Agriculture, South Africa's chicken meat production is forecasted to reach 1.68 million tons in 2026, up from an estimated 1.64 million tons in 2025, supported by industry growth and improved feed economics. With the increase in poultry production, the demand for specialized feed additives, such as carotenoid pigments, is also rising. Egg producers are increasingly incorporating pigments to ensure consistent yolk coloration that meets retail and branded egg program standards. As yolk color significantly influences consumer purchasing decisions, feed pigments have become a critical component of layer feed formulations, driving their adoption across the poultry feed industry and contributing to market growth in Africa.

Expansion of Commercial Feed Mills Across Africa

The establishment of large-scale commercial feed manufacturing facilities is strengthening the foundation of the Africa feed pigments market. Modern feed mills are equipped to incorporate specialty additives through precise formulation and quality-control systems. For instance, in February 2026, De Heus inaugurated a USD 23.2 million feed manufacturing plant in Athi River, Kenya, with an initial annual production capacity of 240,000 metric tons, catering to poultry, pigs, ruminants, and aquaculture sectors. These investments increase the volume of feed produced through industrial processing facilities, enhancing the potential adoption of feed pigments to improve product quality and consistency in livestock and poultry production. As commercial feed production capacity expands across Africa, pigment suppliers benefit from access to a wider customer base adhering to standardized feed manufacturing practices, thereby driving the growth of the Africa feed pigments market.

High Import Dependence for Carotenoids and Pigment Premixes

The Africa feed pigments market is constrained by its significant dependence on imported specialty feed additives, including carotenoids and pigment premixes. This reliance increases vulnerability to supply chain disruptions and higher procurement costs. A 2025 study published in the journal Ruminants highlighted the high cost and limited availability of feed additives in sub-Saharan Africa as significant obstacles to their adoption in livestock production systems. These issues are particularly critical for feed pigments, which are predominantly sourced through international supply chains and require additional logistics and distribution efforts. Consequently, feed manufacturers may reduce pigment inclusion in feed formulations during periods of cost pressure, limiting market penetration and constraining the growth of the Africa feed pigments market.

Other drivers and restraints analyzed in the detailed report include:

- Aquaculture Scale-Up in Egypt, Nigeria, and East Africa

- Shift Toward Natural Pigments in Branded Poultry Products

- Cost-Sensitive Poultry Economics Limit Pigment Inclusion Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Africa feed pigment market share for curcumin and spirulina accounted for the largest 51.4% in 2025. Curcumin and spirulina maintain their leading position due to their combined pigmentation benefits and functional nutritional attributes, which appeal to commercial livestock and aquaculture producers. Their usage aligns with the increasing preference for natural feed ingredients that enhance animal performance while providing color enhancement. This dual-purpose value proposition drives adoption across various species and sustains demand for naturally sourced pigment solutions.

The Africa feed pigment market size for carotenoids is projected to grow at the fastest CAGR of 4.0% from 2026 to 2031. This growth is primarily attributed to their increasing application in aquaculture and poultry feed, where coloration is a critical quality factor for fish flesh, shrimp, egg yolks, and poultry skin. Additionally, carotenoids offer antioxidant benefits that promote animal health and productivity. The expansion of commercial feed production and the rising demand for premium-quality animal protein products are further driving the inclusion of carotenoid-based additives. These factors collectively support strong long-term growth prospects for this segment.

Complete Report Scope:

- By Sub-Additive

- Carotenoids

- Curcumin and Spirulina

- By Animal Type

- Aquaculture

- Fish

- Shrimp

- Other Aquaculture Species

- Poultry

- Broiler

- Layer

- Other Poultry Birds

- Ruminants

- Beef Cattle

- Dairy Cattle

- Other Ruminants

- Swine

- Other Animals

- Aquaculture

- By Geography

- Egypt

- Kenya

- South Africa

- Rest of Africa

List of Companies Covered in this Report:

- BASF SE

- dsm-firmenich AG

- Kemin Industries, Inc.

