|

市場調查報告書

商品編碼

2063838

薪資和人力資源合規軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Payroll And HR Compliance Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

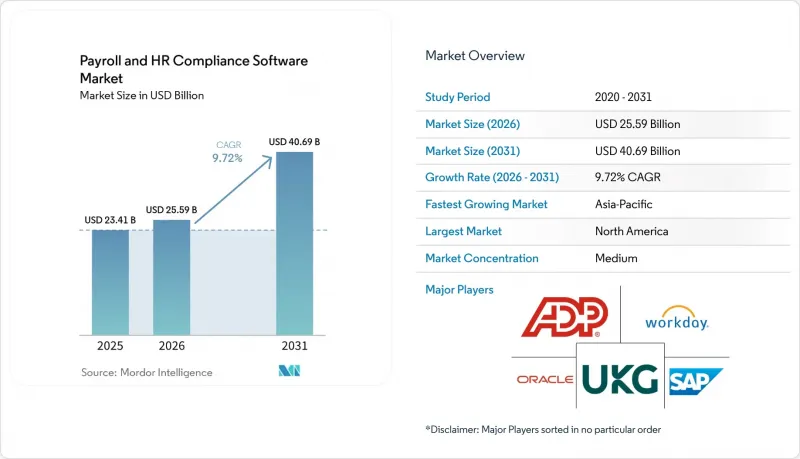

根據 Mordor Intelligence 預測,薪資核算和人力資源合規軟體的市場規模預計將從 2025 年的 234 億美元和 2026 年的 256 億美元成長到 2031 年的 407 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 9.72%。

本報告按部署模式(雲端、本地部署、混合部署)、最終用戶規模(大型企業、中小企業)、應用領域(薪資核算、人力資源合規、考勤管理、核心人力資源管理)、行業(銀行、金融服務和保險、醫療保健、IT和電信、製造業、零售業、政府部門等)以及地區進行細分。市場預測以美元計價。

全球薪資核算與人力資源合規軟體市場趨勢與洞察

中小企業採用雲端運算正在加速 SaaS薪資核算的普及。

在薪資核算和人力資源合規軟體市場,需求變化最顯著的領域是中小企業 (SME)。這些企業正在從手動流程和功能有限的薪資核算工具轉向將薪資核算、記錄保存和合規作業整合於單一環境的雲端系統。這種轉變意義重大,因為與大型企業買家相比,中小企業通常要求實施工作量更少、產品更新速度更快,而且更換供應商的次數也更少。在法國,到 2025 年,86% 的公司將使用薪資核算軟體,62% 的員工將收到電子薪資單,這表明數位化薪資管理在成熟的中小企業環境中已變得非常普遍。隨著越來越多的中小企業採用更全面的人力資源平台,與會計系統整合的獨立薪資核算模組正逐漸失去其重要性。這是因為買家更傾向於集中管理薪資、員工記錄和合規作業的工作流程。因此,薪資核算和人力資源合規軟體市場不僅受益於短期軟體更新周期,也受益於採購行為的結構性變化。

嚴格的多邊稅收和勞工合規要求

薪資和人力資源合規軟體市場持續受到合規要求的驅動,這些要求涵蓋薪資透明度、薪資文件、網路安全措施以及各國特定的勞動管理規則。當雇主跨多個司法管轄區管理薪資時,實施合規軟體帶來的業務效益將更加顯著,因為規則變更、報告要求和本地報告實踐已無法由單一的薪資團隊或本地系統來應對。 CloudPay 的 2025 年底報告指出,超過 36% 的組織目前在六個或更多國家管理薪資核算,這凸顯了在單一平台上集中管理規則和全面本地合規的必要性。這種跨國負擔並非一勞永逸,因為在初始部署之後,新的特定國家的規則和合規更新會不斷出現。因此,薪資核算和人力資源合規軟體市場由持續的合規任務驅動,雇主越來越需要將軟體管理融入薪資核算流程本身。

全球資料隱私法規的複雜性

由於各國資料隱私法規不一致,薪資及人力資源合規軟體市場持續面臨許多阻礙。由於薪資系統處理敏感的員工記錄、薪資、納稅人識別號碼和銀行帳戶訊息,每個跨境工作流程都可能需要額外的控制措施、本地審計,甚至產品重新設計。當單一雇主在多個國家處理薪資核算,並期望單一系統既能支持集中監管又能滿足當地法律要求時,這項挑戰尤其突出。對跨國薪資核算的研究表明,這些跨境營運模式已變得十分普遍,這意味著隱私摩擦對買家的影響比以往引進週期都更為顯著。因此,薪資和人力資源合規軟體市場的標準化進程較為緩慢,因為供應商通常需要提供本地託管選項、特定區域的流程邏輯以及更謹慎的資料存取設計,才能吸引跨國公司。

