|

市場調查報告書

商品編碼

2073323

歐洲SPC(石塑複合材料)地板:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031年)Europe Stone Plastic Composite (SPC) Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

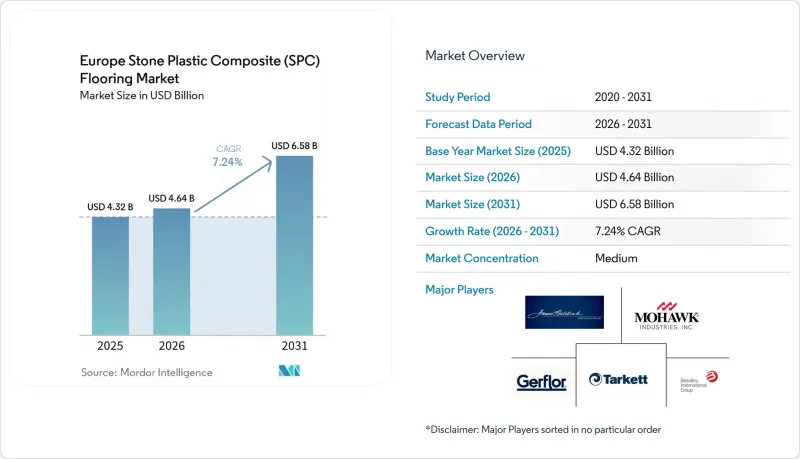

據 Mordor Intelligence 稱,歐洲 SPC(石塑複合)地板市場預計將從 2025 年的 43.2 億美元成長到 2026 年的 46.4 億美元,到 2031 年達到 65.8 億美元,預計 2026 年至 2031 年的複合成長率為 7.24%。

本報告按產品類型(SPC地磚、SPC板材)、產品厚度(4.0–5.0毫米、5.1–6.0毫米、6.1–6.5毫米、6.5毫米及以上)、最終用戶(住宅、商業)、配銷通路(B2C/零售、B2B/承包商)和地區(英國、德國、法國國家/地區進行歐洲國家/歐洲國家/歐洲國家/地區。市場預測以美元計價。

歐洲SPC(石塑複合材料)地板市場的趨勢與洞察

對建築能源性能指令 (EPBD) 的修訂和維修熱潮,以及對快速移動的地板材料的需求(這些材料可以最大限度地減少對施工的影響)。

歐盟建築能源性能指令 (EPBD) 的修正案要求成員國將更新的能源性能法規納入其國家立法,並對新建築進行生命週期評估。這凸顯了維修工程中兼具快速施工、碳效率和最小營運影響的材料的重要性。 SPC 的剛性礦物芯材可直接安裝在許多現有基層上,使承包商能夠縮短在必須保持營運的已入住建築物和公共設施中的施工時間。 2024 年,SPC 在法國的銷售量達到 1,390 萬平方米,連續第二年超過德國,這得益於公共工程和消費者偏好與快速施工解決方案的需求相一致。歐洲製造業的資本投資也在推動這一趨勢,例如 Unilin 公司在 2025 年的投資,旨在加速生產針對維修應用情境的剛性規格和表面客製化產品。在北歐市場,政策與產品選擇之間的關聯性日益增強,丹麥和挪威在 2024 年的 SPC銷售量均超過 100 萬平方米,這得益於嚴格的公共採購標準推動的強勁成長。因此,隨著政府機構和建築業主優先考慮能夠以最小的營運干擾進行安裝的認證產品,歐洲SPC地板市場的預算和規格正在趨於一致。

SPC 在 MMF 市場的佔有率正在擴大,並且正在向嚴格的磁芯規格轉變。

在歐洲多層模組化地板(MMF)市場,SPC的市佔率從2023年的65%成長到2024年的75%。這主要歸功於規範制定者在重視木紋和石紋圖案多樣性的同時,也更加重視尺寸穩定性。這一市場趨勢的轉變與LVT(豪華乙烯基複合地板)和EPC(工程塑膠複合地板)的點擊率(CTR)下降有關,因為買家更關注能夠抵抗濕度波動和高人流量的剛性芯材。在義大利和波蘭等市場,聚合物產品的銷售量在2024年顯著成長。這主要得益於消費者和公共部門專案在維修工程中對防水耐刮擦表面的需求。 2025年3月,MMFA發布了SPC的環境產品聲明(EPD),使成員公司能夠以標準化的方式向公共採購機構展示其環境績效,從而支持競標中需要提供檢驗的生命週期數據的合規性和文件記錄。 2024年西班牙的復甦趨勢在酒店業和綜合用途項目中尤為明顯,這些項目傾向於採用硬芯瓷磚外牆,優先考慮提高客房周轉率和在高人流量區域進行統一維護。這種選擇趨勢促使市場持續轉向SPC規格,儘管新建專案週期放緩,但仍支撐了歐洲SPC地板市場的銷售量成長。

