|

市場調查報告書

商品編碼

2062118

煤的活性炭:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Coal Based Activated Carbon - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

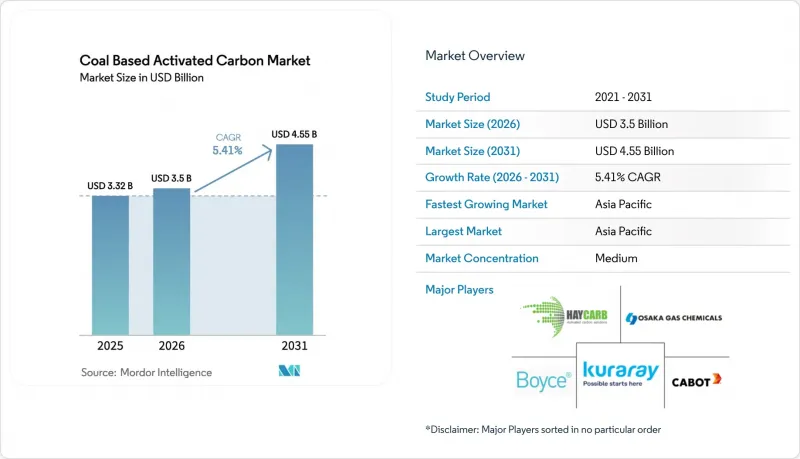

根據 Mordor Intelligence 預測,煤的活性炭市場規模預計將在 2025 年達到 33.2 億美元,2026 年達到 35 億美元,到 2031 年達到 45.5 億美元,2026 年至 2031 年的複合年成長率為 5.41%。

本報告按產品類型(粉末、顆粒、擠出/造粒、珠粒和毛氈)、活化過程(蒸氣、二氧化碳、磷酸、氯化鋅)、應用領域(水/污水、空氣/廢氣、食品飲料、製藥、採礦及其他)和地區(亞太、北美、歐洲及其他)進行細分。市場預測以美元計價。

全球煤的活性炭市場趨勢及洞察

更嚴格的排放氣體法規將促進廢氣淨化。

2024年,美國《大氣污染防治標準》(MATS)和中國的超低排放標準將強制要求在發電廠和水泥廠注入高碘值粉末活性碳。內蒙古和山西煤田附近的供應商已簽訂與動力煤基準價格掛鉤的供應契約,此舉有助於在原物料價格波動的情況下穩定毛利率。在歐盟,生質能衍生活性碳價格高企,而生質能混燒電廠正在迅速轉型以滿足2026年最佳利用技術(BAT)標準,導致先導工廠訂單激增。這些法規正在推動煤衍生活性碳市場的發展,因為營運商必須處理廢氣才能維持其營運許可證。預計即使在負荷率波動的情況下,硫污染極低且吸附速率快的設備也能帶來可觀的利潤。

基於 PFAS 因應措施的飲用水水源產業超微量標準

2024年4月,美國環保署(EPA)將六種PFAS化合物的最大過濾限值(MCL)設定為4 ppt。同時,EPA也指定煤基顆粒活性碳為處理總PFAS濃度低於100 ppt水體的「最佳可行可用技術(BAT)」。此後,為數百萬美國居民提供服務的供水事業紛紛簽訂「照付不議」的回收協議,以避免因掩埋廢棄吸附劑而產生的責任。KURARAY CO. LTD.預測,到2030年,美國市場將大幅擴張。為了抓住這一機遇,該公司計劃透過加強其新產品生產和回收能力來確保更大的市場佔有率。同時,印度提出了一項與歐盟標準相符的PFAS法規草案,顯示南亞地區的需求正在成長。這些發展趨勢促使煤的活性炭市場轉向服務導向收入模式轉變,垂直整合的供應商從中受益。

煤炭原料價格波動與物流風險

2024年,海上煤炭價格的季度波動受到天氣狀況、印尼出口配額和中國進口政策等因素的影響。嚴重依賴進口的歐洲生產商由於運費飆升,面臨大幅上漲的煤炭裝卸成本。受短期採購合約約束的小規模生產商利潤率承壓,因為原料價格的飆升超過了合約重新定價帶來的收益。相較之下,在山西省擁有自有礦山的生產商以及在美國伊利諾伊盆地擁有長期承購合約的生產商,其息稅折舊攤銷EBITDA獲利率)高於以現貨價格採購的生產商。同時,儘管洗煤廠努力提高煤漿質量,使得活性碳的碘值範圍有所限制,但這一限制使其應用僅限於低價值的染料去除市場,從而削弱了煤的活性炭領域的潛力。

