|

市場調查報告書

商品編碼

2073095

碳排放預測和情境建模軟體:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Predictive Carbon Forecasting and Scenario Modeling Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

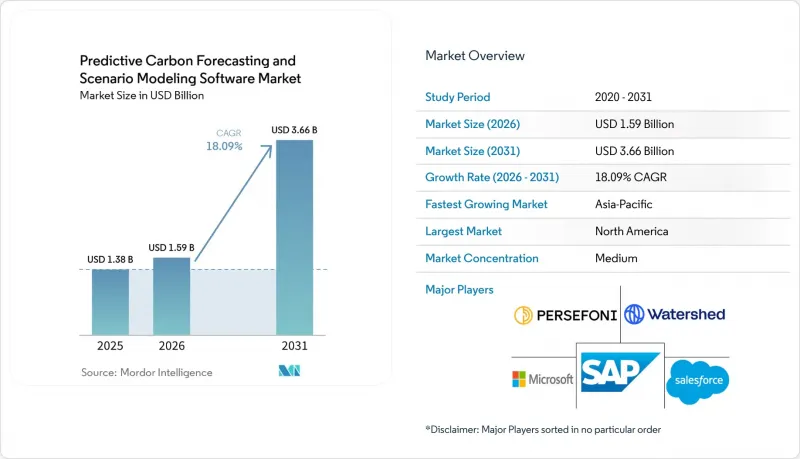

根據 Mordor Intelligence 預測,碳排放預測和情境建模軟體的市場規模預計將從 2025 年的 13.8 億美元和 2026 年的 15.9 億美元成長到 2031 年的 36.6 億美元,2026 年至 2031 年的複合年成長率為 18.09%。

本報告按交付類型(軟體和服務)、部署類型(雲端、本地部署、混合部署)、應用領域(排放預測及其他)、公司規模(大型企業和中小企業)、最終用戶行業(能源和公共產業、銀行、金融服務和保險業及其他)以及地區進行細分。市場預測以美元計價。

全球碳排放預測及情境建模軟體市場趨勢及洞察

監管機構對氣候變遷資訊揭露和淨零排放計畫施加壓力

監管壓力仍然是推動軟體需求的最緊迫因素,因為揭露規則現在要求企業系統化碳數據,以支援規劃、檢驗和情境檢驗,而不僅僅是在財政年度結束時進行報告。國際財務報告準則基金會於2025年12月修訂了IFRS S2下的溫室氣體揭露要求,旨在降低實施複雜性,同時維持報告對決策的實用性。這有助於維持企業需求,即使整個市場的報告預期都在變化。在美國,當美國證券交易委員會(SEC)提案在2026年5月廢除氣候變遷揭露規則時,市場出現了不不確定性,但對決策工具的廣泛需求並未消失,因為許多公司仍在多個報告系統下運營,並且必須滿足投資者的期望。這對碳排放預測和情境建模軟體市場有重大影響,因為情境分析正日益被視為財務管治的一部分,而不僅僅是永續發展合規任務。因此,將自身工具定位為「規劃基礎設施」的供應商比主要依賴合規清單的供應商更具優勢。因此,即使個別法規被修改、推遲或受到質疑,碳排放預測和情境建模軟體市場仍將繼續受益於這些法規。

將人工智慧應用於排放預測和減排管道最佳化

人工智慧正在改變碳排放軟體的使用方式,因為買家現在期望在單一工作流程中獲得更快的資料清洗、更快速的模擬以及更具互動性的結果解讀。 2026年5月,SAP宣布其足跡最佳化代理將情境模擬時間從大約一天縮短至20分鐘,顯示軟體競爭正朝著更快的反應速度和更高的操作便利性方向發展。 2026年4月發表的一項同行評審研究也發現,在能源密集產業的碳排放預測方面,協作式深度學習架構優於傳統的基準方法,這支持了向人工智慧驅動的預測模型的廣泛轉變。這種轉變擴展了這些工具的作用,使其從靜態的排放報告擴展到主動的減排管道選擇、交易層級分析和更快的決策支援。這也提高了碳排放預測和情境建模軟體市場的產品設計標準,因為買家現在不僅比較模型的全面性,還比較得出可操作答案所需的時間。隨著越來越多的平台原生整合人工智慧,碳排放預測和情境建模軟體市場預計將出現更加明顯的兩極化,一方是擁有技術深度的供應商,另一方則只是提供表面報告任務自動化的供應商。