細分市場分析

預計到2025年,雲端服務將佔總營收的68.4%,並在2031年之前以10.8%的複合年成長率成長,明顯優於本地部署和混合部署。因此,到2025年,雲端服務將佔據薪資和人力資源合規軟體市場68.4%的佔有率,而這一領先優勢不僅體現在對託管服務的偏好上。買家選擇雲端服務的原因在於薪資核算規則頻繁變更、區域要求各異,以及軟體更新需要比傳統發布週期更快的速度。在薪資和人力資源合規軟體市場,這種模式也便於將軟體部署到新業務部門和新國家的薪資核算系統。另一方面,對於擁有高度客製化ERP系統、嚴格管理要求或分階段遷移計畫的公司而言,本地部署和混合部署仍然至關重要。

剩餘的部署模式繼續為那些無法一次性遷移所有薪資核算工作負載的買家提供支持,尤其是在監管嚴格的行業和跨國公司中,這些企業在不同國家/地區的準備程度各不相同。當企業希望在新國家/地區享受雲端薪資核算的速度,同時又能對特定資料集保持更嚴格的本地控制並與舊有系統整合時,混合部署模式就顯得尤為重要。第三方認證、安全託管和完善的管理框架已成為歐洲和其他監管嚴格地區雲端供應商的基本准入要求。這一趨勢導致薪資核算和人力資源合規軟體行業值得信賴的供應商選擇範圍縮小,因為小規模的供應商需要建立更強大的合規體系才能繼續留在候選名單上。因此,儘管薪資核算和人力資源合規軟體市場日益向雲端主導,但遷移路徑仍取決於風險接受度、在地化需求以及現有系統的複雜性。

預計到2025年,大型企業(SME)將佔總收入的61.7%,而中小企業(SME)預計到2031年將以10.4%的複合年成長率成長。大型企業仍然是薪資和人力資源合規軟體市場的基礎,這主要歸因於其多實體結構、全球稅務申報和審計要求以及與ERP系統的整合,這些因素都提高了每個客戶的軟體使用率。這些公司通常需要更精細的工作流程管理、更強大的報表功能以及薪資核算和財務系統之間更緊密的整合。同時,中小企業正從市場邊緣轉向未來需求的中心,因為他們現在將薪資核算軟體視為其業務運營的重要組成部分,而不僅僅是可有可無的後勤部門工具。這種需求在希望在一個平台上管理薪資核算、員工記錄、福利和合規性的小規模企業中尤為明顯。

中小企業市場的成長也反映出產品設計的轉變,新供應商優先考慮部署速度和降低營運負擔,而非複雜的配置。在法國,到2025年,已有86%的企業在使用薪資核算軟體,這意味著一旦中小企業更清楚地認知到薪資管理軟體的價值,其普及速度將迅速加快。新興供應商也透過將薪資核算作為其平台的切入點,進而擴展到相關服務,從而提高長期客戶維繫和市場佔有率。這種交叉銷售模式對薪資核算和人力資源合規軟體產業至關重要,因為它促使競爭對手的關注點從簡單的薪資核算處理轉向更廣泛的勞動力管理。因此,預計在整個預測期內,中小企業仍將是薪資核算和人力資源合規軟體市場中最商業性的買家群體。

區域分析

2025年,北美將佔全球整體銷售額的38.6%,成為薪資核算和人力資源合規軟體中最大的區域市場。因此,北美將在2025年佔據薪資核算和人力資源合規軟體市場38.6%的佔有率,這主要得益於美國的強勁成長。美國擁有強大的薪資核算平台和整合解決方案,以及對合規產品的高需求。該地區也受益於「薪資預支」(Earned Wage Access)的積極發展,這是薪資連接的一個重要相關應用場景。 2025年12月,關於某些「工資預支」產品不被視為Z條例下的信貸的明確規定,解決了雇主整合模式方面的一個重要監管擔憂。此外,由於企業客戶持續投資於整合薪資核算、勞動力管理和員工財務服務的系統,北美薪資和人力資源合規軟體市場仍保持著吸引力。