與含 PFAS 面漆重組相關的風險

歐盟REACH法規對PFAS的限制為高性能表面處理中使用的塗料和添加劑帶來了不確定性,促使供應商加快替代化學品的檢驗。許多品牌都在強調低排放、高耐久性的塗層,這些塗層無需依賴有問題的添加劑即可滿足嚴苛使用條件的標準。隨著歐洲化學品管理局(ECHA)PFAS提案的推進,這一趨勢仍在持續。公共專案的採購標準通常要求提供文件和第三方測試,這促使企業確保塗層系統符合預期法規。這意味著供應商可能需要結合EN 13329標準進行磨損測試和排放測量,以維持規格,這可能會增加產品開發的時間和成本。隨著各品牌將其產品線過渡到不含PFAS的產品,過渡期可能會影響歐洲SPC地板市場高階產品的上市計劃和產品組合。

細分市場分析

2025年,SPC板材佔據了歐洲SPC地板市場69.50%的佔有率。這反映了消費者對木紋外觀的偏好,以及承包商在翻新工程中對快速浮動安裝的需求。 SPC地板的優勢在於,它能夠彌合DIY市場和專業通路之間的差距,因為它使用相同的芯材尺寸和耐磨層。這簡化了庫存管理,並縮短了居住在場時的現場安裝時間。卡扣式結構和整合式底層有助於降低噪音傳播,這在多用戶住宅和頂層整修專案中仍然是一個重要的考慮因素。歐洲SPC地板市場也重視那些將堅固的耐磨層與暫存器壓紋結合的產品系列,以增強生活空間和零售區域的真實感。快速安裝、美觀以及易於維護等優勢的結合,使得板材成為住宅翻新的首選,也是小規模商業項目的必備之選。

預計到2031年,SPC地磚的複合年成長率將達到7.40%,這主要得益於市場對大尺寸石材設計和防滑飾面的青睞,這些特性有助於酒店、醫療保健和綜合用途設施的翻新改造,從而確保設施的運作。在歐洲SPC地板材料市場,隨著針對公共項目和飯店客房最佳化尺寸、厚度和飾面的產品推出,地磚規格預計將進一步擴大。在方形房間和開放區域,地磚鋪設可以減少廢棄物;而在走廊和大廳等經常使用手推車和擔架的區域,採用粘合劑進行安裝可以提高地磚對點荷載的抵抗力。面向南歐市場的新產品系列,例如為希臘推出的Elegance Rigid 55,展示了各品牌如何根據清晰的性能評估,將礦物芯地磚定位為適用於高荷載住宅和中等荷載商業應用的地板。隨著認證材料和可預測的維護在公共採購中變得越來越重要,瓷磚設計有望在歐洲 SPC 地板市場穩步擴大其市場佔有率,尤其是在可以利用石材等材料的美觀統一性和優異的清潔性的項目中。

預計到2025年,厚度在5.1-6.0毫米之間的地板將佔據33.60%的市場佔有率,憑藉其在成本、重量和日常使用性能方面的平衡,該厚度範圍將支撐該品類的核心銷售量。此厚度範圍適用於中檔住宅和輕量商業環境,透過浮動安裝和整合式襯墊的組合,可輕鬆實現舒適性和隔音效果。該範圍內的許多產品都具有無甲醛和低揮發性等特性,並且通常獲得23級或31級認證,從而擴大了其適用的房間範圍。市場上的一個典型例子是,一款經濟實惠的硬芯地板產品系列,憑藉其便捷的卡扣式安裝、成本績效和與標準地暖系統的兼容性,深受現代公寓的青睞。基於此優勢,歐洲SPC地板市場在專業零售和專業客戶中均保持著穩定的銷售記錄。