- EW Nutrition GmbH (EW Group)

- Nutreco N.V.

- Adisseo (China National Bluestar (Group) Co., Ltd.)

- Kalsec, Inc.

- Synthite Industries Private Limited

- Divi's Laboratories Limited

- ROHA Dyechem Private Limited

- Industrias Vepinsa, S.A. de C.V.

- Innov Ad NV/SA (PAI Partners)

- Bioergex S.A.

- Behn Meyer Holding AG

- Phytobiotics Futterzusatzstoffe GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Egypt

- 4.3.2 Kenya

- 4.3.3 South Africa

- 4.3.4 Rest of Africa

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Rising poultry feed demand and premium egg color requirements

- 4.5.2 Expansion of commercial feed mills across Africa

- 4.5.3 Aquaculture scale-up in Egypt, Nigeria, and East Africa

- 4.5.4 Shift toward natural pigments in branded poultry products

- 4.5.5 Modern retail and foodservice color consistency requirements

- 4.5.6 Tax and VAT relief on specialized feed inputs in select markets

- 4.6 Market Restraints

- 4.6.1 High import dependence for carotenoids and pigment premixes

- 4.6.2 Cost-sensitive poultry economics limit pigment inclusion rates

- 4.6.3 Foreign exchange shortages delay additive procurement

- 4.6.4 Heat and storage instability in fragmented logistics networks

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Sub-Additive

- 5.1.1 Carotenoids

- 5.1.2 Curcumin and Spirulina

- 5.2 By Animal Type

- 5.2.1 Aquaculture

- 5.2.1.1 Fish

- 5.2.1.2 Shrimp

- 5.2.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 Broiler

- 5.2.2.2 Layer

- 5.2.2.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 Beef Cattle

- 5.2.3.2 Dairy Cattle

- 5.2.3.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 By Geography

- 5.3.1 Egypt

- 5.3.2 Kenya

- 5.3.3 South Africa

- 5.3.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 dsm-firmenich AG

- 6.4.3 Kemin Industries, Inc.

- 6.4.4 EW Nutrition GmbH (EW Group)

- 6.4.5 Nutreco N.V.

- 6.4.6 Adisseo (China National Bluestar (Group) Co., Ltd.)

- 6.4.7 Kalsec, Inc.

- 6.4.8 Synthite Industries Private Limited

- 6.4.9 Divi's Laboratories Limited

- 6.4.10 ROHA Dyechem Private Limited

- 6.4.11 Industrias Vepinsa, S.A. de C.V.

- 6.4.12 Innov Ad NV/SA (PAI Partners)

- 6.4.13 Bioergex S.A.

- 6.4.14 Behn Meyer Holding AG

- 6.4.15 Phytobiotics Futterzusatzstoffe GmbH

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

飼料著色劑市場:依形態、原料、目標動物、顏色類別和應用分類-2026-2032年全球市場預測

飼料著色劑市場:依形態、原料、目標動物、顏色類別和應用分類-2026-2032年全球市場預測 中東飼料色素:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

中東飼料色素:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 全球飼料著色劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球飼料著色劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 飼料色素市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、類胡蘿蔔素來源、牲畜、地區和競爭情況細分,2020-2030 年

飼料色素市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、類胡蘿蔔素來源、牲畜、地區和競爭情況細分,2020-2030 年 2032 年飼料色素市場預測:按產品類型、來源、牲畜、應用和地區進行的全球分析飼料色素市場(按類型、產地、牲畜和地區劃分),2024 年至 2031 年

2032 年飼料色素市場預測:按產品類型、來源、牲畜、應用和地區進行的全球分析飼料色素市場(按類型、產地、牲畜和地區劃分),2024 年至 2031 年 飼料顏料市場、機會、成長動力、產業趨勢分析與預測,2024-2032

飼料顏料市場、機會、成長動力、產業趨勢分析與預測,2024-2032