|

市場調查報告書

商品編碼

2038399

複合薄膜市場機會、成長要素、產業趨勢分析及2026-2035年預測Composite Film Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

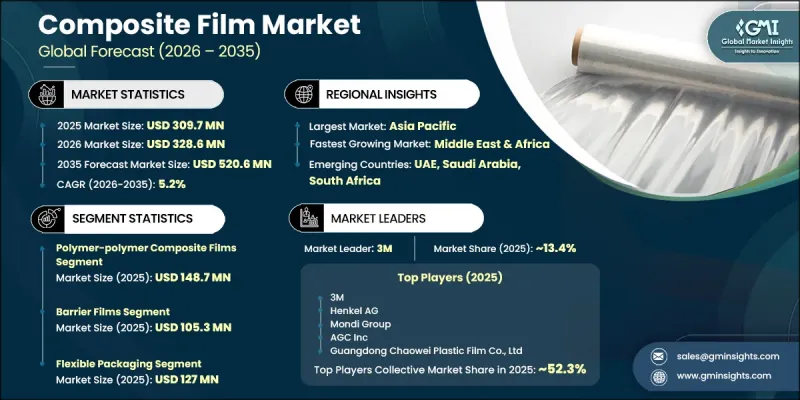

全球複合薄膜市場預計到 2025 年將達到 3.097 億美元,到 2035 年將以 5.2% 的複合年成長率成長,達到 5.206 億美元。

隨著工業界對高性能多層薄膜的需求不斷成長,市場持續穩步擴張。這些薄膜具有卓越的耐久性、防護性和功能效率,可應用於各種領域。它們因其能夠提升阻隔性能、增強強度並延長產品壽命而被廣泛應用。隨著製造商優先考慮可回收和生物基解決方案以符合環境法規和企業永續發展目標,向永續材料的轉型正成為市場發展的關鍵驅動力。材料科學和生產技術的不斷進步,使得製造更精確、擴充性且更具成本效益的複雜薄膜結構成為可能。對能夠確保產品安全、保持完整性並延長保存期限的可靠包裝解決方案的需求不斷成長,進一步推動了市場成長。此外,對具有先進耐熱性、機械防護性和特殊表面性能的薄膜的需求,也持續推動市場需求,凸顯了複合薄膜在現代製造和包裝生態系統中的重要性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 3.097億美元 |

| 預測金額 | 5.206億美元 |

| 複合年成長率 | 5.2% |

預計到2025年,阻隔薄膜市場規模將達到1.053億美元,凸顯其在許多領域的廣泛應用。儘管複合薄膜產業在不同產品類型中呈現出不同的成長趨勢,但阻隔薄膜憑藉其在提升防護性能和延長保存期限方面的顯著優勢,仍佔據主導地位。其在工業和包裝領域的廣泛應用也反映了其可靠性和卓越的功能性。同時,具有先進性能的高性能薄膜在需要高精度、高耐久性和多功能性的領域也備受關注。人們對性能最佳化和產品安全性的日益重視,不斷推動該領域的創新,促使製造商在保持生產效率和擴充性的同時,不斷提升薄膜的性能。

預計到2025年,軟包裝市場規模將達到1.27億美元,凸顯其在複合薄膜市場需求成長中的重要角色。儘管應用範圍依然廣泛,但軟包裝憑藉其提升產品保護、延長保存期限和增強終端用戶便利性的優勢,正成為市場成長的主要驅動力。尤其是在各行業日益關注效率和永續性的背景下,兼具輕量化設計和強大防護性能的包裝解決方案的需求持續成長。製造商正擴大採用先進的薄膜技術,以提高各種包裝形式的密封性、耐用性和適應性,確保即使在惡劣環境下也能保持穩定的性能。

預計2025年,北美複合薄膜市場規模將達到8,660萬美元。該地區擁有完善的製造基礎設施,有利於供應商與終端用戶產業之間的緊密合作。市場擴張的驅動力來自強調性能標準和可回收性的法律規範,這反過來又促進了先進複合薄膜解決方案的應用。新興技術領域的工業發展和對防護材料日益成長的需求持續支撐著該地區的成長。對創新的重視,以及不斷變化的永續性要求,正在塑造產品開發的方向,並增強複合薄膜在各行業的市場地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 金銀開採活動激增