範圍 3 的限制以及供應商活動資料的品質和可用性

供應商資料的品質仍然是最大的營運限制因素。這是因為最關鍵的排放類別往往標準化程度最低,且在整個複雜的價值鏈中檢驗也最困難。 2025年4月進行的一項調查發現,79%的組織認為供應商資料的可用性是他們面臨的最大挑戰,62%的組織指出內部資料的品質是主要障礙,這表明即使提高了報告系統的成熟度,輸入問題也並未解決。調查也指出,範圍3排放通常占公司總排放的75%以上,而準確量化的主要障礙仍是缺乏供應商數據。這個弱點直接影響碳排放預測和情境建模軟體市場,因為模型的可靠性取決於用於訓練、映射和測試的資料的可靠性。雖然公司仍然可以使用基於支出的替代指標和估算邏輯,但當投資者、審計師或採購團隊要求更高的精確度時,這些方法的可靠性就會降低。在供應商參與度顯著提高之前,碳排放預測和情境建模軟體市場在關鍵決策中模型輸出的可靠性方面,可能仍將面臨實際限制。

細分市場分析

2025年,軟體收入佔總收入的76.12%,顯示基於授權的平台仍然是企業在預測碳排放和情境建模市場支出的核心。買家越來越傾向於選擇可在報告、規劃和風險評估週期中重複使用的工具,而不是僅依賴專案主導的諮詢服務。這一趨勢也表明,許多組織已經超越了最初的範圍界定階段,開始將碳分析融入日常營運流程中。在此背景下,平台所有者變得至關重要,因為持續存取能夠實現更快的更新、更廣泛的公司內部應用,以及對假設和審計追蹤更一致的管治。此外,訂閱收入可以再投資於建模深度、人工智慧功能和工作流程設計,為供應商的產品改進奠定更堅實的基礎。

服務領域持續快速成長,預計到2031年複合年成長率將達到21.54%。這是因為僅靠軟體本身無法滿足實施支援、情境設計和結果解讀等方面的需求。雖然許多組織可以收集基本的排放數據,但它們仍然需要外部支援來建立可靠的排放管道、對承諾進行壓力測試,並創建供投資者和審計人員審查的交付成果。服務領域的成長並非顯示軟體應用不足;相反,它標誌著碳排放預測和情境建模軟體市場正朝著更複雜的應用情境轉變。隨著建模對策略的重要性日益凸顯,買家更願意為模型配置和管治的專家支援付費。隨著時間的推移,一種相互關聯的收入模式將逐漸形成,軟體作為基礎,服務則作為附加層,在更廣泛的應用背景下不斷發展。因此,預測性碳排放預測和情境建模軟體市場的特徵並非是兩種模型之間的選擇,而是擁有成熟的軟體核心和不斷擴展的諮詢能力。

到2025年,基於雲端的採用將佔收入的65.13%。這反映了企業對靈活平台的需求,該平台能夠處理大量數據、適應定期更新,並支援跨不同業務部門的情境測試。在預測性碳排放預測和情境建模軟體市場,採用雲端技術可以減少基礎設施摩擦,並實現集中式排放數據、情境庫以及全球業務營運中的使用者存取。當規則、管道和揭露要求發生變化時,雲端技術還能支援更快的產品更新。這在該領域至關重要,因為隨著假設的演變和企業擴大其範圍3的覆蓋範圍,模型必須不斷更新。此外,雲端架構也有助於供應商提供需要更強大運算能力和共用建模環境的分析功能。

