|

市場調查報告書

商品編碼

2073293

醫療保健產業薪資核算軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)Payroll Software In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

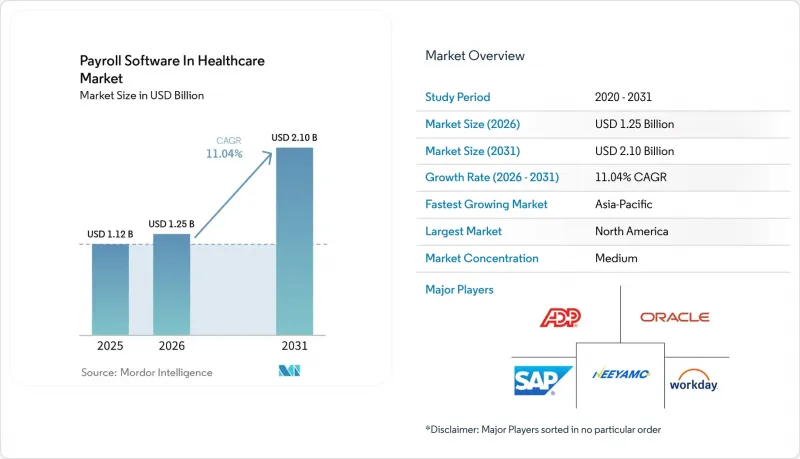

根據 Mordor Intelligence 預測,醫療保健薪資核算軟體市場規模將從 2025 年的 11.2 億美元和 2026 年的 12.5 億美元成長到 2031 年的 21 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 11.04%。

本報告按組件(軟體和服務)、應用(薪資核算、考勤管理、合規和稅務管理、福利管理及其他應用)、部署模式(雲端和本地部署)、最終用戶(醫院、長期護理和養老機構等)以及地區進行細分。市場預測以美元計價。

全球醫療保健薪資核算軟體市場趨勢與洞察

醫療保健產業在多個司法管轄區內薪資核算合規的複雜性日益增加。

明尼蘇達州和馬裡蘭州將於2026年實施的強制帶薪休假制度要求雇主代扣代繳保險費、維護個人帳簿並提交季度納稅申報表——這些任務繁重,人工操作難以完成。 SECURE Act 2.0法案新增了針對年收入超過14.5萬美元員工的虧損補繳繳款,迫使企業在年中進行稅法修改。 Symmetry Tax Engine Premium目前能夠處理超過7000個稅務管轄區的數據,延遲時間不到4毫秒,這表明人工智慧分析重疊規則的速度比人工負責人更快。 ADP在2026年的一項調查顯示,亞太地區71%的企業將因違規支付罰款,凸顯了其中巨大的財務風險。對於跨州連鎖醫院而言,審計和補繳課稅的風險進一步擠壓了本已微薄的利潤空間,使得合規自動化成為關鍵的採購標準。

醫院轉向基於雲端的薪資核算解決方案的轉變正在加速。

2025年,美國衛生與公眾服務部將薪資核算系統遷移到雲端平台,以降低維護成本並提升災害復原能力。克里斯蒂安娜醫療保健中心(ChristianaCare)在遷移後也將薪資處理時間縮短了30%。 2024年,Change Healthcare的資料外洩事件導致1.927億筆記錄曝光,引發了安全性擔憂,促使監管機構提案強制要求資料加密,並在資料外洩發生後72小時內發出通知。 2025年,Workday和銷售團隊的資料外洩事件影響了700多家機構,顯示即使是頂級供應商也存在安全漏洞。儘管發生了這些事件,雲端採用率預計仍將以14.02%的複合年成長率成長。這是因為門診手術中心和當地診所更傾向於雲端平台較低的資本負擔和持續的功能更新,而這些是本地部署系統所不具備的。

資料安全和病患隱私問題阻礙了薪資核算。

由於薪資文件包含休假資料和福利選擇,因此根據《健康保險流通與責任法案》(HIPAA),它們屬於受保護的健康資訊 (PHI)。一項針對 2025 年的提案修正案強制要求對靜態資料和傳輸中的資料進行加密、採用多因素身份驗證,並在 72 小時內通知資料外洩事件。 2025 年 Workday 和 Salesforce 的資料外洩事件引發了集體訴訟,迫使一些醫院恢復使用本地備份。 IBM 估計,醫療產業資料外洩造成的平均損失為 742 萬美元,是行業平均水平的三倍,其中包括罰款和信用監控成本。安全負責人現在要求每年進行滲透測試,併購買超過 5000 萬美元的網路保險契約,這可能會使採購流程延遲長達九個月,使小規模的雲端初創公司處於不利地位。