- 金價上漲和投資需求

- 氰化物處理製程的技術進步

- 產業潛在風險與挑戰

- 環境問題和大規模洩漏

- 嚴格的監管限制和合規成本

- 市場機遇

- 新興國家採礦活動的擴張

- 更安全的氰化物處理技術取得進展

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計資料(HS編碼)(註:僅提供主要國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依材料類型分類,2022-2035年

- 聚合物-聚合物複合薄膜

- PE/PP組合

- PET/PA複合材料

- 多層聚烯結構

- 特殊聚合物混合物

- 聚合物-金屬複合薄膜

- 金屬化薄膜(鋁沉澱)

- 金屬箔複合膜

- 聚合物-紙複合膜

- 紙和聚合物層壓板

- 塗佈紙複合結構

- 特殊複合膜

- 可生物分解和可堆肥的複合材料

- 陶瓷增強膜

- 混合多層基底薄膜

第6章 市場估算與預測:依薄膜類型分類,2022-2035年

- 阻隔膜

- 防潮膜

- 氧氣阻隔膜

- 遮光膜

- 多層阻隔膜

- 導電膜

- 導電膜

- 導熱膜

- 黏合膜

- 壓敏黏著劑膜

- 熱活化黏合膜

- 光學薄膜

- 透明薄膜

- 反光膜

- 擴散膜

- 保護膜

- 耐刮薄膜

- 紫外線阻隔膜

- 表面保護膜

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 軟包裝

- 食品包裝

- 飲料包裝

- 藥品包裝

- 個人護理套裝

- 工業應用

- 建築用薄膜

- 隔熱膜

- 保護性包裝

- 電子與電機工程

- 展示膜

- 電路基板用薄膜

- 電容器膜

- 汽車和交通運輸

- 內膜

- 玻璃膜

- 保護膜

- 航太/國防

- 結構複合膜

- 保護塗層薄膜

- 醫療保健

- 醫療設備包裝

- 診斷膠片

- 無菌屏障膜

- 農業

- 溫室薄膜

- 多重膠片

- 青貯飼料包裹

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- 3M

- Benison

- Fengchen Group Co.,Ltd

- Guangdong Chaowei Plastic Film Co., Ltd

- Shandong Top Leader Plastic Packing Co.,Ltd

- Hysum

- Huizhou Yangrui Printing & Packaging Co.,Ltd

- Henkel AG

- Mondi Group

- AGC Inc

- Krus company

- Park Aerospace Corp

The Global Composite Film Market was valued at USD 309.7 million in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 520.6 million by 2035.

The market continues to advance steadily as industries increasingly demand high-performance, multi-layer films that offer superior durability, protection, and functional efficiency across diverse applications. These films are widely utilized due to their ability to deliver enhanced barrier performance, improved strength, and extended product lifespan. The shift toward sustainable materials is becoming a defining factor, as manufacturers prioritize recyclable and bio-based solutions to align with environmental regulations and corporate sustainability targets. Continuous developments in material science and production technologies are enabling the creation of complex film structures with higher precision, scalability, and cost efficiency. The increasing need for reliable packaging solutions that ensure product safety, maintain integrity, and extend usability further strengthens market growth. Additionally, industries requiring advanced thermal resistance, mechanical protection, and specialized surface properties are contributing to sustained demand, reinforcing the importance of composite films in modern manufacturing and packaging ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $309.7 Million |

| Forecast Value | $520.6 Million |

| CAGR | 5.2% |

The barrier films segment accounted for a USD 105.3 million in 2025, highlighting their strong adoption across multiple sectors. The composite film industry demonstrates varied growth dynamics across different product categories, with barrier films maintaining a dominant presence due to their effectiveness in enhancing protection and prolonging shelf life. Their widespread use in industrial and packaging applications reflects their reliability and functional performance. At the same time, high-performance films with advanced properties are gaining traction in sectors that demand precision, durability, and multifunctional capabilities. The growing emphasis on performance optimization and product safety continues to drive innovation within this segment, encouraging manufacturers to enhance film properties while maintaining efficiency and scalability in production processes.

