|

市場調查報告書

商品編碼

2073320

醫療領域學習管理系統(LMS):市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Learning Management System (LMS) In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

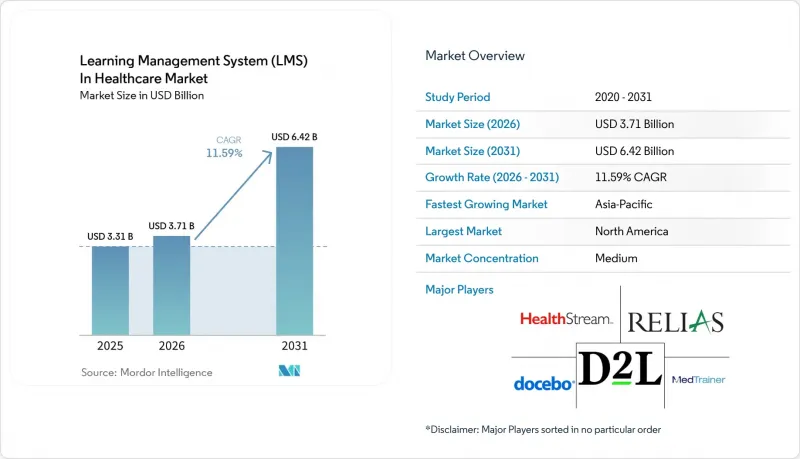

根據 Mordor Intelligence 預測,醫療保健產業的學習管理系統 (LMS) 市場規模預計將在 2025 年達到 33.1 億美元,到 2031 年達到 64.2 億美元,2026 年至 2031 年的複合年成長率為 11.59%。

本報告按組件(軟體和服務)、部署模式(雲端等)、交付模式(自主學習和遠距學習等)、應用(合規培訓、臨床和護理培訓等)、最終用戶(醫院和醫療保健系統等)以及地區進行細分。市場預測以美元計價。

全球醫療保健學習管理系統 (LMS) 市場趨勢與洞察

追蹤監管合規性和認證狀態

醫療保健產業的學習管理系統 (LMS) 市場需求持續穩定,這主要源自於醫療機構無法推遲認證相關的培訓義務,否則將增加營運風險。記錄在案的特定角色能力檢驗正逐漸融入日常人力資源管理,使 LMS 從單純的便利工具轉變為與檢查、認證續約和內部審計直接相關的合規系統。這在大規模醫療服務提供者網路中尤其重要,因為政策批准、認證簽署和再培訓記錄必須在單一的證據鏈中跨機構、部門和專業進行搜尋。因此,切換系統具有很高的成本效益比。當報告架構、稽核日誌和認證證據整合到單一平台時,採購團隊在更換供應商時會更加謹慎。此外,醫療保健產業的學習管理系統也受惠於各專業領域持續教育需求的不斷成長,因為即使人員配備水準沒有相應增加,需要記錄的培訓活動數量也會增加。

人員短缺和臨床技能的持續提升

醫療保健產業對學習管理系統的需求也源自於勞動力短缺迫使醫療機構依賴更快速、更擴充性的培訓模式。美國醫院協會 (AHA) 預測,到 2030 年,美國將出現 64,000 名護理師的缺口,並預計未來十年醫療保健產業將占美國新增就業機會的 24%。這意味著每個新增職位都會增加對新員工培訓和繼續教育的需求。美國醫療集團協會 (AMGA) 的報告顯示,2022 年至 2024 年間,基層醫療和專科診所的員工總數下降了 5% 至 7%。同時,2024 年患者就診量增加了 2.3%,這使得在繁忙的臨床環境中維持僅靠面對面授課的培訓變得越來越困難。類似的壓力也出現在輔助崗位和藥局營運中,這些崗位的高離職率導致新員工的年度培訓週期延長。根據藥劑師技術員認證委員會對 17,112 名受訪者進行的調查,預計到 2025 年,雇主主導的培訓計畫將增加 6.3%。隨著護理團隊日益多元化,角色也日益專業化,醫療保健行業的學習管理系統正受益於跨轄區、資格認證和護理路徑標準化培訓的需求,而無需依賴額外的面對面管理人員。

