|

市場調查報告書

商品編碼

2073284

薪資稅合規自動化:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)Payroll Tax Compliance Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

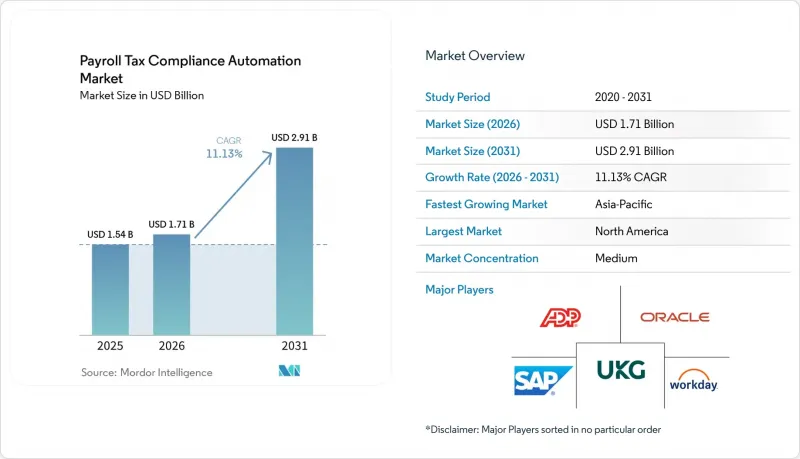

根據 Mordor Intelligence 預測,工資稅合規自動化市場預計將從 2025 年的 15.4 億美元成長到 2026 年的 17.1 億美元,到 2031 年達到 29.1 億美元,2026 年至 2031 年的複合年成長率為 11.13%。

本報告按組件(軟體和服務)、解決方案類型(工資稅計算引擎、自動報稅和繳稅等)、部署模式(雲端和本地部署)、組織規模(中小企業和大型企業)、行業(銀行、金融服務和保險等)以及地區進行細分。市場預測以美元計價。

全球薪資稅合規自動化市場趨勢與洞察

全球監管日益複雜化

由於美國有超過7,000個稅務機關、歐盟的《工資透明指令》以及印度的四項勞動法,雇主必須追蹤、檢驗和報告的工資資料項數量正在同步成長。 「一項全面而美好的法案」將在2025年後取消過渡性措施,要求系統區分《公平勞動標準法》(FLSA)規定的加班費和合約規定的額外工資,按職業代碼追蹤員工的小費收入,並管理各州特定的計算邏輯。歐洲雇主也面臨類似的壓力,因為歐盟成員國將在2026年前將歐盟指令2023/970納入本國法律。同時,印度的銀行、金融和保險(BFSI)公司必須重新設計其薪酬結構,使基本工資和生活總合合計至少佔其薪酬的50%。隨著監管日益分散,各組織被迫實施基於規則的引擎,以捕獲即時數據、應用特定司法管轄區的邏輯並產生適用於審計的審計追蹤。

快速普及基於雲端的薪資核算平台

為了獲取持續的合規性更新和人工智慧驅動的檢驗,而無需維護自身的基礎設施,各組織正在加速向雲端遷移。 UKG One View Direct 等解決方案可提供即時跨國數據,而 Symmetry Tax Logic AI 則可自動繪製 150 個國家/地區的司法管轄區。儘管雲端的複合年成長率已達到 14.32%,但由於資料主權法規和客製化需求,本地部署環境仍然佔據主導地位。因此,混合架構正被廣泛採用,在這種架構中,敏感資料儲存在本地,同時利用雲端進行分析。由於管理和維護來自供應商的合規性更新的負擔減輕,中小企業 (SME) 在雲端採用方面處於領先地位。

雲端採用中的資料安全和隱私問題

集中管理社會安全號碼和薪資資料的儲存庫是老練的網路犯罪分子的攻擊目標。 2026 年 4 月的「Storm-2755」宣傳活動暴露了一個基本的多因素身份驗證漏洞,攻擊者透過劫持會話來欺詐性地濫用加拿大工資存款。由於 GDPR 規定的資料外洩通知義務,成本風險不斷增加,企業現在要求其設施具備 SOC 2 II 型認證、靜態資料加密、特權存取監控和本地託管選項。所有這些因素都增加了實施的複雜性。

細分市場分析

2025年,軟體仍將以57.45%的市佔率主導薪資稅合規自動化市場,但隨著雇主擴大將系統設定和監管合規監控外包給外部專家,預計到2031年,服務領域將以14.01%的複合年成長率成長。託管服務供應商正以訂閱包的形式提供諮詢、變更管理和申報支援服務,充分利用「一項全面法案」(One Big Beautiful Bill Act)中關於詳細加班追蹤的要求、印度勞動法審計以及巴西FGTS數位申報系統。