細分市場分析

由於亞太地區71%的醫療機構每年都面臨稅務申報罰款,醫療服務機構已開始將稅務申報外包,因此,外包服務在醫療薪資核算軟體市場中的佔有率日益成長。預計到2025年,軟體收入仍將佔總收入的66.41%,大規模綜合醫療服務網路更傾向於使用能夠大規模適應工會規定的永久許可。然而,ADP的共同僱用模式正吸引著那些沒有專門薪資核算人員的門診診所的關注,因為它轉移了預扣稅款錯誤的責任。根據《SECURE Act 2.0》規定,洛杉磯IRA的補繳繳款要求以及不斷上漲的全州帶薪假期津貼,將使2026年的申報流程更加複雜,從而導致對薪資核算外包服務的諮詢量激增。 Paychex以41億美元收購Paycor,體現了軟體和服務在同一平台下的整合趨勢。

混合服務模式正在模糊各個細分市場的界線。供應商現在將軟體訂閱與報稅服務捆綁銷售,這使得醫療保健行業薪資核算軟體的市場佔有率計算變得更加複雜。中型醫院優先考慮價格的可預測性而非配置控制,這推動了外包業務兩位數的成長。傳統的本地部署套件仍然主導著每兩週處理 5 萬份薪資單的多州系統,但即使是這些供應商也在試點提供保證違約賠償的服務擴展。在整個預測期內,即使軟體仍保持最大的絕對市場佔有率,業務收益也預計將超過授權收入。

2025年,薪資核算處理業務佔總營收的45.89%,但合規和稅務管理業務預計將以12.98%的複合年成長率成長,成為成長最快的業務。由於醫院無法承擔罰款和糾正措施所耗費的時間,因此他們願意為即時合規數據支付30-40%的溢價。 Symmetry Tax Engine Premium已在7000個司法管轄區證明了其在4毫秒以內規則處理的價值,將原本的成本中心轉變為戰略職能。 2026年Medicare醫生報銷方案中工作相對價值單位(WRVU)2.5%的變化迫使系統進行週期中期更新,這給那些將合規數據視為靜態表格而非即時流的系統帶來了壓力。

考勤管理在連接排班和薪資核算繼續發揮著至關重要的作用,生物識別掃描器和行動地理圍欄技術的應用旨在遏制詐欺行為。在福利管理方面,註冊流程和保費核對正在自動化,從而減少了薪資核算週期之外的調整。雖然薪資扣押處理和工會會費繳納仍屬於小眾領域,但它們正促使買家轉向能夠處理所有支付方式的平台。醫療保健薪資核算軟體市場的合規模組正在不斷擴展。這是因為錯誤可能導致審計、補繳課稅,甚至損害臨床醫生的聲譽,造成的損失遠遠超過軟體授權費用。能夠將合規更新按週而非按年計費的供應商將抓住這部分不斷成長的支出。

區域分析

2025年,北美繼續佔據醫療保健薪資核算軟體市場37.54%的佔有率。這是因為各州和地方的稅收系統需要專門的合規引擎。僅加州就有九種不同的意外保險率和58種縣級稅,所有這些都必須反映在每張薪資單上。 2026年聯邦醫療保險(Medicare)醫生收費標準和診所營運費用的更新要求即時調整醫生薪酬,因此夜間批量更新已不再適用。加拿大薩斯喀徹爾省成本的激增清楚地表明了轉換成本的障礙。 2024年墨西哥的社會安全改革迫使私人醫院連鎖機構遷移到整合電子申報功能的雲端薪資核算系統。

在歐洲,一般資料保護規則(GDPR) 和即將實施的歐洲健康資料空間 (EHDS) 都已生效,這兩項法規都強制要求資料儲存在區域內。英國、德國和法國的國家醫療服務體系 (NHS) 正在推進考勤管理數位化,以符合《工作時間指令》的限制。像 Zalaris 這樣的供應商正在利用其位於國內的資料中心來滿足這些要求。同時,受勞動力短缺和政府主導的數位化進程的推動,亞太地區預計到 2031 年將以 12.54% 的年成長率成長。印度的統一支付介面 (UPI) 實現了即時工資支付。日本規定了每月加班時間上限,而澳洲的單一接點薪資系統 (Single Touch 薪資核算 System) 則在每次薪資核算時將資料即時傳輸給稅務機關。