細分市場分析

2025年,顆粒狀活性碳佔了41.12%的市場佔有率,佔據主導地位。然而,預測顯示,在2026年至2031年的預測期內,擠壓成型和造粒狀活性碳將以5.89%的複合年成長率強勁成長,超過所有其他類別。在化學和煉油領域,高能耗的VOC洗滌器正逐漸轉向使用擠壓成型的顆粒狀活性碳。這些顆粒狀活性碳不僅降低了風機能耗,還顯著降低了運行成本,從而推動了圓柱形介質規格的普及。

大阪瓦斯化學公司透過投入運作新的壓機設備,鞏固了其在日本煤的活性炭市場的地位。加之黏合劑技術的進步提高了BET比表面積,擠壓成型產品的銷售量正穩定成長。粉狀活性碳在緊急水淨化和製藥精煉領域發揮至關重要的作用,而珠狀和氈狀活性碳則滿足醫療設備等特定應用的需求。然而,萬噸級生產線所需的巨額資本投入限制了擠壓成型製程的應用,使其僅限於財務狀況良好的公司,從而導致煤的活性炭市場該細分領域的集中度適中。

區域分析

2025年,亞太地區在全球市場佔據主導地位,市佔率高達43.22%,預計在2026年至2031年的預測期內將維持5.96%的強勁複合年成長率。儘管中國仍然是主要生產國,但已轉向進口,以遠高於平均出口價格的價格購買高品質產品。這一趨勢凸顯了煤的活性炭市場對特種等級產品的強勁需求和穩健發展。在印度,安得拉邦和奧裡薩邦的產量水準以及物流成本的降低,為提高區域自給率鋪平了道路。同時,菲律賓憑藉其混合原料的成本優勢,成為日本和韓國買家的理想選擇。

北美,尤其是美國,在2025年的需求趨勢中扮演了至關重要的角色,這主要歸功於嚴格的PFAS法規和汞排放限制,這些法規和限制促進了回收合約的成長。加拿大與油砂相關的水處理流程以及墨西哥蓬勃發展的食品加工業進一步豐富了區域趨勢。歐洲保持了較大的市場佔有率,但面臨著煤炭價格飆升和ESG資金籌措壓力等挑戰。這些因素迫使生產商轉向使用回收窯爐,增加了可再生動力來源的使用。南美洲市場穩定成長,這得歸功於秘魯和智利的黃金產量。中東和非洲雖然在全球市場佔有率不大,但在海水淡化預處理和西非黃金專案方面發展了利基市場。這些複雜的區域趨勢共同構成了煤的活性炭市場均衡的全球成長軌跡。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 更嚴格的排放氣體法規將促進廢氣淨化。

- 符合 PFAS 標準的供水事業超微量標準

- 金礦氰化浸出和回收製程激增。

- 水泥窯與煉鋼窯中碳回收吸附劑的應用

- 「再生即服務」經營模式的興起

- 市場限制因素

- 煤炭原料價格波動與物流風險

- 與生質能衍生活性碳的競爭

- 受 ESG(環境、社會和治理)因素驅動,資本正從煤炭供應鏈撤資。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 粉末

- 顆粒狀

- 擠壓/造粒

- 珠子和毛氈

- 逐一過程的啟動過程

- 蒸氣

- 二氧化碳

- 磷酸

- 氯化鋅

- 透過使用

- 水和污水

- 空氣和廢氣

- 食品/飲料

- 藥品和醫療應用

- 採礦(黃金回收)

- 其他用途(工業溶劑回收、沼氣及氫氣純化等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Active Char Pvt. Ltd.

- Boyce Carbon Ltd

- Cabot Corporation

- Carbon Activated Corporation

- Carbotech

- Donau Carbon US LLC

- Eurocarb Products Limited

- Haycarb PLC

- Jacobi Carbons Group

- KURARAY CO., LTD.

- KUREHA CORPORATION

- Osaka Gas Chemicals

第7章 市場機會與未來展望

According to Mordor Intelligence, the coal-Based activated carbon market size is projected to be USD 3.32 billion in 2025, USD 3.5 billion in 2026, and reach USD 4.55 billion by 2031, growing at a CAGR of 5.41% from 2026 to 2031.

This report is Segmented by Product Type (Powdered, Granular, Extruded/Pelletized, and Bead and Felt), Activation Process (Steam, Carbon Dioxide, Phosphoric Acid, and Zinc Chloride), Application (Water/Wastewater, Air/Flue-Gas, Food/Beverage, Pharmaceutical, Mining, and Other), and Geography (Asia-Pacific, North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Coal Based Activated Carbon Market Trends and Insights

Stricter Air-Emission Norms Boosting Flue-Gas Purification

In 2024, the U.S. MATS rule and China's ultra-low-emission standards mandate power and cement plants to inject high-iodine-number powdered activated carbon. Suppliers near the Inner Mongolia and Shanxi coal basins are securing supply contracts tied to the thermal-coal benchmarks, a move that stabilizes gross margins amid feedstock fluctuations. In the EU, while biomass-based carbons command a premium, biomass co-firing plants are racing to meet the 2026 BAT conclusions, resulting in a surge in pilot orders. These regulations bolster the coal-based activated carbon market, as operators treat flue gas to maintain their operational licenses. Facilities that ensure minimal sulfur bleed-through and rapid adsorption kinetics stand to gain significantly, even with fluctuating load factors.