資料隱私和網路安全要求

醫療保健產業的學習管理系統面臨著巨大的限制,因為儲存員工培訓記錄、合規性證明和使用者層級識別碼的系統會帶來沉重的安全負擔。 2026 年發表在《應用科學》(Applied Sciences)上的一項研究預測,美國醫療保健產業的資料外洩事件將在 2024 年達到峰值,屆時將有 2.76 億筆記錄外洩。該研究還顯示,到 2025 年,該行業平均需要 279 天才能識別和控制資料外洩事件。在此背景下,買家在簽訂合約前會更加嚴格地審查加密、存取控制、稽核追蹤、測試程序和供應商文件。檢驗這些控制措施的成本可能會顯著增加小規模醫院和聯邦認證醫療中心 (FQHC) 的部署成本,使得中端市場比高階醫療保健系統對價格更加敏感。因此,如果供應商能夠集中打包安全合規性,並減輕內部網路安全資源有限的客戶的現場監控負擔,那麼醫療保健產業的學習管理系統市場將會成長得更快。

細分市場分析

該解決方案預計到2025年將佔據70.12%的構成比,成為醫療保健學習管理系統市場最大的收入來源。買家更傾向於將內容庫、工作流程自動化、報告功能和使用者管理整合到一個統一介面的整合平台,而不是將各項功能分散在多個工具中。這種配置透過單一的證據記錄即可驗證培訓完成情況、政策批准和能力認證,從而減少了審計的阻力。它還支援企業級標準化,這對於需要在醫院、診所和復健護理機構之間採用相同培訓邏輯的醫療保健系統至關重要。

服務業是成長最快的領域,預計到2031年將以12.23%的複合年成長率成長。這反映出醫療保健產業學習管理系統(LMS)的購買行為發生了明顯轉變。許多客戶已經超越了基礎平台部署階段,現在尋求外部支持,以獲得部署協助、法規更新、內容維護和多站點管理方面的協助。 MedTrainer宣布,在2025年期間,該公司為醫療產業發布了250多門新課程,實施了130多項軟體增強功能,並將其工程團隊規模擴大了25%。這表明供應商正在其軟體基礎設施之上建立持續服務層。隨著應用場景擴展到技能差距分析、人工智慧驅動的再培訓和分散式認證,服務正成為醫療保健提供者在無需組建大規模的內部LMS團隊的情況下,保持其學習環境更新的實用方法。

預計到2025年,基於雲端的部署將佔據65.23%的市場佔有率,繼續成為醫療保健學習管理系統市場的重要組成部分。其主要原因在於營運優勢。雲端基礎架構支援集中式的角色分配、內容更新和跨所有地點的報告變更,無需在每個機構進行本地系統管理。它還支援快速部署需要適應現有合規框架的新地點以及新收購的醫療機構。對於擁有大規模員工隊伍和小規模IT團隊的採購者而言,這些優勢使得雲端成為維持大規模訓練連續性的最有效模式。

雲端也是成長最快的部署方式,到2031年複合年成長率將達到12.46%,但在監管更嚴格的環境中,對混合解決方案的需求仍然顯著。歐洲健康資料空間法規進一步提升了對支援數位互通性並提供特定司法管轄區管治控制的平台的需求。對於希望在保留某些記錄本地管理的同時,利用雲端的擴充性進行內容傳送和分析的大型大學醫院和綜合醫療保健網路而言,混合部署仍然是一個至關重要的選擇。雖然本地系統仍然用於大規模安全性和資源受限的環境中,但醫療保健領域的學習管理系統市場顯然正在向託管架構轉變,這種架構既能滿足合規性要求,又能減輕維護負擔。

區域分析

到2025年,北美將佔據醫療保健學習管理系統36.58%的市場佔有率,成為最大的區域市場。美國繼續保持其作為主要國內市場的地位。這是因為美國醫療保險和醫療補助服務中心(CMS)的參與規則、認證標準和隱私義務,使得記錄培訓成為強制性營運要求,而不僅僅是可選的軟體升級。這種環境支撐了對能夠實現企業級入職培訓、能力檢驗、政策批准和持續合規管理的平台的穩定需求。在加拿大,各機構也積極採用此類平台;2025年,多倫多大學特馬蒂醫學院採用了一個基於雲端的學習者管理平台,以支持其醫學博士(MD)和研究生教育,符合「基於能力的設計」框架。墨西哥在該地區仍然是一個較小的市場,但隨著保險公司和品質期望的提高,私立醫院集團正在逐步將人才發展和能力驗證制度化。