預計到2031年,基於雲端的採用率將以20.92%的複合年成長率成長,這意味著在碳排放預測和情境建模軟體市場中,規模最大的模型仍然是成長最快的。 2026年5月,一家供應商宣布推出一個雲端原生平台,旨在幾週內提供可用於審計的基準,同時減輕數據收集的負擔。這凸顯了買家為何將雲端模式與更快的設定和更低的運維負擔連結起來。對於需要嚴格控制的機構而言,本地部署環境仍然至關重要;而當資料儲存位置和合約保密性受到關注時,混合模式仍然非常有用。快速部署、共用存取和易於擴展的優勢在本地環境中難以實現,因此雲端仍然是新部署的首選。這一趨勢為雲端供應商在碳排放預測和情境建模軟體市場中拓展業務範圍提供了更大的空間。這也促使產品設計朝著持續資料擷取和頻繁情境迭代的方向發展,而不是間歇性的大量分析。

區域分析

2025年,北美地區佔全球銷售額的35.12%,成為碳排放預測和情境建模軟體市場最大的區域貢獻者。該地區擁有眾多上市公司、成熟的軟體採購流程以及集中的企業平台供應商,這些都是其優勢所在。此外,其強大的投資者生態系統意味著,與發展尚不成熟的企業軟體市場相比,氣候變遷報告和規劃問題往往會更早提交董事會和財務部門討論。美國仍然是主要的需求中心,因為許多大型公司已經建立了完善的資訊揭露流程和內部控制機制,這些機制可以擴展到碳排放規劃工作流程。儘管聯邦政策環境的穩定性有所下降,但這使得碳排放預測和情境建模軟體市場在北美地區建立了強大的商業基礎。

預計到2031年,亞太地區將以22.91%的複合年成長率成長,成為碳排放預測和情境建模軟體市場成長最快的區域市場。這一成長主要得益於向正式氣候資訊揭露要求的廣泛過渡、脫碳投資的增加以及出口導向生產網路中對供應商層面碳排放可見性的日益成長的需求。中國科學院於2026年4月發布的「盤石宇恆」大型碳計量模型1.0版,發出了一個重要的技術訊號,顯示國內碳建模基礎設施正在積極發展(NEA.GOV.CN)。這一點至關重要,因為區域應用不僅取決於引進的合規框架,還取決於本地能力建設和產業政策目標。因此,在跨國需求和本地平台發展的雙重推動下,亞太地區的碳排放預測和情境建模軟體市場仍有成長空間。

歐洲仍然是碳排放預測和情境建模軟體市場的堅實基礎,因為氣候管治已經融入許多公司的報告和風險管理流程中。即使簡化的報告流程在一定程度上減輕了合規負擔,情境分析仍然與公司如何評估關鍵氣候風險以及製定長期計畫密切相關。南美洲雖然市場規模仍然較小,但出口導向產業和金融機構對更有系統的碳規劃工具的需求正在成長。中東和非洲市場尚處於起步階段,但隨著國營能源公司、主權投資者和上市公司製定更正式的氣候轉型藍圖,市場興趣日益濃厚。在全部區域,預測性碳排放預測和情境建模軟體市場成長最快的地區,可能是那些買家能夠將合規需求與可操作的規劃價值聯繫起來的地區,而不僅僅是將軟體視為一種報告工具。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 監管機構對氣候變遷資訊揭露和淨零排放計畫施加壓力

- 企業對前瞻性碳排放情境規劃的需求日益成長

- 在董事會層級擴大與環境、社會和治理相關的資本配置和氣候管治。

- 大型企業正擴大採用基於雲端的永續發展平台。

- 將人工智慧應用於排放預測和最佳化排放管道

- 供應商、資產和投資組合決策中需要量化轉型風險。

- 市場限制因素

- 範圍 3 的限制以及供應商活動資料的品質和可用性

- ERP、EHS 和資料湖環境中高層整合的複雜性

- 中型企業採購負責人在預算審查和投資報酬率實現方面存在延誤

- 由於假設的敏感性和審計的嚴格審查,人們對該模型的可靠性存在擔憂。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按規定表格

- 軟體

- 服務

- 按實現類型

- 基於雲端的

- 本地部署

- 混合型

- 透過使用

- 排放預測

- 氣候情境和路徑模型

- 氣候和轉型風險評估

- 脫碳計劃和排放最佳化

- 按公司規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- BFSI

- 能源與公共產業

- 石油和天然氣

- 製造業和工業

- 運輸/物流

- 科技與通訊

- 零售和消費品

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- Salesforce, Inc.