歐洲仍然是第二大區域市場,其中英國、德國、法國和西班牙是主要的需求中心。歐洲的薪資和人力資源合規軟體市場受各國薪資格式、報告要求和資料處理預期的影響,因此既需要在地化,也需要可擴展性。在法國,到2025年,86%的公司將使用薪資核算軟體,62%的員工將收到電子薪資單,這表明法國的數位化薪資環境已經成熟,預計對檢驗和升級的需求將會增加。這些在地化需求使得歐洲成為既能提供跨國服務又能深度支援特定國家工作流程的供應商的理想市場。

預計到2031年,亞太地區將以12.7%的複合年成長率成長,成為薪資核算和人力資源合規軟體市場成長最快的地區。隨著勞動力市場日趨規範化、中小企業數位轉型以及跨國公司在印度、東南亞和澳洲等地深化佈局,市場需求不斷成長。 2025年10月,一家供應商宣布計畫在2029年在100多個國家/地區實現原生薪資核算支援。這表明,供應商如今已將針對特定國家/地區的功能視為此快速變化地區的關鍵成長驅動力。南美洲和中東及非洲市場仍處於發展初期,但隨著勞動法現代化、雇主外包服務以及全球人力資源平台的擴展,薪資核算營運逐漸擺脫人工流程,這些地區的市場採用率也不斷上升。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中小企業採用雲端運算正在加速基於 SaaS 的薪資核算系統的普及。

- 嚴格的多邊稅收和勞工合規要求

- 將薪資核算API 整合到金融科技生態系統中

- 過渡到按需工資和預支工資服務

- 人工智慧驅動的薪資核算錯誤偵測和詐欺預防

- 自由工作者和零工人員數量的增加需要彈性的薪資核算。

- 市場限制因素

- 全球資料隱私法規的複雜性

- 由於遺留ERP模組,遷移成本高昂

- 薪資合規專員技能短缺

- 受監管產業對外包薪資核算的抵制

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 雲

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 透過使用

- 薪資核算

- 考勤管理

- 人力資源合規與監管管理

- 員工福利與薪資管理

- 核心人力資源與員工檔案管理

- 按最終用戶行業分類

- 資訊科技(IT)和通訊

- 銀行、金融服務和保險(BFSI)

- 醫療保健和生命科學

- 工業製造

- 零售與電子商務

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Automatic Data Processing, Inc.

- Paychex, Inc.

- Workday, Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- Paylocity Holding Corporation

- Oracle Corporation

- SAP SE

- Intuit Inc.

- Paycom Software, Inc.

- Rippling People Center Inc.

- Gusto, Inc.

- HiBob Inc.

- Deel Inc.

- Papaya Global Ltd.

- BambooHR LLC

- Sage Group plc

- Paycor HCM, Inc.

- Personio

- Ramco Systems Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the payroll and HR compliance software market size is projected to expand from USD 23.4 billion in 2025 and USD 25.6 billion in 2026 to USD 40.7 billion by 2031, registering a CAGR of 9.72% between 2026 and 2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), End User Size (Large Enterprises, and Small and Medium Enterprises), Application (Payroll Processing, HR Compliance, Time and Attendance, and Core HR), Vertical (BFSI, Healthcare, IT and Telecom, Manufacturing, Retail, Government, and More), and Geography. The Market Forecast are Provided in Terms of Value (USD).

Global Payroll And HR Compliance Software Market Trends and Insights

Cloud Adoption by SMEs Accelerating SaaS Payroll Uptake

The payroll and HR compliance software market is seeing one of its clearest demand shifts in the SME segment, where buyers are moving from manual processes and narrow payroll tools to cloud systems that combine payroll, records, and compliance tasks in a single environment. This change matters because smaller firms usually need lower setup effort, faster product updates, and fewer vendor handoffs than large enterprise buyers. In France, 86% of companies used payroll software in 2025, and 62% of employees received digital payslips, indicating how commonplace digital payroll administration has become in a mature SME setting. As more SMEs adopt broader HR platforms, standalone accounting-linked payroll modules become less relevant, as buyers prefer a single workflow for pay, employee records, and compliance actions. The payroll and HR compliance software market, therefore, benefits from a structural shift in buying behavior, not just from short-term software replacement cycles.

Stringent Multi-Country Tax and Labor Compliance Mandates

The payroll and HR compliance software market continues to gain support from compliance mandates that now span pay transparency, payroll documentation, cyber controls, and country-specific labor administration rules. The commercial case becomes stronger when employers manage payroll across several jurisdictions, because rule changes, reporting demands, and local filing practices no longer sit neatly inside one payroll team or one local system. CloudPay reported in late 2025 that more than 36% of organizations now manage payroll across 6 or more countries, underscoring the need for centralized rules and local compliance enforcement within a single platform. This multi-country burden does not act as a one-time trigger, because new country rules and compliance updates continue to arrive after the initial implementation. The payroll and HR compliance software market is therefore being pulled forward by recurring compliance work that employers increasingly want software to manage inside the payroll process itself.