由於歐洲擁有密集的醫院網路和不斷擴展的數位化醫療管治體系,因此它仍然是醫療保健學習管理系統領域的關鍵參與者。將於2025年通過的《歐洲健康資料空間條例》正在為跨境健康資料管理建立一個更健全的框架,這推動了對負責處理數位記錄、系統存取和合規流程的工作人員的培訓需求不斷成長。英國、德國和法國仍然是主要的需求中心,而西班牙、義大利和東歐地區則隨著記錄數位化和人力資源管治的日益系統化,在小規模的基數上實現了成長。這確保了歐洲市場仍然是一個供應商既需要區域數據洞察,又需要能夠根據不同的醫療保健系統模式調整培訓框架的市場。

亞太地區是醫療保健產業學習管理系統成長最快的市場,預計到2031年將以13.41%的複合年成長率成長。這一成長主要得益於中國和印度政府主導的醫療保健體系的擴張、東南亞私立醫院網路的蓬勃發展,以及人們日益認知到數位化培訓基礎設施對於保障醫療保健專業人員的品質至關重要。世界衛生組織(世衛組織)在2025年指出,只有30%的成員國能夠擁有成熟度達到3級或4級的完善監管體系,並推出了一個學習目錄以幫助提升負責人的技能。這反映出多個開發中國家的醫療保健系統對系統化培訓能力有廣泛的需求。 2026年發表在《醫學前沿》(Frontiers in Medicine)上的一項研究也顯示,中國醫學生對人工智慧驅動的臨床學習表現出濃厚的興趣。 45.6%的學生參與了15至30分鐘的課程,63.4%的學生更傾向於透過行動應用程式進行學習,這表明全部區域預計將採用「行動優先」的設計模式。澳洲和新加坡仍然是規模較小但發展成熟的數位醫療市場,而南美洲、中東和非洲,特別是巴西、沙烏地阿拉伯和阿拉伯聯合大公國,仍然存在早期階段的商業機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 追蹤監管合規性和認證狀態

- 人員短缺和臨床技能的持續提升

- 引入基於雲端和混合的培訓交付方式

- 人工智慧驅動的個人化學習與技能分析

- 隨著環境人工智慧和數位化工作流程的採用,出現了再培訓需求。

- 網路安全事件和病患安全事件發生後,需要進行跨站點審計。

- 市場限制因素

- 資料隱私和網路安全要求

- 與電子病歷、人力資源資訊系統和認證系統整合的複雜性。

- 快速變化的臨床方案中的內容管治瓶頸

- 輪班制護理模式降低了豐富格式訓練的完成率。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 部署模式

- 基於雲端的

- 現場

- 混合

- 透過串流媒體模式

- 自主學習與遠距學習

- 講師主導式培訓

- 混合式學習

- 透過使用

- 合規培訓

- 臨床和護理培訓

- 持續醫學教育和認證培訓

- 產品和銷售培訓

- 病人安全訓練

- 電子病歷/臨床系統培訓

- 感染控制培訓

- 網路安全與資料隱私培訓

- 遠端醫療培訓

- 員工資質和能力管理

- 最終用戶

- 醫院和醫療系統

- 診所和門診醫療保健機構

- 製藥公司

- 醫療設備製造商

- 學術醫療機構

- 長期照護機構

- 家庭醫療保健服務提供者

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 新加坡

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- HealthStream, Inc.

- Relias LLC

- MedTrainer, Inc.

- Docebo SpA

- D2L Corporation

- Absorb Software Inc.

- Cornerstone OnDemand, Inc.

- Epignosis LLC

- LearnUpon Limited

- iSpring Solutions, Inc.

- SkyPrep Inc.

- Kallidus Limited

- TOVUTI, Inc.

- Medbridge Inc.

- ACTO Technologies Inc.

- Knowledge Factor, Inc. dba Amplifire

- CareAcademy.co, Inc.

- The World Continuing Education Alliance Ltd

- Biomedical Research Alliance of New York LLC

- Thought Industries, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the learning management system (LMS) in the Healthcare Market in healthcare reached USD 3.31 billion in 2025 and is forecast to reach USD 6.42 billion by 2031, growing at a CAGR of 11.59% over 2026-2031.