- SAP SE

- IBM Corporation

- Oracle Corporation

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Sweep SAS

- Plan A Earth GmbH

- Greenly SAS

- Normative AB

- Sinai Technologies, Inc.

- Emitwise Ltd.

- Position Green AB

- Gaia Carbon Accounting Ltd.

- Sphera Solutions, Inc.

- Enablon North America Corp.

- Evercomm Singapore Pte. Ltd.

- Workiva Inc.

- Terrascope Pte. Ltd.

- VelocityEHS Holdings, Inc.

- ClimateView AB

- Intelex Technologies ULC

- CarbonChain Ltd.

- Accacia AI Solutions Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the predictive carbon forecasting and scenario modeling software market size is projected to expand from USD 1.38 billion in 2025 and USD 1.59 billion in 2026 to USD 3.66 billion by 2031, registering a CAGR of 18.09% between 2026 and 2031.

This report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Emissions Forecasting, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Energy and Utilities, BFSI, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Predictive Carbon Forecasting and Scenario Modeling Software Market Trends and Insights

Regulatory Pressure on Climate Disclosures and Net-Zero Planning

Regulatory pressure remains the most immediate driver of software demand, as disclosure rules now require companies to organize carbon data to support planning, verification, and scenario testing rather than simple year-end reporting. The IFRS Foundation updated greenhouse gas disclosure requirements under IFRS S2 in December 2025 to reduce implementation complexity while preserving decision-useful reporting, helping sustain enterprise demand as reporting expectations evolved across market. The United States introduced uncertainty when the SEC proposed rescinding its climate disclosure rules in May 2026, but that did not remove the broader demand for decision-ready tools, as many companies still operate across multiple reporting regimes and face investor expectations. This matters for the predictive carbon forecasting and scenario modeling software market because scenario analysis is increasingly treated as part of financial governance, not only as a sustainability compliance task. Vendors that frame their tools as planning infrastructure are therefore better positioned than vendors that depend mainly on compliance checklists. The effect is that the predictive carbon forecasting and scenario modeling software market continues to benefit from regulation even when individual rules are revised, delayed, or challenged.

Integration of AI for Emissions Forecasting and Abatement Pathway Optimization

AI is reshaping how carbon software is used because buyers now expect faster data cleaning, quicker simulations, and more interactive interpretation of results within a single workflow. SAP stated in May 2026 that its Footprint Optimization Agent reduced scenario simulation time from around 1 day to 20 minutes, demonstrating how software competition is moving toward faster response times and greater operational usability. A peer-reviewed study published in April 2026 also found that coordinated deep-learning architectures outperformed traditional baseline methods for predicting carbon emissions in energy-intensive industries, supporting the broader move toward AI-driven forecasting models. That shift expands the role of these tools from static emissions reporting into active pathway selection, transaction-level analysis, and faster decision support. It also raises the bar for product design in the predictive carbon forecasting and scenario modeling software market, because buyers will compare not only model breadth but also the time needed to reach a usable answer. As more platforms embed AI natively, the predictive carbon forecasting and scenario modeling software market is likely to further separate between vendors with strong technical depth and those that only automate surface-level reporting tasks.