隨著豪華住宅和高階商業房地產的規範負責人對地板的耐用性和隔音性能提出更高的要求,厚度超過 6.5 毫米的產品預計到 2031 年將以 7.85% 的複合年成長率成長。隨著專案優先考慮提高隔音性能和抗滾動荷載衝擊能力,歐洲 SPC 地板市場中此類較厚規格的市場規模將進一步擴大。在零售市場,芯材密度的提高和整合隔熱材料的應用表明,即使在高人流量場所,也能在滿足 23 級和 34 級使用等級要求的同時,保持卡扣式安裝的便捷性。法國的 EPR 生態調節框架進一步鼓勵設計能夠承受拆卸和重新安裝而不損壞鎖扣的地板,進一步證明了在圓形地板中引入堅固芯材的必要性。在整個預測期內,在那些優先考慮卓越聲學性能和耐用性而非每平方公尺成本的場所,較厚規格地板的市場滲透率將持續成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 建築能源性能指令 (EPBD) 的修訂和翻新浪潮正在加速住宅和公共建築的維修(導致對安裝快速且施工影響最小的地板材料的需求增加)。

- 隨著SPC在多層模組化地板(MMF)市場的佔有率不斷擴大,產品規格正朝著剛性芯材設計轉變。

- 低 VOC 和鄰苯二甲酸酯法規正在推動不含鄰苯二甲酸酯的硬質 LVT/SPC 的採用。

- 品牌和歐盟的循環經濟計畫(VinylPlus、歐盟生態標籤/CPR/ESPR)評估再生材料的使用和可追溯性。

- REACH 對二異氰酸酯的培訓正在促使承包商從黏合系統轉向卡扣式剛性芯材系統。

- 一個被忽視的發展:法國針對 PMCB 的 EPR 生態調節(獎勵和懲罰)正在鼓勵可回收、可移除和可收集的 SPC。

- 市場限制因素

- 廣泛的 PFAS 法規可能會影響面漆和添加劑,這可能會增加配方變更的風險。

- 建設產業放緩以及物流和原料成本的波動給需求和利潤率帶來了壓力。

- 法國生產者責任制 (EPR) 對優質混凝土自行車 (PMCB) 的環境收費增加,導致製造商和進口商的合規成本上升。

- 除了歐盟防火安全分類(Bfl-s1/s1 煙霧)之外,隔音層的引入增加了測試項目的數量,獲得 CE 標誌的成本也隨之上升。

- 產業價值鏈分析

- 波特五力分析

- 洞察最新產業趨勢與創新

- 洞察近期產業趨勢(新產品發布、策略性舉措、投資、合作、合資、業務擴張、併購等)

第5章 市場規模與成長預測

- 依產品類型

- SPC磁磚

- SPC板材

- 產品厚度(依類別)

- 4.0~5.0 mm

- 5.1~6.0 mm

- 6.1~6.5 mm

- 6.5毫米或以上

- 透過安裝方法

- 自黏式

- 黏牢

- 互鎖/卡扣

- 其他

- 最終用戶

- 住宅

- 商業

- 透過分銷管道

- B2C/零售

- 家居建材商店

- 地板材料專賣店

- 線上

- 當地金屬製品(非正規市場)

- 其他分銷管道

- B2B/承包商/建築公司

- B2C/零售

- 按地區

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟

- 北歐的

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mohawk Industries(Unilin/Quick-Step;IVC/Moduleo)

- Tarkett

- Gerflor

- Beaulieu International Group(BerryAlloc)

- James Halstead plc(Polyflor)

- Karndean Designflooring

- CFL Flooring(FirmFit, NovoCore)

- Kahrs Group

- Kronospan

- Parador

- Decora SA(Arbiton, Afirmax)

- Amtico(Mannington)

- COREtec(USFloors Europe/Shaw)

- Moduleo(Unilin Flooring)

- Quick-Step(Unilin/Mohawk)

- BerryAlloc(Beaulieu International Group)

- Polyflor(James Halstead)

- Windmoller(wineo)

- Novalis International

- PROJECT FLOORS GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe stone plastic composite flooring market size is expected to increase from USD 4.32 billion in 2025 to USD 4.64 billion in 2026 and reach USD 6.58 billion by 2031, growing at a CAGR of 7.24% over 2026-2031.