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud-Based, and More), Delivery Mode (Self-Paced and Distance Learning, and More), Application (Compliance Training, Clinical and Care Training, and More), End User (Hospitals and Health Systems, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Learning Management System (LMS) In Healthcare Market Trends and Insights

Regulatory Compliance and Accreditation Tracking

The learning management system market in healthcare continues to draw steady demand from accreditation-linked training mandates that health systems cannot defer without increasing operating risk. Documented, role-specific competency validation has become embedded in routine workforce management, turning the LMS from a convenience tool into a compliance system tied to inspections, renewals, and internal audit readiness. This matters even more in large provider networks, where policy acknowledgment, competency sign-off, and retraining records need to be searchable across facilities, units, and job categories within a single evidentiary trail. The result is a strong switching-cost effect: once reporting architecture, audit logs, and accreditation evidence are aligned on a single platform, procurement teams become more cautious about vendor changes. The learning management system in the healthcare market also benefits as continuing education requirements expand across specialties, since the number of training events that must be recorded can rise even without a corresponding increase in headcount.

Workforce Shortages and Continuous Clinical Upskilling

The learning management system in the healthcare market is also being supported by staffing shortages that are forcing providers to rely on faster, more scalable training models. The American Hospital Association projected a shortfall of 64,000 nurses by 2030 and said health care is expected to account for 24% of all new U.S. jobs this decade, meaning every new role created will increase demand for onboarding and continuing education. The American Medical Group Association reported that total clinic staffing in primary care and medical specialties declined by 5% to 7% between 2022 and 2024, even as patient visits rose 2.3% in 2024, making classroom-only delivery harder to sustain in busy clinical settings. The same pressure is visible in frontline support roles, where high turnover expands the annual cycle of onboarding-linked training, and in pharmacy operations, where the Pharmacy Technician Certification Board found employer-based training programs rose 6.3% in 2025 across its survey base of 17,112 respondents. As care teams diversify and role scopes become more specialized, the learning management system in the healthcare market benefits from the need to standardize training across jurisdictions, credentials, and care pathways without relying on additional in-person administrative staff.

Data Privacy and Cybersecurity Requirements

The learning management system in the healthcare market faces a significant brake due to the security burden imposed by systems that store staff training records, compliance evidence, and user-level identifiers. A 2026 survey published in Applied Sciences noted that U.S. health care breaches peaked in 2024 with 276 million records exposed, and that incidents in the sector averaged 279 days to identify and contain in 2025. This environment heightens buyer scrutiny of encryption, access controls, audit trails, testing procedures, and vendor documentation before contracts move forward. The cost of validating these controls can materially increase deployment expenses for smaller hospitals and federally qualified health centers, making the mid-market more price-sensitive than top-tier health systems. The learning management system market in healthcare, therefore, grows faster when vendors can centrally package security compliance and reduce the burden of local oversight for customers with limited internal cyber resources.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Personalized Learning and Skills Analytics

- Cloud-Based and Hybrid Training Delivery Adoption

- Integration Complexity With EHR, HRIS, And Credentialing Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 70.12% of the 2025 component split, making them the largest revenue stream in the healthcare learning management system market. Buyers favored integrated platforms because they combine content libraries, workflow automation, reporting, and user management in a single interface, rather than spreading accountability across multiple tools. That setup reduces audit friction because training completion, policy acknowledgment, and competency sign-off can be reviewed through a single evidence trail. It also supports enterprise standardization, which is important for health systems that need the same training logic across hospitals, clinics, and post-acute settings.

Services are the faster-growing component, with a 12.23% CAGR projected through 2031, reflecting a clear shift in buyer behavior within the learning management system in the healthcare industry. Many customers have moved past basic platform deployment and now want outside help with implementation, regulatory updates, content maintenance, and multi-site administration. MedTrainer said it released more than 250 new healthcare-specific courses and more than 130 software enhancements during 2025, while also expanding its engineering team by 25%, demonstrating how vendors are building recurring service layers on top of the software base. As use cases broaden into skills gap analysis, AI retraining, and distributed credentialing, services become a practical way for providers to keep the learning environment current without hiring large internal LMS teams.