在非洲和中東,隨著沙烏地阿拉伯「2030願景」和阿拉伯聯合大公國醫療保健擴張計畫的推進,雲端基礎設施投資正在穩步成長,但合約嚴重偏向於提供阿拉伯語本地化和本地資料中心的訂單。南美洲和非洲仍處於雲端技術應用的早期階段,但巴西的「eSocial」舉措和南非對其PAYE(預扣稅)系統的現代化改造正在為未來的成長奠定基礎。這些區域特點促使供應商擴展其稅務引擎的功能範圍,並增加在地化能力,以擴大其在醫療保健行業薪資核算軟體的潛在基本客群。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 醫療產業在多個司法管轄區內薪資核算合規的複雜性日益增加。

- 醫院轉向基於雲端的薪資核算解決方案的轉變正在加速。

- 擴大採用綜合人力資源管理的方式,以降低管理成本。

- 對即時分析以最佳化人員配置的需求日益成長。

- 擴展以價值為基礎的醫療保健模式需要詳細分配人事費用

- 醫療保健產業零工人員的激增,增加了對彈性薪資核算系統的需求。

- 市場限制因素

- 資料安全和病患隱私問題阻礙了薪資核算。

- 大型醫療保健系統從傳統人力資源資訊系統遷移成本高昂

- 醫療領域薪資稅專家短缺

- 不固定的輪班薪資和工會規定使得標準化變得困難。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 透過使用

- 薪資核算

- 考勤管理

- 合規與稅務管理

- 員工福利管理

- 其他用途

- 部署模式

- 雲

- 現場

- 最終用戶

- 醫院

- 診所和門診中心

- 門診及診斷中心

- 長期照護和老年護理機構

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Automatic Data Processing, Inc.

- Ceridian HCM Holding Inc.

- Paychex, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paycor HCM, Inc.

- Ultimate Kronos Group LLC

- Intuit Inc.

- SAP SE

- Oracle Corporation

- Workday, Inc.

- BambooHR LLC

- Gusto, Inc.

- Sage Group plc

- TriNet Zenefits LLC

- Patriot Software Company

- Xero Limited

- Neeyamo Inc.

- Zalaris ASA

- Deel Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the payroll software in healthcare market size is projected to expand from USD 1.12 billion in 2025 and USD 1.25 billion in 2026 to USD 2.10 billion by 2031, registering a CAGR of 11.04% between 2026 to 2031.

This report is Segmented by Component (Software, and Services), Application (Payroll Processing, Time and Attendance Tracking, Compliance and Tax Management, Benefits Administration, and Other Applications), Deployment Mode (Cloud, and On-Premises), End User (Hospitals, Long-term Care and Aged Care Facilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Payroll Software In Healthcare Market Trends and Insights

Rising Complexity of Multi-Jurisdiction Healthcare Payroll Compliance

Paid-leave mandates in Minnesota and Maryland that took effect in 2026 oblige employers to withhold premiums, maintain separate accrual ledgers, and file quarterly returns, tasks that manual workflows cannot scale. The SECURE Act 2.0 adds Roth catch-up deferrals for employees earning above USD 145,000, forcing mid-year code changes. Symmetry Tax Engine Premium now processes more than 7,000 tax jurisdictions with sub-four-millisecond latency, proving that artificial intelligence can parse overlapping rules faster than human auditors. A 2026 ADP survey showed 71% of Asia-Pacific organizations paid non-compliance penalties, underlining the financial stakes. For multistate hospital chains, the risk of audits and back-tax assessments erodes already-tight margins, making compliance automation a primary purchasing criterion.

Accelerating Shift Toward Cloud-Based Payroll Solutions in Hospitals

The U.S. Department of Health and Human Services migrated payroll to a cloud platform in 2025, citing lower maintenance overhead and better disaster recovery. ChristianaCare cut payroll-processing time by 30% after its own migration. Security expectations rose after the 2024 Change Healthcare breach, which compromised 192.7 million records, prompting regulators to propose mandatory encryption and 72-hour breach notification windows. Workday and Salesforce experienced a 2025 breach that affected more than 700 organizations, demonstrating that even tier-one vendors remain vulnerable. Despite these incidents, cloud deployments are set to grow at a 14.02% CAGR because ambulatory surgery centers and rural clinics prefer capital-light models and continuous feature updates that on-premises systems lack.