PFAS-Driven Ultra-Trace Standards for Potable-Water Utilities

In April 2024, the EPA set Maximum Contaminant Levels for six PFAS compounds at 4 ppt. They also identified coal-based granular activated carbon as the Best Available Technology for treating waters with total PFAS levels below 100 ppt. In response, utilities serving millions of U.S. residents entered into take-or-pay regeneration contracts, avoiding landfill liabilities for spent sorbent. Kuraray had anticipated the U.S. market opportunity to grow significantly by 2030. To capitalize, the company enhanced both virgin and reactivation capacities, aiming to secure a substantial share of that market. Meanwhile, India proposed a draft PFAS limit in line with EU Standards, signaling increased demand in South-Asia. These developments have driven the coal-based activated carbon market toward a service-oriented revenue model, favoring vertically integrated suppliers.

Price Volatility and Logistics Risk in Coal Feedstock

In 2024, quarterly fluctuations in seaborne coal prices were influenced by factors such as weather conditions, Indonesian export quotas, and Chinese import policies. European producers, who rely heavily on imports, are seeing a significant increase in their landed coal costs due to rising freight charges. Smaller producers, bound by short-term procurement contracts, are experiencing margin compression as spikes in feedstock prices outpace the repricing of their contracts. In contrast, producers with captive mines in Shanxi or long-term offtakes in the U.S. Illinois Basin are enjoying higher EBITDA margins than those buying at spot prices. While efforts to enhance coal fines from wash-plants have led to carbons with iodine numbers in a limited range, this constraint restricts their use to low-value dye-removal markets and diminishes their potential in the coal-based activated carbon sector.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Gold-Ore Cyanidation Recovery Circuits

- Adoption of Carbon-Capture Sorbents for Cement and Steel Kilns

- Competition from Biomass-Based Activated Carbon

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the market saw granulated activated carbon holding a dominant 41.12% share. However, projections indicate that during the forecast period of 2026-2031, both extruded and pelletized forms are poised to expand at a vigorous 5.89% CAGR, outpacing all other categories. Within the chemicals and refining sectors, energy-intensive VOC scrubbers are increasingly leaning towards extruded pellets. These pellets not only reduce fan energy consumption but also lead to substantial savings in operating expenses, prompting a shift in specifications toward cylindrical media.

Osaka Gas Chemicals has bolstered Japan's coal-based activated carbon market by activating new presses. This, combined with binder advancements that enhance BET surface areas, has fueled steady growth for extruded products. While powdered forms play a pivotal role in emergency water remediation and pharmaceutical purification, bead and felt derivatives cater to niche applications in medical devices. However, the high capital investment required for a 10,000-ton line confines extrusion to financially robust players, resulting in a moderate concentration within this segment of the coal-based activated carbon market.

Geography Analysis

In 2025, the Asia-Pacific region dominated the global stage, capturing a notable 43.22% share of the global market and charting a robust projected CAGR of 5.96% for the forecast period 2026-2031. China, while a significant producer, turned to imports, acquiring premium products at prices considerably above the average export rates. This trend highlighted the resilience and demand for specialty grades in the coal-based activated carbon market. In India, production levels, combined with reduced logistics costs in Andhra Pradesh and Odisha, paved the way for enhanced regional self-sufficiency. Meanwhile, the Philippines showcased the cost benefits of blended feedstock, making it an attractive proposition for buyers in Japan and South Korea.

North America, particularly the United States, played a pivotal role in the 2025 demand landscape, largely influenced by stringent PFAS regulations and mercury limits that leaned towards regeneration contracts. Canada's oil-sands water circuits and Mexico's vibrant food processing industry further enriched the regional dynamics. Europe, while holding a significant market share, faced challenges with rising coal prices and ESG capital pressures. These factors nudged producers to pivot towards reactivation kilns, increasingly powered by renewable energy. In South America, buoyed by gold outputs from Peru and Chile, the market witnessed steady growth. The Middle-East and Africa, though modest in their global share, carved out niches in desalination pre-treatment and gold projects in West Africa. These intricate regional dynamics collectively shaped a balanced global growth trajectory for the coal-based activated carbon market.

- Active Char Pvt. Ltd.