The flexible packaging segment captured USD 127 million in 2025, emphasizing its critical role in driving demand within the composite film market. The application landscape remains diverse, with flexible packaging emerging as a key growth driver due to its ability to improve product protection, extend shelf life, and enhance convenience for end users. The demand for packaging solutions that combine lightweight properties with strong protective capabilities continues to rise, particularly as industries focus on efficiency and sustainability. Manufacturers are increasingly adopting advanced film technologies that enable improved sealing, durability, and adaptability across various packaging formats, ensuring consistent performance in demanding environments.

North America Composite Film Market accounted for USD 86.6 million in 2025. The region benefits from a well-established manufacturing infrastructure that supports strong collaboration between suppliers and end-use industries. Market expansion is influenced by regulatory frameworks that emphasize performance standards and recyclability, encouraging the adoption of advanced composite film solutions. Industrial development and increasing demand for protective materials in emerging technology sectors continue to support regional growth. The focus on innovation, combined with evolving sustainability requirements, is shaping product development and strengthening the market presence of composite films across various industries.

Key companies operating in the Global Composite Film Market include 3M, Mondi Group, Henkel AG, AGC Inc, Park Aerospace Corp., Benison, Hysum, Fengchen Group Co., Ltd, Shandong Top Leader Plastic Packing Co., Ltd, Guangdong Chaowei Plastic Film Co., Ltd, Huizhou Yangrui Printing & Packaging Co., Ltd, and Krus Company. Companies in the Composite Film Market are actively strengthening their position through continuous investment in research and development to enhance product performance and sustainability. Manufacturers are focusing on developing advanced multi-layer films with improved barrier properties, durability, and recyclability to meet evolving regulatory and consumer expectations. Strategic partnerships and collaborations with end-use industries are enabling companies to better align product innovation with application-specific requirements. Expansion of production capacities and adoption of advanced manufacturing technologies are improving operational efficiency and scalability. Additionally, firms are emphasizing sustainable material sourcing, circular economy initiatives, and eco-friendly product portfolios to gain a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Form

- 2.2.3 End Use Industry

- 2.2.4 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in gold & silver mining activities

- 3.2.1.2 Rising gold prices & investment demand

- 3.2.1.3 Technological advancements in cyanidation processes.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental concerns & catastrophic spill incidents

- 3.2.2.2 Stringent regulatory constraints & compliance costs.

- 3.2.3 Market opportunities

- 3.2.3.1 Growing mining activities in emerging economies

- 3.2.3.2 Advancements in safer cyanide handling technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Polymer-Polymer Composite Films

- 5.2.1 PE/PP Combinations

- 5.2.2 PET/PA Combinations

- 5.2.3 Multi-Layer Polyolefin Structures

- 5.2.4 Specialty Polymer Blends

- 5.3 Polymer-Metal Composite Films

- 5.3.1 Metallized Films (Aluminum Deposition)

- 5.3.2 Metal Foil Laminated Films

- 5.4 Polymer-Paper Composite Films

- 5.4.1 Paper-Polymer Laminates

- 5.4.2 Coated Paper Composite Structures

- 5.5 Specialty Composite Films

- 5.5.1 Biodegradable & Compostable Composites

- 5.5.2 Ceramic-Enhanced Films

- 5.5.3 Hybrid Multi-Substrate Films

Chapter 6 Market Estimates and Forecast, By Film Type, 2022 - 2035 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Barrier Films