Data Security and Patient Privacy Concerns Hindering Cloud Payroll Adoption

Because payroll files contain leave data and benefit elections, they qualify as protected health information under HIPAA. Proposed 2025 amendments require encryption at rest and in transit, multi-factor authentication, and breach notification in under 72 hours. The 2025 breach at Workday and Salesforce triggered class-action lawsuits and forced some hospitals to revert to on-premises backups. IBM pegged the average healthcare breach at USD 7.42 million, triple the cross-industry mean, due to fines and credit-monitoring expenses. Security officers now demand annual penetration tests and cyber-insurance policies above USD 50 million, delaying procurements by up to nine months and putting small cloud startups at a disadvantage.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Integrated Workforce Management to Reduce Administrative Costs

- Growing Demand for Real-Time Analytics for Staffing Optimization

- High Switching Costs From Legacy HRIS in Large Health Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services accounted for a rising slice of the payroll software in healthcare market as health systems outsource tax filing to avoid penalties that 71% of Asia-Pacific organizations report each year. Software still generated 66.41% of 2025 revenue because large integrated delivery networks favor perpetual licenses that can handle union rules at scale. However, ADP's co-employment model transfers liability for withholding errors, attracting ambulatory centers that lack dedicated payroll staff. The SECURE Act 2.0 Roth catch-up mandate and new state paid-leave premiums increased filing complexity in 2026, spurring a surge in managed-payroll inquiries. Paychex's USD 4.1 billion purchase of Paycor underscores the convergence of software and services under one roof.

Hybrid offerings blur segment boundaries. Vendors now sell software subscriptions bundled with tax-filing services, complicating the attribution of payroll software in healthcare market share. Mid-sized hospitals prefer predictable pricing over configuration control, driving double-digit growth in outsourcing. Legacy on-premises suites still dominate among multistate systems processing 50,000 paychecks every two weeks, but even these providers are piloting service extensions that guarantee penalty reimbursement. Over the forecast horizon, service revenues are set to outpace license revenues even if software retains the largest absolute pool.

While payroll processing captured 45.89% of 2025 revenue, compliance and tax management is on course for the fastest expansion at a 12.98% CAGR. Hospitals cannot afford fines or remediation time, so they pay a 30% to 40% premium for real-time compliance feeds. Symmetry Tax Engine Premium demonstrates the value of sub-four-millisecond rule processing across 7,000 jurisdictions, turning an erstwhile cost center into a strategic feature. The 2026 Medicare Physician Fee Schedule's 2.5% work-relative-value-unit change forced mid-cycle updates, stressing systems that treat compliance as static tables instead of streaming feeds.

Time and attendance remains the connective tissue between scheduling and payroll, adding biometric scanners and mobile geofencing to curb buddy punching. Benefits administration automates enrollment and premium reconciliation, reducing off-cycle adjustments. Garnishment processing and union-dues remittance remain niche, yet they push buyers toward platforms that handle the full payments spectrum. The payroll software in healthcare market size for compliance modules grows because errors escalate to audits, back taxes, and damaged credit for clinicians, dwarfing software fees. Vendors able to monetize compliance updates weekly rather than annually will capture the incremental spend.

Complete Report Scope:

- By Component

- Software

- Services

- By Application

- Payroll Processing

- Time and Attendance Tracking

- Compliance and Tax Management

- Benefits Administration

- Other Applications

- By Deployment Mode

- Cloud

- On-Premises

- By End User

- Hospitals

- Clinics and Outpatient Centers

- Ambulatory and Diagnostic Centers

- Long-Term Care and Aged Care Facilities

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America retained 37.54% of payroll software in healthcare market revenue in 2025 because state and local tax regimes demand specialized compliance engines. California alone posts nine disability-insurance rates and 58 county levies, all of which must be reflected in each paycheck. The 2026 Medicare Physician Fee Schedule and practice-expense updates forced real-time physician-compensation recalibration, revealing that nightly batch updates no longer suffice. Canada's Saskatchewan cost blowout illustrates the switching-cost hurdle. Mexico's 2024 social-security reform pushed private hospital chains toward cloud payroll that integrates electronic filing.

Europe is governed by the General Data Protection Regulation and the forthcoming European Health Data Space, both of which compel in-region data residency. National health services in the United Kingdom, Germany, and France digitalize timekeeping to enforce Working Time Directive limits. Vendors such as Zalaris use sovereign data centers to navigate these requirements. Meanwhile, Asia-Pacific is forecast to grow at 12.54% through 2031, buoyed by workforce shortages and government digitalization. India's Unified Payments Interface enables instant salary disbursement; Japan enforces monthly overtime caps, and Australia's single-touch payroll regime submits every run to the tax office in real time.

The Middle East and Africa invest in cloud infrastructure under Saudi Vision 2030 and United Arab Emirates health-care expansion plans, though contract awards skew to vendors offering Arabic localization and local data centers. South America and Africa remain earlier in the adoption curve, but Brazil's eSocial initiative and South Africa's PAYE modernization lay groundwork for future growth. Together, these regional nuances encourage vendors to broaden tax-engine coverage while adding localization features that extend the payroll software in healthcare market addressable base.

- Automatic Data Processing, Inc.

- Ceridian HCM Holding Inc.

- Paychex, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paycor HCM, Inc.

- Ultimate Kronos Group LLC

- Intuit Inc.

- SAP SE

- Oracle Corporation

- Workday, Inc.

- BambooHR LLC

- Gusto, Inc.

- Sage Group plc

- TriNet Zenefits LLC

- Patriot Software Company

- Xero Limited

- Neeyamo Inc.

- Zalaris ASA

- Deel Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Complexity of Multi-Jurisdiction Healthcare Payroll Compliance

- 4.2.2 Accelerating Shift Toward Cloud-Based Payroll Solutions in Hospitals

- 4.2.3 Increasing Adoption of Integrated Workforce Management to Reduce Administrative Costs

- 4.2.4 Growing Demand for Real-Time Analytics for Staffing Optimization

- 4.2.5 Expansion of Value-Based Care Models Requiring Granular Labor Cost Allocation

- 4.2.6 Surge in Healthcare Gig Workforce Driving Need for Flexible Payroll Engines

- 4.3 Market Restraints

- 4.3.1 Data Security and Patient Privacy Concerns Hindering Cloud Payroll Adoption

- 4.3.2 High Switching Costs From Legacy HRIS in Large Health Systems

- 4.3.3 Shortage of Healthcare-Specific Payroll Tax Professionals

- 4.3.4 Fragmented Shift Differentials and Union Rules Complicating Standardization

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Application

- 5.2.1 Payroll Processing

- 5.2.2 Time and Attendance Tracking

- 5.2.3 Compliance and Tax Management

- 5.2.4 Benefits Administration

- 5.2.5 Other Applications

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-Premises

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Clinics and Outpatient Centers

- 5.4.3 Ambulatory and Diagnostic Centers

- 5.4.4 Long-Term Care and Aged Care Facilities

- 5.4.5 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 Ceridian HCM Holding Inc.

- 6.4.3 Paychex, Inc.

- 6.4.4 Paycom Software, Inc.

- 6.4.5 Paylocity Holding Corporation

- 6.4.6 Paycor HCM, Inc.

- 6.4.7 Ultimate Kronos Group LLC

- 6.4.8 Intuit Inc.

- 6.4.9 SAP SE

- 6.4.10 Oracle Corporation

- 6.4.11 Workday, Inc.

- 6.4.12 BambooHR LLC

- 6.4.13 Gusto, Inc.

- 6.4.14 Sage Group plc

- 6.4.15 TriNet Zenefits LLC

- 6.4.16 Patriot Software Company

- 6.4.17 Xero Limited

- 6.4.18 Neeyamo Inc.

- 6.4.19 Zalaris ASA

- 6.4.20 Deel Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

負責人薪酬管理軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

負責人薪酬管理軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 雲端薪資核算軟體市場報告:按組件、組織規模、產業和地區分類(2026-2034 年)

雲端薪資核算軟體市場報告:按組件、組織規模、產業和地區分類(2026-2034 年) 2026年全球人力資源與薪資軟體市場報告2026年全球雲端薪資核算軟體市場報告

2026年全球人力資源與薪資軟體市場報告2026年全球雲端薪資核算軟體市場報告 雲端薪資核算軟體市場:依企業規模、元件、部署類型、服務類型和產業分類-2026-2032年全球預測

雲端薪資核算軟體市場:依企業規模、元件、部署類型、服務類型和產業分類-2026-2032年全球預測 2026-2030年全球薪資軟體市場

2026-2030年全球薪資軟體市場 人力資源和薪資軟體市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、組織規模、產業橫斷面、區域和競爭格局分類,2021-2031年

人力資源和薪資軟體市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、部署模式、組織規模、產業橫斷面、區域和競爭格局分類,2021-2031年 人力資源與薪資軟體市場規模、佔有率及成長分析(按應用、組織規模、部署類型和地區分類)-2026-2033年產業預測

人力資源與薪資軟體市場規模、佔有率及成長分析(按應用、組織規模、部署類型和地區分類)-2026-2033年產業預測 全球人力資源與薪資軟體市場2034 年全球人力資源與薪資軟體市場機會與策略

全球人力資源與薪資軟體市場2034 年全球人力資源與薪資軟體市場機會與策略