Cloud-based deployment held a 65.23% share in 2025 and remains the leading configuration in the healthcare learning management system market. The main reason is operational, because cloud infrastructure lets role-based assignments, content updates, and reporting changes move across all sites without local system administration at each facility. It also supports faster onboarding for new locations and newly acquired provider groups that need to fit into an existing compliance framework. For buyers with large workforces and lean IT teams, these benefits make cloud the most efficient model for maintaining training continuity at scale.

Cloud is also the fastest-growing deployment mode, with a 12.46% CAGR through 2031, while hybrid demand remains relevant in more tightly regulated environments. The European Health Data Space regulation strengthened the case for platforms that can support digital interoperability together with jurisdiction-aware governance controls. Hybrid deployment remains a key option for large academic medical centers and integrated delivery networks that want on-premises control for selected records while still leveraging cloud elasticity for content delivery and analytics. On-premises systems continue to be used in high-security or resource-constrained environments, but the learning management system market in healthcare is clearly moving toward hosted architectures that offer compliance parity with lower maintenance overhead.

Complete Report Scope:

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Delivery Mode

- Self-Paced and Distance Learning

- Instructor-Led Training

- Blended Learning

- By Application

- Compliance Training

- Clinical and Care Training

- CME and Certification Training

- Product and Commercial Training

- Patient Safety Training

- EHR/Clinical Systems Training

- Infection Control Training

- Cybersecurity and Data Privacy Training

- Telehealth Training

- Workforce Credentialing and Competency Management

- By End User

- Hospitals and Health Systems

- Clinics and Ambulatory Care Providers

- Pharmaceutical Companies

- Medical Device Companies

- Academic Medical Institutions

- Long-Term Care Facilities

- Home Healthcare Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 36.58% of the healthcare learning management system market share in 2025, making it the largest regional market. The United States remained the dominant national market because CMS participation rules, accreditation standards, and privacy obligations make documented training an operational requirement rather than an optional software upgrade. This environment supports a stable demand for platforms that can manage onboarding, competency validation, policy acknowledgment, and recurring compliance at enterprise scale. Canada also showed active institutional adoption, and the University of Toronto Temerty Faculty of Medicine selected a cloud-based learner management platform in 2025 to support MD and postgraduate education aligned with the Competence by Design framework. Mexico remains a smaller opportunity in the region, but private hospital groups are gradually formalizing workforce development and competency documentation as payer and quality expectations rise.

Europe remains an important part of the learning management system in the healthcare market because it combines dense hospital networks with expanding digital health governance. The European Health Data Space regulation, adopted in 2025, created a stronger framework for cross-border health data management, which adds training needs for staff who handle digital records, system access, and compliance processes. The United Kingdom, Germany, and France remain the main national demand centers, while Spain, Italy, and Eastern Europe are moving forward from a smaller base as record digitization and workforce governance become more structured. This keeps Europe positioned as a market where vendors need both regional data awareness and the ability to adapt training structures to varied health system models.

Asia-Pacific is the fastest-growing region in the learning management system market for healthcare, with a 13.41% CAGR projected through 2031. Growth is being driven by state-led health system expansion in China and India, by scaling private hospital networks across Southeast Asia, and by a broader recognition that workforce quality assurance requires digital training infrastructure. The World Health Organization said in 2025 that only 30% of member states have well-functioning regulatory systems at Maturity Levels 3 or 4, and it launched a learning catalog to help upskill regulatory workforces, reflecting a wider need for structured training capacity across several developing health systems. A 2026 study in Frontiers in Medicine also showed strong engagement with AI-enabled clinical learning among Chinese medical students, with 45.6% participating in sessions of 15 to 30 minutes and 63.4% preferring mobile app delivery, pointing to mobile-first design expectations across the region. Australia and Singapore remain smaller but advanced digital health markets, while South America, the Middle East, and Africa continue to present earlier-stage opportunities led by Brazil, Saudi Arabia, and the UAE.

- HealthStream, Inc.

- Relias LLC

- MedTrainer, Inc.

- Docebo S.p.A.

- D2L Corporation

- Absorb Software Inc.

- Cornerstone OnDemand, Inc.

- Epignosis LLC

- LearnUpon Limited

- iSpring Solutions, Inc.

- SkyPrep Inc.

- Kallidus Limited

- TOVUTI, Inc.

- Medbridge Inc.

- ACTO Technologies Inc.