- 6.2.1 Moisture Barrier Films

- 6.2.2 Oxygen Barrier Films

- 6.2.3 Light Barrier Films

- 6.2.4 Multi-Barrier Films

- 6.3 Conductive Films

- 6.3.1 Electrically Conductive Films

- 6.3.2 Thermally Conductive Films

- 6.4 Adhesive Films

- 6.4.1 Pressure-Sensitive Adhesive Films

- 6.4.2 Heat-Activated Adhesive Films

- 6.5 Optical Films

- 6.5.1 Transparent Films

- 6.5.2 Reflective Films

- 6.5.3 Diffusion Films

- 6.6 Protective Films

- 6.6.1 Scratch-Resistant Films

- 6.6.2 UV-Protective Films

- 6.6.3 Surface Protection Films

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Flexible Packaging

- 7.2.1 Food Packaging

- 7.2.2 Beverage Packaging

- 7.2.3 Pharmaceutical Packaging

- 7.2.4 Personal Care Packaging

- 7.3 Industrial Applications

- 7.3.1 Construction Films

- 7.3.2 Insulation Films

- 7.3.3 Protective Wrapping

- 7.4 Electronics & Electrical

- 7.4.1 Display Films

- 7.4.2 Circuit Board Films

- 7.4.3 Capacitor Films

- 7.5 Automotive & Transportation

- 7.5.1 Interior Trim Films

- 7.5.2 Glazing Films

- 7.5.3 Protective Films

- 7.6 Aerospace & Defense

- 7.6.1 Structural Composite Films

- 7.6.2 Protective Coating Films

- 7.7 Medical & Healthcare

- 7.7.1 Medical Device Packaging

- 7.7.2 Diagnostic Films

- 7.7.3 Sterile Barrier Films

- 7.8 Agriculture

- 7.8.1 Greenhouse Films

- 7.8.2 Mulch Films

- 7.8.3 Silage Wraps

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 Benison

- 9.3 Fengchen Group Co.,Ltd

- 9.4 Guangdong Chaowei Plastic Film Co., Ltd

- 9.5 Shandong Top Leader Plastic Packing Co.,Ltd

- 9.6 Hysum

- 9.7 Huizhou Yangrui Printing & Packaging Co.,Ltd

- 9.8 Henkel AG

- 9.9 Mondi Group

- 9.10 AGC Inc

- 9.11 Krus company

- 9.12 Park Aerospace Corp

複合薄膜市場-2026-2032年全球市場預測

複合薄膜市場-2026-2032年全球市場預測 複合薄膜市場規模、佔有率和成長分析:按材料、薄膜結構、應用、終端用戶產業、製造流程、分銷管道和地區分類-2026-2033年產業預測

複合薄膜市場規模、佔有率和成長分析:按材料、薄膜結構、應用、終端用戶產業、製造流程、分銷管道和地區分類-2026-2033年產業預測 歐洲SPC(石塑複合材料)地板:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031年)

歐洲SPC(石塑複合材料)地板:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031年) 2026年全球發光二極體(LED)照明用光擴散聚碳酸酯(PC)市場報告

2026年全球發光二極體(LED)照明用光擴散聚碳酸酯(PC)市場報告 全球共擠薄膜市場分析:市場規模、佔有率、應用及預測(2018-2034)複合表面薄膜市場:依技術、類別、材料、厚度和應用分類-2026年至2032年全球預測按產品類型、黏合劑類型、製造流程、厚度、產品形式、應用和最終用途產業分類的穿孔離型膜市場,全球預測,2026-2032年酚醛樹脂裝飾導軌市場依產品類型、最終用途產業、應用及通路分類,全球預測(2026-2032)

全球共擠薄膜市場分析:市場規模、佔有率、應用及預測(2018-2034)複合表面薄膜市場:依技術、類別、材料、厚度和應用分類-2026年至2032年全球預測按產品類型、黏合劑類型、製造流程、厚度、產品形式、應用和最終用途產業分類的穿孔離型膜市場,全球預測,2026-2032年酚醛樹脂裝飾導軌市場依產品類型、最終用途產業、應用及通路分類,全球預測(2026-2032) 複合薄膜全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)3D真空成型穿孔薄膜市場:依材料、製造流程、厚度範圍、應用和分銷管道分類-全球預測(2026-2032年)

複合薄膜全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)3D真空成型穿孔薄膜市場:依材料、製造流程、厚度範圍、應用和分銷管道分類-全球預測(2026-2032年)