Limited Quality and Availability of Scope 3 and Supplier Activity Data

Supplier data quality remains the largest operating constraint, because the most material emissions categories are often the least standardized and the hardest to verify across complex value chains. In April 2025, one survey found that 79% of organizations identified supplier data availability as their top challenge, while 62% pointed to internal data quality as a major barrier, which shows that reporting maturity has not solved the input problem. Another study noted that Scope 3 emissions often account for more than 75% of a company's total emissions and that supplier data gaps remain the main obstacle to accurate quantification. That weakness directly affects the predictive carbon forecasting and scenario modeling software market because models can only be as credible as the data used to train, map, and test them. Companies can still use spend-based proxies and estimation logic, but those methods weaken confidence when investors, auditors, or procurement teams need greater precision. Until supplier participation improves at scale, the predictive carbon forecasting and scenario modeling software market will continue to face a practical ceiling on how far model outputs can be trusted in high-stakes decisions.

Other drivers and restraints analyzed in the detailed report include:

- Rising Enterprise Demand for Forward-Looking Carbon Scenario Planning

- Expansion of ESG-Linked Capital Allocation and Board-Level Climate Governance

- High Integration Complexity With ERP, EHS, and Data-Lake Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 76.12% of revenue in 2025, indicating that licensed platforms remained the center of enterprise spending in the predictive carbon forecasting and scenario modeling market. Buyers increasingly favored tools they could use repeatedly across reporting, planning, and risk review cycles rather than relying solely on project-led advisory work. This pattern also indicates that many organizations had already moved past early scoping exercises and started embedding carbon analysis into routine operating processes. In that setting, platform ownership matters because recurring access enables faster updates, broader internal use, and more consistent governance of assumptions and audit trails. It also gives vendors a stronger basis for product improvement because subscription revenue can be reinvested in modeling depth, AI functionality, and workflow design.

Services are still expanding faster, with a projected CAGR of 21.54% through 2031, because software alone does not remove the need for implementation support, scenario design, and interpretation of results. Many organizations can collect basic emissions data, but they still need external help to build credible abatement pathways, stress-test commitments, and prepare outputs for investor or auditor review. This means service growth is not a sign of weak software adoption, but rather that the predictive carbon forecasting and scenario modeling software market is moving into more complex use cases. As modeling becomes more material to strategy, buyers are more willing to pay for expert support around model setup and governance. Over time, this creates a linked revenue pattern in which software remains the anchor and services grow as an attached layer around deeper adoption. The predictive carbon forecasting and scenario modeling software market, therefore, shows a mature software core with a growing advisory edge, rather than a choice between the 2 models.

Cloud-based deployment accounted for 65.13% of revenue in 2025, reflecting enterprise demand for flexible platforms that can handle large data volumes, support regular updates, and enable scenario testing across different business units. In the predictive carbon forecasting and scenario modeling software market, cloud deployment reduces infrastructure friction and enables centralization of emissions data, scenario libraries, and user access across global operations. It also supports faster product updates when rules, pathways, and disclosure requirements change. That is important in a category where models must be refreshed as assumptions evolve and as companies widen their Scope 3 coverage. Cloud architecture further helps vendors deliver analytics features that require greater computing capacity and shared model environments.

Cloud-based deployment is projected to expand at a 20.92% CAGR through 2031, indicating that the largest model remains the fastest-growing in the predictive carbon forecasting and scenario modeling software market. In May 2026, one vendor introduced a cloud-native platform designed to deliver an audit-ready baseline within weeks while reducing data-collection effort, underscoring why buyers associate cloud models with faster setup and lower operating drag. On-premise environments still matter for institutions with strict control needs, and hybrid models remain useful where data residency or contractual sensitivity is a concern. Even so, new deployments continue to favor the cloud because the value of faster onboarding, shared access, and easier scaling is hard to match through local infrastructure. This dynamic gives cloud vendors more room to widen their reach inside the predictive carbon forecasting and scenario modeling software market. It also encourages product design that assumes continuous data ingestion and frequent scenario iteration rather than infrequent batch analysis.