- Knowledge Factor, Inc. dba Amplifire

- CareAcademy.co, Inc.

- The World Continuing Education Alliance Ltd

- Biomedical Research Alliance of New York LLC

- Thought Industries, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Compliance and Accreditation Tracking

- 4.2.2 Workforce Shortages and Continuous Clinical Upskilling

- 4.2.3 Cloud-Based and Hybrid Training Delivery Adoption

- 4.2.4 AI-Enabled Personalized Learning and Skills Analytics

- 4.2.5 Retraining Demand From Ambient AI and Digital Workflow Adoption

- 4.2.6 Cross-Site Auditability Needs After Cyber and Patient-Safety Incidents

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Requirements

- 4.3.2 Integration Complexity With EHR, HRIS, and Credentialing Systems

- 4.3.3 Content Governance Bottlenecks in Fast-Changing Clinical Protocols

- 4.3.4 Shift-Based Care Models Reduce Rich-Format Training Completion

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Delivery Mode

- 5.3.1 Self-Paced and Distance Learning

- 5.3.2 Instructor-Led Training

- 5.3.3 Blended Learning

- 5.4 By Application

- 5.4.1 Compliance Training

- 5.4.2 Clinical and Care Training

- 5.4.3 CME and Certification Training

- 5.4.4 Product and Commercial Training

- 5.4.5 Patient Safety Training

- 5.4.6 EHR/Clinical Systems Training

- 5.4.7 Infection Control Training

- 5.4.8 Cybersecurity and Data Privacy Training

- 5.4.9 Telehealth Training

- 5.4.10 Workforce Credentialing and Competency Management

- 5.5 By End User

- 5.5.1 Hospitals and Health Systems

- 5.5.2 Clinics and Ambulatory Care Providers

- 5.5.3 Pharmaceutical Companies

- 5.5.4 Medical Device Companies

- 5.5.5 Academic Medical Institutions

- 5.5.6 Long-Term Care Facilities

- 5.5.7 Home Healthcare Providers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 HealthStream, Inc.

- 6.4.2 Relias LLC

- 6.4.3 MedTrainer, Inc.

- 6.4.4 Docebo S.p.A.

- 6.4.5 D2L Corporation

- 6.4.6 Absorb Software Inc.

- 6.4.7 Cornerstone OnDemand, Inc.

- 6.4.8 Epignosis LLC

- 6.4.9 LearnUpon Limited

- 6.4.10 iSpring Solutions, Inc.

- 6.4.11 SkyPrep Inc.

- 6.4.12 Kallidus Limited

- 6.4.13 TOVUTI, Inc.

- 6.4.14 Medbridge Inc.

- 6.4.15 ACTO Technologies Inc.

- 6.4.16 Knowledge Factor, Inc. dba Amplifire

- 6.4.17 CareAcademy.co, Inc.

- 6.4.18 The World Continuing Education Alliance Ltd

- 6.4.19 Biomedical Research Alliance of New York LLC

- 6.4.20 Thought Industries, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

教育內容市場預測至2034年—按內容類型、交付方式、教育程度、學科領域、最終用戶和地區分類的全球分析數位素養提昇市場預測至2034年-按組件、部署模式、學習模式、技術、應用、最終用戶和地區分類的全球分析數位教科書和數位學習內容市場預測至2034年——按內容類型、學科領域、格式、分發管道和最終用戶分類的全球分析

教育內容市場預測至2034年—按內容類型、交付方式、教育程度、學科領域、最終用戶和地區分類的全球分析數位素養提昇市場預測至2034年-按組件、部署模式、學習模式、技術、應用、最終用戶和地區分類的全球分析數位教科書和數位學習內容市場預測至2034年——按內容類型、學科領域、格式、分發管道和最終用戶分類的全球分析 數位教育內容市場:依內容類型、交付方式、技術和最終用戶分類-2026-2032年全球市場預測

數位教育內容市場:依內容類型、交付方式、技術和最終用戶分類-2026-2032年全球市場預測 2026年全球數位教育內容市場報告

2026年全球數位教育內容市場報告 2026-2030年全球數位教育內容市場

2026-2030年全球數位教育內容市場 數位教育內容市場報告:趨勢、預測和競爭分析(至 2031 年)

數位教育內容市場報告:趨勢、預測和競爭分析(至 2031 年)