This report is Segmented by Product Type (SPC Tiles, SPC Planks), Product Thickness (4. 0-5. 0 Mm, 5. 1-6. 0 Mm, 6. 1-6. 5 Mm, Above 6. 5 Mm), End User (Residential, Commercial), Distribution Channel (B2C/Retail, B2B/Contractors), and Geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Stone Plastic Composite (SPC) Flooring Market Trends and Insights

Energy Performance of Buildings Directive (EPDB) Recast and Renovation Wave, Fast Low-Disruption Flooring Demand

The EPBD recast requires member states to transpose updated energy performance rules and to adopt whole-life-cycle assessments for new buildings, which underscores the importance of materials that combine speed, carbon efficiency, and low operational disruption in retrofit work. SPC's rigid mineral core enables direct installation over many existing substrates, helping contractors compress schedules in occupied buildings and public facilities that must remain open. SPC volumes in France reached 13.9 million m2 in 2024, surpassing Germany for a second year as public programs and consumer preferences aligned with quick install solutions. Capital deployment within European manufacturing reinforces this direction, including Unilin's 2025 investment to accelerate production and surface customization for rigid formats that target renovation use cases. Nordic markets reinforce the connection between policy and product choice, with Denmark and Norway each exceeding 1 million m2 of SPC in 2024 alongside strong growth from a base of demanding public procurement standards. These conditions collectively channel budget and specifications toward the European SPC flooring market as agencies and building owners prioritize certified products that can be installed with minimal disruption.

SPC Share Gains Within MMF, Rigid Core Specification Shift

Within Europe's multilayer modular flooring (MMF) ecosystem, SPC expanded its share to 75% of the MMF category in 2024, up from 65% in 2023, as specifiers favored dimensional stability alongside wood- and stone-look versatility. The category shift correlated with declines in LVT click-through rate (CTR) and EPC as buyers converged on rigid cores that better withstand moisture variation and heavy traffic. Markets such as Italy and Poland posted strong 2024 increases in polymer products, reflecting consumer and institutional projects that prefer waterproof, scratch-resistant surfaces in refurbishments. The publication of an SPC EPD by MMFA in March 2025 provides members with a standardized way to communicate environmental performance to public buyers, supporting bid compliance and documentation in tenders that require verified life-cycle data. Spain's 2024 rebound highlighted hospitality and mixed-use projects that favor rigid-core tile looks for faster room turns and coordinated maintenance in high-traffic spaces. This set of choices continues to move specifications toward SPC, supporting volume growth in the European SPC flooring market even as new-build cycles soften.

PFAS-Related Topcoat Reformulation Risks

The EU REACH PFAS restriction creates uncertainty for coatings and auxiliaries used in high-performance surface treatments, prompting suppliers to validate alternative chemistries early. Many brands have highlighted low-emission, durable finishes that meet intensive-use standards without relying on problematic additives, and this trend continues as the ECHA PFAS proposal evolves. Procurement criteria in public projects typically reward documentation and third-party testing, incentivizing companies to align coating systems with anticipated restrictions. This can add time and cost to product development as suppliers test EN 13329 wear testing alongside emissions outcomes to maintain specifications. As brands move their ranges toward PFAS-free products, the transition period may shift launch calendars and assortment decisions for premium lines in the European SPC flooring market.

Other drivers and restraints analyzed in the detailed report include:

- Phthalate Free Rigid LVT/SPC, VOC Rules Speed Substitution

- EU Circularity Programs, EPR, and Ecolabels Accelerate Recycled Content Use

- Construction Slowdown and Raw Material Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SPC planks held 69.50% of Europe's SPC flooring market share in 2025, reflecting consumer preference for wood look visuals and installers' need for fast, floating systems in renovation projects. The European SPC flooring market benefits from this format's ability to bridge the DIY and professional channels by using the same core sizes and wear layers, simplifying inventory and shortening installation time on occupied sites. Click profiles and integrated underlays help reduce noise transmission, which remains important in multi-family buildings and top-floor conversions. The European SPC flooring market also sees value in product lines that pair robust wear layers with embossed-in-register textures to improve realism in living spaces and retail zones. This combination of speed, aesthetics, and day-two maintenance advantages makes planks the default choice in residential upgrades and a mainstay in light commercial programs.

SPC tiles are projected to grow at a 7.40% CAGR to 2031 as hospitality, healthcare, and mixed-use refurbishments prioritize large-format stone looks and slip-resistant finishes that maintain uptime. The European SPC flooring market size for tile formats is expected to expand alongside region-specific launches that tailor formats, thicknesses, and finishes for public projects and hotel rooms. Tile layouts can reduce waste in square rooms and open areas, and glue-down installation in corridors or lobbies can enhance point load resilience where trolleys or gurneys are common. New assortments for Southern Europe, including Elegance Rigid 55, introduced for Greece, show how brands position mineral core tiles for heavy residential and moderate commercial applications with clear performance ratings. As public procurement emphasizes certified materials and predictable maintenance, tile designs will steadily capture a larger slice of the European SPC flooring market in projects that benefit from stone aesthetic continuity and robust cleanability.