在新興市場,由於需要本地專業知識,例如本地語言的文檔創建、電子工資單以及與稅務機關的資料整合,服務普及速度正在進一步加快。雖然核心引擎仍然是交易處理的基礎,但收入正轉向附加價值服務,這些服務可以降低罰款風險、加快部署速度並提供按需審計支援。

預計到2025年,稅務申報和支付引擎將佔總支出的33.62%,但隨著雇主從被動申報轉向持續檢驗,合規監控平台正以12.89%的複合年成長率快速成長。供應商正在整合監管數據,以便在申報前檢測異常情況,並應對逾期付款罰款從2%逐步提高到15%的系統。

一個能夠解讀 OBBBA 加班標準、對合格的消費小費進行分類並檢驗職位代碼的平台正在推動這一轉變,而人工智慧代理則產生符合內部和外部審計要求的審計追蹤。 SAP 的四款人工智慧薪資核算代理體現了合規監控和報告自動化的整合,PostNL 預計透過自動化日常查詢並根據管轄規則檢驗數據,可將薪資核算查詢成本降低約 80%。逐筆交易報告仍然至關重要,但自主監控正在成為跨國薪資核算營運的差異化優勢。

區域分析

預計到2025年,北美地區的收入將佔全球總收入的36.18%,這主要得益於美國超過7000個稅務管轄區、嚴格的處罰措施以及《統一商業銀行和商業法案》(OBBBA)將於2026年2月生效的最後期限。 Paychex以41億美元收購Paycor以及Intuit整合GoCo等大規模收購案凸顯了該地區的行業重組趨勢,而這一趨勢的驅動力在於人工智慧驅動的合規工具的規模化和交叉銷售。 Storm-2755等網路威脅進一步提升了經營團隊對薪資核算安全的關注,並推動了對零信任架構的投資。

預計到2031年,亞太地區將以13.26%的複合年成長率成長,主要得益於印度的勞動法、中國電子帳單的普及以及新加坡的《平台工作者法》。調查顯示,該地區80%的雇主在勞動力短缺的情況下面臨複雜的監管挑戰,這推動了人工智慧驅動的檢驗和合規管理技術的應用。印度的e-Shram和巴西的eSocial等政府入口網站正在鼓勵雲端原生整合,為本地服務供應商提供了結構性利好。

在歐洲,歐盟工資透明指令將於2026年納入各國國內法,GDPR對跨國資料傳輸設置了障礙,加上及時報告的要求日益嚴格,導致53%的雇主選擇將薪資核算外包。在南美洲,新的數位化義務正在逐步落實,例如巴西的FGTS Digital和阿根廷的Libro de Sueldos Digital。同時,中東和非洲的監管機構正在加強工資保護和電子帳單的監管。奈及利亞分階段實施的電子稅務系統和阿拉伯聯合大公國的工資申報截止日期表明,法律強制推行的數位化正在擴大整個工資稅合規自動化市場對定向服務的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球監管日益複雜

- 基於雲端的薪資核算平台迅速普及

- 跨境遠距工作者的增加

- 整合人工智慧和機器學習技術,實現即時合規

- 新興國家的政府數位化努力

- 罰款力度加大,促使人們對準確無誤的報稅表提出了更高的要求。

- 市場限制因素

- 雲端採用中的資料安全和隱私問題

- 從傳統薪資核算系統轉換過來成本很高。

- 薪資核算合規的專家短缺

- 地方稅收管轄權的細分阻礙了標準化

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 按解決方案類型

- 薪資稅計算引擎

- 稅務申報和支付自動化

- 合規監控和監管趨勢資訊平台

- 預扣稅和扣除管理系統

- 適用於多個司法管轄區的薪資核算合規模組

- 其他解決方案類型

- 部署模式

- 雲

- 現場

- 按組織規模

- 小型企業

- 大公司

- 按行業分類

- BFSI

- 衛生保健

- 資訊科技/通訊

- 零售

- 製造業

- 政府

- 其他工業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Automatic Data Processing, Inc.

- Paychex, Inc.

- Intuit Inc.

- Workday, Inc.

- Ceridian HCM Holding Inc.

- Sage Group plc

- Oracle Corporation

- SAP SE

- Gusto, Inc.

- Zenefits Global, Inc.

- Paycor HCM, Inc.

- Rippling People Center Inc.

- BambooHR LLC

- UKG Inc.

- Patriot Software Company, Inc.