Complexities in Global Data Privacy Regulations

The payroll and HR compliance software market still faces a major restraint from data privacy rules that do not align neatly across countries. Payroll systems handle sensitive employee records, pay details, tax identifiers, and banking data so that each cross-border workflow can trigger extra controls, local review, or product redesign. This becomes harder when one employer runs payroll across multiple countries and expects one system to support both centralized oversight and local legal requirements. Multi-country payroll findings show how common these cross-border operating models have become, indicating that privacy friction now affects a wider share of buyers than in earlier deployment cycles. The payroll and HR compliance software market, therefore, faces slower standardization because vendors often need local hosting choices, regional process logic, and more careful data access design to win multinational clients.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Payroll Error Detection and Fraud Prevention

- Integration of Payroll APIs Into Fintech Ecosystems

- High Switching Costs From Legacy ERP Modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud accounted for 68.4% of revenue in 2025 and is projected to expand at a 10.8% CAGR through 2031, keeping it clearly ahead of on-premises and hybrid options. Cloud, therefore, represented 68.4% of the payroll and HR compliance software market share in 2025, and that lead reflects more than hosting preference alone. Buyers are choosing the cloud because payroll rules change frequently, local requirements vary, and software updates need to move faster than traditional release cycles. In the payroll and HR compliance software market, this model also supports easier rollout across new business units and new country payrolls. On-premises and hybrid deployments still matter for enterprises with heavy ERP customization, strict control requirements, or gradual migration plans.

The remaining deployment mix continues to serve buyers that cannot move all payroll workloads at once, particularly in regulated verticals and multinational groups with uneven country readiness. Hybrid deployments remain useful where firms want cloud speed for new-country payrolls but still want tighter local control for selected data sets or legacy integrations. Third-party certifications, secure hosting, and documented control frameworks have become a basic entry requirement for cloud vendors in Europe and other sensitive regions. That dynamic is narrowing the field of credible providers in the payroll and HR compliance software industry, because smaller vendors need a stronger compliance posture just to stay on the shortlist. The payroll and HR compliance software market is thus becoming more cloud-led, but the migration path still depends on risk tolerance, localization needs, and installed-base complexity.

Large enterprises accounted for 61.7% of revenue in 2025, while SMEs are expected to record the faster 10.4% CAGR through 2031. The large enterprise base still anchors the payroll and HR compliance software market because multi-entity structures, global tax filings, audit demands, and ERP links create higher software intensity per customer. These employers often need deeper workflow control, stronger reporting layers, and closer coordination between payroll and finance systems. SMEs, however, are shifting from the margin of the category to the center of future demand because they now see payroll software as an operating necessity rather than an optional back-office tool. That demand is especially evident among small firms that want a single platform for payroll, employee records, benefits, and compliance.

Growth in the SME segment also reflects a shift in product design, as newer vendors emphasize speed of deployment and lower operational burden rather than heavy configuration. In France, 86% of companies were already using payroll software in 2025, suggesting that adoption can move quickly once the value case becomes clear among SMEs. Challenger vendors are also turning payroll into a platform entry point, then expanding into adjacent services that raise retention and wallet share over time. That cross-sell pattern matters for the payroll and HR compliance software industry because it shifts competition away from simple payroll processing and toward broader workforce administration. The payroll and HR compliance software market should therefore see the SME segment remain the most commercially active buyer group during the forecast period.

Geography Analysis

North America accounted for 38.6% of global revenue in 2025, making it the largest regional market for payroll and HR compliance software. North America, therefore, accounted for 38.6% of the payroll and HR compliance software market share in 2025, led by the United States, which has a dense base of payroll platforms, integrations, and compliance-oriented product demand. The region also benefits from active development in earned wage access, which has become a major adjacent use case for payroll connectivity. In December 2025, it was clarified that covered earned wage access products are not considered credit under Regulation Z, which reduced one important regulatory concern for employer-integrated models. The payroll and HR compliance software market in North America also remains attractive because enterprise clients continue to invest in systems that connect payroll, workforce administration, and employee financial services.

Europe remained the second-largest regional market, with the United Kingdom, Germany, France, and Spain forming the main demand centers. The payroll and HR compliance software market in Europe is shaped by country-specific payroll formats, reporting requirements, and data-handling expectations that require both localization and scale. In France, 86% of companies used payroll software in 2025, and 62% of employees received digital payslips, indicating a mature digital payroll environment with room for validation and upgrade demand. These local requirements make Europe a strong region for vendors that combine multi-country coverage with deep in-country workflow support.

Asia-Pacific is projected to grow at a 12.7% CAGR through 2031, making it the fastest-growing region in the payroll and HR compliance software market. Demand is rising as labor markets formalize, SME digitization spreads, and multinational employers expand deeper into India, Southeast Asia, and Australia. In October 2025, one vendor announced plans to target native payroll coverage in 100+ countries by 2029, which shows how seriously vendors now view in-country capability as a growth lever across fast-moving regions. South America, the Middle East, and Africa are still earlier-stage markets, but adoption is rising as labor law modernization, employer-of-record services, and global HR platform expansion push payroll administration away from manual processes.

- Automatic Data Processing, Inc.

- Paychex, Inc.

- Workday, Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- Paylocity Holding Corporation

- Oracle Corporation

- SAP SE

- Intuit Inc.

- Paycom Software, Inc.

- Rippling People Center Inc.

- Gusto, Inc.

- HiBob Inc.

- Deel Inc.

- Papaya Global Ltd.

- BambooHR LLC

- Sage Group plc

- Paycor HCM, Inc.

- Personio

- Ramco Systems Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Adoption by SMEs Accelerating SaaS Payroll Uptake

- 4.2.2 Stringent Multi-country Tax and Labor Compliance Mandates

- 4.2.3 Integration of Payroll APIs into Fintech Ecosystems

- 4.2.4 Shift Toward On-demand Pay and Earned Wage Access

- 4.2.5 AI-driven Payroll Error Detection and Fraud Prevention

- 4.2.6 Growing Freelancer and Gig Workforce Requiring Agile Payroll

- 4.3 Market Restraints

- 4.3.1 Complexities in Global Data Privacy Regulations

- 4.3.2 High Switching Costs from Legacy ERP Modules

- 4.3.3 Skill Shortage in Payroll Compliance Specialists

- 4.3.4 Resistance to Payroll Process Outsourcing in Regulated Verticals

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Application

- 5.3.1 Payroll Processing

- 5.3.2 Time and Attendance Management

- 5.3.3 HR Compliance and Regulatory Management

- 5.3.4 Benefits and Compensation Administration

- 5.3.5 Core HR and Employee Records Management

- 5.4 By End User Industry Vertical

- 5.4.1 Information Technology (IT) and Telecom

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Industrial Manufacturing

- 5.4.5 Retail and eCommerce

- 5.4.6 Government and Public Sector

- 5.4.7 Other End User Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 Paychex, Inc.

- 6.4.3 Workday, Inc.

- 6.4.4 UKG Inc.

- 6.4.5 Ceridian HCM Holding Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Oracle Corporation

- 6.4.8 SAP SE

- 6.4.9 Intuit Inc.

- 6.4.10 Paycom Software, Inc.

- 6.4.11 Rippling People Center Inc.

- 6.4.12 Gusto, Inc.

- 6.4.13 HiBob Inc.

- 6.4.14 Deel Inc.

- 6.4.15 Papaya Global Ltd.

- 6.4.16 BambooHR LLC

- 6.4.17 Sage Group plc

- 6.4.18 Paycor HCM, Inc.

- 6.4.19 Personio

- 6.4.20 Ramco Systems Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

會計軟體市場:2026-2032年全球市場預測(依軟體、功能、定價模式、應用程式、部署類型、企業規模、最終用戶和產業分類)

會計軟體市場:2026-2032年全球市場預測(依軟體、功能、定價模式、應用程式、部署類型、企業規模、最終用戶和產業分類) 2026年全球稅務和會計軟體市場報告

2026年全球稅務和會計軟體市場報告 人力資源和薪資管理軟體市場:按部署類型、行業和地區分類

人力資源和薪資管理軟體市場:按部署類型、行業和地區分類 全球基金會計軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球會計軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球線上記帳與會計軟體市場報告2026年全球商業會計軟體市場報告2026年全球會計軟體市場報告2026年全球雲端會計軟體市場報告2026年全球預算管理軟體市場報告

全球基金會計軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球會計軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034)2026年全球線上記帳與會計軟體市場報告2026年全球商業會計軟體市場報告2026年全球會計軟體市場報告2026年全球雲端會計軟體市場報告2026年全球預算管理軟體市場報告