The 5.1-6.0 mm band captured a 33.60% share in 2025, anchoring the volume center of the category by balancing cost, weight, and performance for everyday use. This range serves mid-tier residential and light commercial environments where floating installation and integrated underlay offer a straightforward path to comfort and sound control. Company assortments in this zone often highlight formaldehyde-free and low-emission claims, as well as Class 23 or 31 ratings that broaden placement options across rooms. Examples on the market include budget-oriented rigid core lines that promote click ease, durability, and compatibility with standard underfloor heating systems for modern apartments. The European SPC flooring market relies on this sweet spot to deliver consistent throughput across both specialty retail and trade accounts.

Formats above 6.5 mm are projected to grow at a 7.85% CAGR through 2031 as specifiers in luxury residential and premium commercial segments seek greater underfoot solidity and improved impact sound performance. The European SPC flooring market size for these thicker profiles will scale with projects that emphasize acoustic upgrades and dent resistance under rolling loads. Retail offerings demonstrate how added core density and integrated insulation help meet Class 23 and 34 use ratings while preserving click install convenience in intensive spaces. France's EPR eco-modulation framework further favors designs that withstand disassembly and reinstallation without damage to locking profiles, thereby strengthening the case for robust cores in circular models. Over the forecast, thicker formats will continue to gain penetration in rooms where premium acoustics and durability carry more weight than cost per square meter.

Complete Report Scope:

- By Product Type

- SPC Tiles

- SPC Planks

- By Product Thickness

- 4.0-5.0 mm

- 5.1-6.0 mm

- 6.1-6.5 mm

- Above 6.5 mm

- By Installation Method

- Self-Adhesive

- Glue-Down

- Interlocking/Click-lock

- Others

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Flooring Stores

- Online

- Local Hardware Shops (unorganized market)

- Other Distribution Channels

- B2B/Contractors/Builders

- B2C/Retail

- By Geography

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX

- NORDICS

- Rest of Europe

List of Companies Covered in this Report:

- Mohawk Industries (Unilin/Quick-Step

- IVC/Moduleo)

- Tarkett

- Gerflor

- Beaulieu International Group (BerryAlloc)

- James Halstead plc (Polyflor)

- Karndean Designflooring

- CFL Flooring (FirmFit, NovoCore)

- Kahrs Group

- Kronospan

- Parador

- Decora S.A. (Arbiton, Afirmax)

- Amtico (Mannington)

- COREtec (USFloors Europe/Shaw)

- Moduleo (Unilin Flooring)

- Quick-Step (Unilin/Mohawk)

- BerryAlloc (Beaulieu International Group)

- Polyflor (James Halstead)

- Windmoller (wineo)

- Novalis International

- PROJECT FLOORS GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy Performance of Buildings Directive recast and Renovation Wave accelerate residential and public building retrofits (demand pull for fast, low-disruption flooring)

- 4.2.2 SPC's rising share within multilayer modular flooring (MMF) channels shifts specifications toward rigid core designs

- 4.2.3 Low-VOC and phthalate restrictions drive phthalate-free rigid LVT/SPC adoption

- 4.2.4 Brand and EU circularity programs (VinylPlus, EU Ecolabel/CPR/ESPR) reward recycled content and traceability

- 4.2.5 REACH diisocyanates training nudges installers from glue-down to click rigid-core systems

- 4.2.6 Under-the-radar: France PMCB EPR eco-modulation (bonuses/penalties) favors recyclable, detachable, take-back-ready SPC

- 4.3 Market Restraints

- 4.3.1 Broad PFAS restriction proposals could affect topcoats/auxiliaries, raising reformulation risk

- 4.3.2 Construction slowdown and logistics/raw-material cost swings pressure demand and margins

- 4.3.3 France PMCB EPR eco-contributions increase producer/importer compliance costs

- 4.3.4 EU fire classification (Bfl-s1/s1 smoke) plus acoustic layers add testing/CE-mark costs

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Industry

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD Billion)

- 5.1 By Product Type

- 5.1.1 SPC Tiles

- 5.1.2 SPC Planks

- 5.2 By Product Thickness

- 5.2.1 4.0-5.0 mm

- 5.2.2 5.1-6.0 mm

- 5.2.3 6.1-6.5 mm

- 5.2.4 Above 6.5 mm

- 5.3 By Installation Method

- 5.3.1 Self-Adhesive

- 5.3.2 Glue-Down

- 5.3.3 Interlocking/Click-lock

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C/Retail

- 5.5.1.1 Home Centers

- 5.5.1.2 Specialty Flooring Stores

- 5.5.1.3 Online

- 5.5.1.4 Local Hardware Shops (unorganized market)

- 5.5.1.5 Other Distribution Channels

- 5.5.2 B2B/Contractors/Builders

- 5.5.1 B2C/Retail

- 5.6 By Geography

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Spain

- 5.6.5 Italy

- 5.6.6 BENELUX

- 5.6.7 NORDICS

- 5.6.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Mohawk Industries (Unilin/Quick-Step; IVC/Moduleo)

- 6.4.2 Tarkett

- 6.4.3 Gerflor

- 6.4.4 Beaulieu International Group (BerryAlloc)

- 6.4.5 James Halstead plc (Polyflor)

- 6.4.6 Karndean Designflooring

- 6.4.7 CFL Flooring (FirmFit, NovoCore)

- 6.4.8 Kahrs Group

- 6.4.9 Kronospan

- 6.4.10 Parador

- 6.4.11 Decora S.A. (Arbiton, Afirmax)

- 6.4.12 Amtico (Mannington)

- 6.4.13 COREtec (USFloors Europe/Shaw)

- 6.4.14 Moduleo (Unilin Flooring)

- 6.4.15 Quick-Step (Unilin/Mohawk)

- 6.4.16 BerryAlloc (Beaulieu International Group)

- 6.4.17 Polyflor (James Halstead)

- 6.4.18 Windmoller (wineo)

- 6.4.19 Novalis International

- 6.4.20 PROJECT FLOORS GmbH

7 Market Opportunities & Future Outlook

- 7.1 Retrofit-in-a-day SPC packages: click SPC with integrated acoustic underlay and doorway transition systems to minimize downtime for EPBD-driven renovations

- 7.2 Low-embodied-carbon, PFAS-free SPC with verified EPD/DPP to win green public procurement and healthcare/education tenders

2026年全球發光二極體(LED)照明用光擴散聚碳酸酯(PC)市場報告

2026年全球發光二極體(LED)照明用光擴散聚碳酸酯(PC)市場報告 全球共擠薄膜市場分析:市場規模、佔有率、應用及預測(2018-2034)

全球共擠薄膜市場分析:市場規模、佔有率、應用及預測(2018-2034) 複合薄膜市場機會、成長要素、產業趨勢分析及2026-2035年預測

複合薄膜市場機會、成長要素、產業趨勢分析及2026-2035年預測 複合薄膜市場:2026-2032年全球市場預測(依材料、薄膜類型、製造流程、功能、厚度、銷售管道及最終用途產業分類)複合表面薄膜市場:依技術、類別、材料、厚度和應用分類-2026年至2032年全球預測按產品類型、黏合劑類型、製造流程、厚度、產品形式、應用和最終用途產業分類的穿孔離型膜市場,全球預測,2026-2032年酚醛樹脂裝飾導軌市場依產品類型、最終用途產業、應用及通路分類,全球預測(2026-2032)

複合薄膜市場:2026-2032年全球市場預測(依材料、薄膜類型、製造流程、功能、厚度、銷售管道及最終用途產業分類)複合表面薄膜市場:依技術、類別、材料、厚度和應用分類-2026年至2032年全球預測按產品類型、黏合劑類型、製造流程、厚度、產品形式、應用和最終用途產業分類的穿孔離型膜市場,全球預測,2026-2032年酚醛樹脂裝飾導軌市場依產品類型、最終用途產業、應用及通路分類,全球預測(2026-2032) 複合薄膜全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)3D真空成型穿孔薄膜市場:依材料、製造流程、厚度範圍、應用和分銷管道分類-全球預測(2026-2032年)PVC/Aclar薄膜市場按薄膜類型、阻隔等級、包裝形式、厚度範圍和應用分類-全球預測,2026-2032年

複合薄膜全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)3D真空成型穿孔薄膜市場:依材料、製造流程、厚度範圍、應用和分銷管道分類-全球預測(2026-2032年)PVC/Aclar薄膜市場按薄膜類型、阻隔等級、包裝形式、厚度範圍和應用分類-全球預測,2026-2032年