Complete Report Scope:

- By offering

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

- By Application

- Emissions Forecasting

- Climate Scenario and Pathway Modeling

- Climate and Transition Risk Assessment

- Decarbonization Planning and Abatement Optimization

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End User Industry

- BFSI

- Energy and Utilities

- Oil and Gas

- Manufacturing and Industrial

- Transportation and Logistics

- Technology and Telecommunications

- Retail and Consumer Goods

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America accounted for 35.12% of revenue in 2025, making it the largest regional contributor to the predictive carbon forecasting and scenario modeling software market. The region benefits from a dense base of listed companies, mature software procurement practices, and a strong concentration of enterprise platform vendors. It also has a deep investor ecosystem that tends to push climate reporting and planning issues into board and finance discussions sooner than in less mature enterprise software markets. The United States remained the main demand center because many large companies already had disclosure processes and internal controls that could be extended into carbon planning workflows. This gave the predictive carbon forecasting and scenario modeling software market a strong commercial base in North America, even as the federal policy environment became less consistent.

Asia-Pacific is projected to expand at a 22.91% CAGR through 2031, which makes it the fastest-growing regional segment in the predictive carbon forecasting and scenario modeling software market. A broader shift toward formal climate disclosure requirements, rising decarbonization investment, and the growing need for supplier-level carbon visibility across export-oriented production networks support growth in the region. China added an important technology signal in April 2026 when the Chinese Academy of Sciences released the Panshi Yuheng carbon accounting large model v1.0, showing active development of domestic carbon modeling infrastructure NEA.GOV.CN. That matters because regional adoption is not driven solely by imported compliance frameworks, but also by local capability-building and industrial policy goals. The predictive carbon forecasting and scenario modeling software market, therefore, has room to grow in Asia-Pacific through both multinational demand and local platform development.

Europe continues to provide a strong base for the predictive carbon forecasting and scenario modeling software market because climate governance is already embedded in many corporate reporting and risk management processes. Even where reporting simplification has reduced some compliance burden, scenario analysis remains closely tied to how enterprises frame material climate exposure and long-term planning. South America is still smaller, but export-oriented sectors and financial institutions are creating selective demand for more structured carbon planning tools. The Middle East and Africa remain early-stage markets, yet interest is rising as state energy companies, sovereign investors, and listed firms are building more formal climate transition roadmaps. Across these regions, the predictive carbon forecasting and scenario modeling software market is most likely to grow where buyers can connect compliance needs with practical planning value rather than treat software as a reporting-only purchase.

- Microsoft Corporation

- Salesforce, Inc.

- SAP SE

- IBM Corporation

- Oracle Corporation

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Sweep SAS

- Plan A Earth GmbH

- Greenly SAS

- Normative AB

- Sinai Technologies, Inc.

- Emitwise Ltd.

- Position Green AB

- Gaia Carbon Accounting Ltd.

- Sphera Solutions, Inc.

- Enablon North America Corp.

- Evercomm Singapore Pte. Ltd.

- Workiva Inc.

- Terrascope Pte. Ltd.

- VelocityEHS Holdings, Inc.

- ClimateView AB

- Intelex Technologies ULC

- CarbonChain Ltd.

- Accacia AI Solutions Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Pressure on Climate Disclosures and Net-Zero Planning

- 4.2.2 Rising Enterprise Demand for Forward-Looking Carbon Scenario Planning

- 4.2.3 Expansion of ESG-Linked Capital Allocation and Board-Level Climate Governance

- 4.2.4 Growing Adoption of Cloud-Based Sustainability Platforms in Large Enterprises

- 4.2.5 Integration of AI for Emissions Forecasting and Abatement Pathway Optimization

- 4.2.6 Need to Quantify Transition Risk Across Supplier, Asset, and Portfolio Decisions

- 4.3 Market Restraints

- 4.3.1 Limited Quality and Availability of Scope 3 and Supplier Activity Data

- 4.3.2 High Integration Complexity With ERP, EHS, and Data-Lake Environments

- 4.3.3 Budget Scrutiny and Slow ROI Realization for Mid-Market Buyers

- 4.3.4 Model Credibility Concerns From Assumption Sensitivity and Audit Scrutiny