- Paylocity Holding Corporation

- TriNet Group, Inc.

- Papaya Global Ltd.

- Justworks, Inc.

- CloudPay Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the payroll tax compliance automation market size is expected to increase from USD 1.54 billion in 2025 to USD 1.71 billion in 2026 and reach USD 2.91 billion by 2031, growing at a CAGR of 11.13% over 2026-2031.

This report is Segmented by Component (Software, and Services), Solution Type (Payroll Tax Calculation Engines, Tax Filing and Remittance Automation, and More), Deployment Mode (Cloud, and On-Premises), Organization Size (Small and Medium Enterprises, and Large Enterprises), Industry Vertical (BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Payroll Tax Compliance Automation Market Trends and Insights

Escalating Global Regulatory Complexity

Over 7,000 U.S. tax authorities, the EU Pay Transparency Directive, and India's four Labour Codes have simultaneously expanded payroll data points employers must track, validate, and report. The One Big Beautiful Bill Act removes transition relief after 2025, compelling systems to distinguish FLSA-required overtime from contractual premiums, trace tipped employees by occupation code, and manage state add-back logic. European employers face similar pressure as member states transpose EU 2023/970 by 2026, while BFSI firms in India must redesign compensation to ensure basic pay and dearness allowance equal at least 50% of remuneration. Heightened fragmentation is pushing organizations toward rule-based engines that ingest real-time feeds, apply jurisdiction-specific logic, and generate audit trails fit for inspection.

Rapid Adoption of Cloud-Based Payroll Platforms

Organizations are accelerating cloud migration to access continuous compliance updates and AI-driven validation without maintaining their own infrastructure. Offerings such as UKG One View Direct deliver real-time multi-country data, whereas Symmetry Tax Logic AI automates jurisdiction mapping across 150 countries.Despite cloud's 14.32% CAGR, on-premises instances remain prevalent due to data-sovereignty rules and customization needs, resulting in hybrid architectures that keep sensitive data local and leverage cloud for analytics. Small businesses lead cloud uptake, citing vendor-managed compliance updates and reduced maintenance overhead.

Data Security and Privacy Concerns in Cloud Deployments

Centralized repositories of Social Security numbers and wage data attract sophisticated cybercriminals. The Storm-2755 campaign in April 2026 diverted Canadian payroll deposits by hijacking sessions, exposing weaknesses in basic multifactor authentication. Breach notification mandates under GDPR intensify cost exposures, prompting enterprises to demand SOC 2 Type II facilities, encryption at rest, privileged-access monitoring, and local hosting options, all of which elevate implementation complexity.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cross-Border Remote Workforces

- Integration of AI and Machine Learning for Real-Time Compliance

- High Switching Costs From Legacy Payroll Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The payroll tax compliance automation market share for software remained dominant at 57.45% in 2025, yet the services segment is projected to grow at a 14.01% CAGR through 2031 as employers outsource configuration and regulatory monitoring to external specialists. Managed-service providers are capitalizing on the One Big Beautiful Bill Act's granular overtime tracking requirements, India's Labour Code audits, and Brazil's FGTS Digital submissions, packaging advisory, change management, and filing support in subscription bundles.

Services uptake is even faster in emerging markets where local-language documentation, electronic payslips, and data integration with revenue authorities demand on-the-ground expertise. Although core engines continue to underpin transaction processing, revenue is shifting toward value-added services that reduce penalty risk, accelerate deployment, and offer on-demand audit support.

Tax filing and remittance engines accounted for 33.62% of 2025 spending, yet compliance monitoring platforms are scaling at a 12.89% CAGR as employers pivot from reactive filing to continuous validation. Vendors embed regulatory feeds that flag anomalies before submission, meeting penalty regimes that escalate from 2% to 15% for late deposits.

Platforms that interpret OBBBA overtime criteria, segregate qualified tips, and validate occupation codes underpin this shift, while AI agents generate audit trails that satisfy internal and external auditors. SAP's four AI Payroll Agents exemplify the integration of compliance monitoring with filing automation, enabling PostNL to anticipate approximately 80% cost reduction for payroll questions by automating routine inquiries and validating data against jurisdiction-specific rules.Transactional filing remains essential, but autonomous monitoring is emerging as the differentiator for multinational payroll operations.