- Boyce Carbon Ltd

- Cabot Corporation

- Carbon Activated Corporation

- Carbotech

- Donau Carbon US LLC

- Eurocarb Products Limited

- Haycarb PLC

- Jacobi Carbons Group

- KURARAY CO., LTD.

- KUREHA CORPORATION

- Osaka Gas Chemicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter air-emission norms boosting flue-gas purification

- 4.2.2 PFAS-driven ultra-trace standards for potable-water utilities

- 4.2.3 Surge in gold-ore cyanidation recovery circuits

- 4.2.4 Adoption of carbon-capture sorbents for cement and steel kilns

- 4.2.5 Emergence of "regeneration-as-a-service" business models

- 4.3 Market Restraints

- 4.3.1 Price volatility and logistics risk in coal feedstock

- 4.3.2 Competition from biomass-based activated carbon

- 4.3.3 ESG-driven capital withdrawal from coal supply chains

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Powdered Activated Carbon (PAC)

- 5.1.2 Granular Activated Carbon (GAC)

- 5.1.3 Extruded/Pelletized Carbon Block

- 5.1.4 Bead and Felt Activated Carbon

- 5.2 By Activation Process

- 5.2.1 Steam Activation

- 5.2.2 Carbon Dioxide Activation

- 5.2.3 Phosphoric Acid

- 5.2.4 Zinc Chloride

- 5.3 By Application

- 5.3.1 Water and Wastewater Treatment

- 5.3.2 Air and Flue-Gas Purification

- 5.3.3 Food and Beverage Processing

- 5.3.4 Pharmaceutical and Medical Uses

- 5.3.5 Mining (Gold Recovery)

- 5.3.6 Other Applications (Industrial Solvent Recovery, Biogas and Hydrogen Purification, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Active Char Pvt. Ltd.

- 6.4.2 Boyce Carbon Ltd

- 6.4.3 Cabot Corporation

- 6.4.4 Carbon Activated Corporation

- 6.4.5 Carbotech

- 6.4.6 Donau Carbon US LLC

- 6.4.7 Eurocarb Products Limited

- 6.4.8 Haycarb PLC

- 6.4.9 Jacobi Carbons Group

- 6.4.10 KURARAY CO., LTD.

- 6.4.11 KUREHA CORPORATION

- 6.4.12 Osaka Gas Chemicals

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

煤的活性炭市場規模、佔有率和成長分析:按產品類型、活化製程、應用、終端用戶產業和地區分類-2026-2033年產業預測

煤的活性炭市場規模、佔有率和成長分析:按產品類型、活化製程、應用、終端用戶產業和地區分類-2026-2033年產業預測 活性碳產品市場-全球產業規模、佔有率、趨勢、機會和預測:按原料、應用、分銷通路、地區和競爭格局分類,2021-2031年

活性碳產品市場-全球產業規模、佔有率、趨勢、機會和預測:按原料、應用、分銷通路、地區和競爭格局分類,2021-2031年 活性碳市場:2026-2032年全球市場預測(依產品類型、原料、孔徑分佈、製造流程、最終用戶、分銷管道及應用分類)

活性碳市場:2026-2032年全球市場預測(依產品類型、原料、孔徑分佈、製造流程、最終用戶、分銷管道及應用分類) 活性碳市場:依產品類型、原料類型、最終用戶和地區分類廢氣吸附淨化系統市場:依技術、吸附劑類型、產品類型、運作模式、流量、應用和最終用戶分類-2026-2032年全球預測竹粒活性碳市場:依原料、製造流程、粒徑、應用及通路-2026-2032年全球預測腐蝕性氣體吸附分析儀市場:依技術、終端用戶產業及通路分類,全球預測(2026-2032年)顆粒活性碳接觸器市場:依應用、階段、最終用戶、操作模式和系統配置分類,全球預測,2026-2032年

活性碳市場:依產品類型、原料類型、最終用戶和地區分類廢氣吸附淨化系統市場:依技術、吸附劑類型、產品類型、運作模式、流量、應用和最終用戶分類-2026-2032年全球預測竹粒活性碳市場:依原料、製造流程、粒徑、應用及通路-2026-2032年全球預測腐蝕性氣體吸附分析儀市場:依技術、終端用戶產業及通路分類,全球預測(2026-2032年)顆粒活性碳接觸器市場:依應用、階段、最終用戶、操作模式和系統配置分類,全球預測,2026-2032年 全球活性碳市場(2026-2036)

全球活性碳市場(2026-2036) 擠壓活性碳市場規模、佔有率和成長分析:按類型、功能、物理形態、包裝類型、應用、最終用戶和地區分類-2026-2033年產業預測

擠壓活性碳市場規模、佔有率和成長分析:按類型、功能、物理形態、包裝類型、應用、最終用戶和地區分類-2026-2033年產業預測