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Emissions Forecasting

- 5.3.2 Climate Scenario and Pathway Modeling

- 5.3.3 Climate and Transition Risk Assessment

- 5.3.4 Decarbonization Planning and Abatement Optimization

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Energy and Utilities

- 5.5.3 Oil and Gas

- 5.5.4 Manufacturing and Industrial

- 5.5.5 Transportation and Logistics

- 5.5.6 Technology and Telecommunications

- 5.5.7 Retail and Consumer Goods

- 5.5.8 Other Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Salesforce, Inc.

- 6.4.3 SAP SE

- 6.4.4 IBM Corporation

- 6.4.5 Oracle Corporation

- 6.4.6 Persefoni AI, Inc.

- 6.4.7 Watershed Technology, Inc.

- 6.4.8 Sweep SAS

- 6.4.9 Plan A Earth GmbH

- 6.4.10 Greenly SAS

- 6.4.11 Normative AB

- 6.4.12 Sinai Technologies, Inc.

- 6.4.13 Emitwise Ltd.

- 6.4.14 Position Green AB

- 6.4.15 Gaia Carbon Accounting Ltd.

- 6.4.16 Sphera Solutions, Inc.

- 6.4.17 Enablon North America Corp.

- 6.4.18 Evercomm Singapore Pte. Ltd.

- 6.4.19 Workiva Inc.

- 6.4.20 Terrascope Pte. Ltd.

- 6.4.21 VelocityEHS Holdings, Inc.

- 6.4.22 ClimateView AB

- 6.4.23 Intelex Technologies ULC

- 6.4.24 CarbonChain Ltd.

- 6.4.25 Accacia AI Solutions Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

煤的活性炭市場規模、佔有率和成長分析:按產品類型、活化製程、應用、終端用戶產業和地區分類-2026-2033年產業預測

煤的活性炭市場規模、佔有率和成長分析:按產品類型、活化製程、應用、終端用戶產業和地區分類-2026-2033年產業預測 活性碳產品市場-全球產業規模、佔有率、趨勢、機會和預測:按原料、應用、分銷通路、地區和競爭格局分類,2021-2031年

活性碳產品市場-全球產業規模、佔有率、趨勢、機會和預測:按原料、應用、分銷通路、地區和競爭格局分類,2021-2031年 活性碳市場:2026-2032年全球市場預測(依產品類型、原料、孔徑分佈、製造流程、最終用戶、分銷管道及應用分類)

活性碳市場:2026-2032年全球市場預測(依產品類型、原料、孔徑分佈、製造流程、最終用戶、分銷管道及應用分類) 煤的活性炭:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

煤的活性炭:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 活性碳市場:依產品類型、原料類型、最終用戶和地區分類廢氣吸附淨化系統市場:依技術、吸附劑類型、產品類型、運作模式、流量、應用和最終用戶分類-2026-2032年全球預測竹粒活性碳市場:依原料、製造流程、粒徑、應用及通路-2026-2032年全球預測腐蝕性氣體吸附分析儀市場:依技術、終端用戶產業及通路分類,全球預測(2026-2032年)顆粒活性碳接觸器市場:依應用、階段、最終用戶、操作模式和系統配置分類,全球預測,2026-2032年

活性碳市場:依產品類型、原料類型、最終用戶和地區分類廢氣吸附淨化系統市場:依技術、吸附劑類型、產品類型、運作模式、流量、應用和最終用戶分類-2026-2032年全球預測竹粒活性碳市場:依原料、製造流程、粒徑、應用及通路-2026-2032年全球預測腐蝕性氣體吸附分析儀市場:依技術、終端用戶產業及通路分類,全球預測(2026-2032年)顆粒活性碳接觸器市場:依應用、階段、最終用戶、操作模式和系統配置分類,全球預測,2026-2032年 全球活性碳市場(2026-2036)

全球活性碳市場(2026-2036)