Complete Report Scope:

- By Component

- Software

- Services

- By Solution Type

- Payroll Tax Calculation Engines

- Tax Filing and Remittance Automation

- Compliance Monitoring and Regulatory Updates Platforms

- Withholding and Deduction Management Systems

- Multi-Jurisdictional Payroll Compliance Modules

- Other Solution Types

- By Deployment Mode

- Cloud

- On-Premises

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Industry Vertical

- BFSI

- Healthcare

- IT and Telecommunication

- Retail

- Manufacturing

- Government

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America generated 36.18% of 2025 revenue, anchored by the United States' 7,000-plus tax jurisdictions, stringent penalty schedules, and the February 2026 OBBBA enforcement deadline. Large acquisitions, such as Paychex's USD 4.1 billion purchase of Paycor and Intuit's integration of GoCo, underscore the region's consolidation trend aimed at scale and cross-selling AI-enabled compliance tools. Cyber threats such as Storm-2755 further sharpen board-level focus on payroll security, driving investments in zero-trust architectures.

Asia-Pacific is forecast to grow at a 13.26% CAGR to 2031, propelled by India's Labour Codes, China's e-invoice expansion, and Singapore's Platform Workers Act. Surveys reveal 80% of regional employers confront regulatory complexity with fewer staff, spurring adoption of AI validation and managed compliance. Government portals such as India e-Shram and Brazil eSocial favor cloud-native integrations, giving a structural lift to local service providers.

Europe grapples with the 2026 transposition of the EU Pay Transparency Directive, GDPR cross-border data-transfer hurdles, and rising enforcement of on-time filing, prompting 53% of employers to outsource payroll. South America enforces new digital mandates, including Brazil's FGTS Digital and Argentina's Libro de Sueldos Digital, while Middle East and Africa authorities tighten wage-protection and e-invoicing rules. Nigeria's phased electronic fiscal system and UAE's salary-payment deadlines illustrate how statutory digitization is expanding addressable demand across the broader payroll tax compliance automation market.

- Automatic Data Processing, Inc.

- Paychex, Inc.

- Intuit Inc.

- Workday, Inc.

- Ceridian HCM Holding Inc.

- Sage Group plc

- Oracle Corporation

- SAP SE

- Gusto, Inc.

- Zenefits Global, Inc.

- Paycor HCM, Inc.

- Rippling People Center Inc.

- BambooHR LLC

- UKG Inc.

- Patriot Software Company, Inc.

- Paylocity Holding Corporation

- TriNet Group, Inc.

- Papaya Global Ltd.

- Justworks, Inc.

- CloudPay Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Regulatory Complexity

- 4.2.2 Rapid Adoption of Cloud-Based Payroll Platforms

- 4.2.3 Expansion of Cross-Border Remote Workforces

- 4.2.4 Integration of AI and Machine Learning for Real-Time Compliance

- 4.2.5 Government Digitalization Initiatives in Emerging Economies

- 4.2.6 Rising Penalties Driving Demand for Error-Free Tax Filing

- 4.3 Market Restraints

- 4.3.1 Data Security and Privacy Concerns in Cloud Deployments

- 4.3.2 High Switching Costs From Legacy Payroll Systems

- 4.3.3 Shortage of Specialized Payroll Compliance Talent

- 4.3.4 Fragmented Local Tax Jurisdictions Hindering Standardization

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Solution Type

- 5.2.1 Payroll Tax Calculation Engines

- 5.2.2 Tax Filing and Remittance Automation

- 5.2.3 Compliance Monitoring and Regulatory Updates Platforms

- 5.2.4 Withholding and Deduction Management Systems

- 5.2.5 Multi-Jurisdictional Payroll Compliance Modules

- 5.2.6 Other Solution Types

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-Premises

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By Industry Vertical

- 5.5.1 BFSI

- 5.5.2 Healthcare

- 5.5.3 IT and Telecommunication

- 5.5.4 Retail

- 5.5.5 Manufacturing

- 5.5.6 Government

- 5.5.7 Other Industry Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 Paychex, Inc.

- 6.4.3 Intuit Inc.

- 6.4.4 Workday, Inc.

- 6.4.5 Ceridian HCM Holding Inc.

- 6.4.6 Sage Group plc

- 6.4.7 Oracle Corporation

- 6.4.8 SAP SE

- 6.4.9 Gusto, Inc.

- 6.4.10 Zenefits Global, Inc.

- 6.4.11 Paycor HCM, Inc.

- 6.4.12 Rippling People Center Inc.

- 6.4.13 BambooHR LLC

- 6.4.14 UKG Inc.

- 6.4.15 Patriot Software Company, Inc.

- 6.4.16 Paylocity Holding Corporation

- 6.4.17 TriNet Group, Inc.

- 6.4.18 Papaya Global Ltd.

- 6.4.19 Justworks, Inc.

- 6.4.20 CloudPay Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment